The article describes the main stages of the transition to international financial reporting standards of domestic enterprises. Also it disclosed in detail the transition to international accounting standards for small and medium-sized businesses. The complete description of the definition of small and medium-sized businesses from the perspective of the Committee on International Financial Reporting Standards and the law on private enterprise is given. The main differences of IFRS for SMEs as compared with full IFRS are analysed. The advantages and disadvantages of international accounting standards for small and medium-sized businesses are showed.

Reforming the system of accounting and financial reporting in the Republic of Kazakhstan continues for more than twenty years. The initial stage of the reform has coincided with the adoption of the Decree of the President of the Republic of Kazakhstan having the force of the Law «On Accounting» in 1995.

The introduction in 1996 of accounting standards of the Republic of Kazakhstan developed on the basis of international accounting standards were the beginning of the transition to international financial reporting standards.

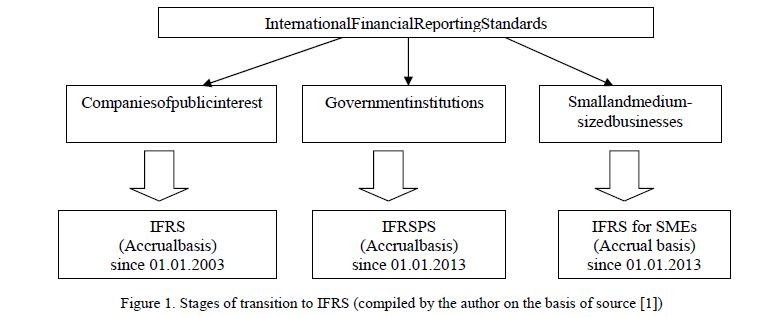

Second and most important step in this process was the addition to this Decree of Article 2–1 «International Financial Reporting Standards in the Republic of Kazakhstan» in 2002. According to this article, IFRS financial statements should be provided by the organizations in the following order: financial institutions make up from January, 1st, 2003, joint-stock companies from January, 1st, 2005, other organizations from January, 1st, 2006 (except public institutions).

The next stage of this reform in the Republic of Kazakhstan is the transition to IFRS of government agencies (public sector’s IFRS) from January, 1st, 2013 and the SMB (IFRS for SMB) from January 1st, 2013 (Fig.).

Figure 1. Stages of transition to IFRS (compiled by the author on the basis of source [1])

The IFRS council has begun working on a standard for small and medium-sized businesses in 2005. In July 2009, the International Accounting Standards Board has issued International Financial Reporting Standard for Small and Medium Business. The IFRS for SMBis intended to apply to general purpose financial statements of companies that are not obliged to submit the financial statements to a wide range of users. There are 35 sections (standards), IFRS for small and medium-sized businesses.

Companies that are required to submit the financial statements to a wide range of users, and therefore not included in the scope of the IFRS for SMB, include businesses whose debt or equity instruments are traded in a public market, banks, credit institutions, brokers / dealers in securities transactions, mutual funds and insurance companies. In many countries, companies that are not obliged to submit the financial statements to a wide range of users are referred to by various terms, including the terms «private enterprises» and «enterprises that are not required to submit the financial statements to a wide range of users» [2].

According to the terminology of a standard for SMB, the small and medium enterprises mean companies whose equity and debt securities are not traded on the open market, and are not required to submit the financial statements to a wide range of users.

At the same time banks, insurance companies, mutual funds, brokers and dealers cannot be small and medium-sized businesses.

The term «small and medium business» is widely recognized and used throughout the world, although in many literatures their own definitions of the term for a wide range of purposes were developed, including the establishment of obligations on financial statements. Such national or regional definitions often include quantified criteria based on revenue, assets, serving or other factors. Often the term is used to refer to very small companies or includes such enterprises, regardless of whether they produce general purpose financial statements for external users.

Law of the Republic of Kazakhstan on private enterprise has the following concept of subjects of small business [3].

Article 6. Subjects of private enterprise

- Small businesses (enterprises) are individual entrepreneurs without a legal entity and legal entities engaged in private business, with the average annual number of employees not more than a hundred people, and the average annual income of not more than 300,000 monthly calculation index (MCI) established by the law on the republican budget and applicable as of January, 1st of the corresponding financial year (MCI for 2016 is 2121 tenge).

- Medium businesses (enterprises) are individual entrepreneurs without a legal entity and legal entities engaged in private business not related to small and large businesses in accordance with paragraphs 5 and 9 of this

- Large businesses (enterprises) are individual entrepreneurs without a legal entity and legal entities engaged in private business and meeting one or two of the following criteria: the average number of employees more than two hundred and fifty people, and (or) average annual income of over 3 000 000 MCI, established by the law on the national budget and applicable as of January 1st of the corresponding fiscal

The IFRS council attached great importance to the development of this standard. The main objective of the development of this standard was to develop a set of high quality accounting standards that:

- would have been collected in a single document;

- would have no direct references to the full set of IFRS, i.e. would be autonomous from it;

- could be used by experts and auditors working in small and medium-sized enterprises with the corresponding qualification level;

- would not require significant investment in the development of a financial statement

The objective of general purpose financial statements of small and medium business is to provide information about the financial position, results of operations and cash flows of the enterprise that is useful in making economic decisions for wide range of users who cannot require the submission of financial statements prepared in accordance with their specific information requirements [4].

In establishing standards for the form and content of general purpose financial statements, the needs of users of financial statements get the paramount importance.

The main groups of external users of financial statements of small and medium-sized businesses include:

- financial institutions providing loans to small and medium-sized businesses;

- customers carrying out trade with small and medium-sized businesses who use the financial statements of small and medium-sized businesses to make decisions about loans and pricing;

- credit rating agencies and other institutions that use the financial statements of small and mediumsized businesses for the assessment of small and medium-sized

- customers of small and medium-sized businesses who use the financial statements of small and medium-sized businesses to decide whether to maintain a business relationship with them or not;

- shareholders of small and medium-sized businesses that are not simultaneously managers of these enterprises.

We believe that users of financial statements of small and medium-sized businesses may be less interested in some information provided in general purpose financial statements prepared in accordance with full version of IFRS than users of financial statements of companies whose securities are registered for treatment in the open securities markets and are required to submit financial statements to a wide range of users for different reasons.

For example, users of financial statements of small and medium-sized businesses may be more interested in short-term cash flows, liquidity, benefits of the balance sheet and interest coverage, as well as historical trends of profit or loss and interest coverage, than information intended to make predictions in long-term cash flows of the enterprise, its profit or loss and cost.

However, users of financial statements of small and medium-sized businesses may need some information, which is usually not in the financial statements of the company whose debt or equity instruments are traded in an open securities market. For example, as an alternative to open capital markets for small and medium-sized businesses they often obtain capital from shareholders, CEOs and suppliers, while shareholders and CEOs often provide personal assets as collateral to small and medium businesses so they can get financing from a bank.

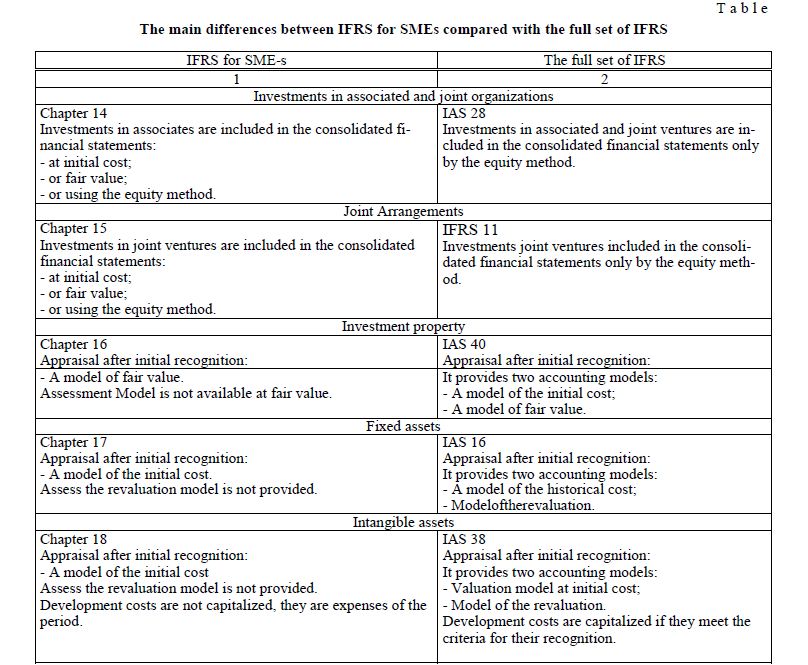

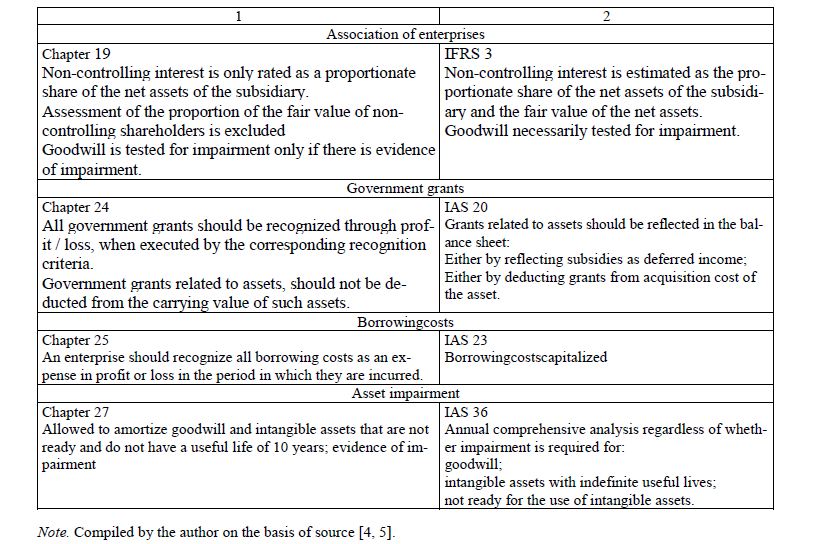

The nature and extent of the differences between full IFRS and the IFRS for SMB are based on user needs and analyzes of the ratio «cost — benefit». In practice, the benefits of accounting standards of reporting in different companies vary mostly depending on the nature, number and information needs of users of their financial statements. Related costs are not significantly different. Therefore, IFRS council came to the conclusion that the optimal ratio of «cost — benefit» should be evaluated with respect to the information needs of users of financial statements. The main differences between IFRS for SMB and full IFRSs are presented in Table.

The main differences between IFRS for SMEs compared with the full set of IFRS

Note. Compiled by the author on the basis of source [4, 5].

Some standards of full IFRSs excluded from consideration. This includes standards such as IFRS (IAS) 33 «Earnings per Share», IFRS (IAS) 34 «Interim Financial Statements», IFRS (IFRS) 4 «Insurance Agreement», IFRS (IFRS) 5 «Long-term assets held for sale» IFRS (IFRS) 8 «Segment reporting», i.e. those standards that are related to the company whose debt or equity instruments are traded in anopen securities market.

Also, some of the standards of full IFRS are combined into one standard. For example, IFRS (IAS) 41 «Agriculture» and IFRS (IFRS) 6 «Exploration and Evaluation of Mineral Resources» are combined into Section 34 «Specialized work». IFRS (IAS) 18 «Revenue» and IFRS (IAS) 11 «Construction Treaties» are combined into Section 23 «Revenue».

The standards relating to financial instruments are divided into two standards: Section 11 «Basic Financial Instruments» and Section 12 «Other Financial Instruments». In full IFRS they are regulated by the following standards: IFRS (IAS) 32 «Financial Instruments — Presentation», IFRS (IAS) 39 « Financial Instruments — recognition and Measurement «, IFRS (IFRS) 7 «Financial Instruments — disclosures «and IFRS (IFRS) 9 «Financial Instruments».

In addition, IFRS for SMB contains a number of simplifications, which will save money for the preparation of reports. The following advantages of the standard can also be set aside for small and medium-sized enterprises [6]:

- Access to For those companies that apply international accounting standards for SMBan access to loan resources can be simplified. In particular, it will be easier to obtain financing on the basis of the financial statements of the company, an access to foreign loan resources appears, a procedure of granting loans for the purchase of fixed assets and working capital simplifies.

- The ability to attract foreign financial institutions as

- Increase of professional level of employees. The IFRS council believes that adoption of international financial reporting standards for small and medium-sized businesses is the first step to the most common and modern The use of international financial reporting standards for small and medium-sized businesses will help raise the level of education of employees in small companies, including raising the level of financial literacy.

- Implementation of the international audit. A company while preparing the financial statements in accordance with International Financial Reporting Standards for Small and Medium Enterprises is able to hold an international audit of its financial This increases the internal control in a company, creates added value of financial statements of the firm itself.

- Ability to abandon the national standards. Companies in some countries during the preparation of financial statements in accordance with IFRS for small and medium-sized businesses cannot apply the requirements of reporting according to national standards. This reduces the costs of transformation of financial reporting to international reporting as in the application of national

- Stable rules of Many accountants at large corporations have faced the inconvenience of constantly changing application of old and the introduction of new standards for a full set of IFRS. For the convenience of small and medium businesses IFRS for SMB cannot be part of the frequent evaluation of its assets and liabilities in full IFRS.

However, the IFRS for SMB has a number of disadvantages:

- The implementation of international financial reporting standards for small and medium-sized businesses is very expensive and can be compared to the cost of implementation of the full set of IFRS;

- Any small and medium business can become public, e. release issued shares, bonds, bills of exchange, then the company will have to prepare financial statements in accordance with the full set of IFRS;

- It is not clear whether the potential investors trust such statements, which is made in accordance with IFRS for SMB. After all, a large number of disclosures in the financial statements allows investors to make sound economic

Thus, international financial reporting standards for small and medium business is the most effective in terms of cost and efficient approach to private companies, which plan to prepare financial statements to its shareholders, banks and other interested parties.

The IFRS for SMB will make a significant contribution to the unification of the accounting principles in the world. Given that small and medium can be called more than 90 % of all companies in the world, the standards for small and medium business will be widely disseminated in the near future. In addition, the use of the IFRS for SMB provides an important opportunity for our small and medium-sized businesses to attract foreign investment.

References

- Accounting and financial reporting Act of the Republic of Kazakhstan, 2007, 324–11, [ER]. Access mode: http://www.grossbuh.kz/information/show/id/75.html.

- CIFRS Foundation: Training Material for the IFRS for SMEs, [ER]. Access mode: http://www.ifrs.org.

- Private entrepreneurship Act of the Republic of Kazakhstan « (with alterations and amendments on 08.2015), [ER]. Access mode: http: //online.zakon.kz.

- International Financial Reporting Standards for Small and Medium Business, [ER]. Access mode: http://www.minfin.gov.kz.

- International Financial Reporting Standards, [ER]. Access mode: http://www.minfin.gov.kz.

- Moderov S. IFRS in practice, 2011,