In the accounting of the insurance company «AAA Insurance» all operations related to the implementation of financial and economic activity, conventionally divided into operations on insurance activities and operations that are typical of any commercial organization. This approach has led to the application of the Standard Chart of Accounts with additional introduction of special accounts intended to account for the directly to insurance business operations. Insurance companies in relation to their needs and peculiarities of activity, develop Chart of Accounts on the basis of the Standard Chart of Accounts for the individual subjects of the financial market of the Republic of Kazakhstan /1/.

In the practice of the company “AAA Insurance” insurance operations are divided according to the form of holding – voluntary and compulsory insurance. In the accounting, reinsurance operations are divided into incoming and outgoing reinsurance.

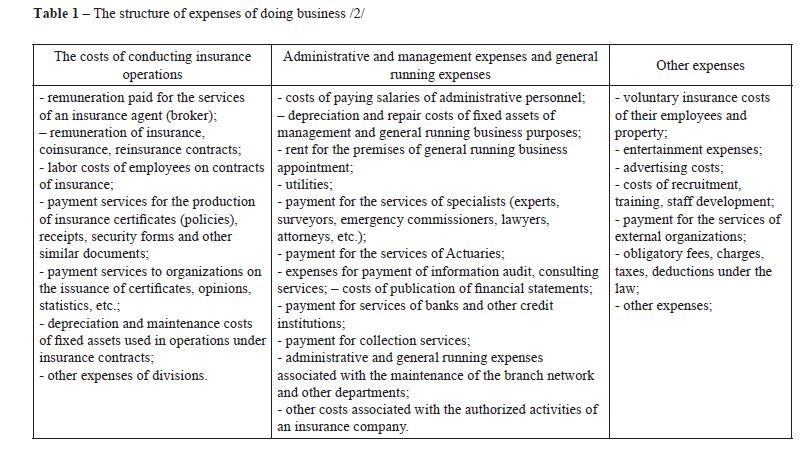

The organization and conduct of insurance business are accompanied by corresponding costs, which are called the cost of doing business. This group of expenses for their share in the total costs of the insurance company is one of the leading places.

The costs of doing business are multi-element costs that include comprehensive article:

- expenses on conducting insurance business (costs of conclusion, management and execution of contracts of insurance, coinsurance and reinsurance);

- administrative and management expenses and general running expenses;

- other expenses;

The structure of expenses of doing business in the “AAA Insurance” company is presented in Table 1.

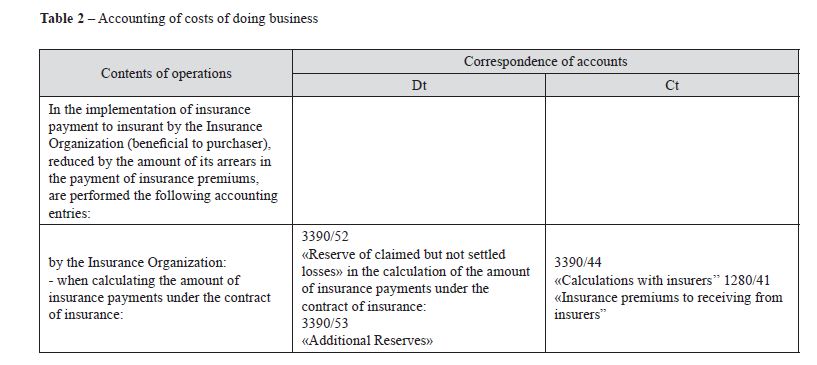

To account the cost of doing business using active accounts 7210 «Administrative expenses» 7470/40 «The costs associated with the insurance (reinsurance) activity», 1620/03 «Other expenses of future periods» and the liability account 5460 «Other reserves».

Account 7210 «Administrative expenses» is intended to account for the amount of administrative expenses that are not related to the production process of the organization, as well as the realization of finished products (goods and services) of the organization. Account 7470/40, «The costs of insurance (reinsurance) activity» is intended to account for the amount of expenses of the insurance organization in the form of insurance payments at insured event approach under a contract of insurance.

Table 1 – The structure of expenses of doing business /2/

Also, to account for the cost of the insurance companies are used separately open accounts:

7470/42 “Expenses for insurance payments for reinsurance”;

7470/43 “Expenses of Claims handling”; 7470/44 “Expenditure on compensation to the reinsurer by recourse claims”;

7470/45 “Expenditure on payment the commission fee of reinsurance”;

7470/46 “The cost of making mandatory con- tributions to the fund of guarantee insurance pay- ments”;

7470/47 “Expenditure on payment of extraor- dinary contributions to the fund of guarantee insur- ance payments”;

7470/48 “Costs for services of insurance bro- kers”;

7470/49 “Costs for services of Actuaries’’; 7470/50 «Other expenses»;

Administrative and management, general running and other expenses are usually defined on the basis of pre-compiled total estimate. In order to control these expenses allocation on general estimate can be provided separate analytical accounts to the account 7210 “Administrative expenses” to reflect the actual costs for each budget item.

Administrative and management, general running and other expenses relate to indirect costs and by the calculated manner distribute to specific types of insurance and insurance contracts. In this case, indirect costs firstly collected in a separate sub-account 7210, then performed their distribution. Direct costs, the amount of collected insurance gross premiums can be including as a base indicator of allocation of indirect costs. The method of allocation of indirect costs should be fixed in the accounting policies of the organization.

In this case, the administrative and management, general running costs and other expenses that are not referred to the relevant types of insurance, recorded on the account 7210, without distribution in the total amount are shown in the corresponding line of the profit and loss account (Form N-2 insurer).

At the end of the reporting period, the amount of the actual costs of doing business is recorded in the income result, which are credited to 7210 “Administrative expenses” in correspondence with the debit of the account 5610 “Total profit (total loss).”

Expenses incurred during the reporting period (month), but relating to other periods are considered on account 1620/03 “Other expenses of future periods”. The costs of irregularly produced repair of fixed assets in one year, advertising costs, fees to obtain licenses for the right to work, one-time payments under license agreements for the right to use intangible assets, the cost of purchasing software packages for personal computers and other costs are recorded on this account.

Costs considered on account 1620/03 “Other expenses of future periods” are charged to the debit of the account 7210 “Administrative expenses” in the proportion relating to the accounting period (month).

The analytical account of the account 7210 “Administrative expenses” is conducted by type of expenditure. In order to include future expenses evenly in the costs on business conducting of the reporting period, the insurance company makes provisions for holiday pay workers; for the payment of annual compensation for years of service; for the payment of royalties under the results for the year, for the repair of fixed assets, for warranty repair and warranty covering hardware and other contingencies costs stipulated by the regulations.

Reservation of certain amounts are credited to 7440, “The costs of establishing a reserve and write off bad requirements” in correspondence with the accounts for cost accounting and settlement. Actual expenses, on which previously has been established reserve, are related to the debit account 7440 in correspondence with the appropriate accounts for the cost accounting and settlement.

The correctness of establishment and using of amounts on a particular reserve is checked periodically (and at the end of the year necessarily) according to estimates, calculations, etc. and, if necessary, is corrected.

The basis for the implementation of the accounting entries on accounting costs of doing business of insurance operations in the “AAA Insurance” company are the following:

- accounts;

- payment order, cash voucher;

- bank statement;

- expendable cash order;

- agency agreement (contract order);

- report of an insurance agent (insurance broker);

- accounting statement-calculation;

- acts of completed works;

- limit-fencing cards, requirements;

- advance report;

- order of the Head.

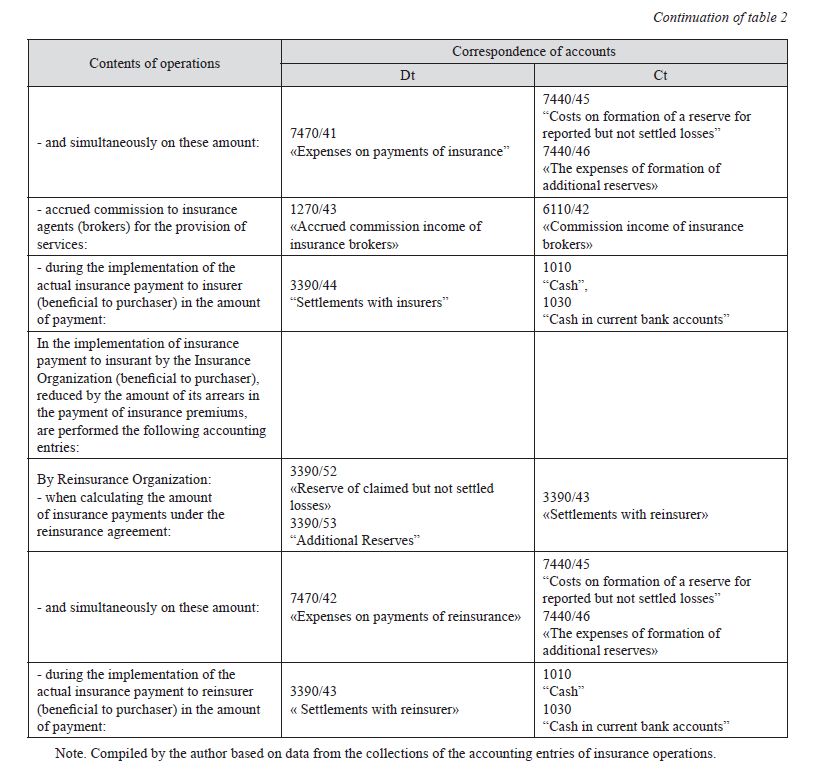

Table 2 – gives the example of correspondence accounts of the costs of doing business in insurance operations in the “AAA Insurance” company, which confirm the operations.

Table 2 – Accounting of costs of doing business

Note. Compiled by the author based on data from the collections of the accounting entries of insurance operations.

“AAA Insurance” company in the formation of expenses from ordinary activities makes their classification by the follow cost components:

- material costs;

- labor costs;

- social contributions;

- depreciation;

- other costs.

This classification describes costs of the insurance company at the aggregate level in the context of the main elements. Information on the main elements of cost appears in the appendix to the balance sheet of insurance organization (Form N 5-insurer). It should be mentioned that cost accounting items are not kept currently, and for the purposes of preparation of financial statements, this information is generated by calculation.

References

- Tipovoj plan schetov buhgalterskogo ucheta dlja otdel’nyh sub#ektov finansovogo rynka

- Savchenko O. S. Bol’shaja kniga buhgaltera strahovoj kompanii. – M.: Reglament, 2006 g. – 230s.