Any government aims to produce an effective economics and enhance the quality of economic decisions no importance of political structure society achieves. Based on the credit policy that made by banks they take an important part to in establishment. The role of credit policy consists in defining foreground orientation of development and refinement of bank’s activity in accumulation and investment of credit resources, maturation of the credit process and generation of its efficiency. This article reviews current state of credit policy of the second-tier banks of the Republic of Kazakhstan and routes for the modernization in contemporary economic situation. There is an overview for the transfer of the second-tier banks to Basel III standards: requirements for the minimal banks’ funds, non-performing loansand prudential normative. Furthermore, authors represent the structure of loan portfolio and banking sector’s funding in the Republic of Kazakhstan.

Permanent glance at economic politics of the countries and economical and financial changes in countries, regions and globally is done by International Monetary Fund (IMF) to bear stability and prevent crises of international financial-monetary system. On the 12th of November IMF members with a head of Hossein Samii took a five-day visit to the Republic of Kazakhstan to analyze situation and overview measures assumed in economic and financial sectors. By the end of call a determination has been made by the members of IMF, the delegates stated that due to crucial and continual shocks, i.e. oil prices plummet, likewise decline in Russia and China’s economic activity, Kazakhstan’s economic growth paces diminished since 2014.

Moreover, the financial conditions became severe, particularly leaving individual sector without a significant loans. It’s estimated, that flexible rate of tenge, which tumble in exchange rate of tenge to dollar by 40 %, affirmed on August the 20th, will allow to minimize external disbalance, yet it will spread the inflation out of the aimed spectrum of 6–8 % and may have a negative impact on the individual sector’s position.

Despite the difficult economic situation, the National Bank of the Republic of Kazakhstan (the NB RK) has taken important steps to modernize the bases of monetary policy and monetary operations. In particular, the decision adopted, in August, 2015 about the transition to a floating exchange rate of tenge and with the introduction of a new key interest rate (base rate), serving as the new «anchor» of monetary policy, the process of modernization of the basics of monetary policy was launched in September. Subsequent minimization of currency interventions of the National Bank of Kazakhstan, starting November 5, allowed to adapt better to shocks and provided tenge’s rate fixing in accordance with the fundamental factors.

Additionally, in October 2015, the National Bank of Kazakhstan had adjusted the program of transition to Basel III by preserving minimum requirements for the equity capital adequacy during 2016, including buffers of equity capital at the level as in 2015. There was a consideration given to increase the transition to Basel III standards by 2021 and reduce targeted value of capital adequacy from 12 % to 10.5 %.

Debates were opened on the basis of transition to the Basel III standard, with main matter, if it should be prolonged by 2021 and descension of targeted value of capital adequacy from 12 % to 10.5 %.

Since 2017 the National Bank will introduce supervisory allowance (capital add-on) in addition to the value of capital adequacy on the account of practice and rules of the European Union [1].

A new international standard will be introduced for the concept of «non-performing loan» since 2017. The definition of «non-performing loan» will be expanded by including restructured loans. At the same time there is no consensus among Kazakhstan bankers about what is classified as non-performing loans, and whether to include restructured loans to the unemployed because there is no universal method for restructuring of loans, each bank determines the issue itself. Therefore, once Kazakhstan makes all efforts to move closer to international standards of bank management, wouldn’t it be better to take the experience of developing countries in the definition of non-performing loans and uniform conditions for loan restructuring. In the next two years indicator of non-performing loans will continue to serve as an indicator of early response, and in 2018 will serve the role of the prudential standard. A proposal for a postponement of the decline period in the share of non-performing loans to less than 10 % by 2018 was approved [2].

Earlier it was planned that Kazakhstan banks over next five years will be proceeding to the new requirements of Basel III — until 2019. In this regard, the National Bank proposed to raise the minimum capital of banks from 10 billion tenge (274 / $1) to 100 billion tenge.

National Bank of Kazakhstan has set the thresholds on the share of non-performing loans in the loan portfolio of commercial banks — from January 1, 2015 — no more than 15 %, from January 1, 2016 — 10 %.

Basel III has been designed to address the deficiencies in financial regulation revealed by the financial crisis in 2008. The updated document strengthens bank capital requirements and introduces new regulatory requirements on liquidity. The main purpose of the agreement is to improve the quality of risk management in the banking industry, which in turn strengthens the stability of the financial system as a whole.

It should be marked, that Kazakhstan has faced difficult conditions in economy before, but this crisis of different of previous ones, consequently measures to be done have to be contradistinct.

New challenges of modern world and problems arised in economy have to be prevailed using both tactical and strategic measures. The aim of entering the top-30 developed countries by 2050 has been targeted in the country President N.A.Nazarbayev’s message reporting «Kazakhstan 2050: new political course of the established state» strategy. The President marked, that nowadays crisis has put everything on belonged places and new era is about to came, world economic system is changing, competition empowers. That is why we have to find our own path [3].

According to the Financial Supervision of the National Bank of Kazakhstan on December 1, 2015 the banking sector is represented by 35 second-tier banks (STB), 16 of which are the banks with foreign participation, including 13 subsidiary banks. Previous year ended with the merger of the banks like JSC «Alliance Bank», JSC «Temirbank» and JSC «Forte Bank» to the group «Forte Bank», the merger of JSC «Kazkommertsbank» with JSC «BTA Bank». In addition, JSC «Halyk Bank of Kazakhstan» JSC has obtained «HSBC Bank Kazakhstan», which was renamed to JSC «Altyn Bank».

Despite the slowdown in the economy, the banking sector was developing dynamically enough: since 2014 assets increased by 24.1 %.

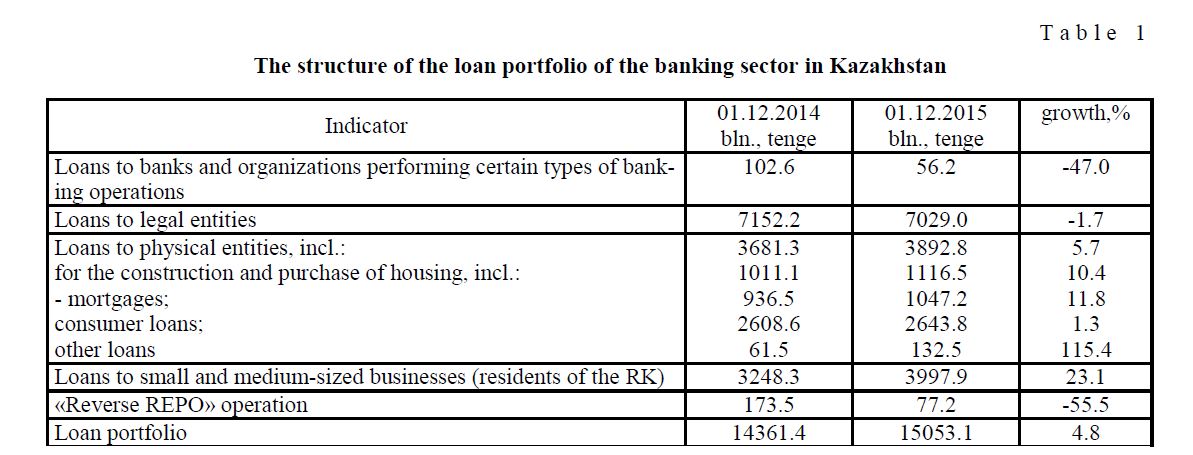

Credit sector continues to build, although the pace of last year dropped significantly. The structure of the loan portfolio of the second-tier banks of the Republic of Kazakhstan is discussed in the Table 1.

The structure of the loan portfolio of the banking sector in Kazakhstan

T a b l e 1

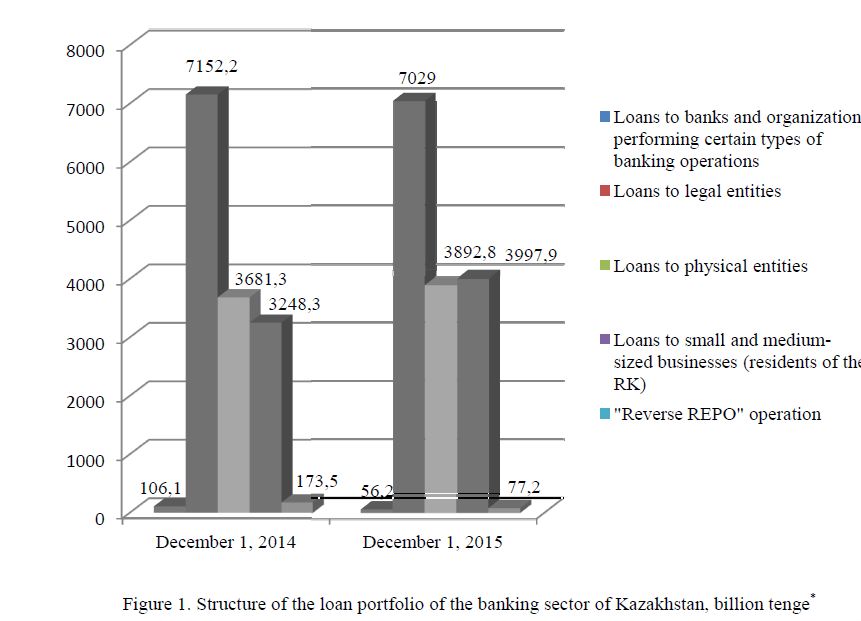

Figure 1 clearly shows decrease of loans in the structure of STBs’ loan capital to banks and organizations performing certain types of banking operations, as well as the «reverse REPO» operations by 47 % and 55.5 %, respectively. While loans to businesses and individuals have a tendency to sustained growth, loans to SMEs in 2015 differ by spike. According to Table 1, an increase of more than 23 %, is caused by the financing of SME projects for young and aspiring entrepreneurs at the expense of JSC «Entrepreneurship Development Fund «Damu» on the basis of implementation of the state policy on the financial support of SMEs in the Republic of Kazakhstan. JSC «Rating Agency of the Regional Financial Center of Almaty» indicated that the main disadvantages and obstacles in the implementation of this program include the unfair attitude of commercial banks and detention of the review process. So, for example, banks can offer to issue loans on its own program for the commission profit, and then after some time to refinance a loan under this state program. The monitoring of JSC «Entrepreneurship Development Fund «Damu» reveals numerous violations at the second-tier banks and leasing companies [4].

Figure 1. Structure of the loan portfolio of the banking sector of Kazakhstan, billion tenge*

In October 2015, members of the Senate of the Parliament of the Republic of Kazakhstan ratified the loan agreement (Competitiveness Enhancement Project SMEs) between the Republic of Kazakhstan and the International Bank for Reconstruction and Development (IBRD). The project aims to increase the competitiveness and potential of small and medium-sized businesses. The project will cost 11.4 billion tenge46 mln. USD, including the republican budget co-financing of external loans of1.5 bln.tenge — 6 million USD, due to external borrowing of 9.9 billion tenge –40 mln. USD. Implementation period is 5 years, until 2019, inclusively. The project will improve the competence of SMEs, which later can be credited under the credit line provided by the World Bank in the amount of US $200 million.

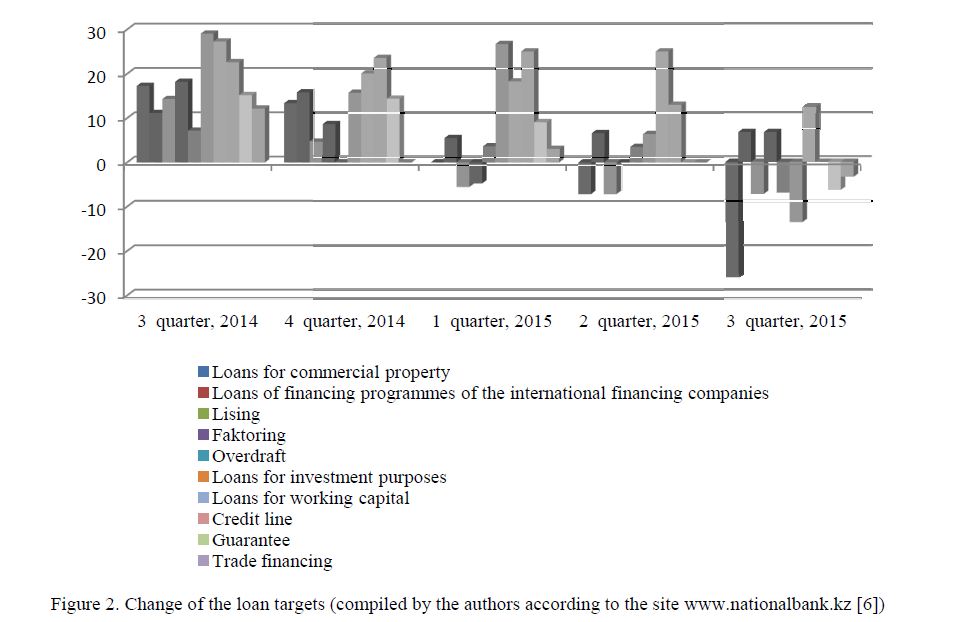

According to a survey printed «Second tier banks' condition and prognosis for the parameters of the credit market» in October 2015 the current situation with the tenge liquidity leads to a tightening of price and non-price lending conditions. Alleviation of the credit policy of the banks is not expected by the end of the year, leaving demand for loans remain low.

In the 3rd quarter of 2015, despite the fact that the credit policy of most banks did not undergo significant changes, some banks continued tightening against business. The Bank estimates that 75 % of respondents kept the credit policy on the same hard level, while 25 % of banks chose to tighten policy [4].

In general, the tightening of credit policy, and slowing growth in supply from banks is stated by limited availability and high cost of funding, as well as expectations of delinquent payments rising on the part of some borrowers in the future.

As before, demand of the enterprises engaged in the trade sector and the service sector for working capital remained, while there was a notable decline in demand from companies for the financing of fixed assets, as well as loans to purchase commercial real estate due to their long-term and high cost (Fig. 2).

* Table 1 and figure 1 compiled by the authors according to the site www.afn.kz [5].

Figure 2. Change of the loan targets (compiled by the authors according to the site www.nationalbank.kz [6])

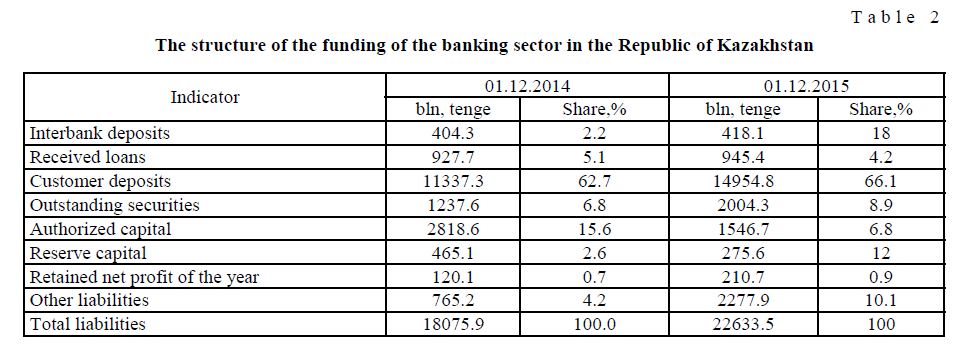

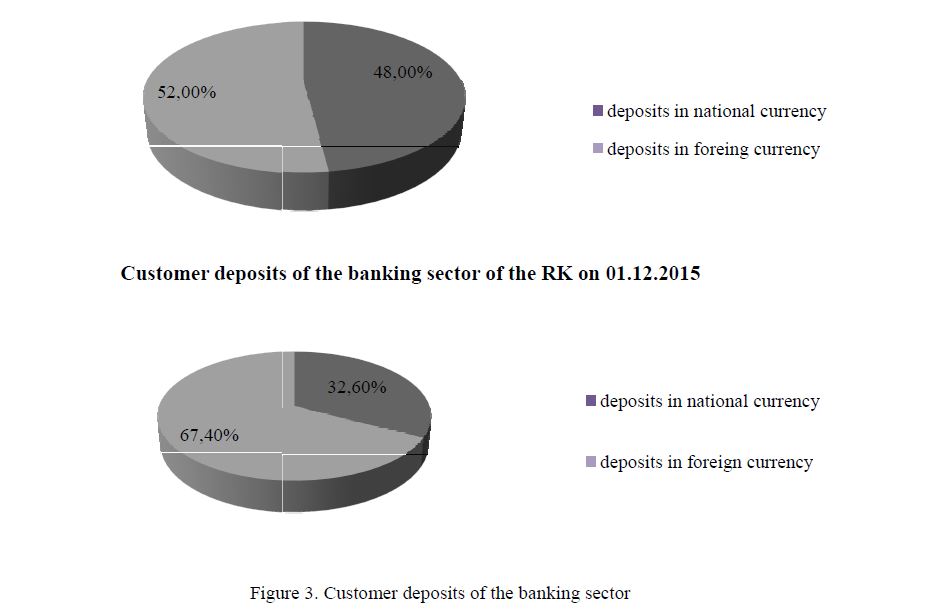

The main sources of the credit activity are customer deposits of the banking sector. Funding structure of the banking sector is presented in Table 2.

The structure of the funding of the banking sector in the Republic of Kazakhstan

T a b l e 2

According to Table 2, on December 1, 2015, more than 60 %in the structure of funding comes from customer deposits; this indicator has increased since 2014 by 3.4 % from 11,337.3 billion tenge to 14,954.8 billion tenge. The practice of the banking sector in Kazakhstan indicates maximum term of urgent loans as three years, which is short-term funding and not all of contributions are subject to renewal. Thus, suggests the main source of funding — the short-term and medium-term deposits. At the same time according to the Committee of Financial Supervision of the National Bank of the Republic of Kazakhstan since 2014 a shortage of tenge liquidity is observed, because deposits in foreign currency accounts compile 70 % of all customer deposits, this index has increased by almost 15 % since the beginning of 2015. (Fig. 3).

Figure 3. Customer deposits of the banking sector

Monetary policy instability of the National Bank brews uncertainty among population in the questions of depositing in national currency. In the meantime growth of the dollar part in retail deposit portfolio is based on re-calculation of the tenge deposits, even with new high exchange rate. In the light of such situation JSC «Fund of Guaranteed deposits of the Republic of Kazakhstan» lowered recommended maximal interest rate for the new deposits of physical entities in foreign currency by 1 % from 5.5 % to 4.5 %. Ergo, making it twice profitable to withhold deposit in tenge rather than in dollars. This actions were arranged to reduce the pressure done to tenge and raise confidence of citizens in national currency [3].

In general, the lack of sources of mediumand long-term funding and economic uncertainty are key factors in reducing lending in the economy, and because of a problem with non-performing loans, the tightening of credit policy of banks leads to raise interest rates on loans. This situation does not allow the current demand from the corporate sector for loans to be satisfied completely.

References

- The Republic of Kazakhstan: Concluding Statement of the IMF staff visit // Official site of the National Bank of the Republic of Kazakhstan, [ER]. Access mode: nationalbank.kz.

- Official site of the informational agency «Interfax-Kazakhstan», [ER]. Access mode: interfax.kz

- Komekbaeva L.S., Artukhevich T.S. of Karaganda University. Ser. Economy, 2015, 3 (79), p. 196–204.

- Official site of the JSC «Rating agency of the regional financial center of Almaty city», [ER]. Access mode: rfcaratings.kz

- Official site of the Financial Supervision of the National Bank of Kazakhstan, [ER]. Access mode: afn.kz

- Official site of the National Bank of the Republic of Kazakhstan, [ER]. Access mode: nationalbank.kz