The Kazakh banking system started to use international standards BASEL since 2003. Classification of the loan portfolio enables the quantitative study of the quality of loans issued in the banking system. The classification of the quality of loan portfolio as it publishes the Financial Supervision Agency of Kazakhstan is represented by a seven categories of quality, which uniquely determine the probability of default / non-payment of borrowers. The first category of loans (referred to as «Standard») reflects the amount of those loans for which failure to fulfill obligations is the minimum because borrowers payments of principal and interest of remuneration is on schedule, which means no debt. The following 5 categories called Doubtful, which are ranked from least risky (category 1) to the most risky (Category 5). Loans relate to these categories according to the degree of fulfillment of obligations on them, if the debt is 90 days or more. The last category («Hopeless») reflects the least solvent credit for which the probability of default is close to unity. For this type of loans the debt exceeds the period of 180 days or more. The classification of loans in this form allows to determine the dynamics of the loan portfolio quality and to evaluate the long- term stability of the loan portfolio, which is important for the analysis of credit risk in the banking system.

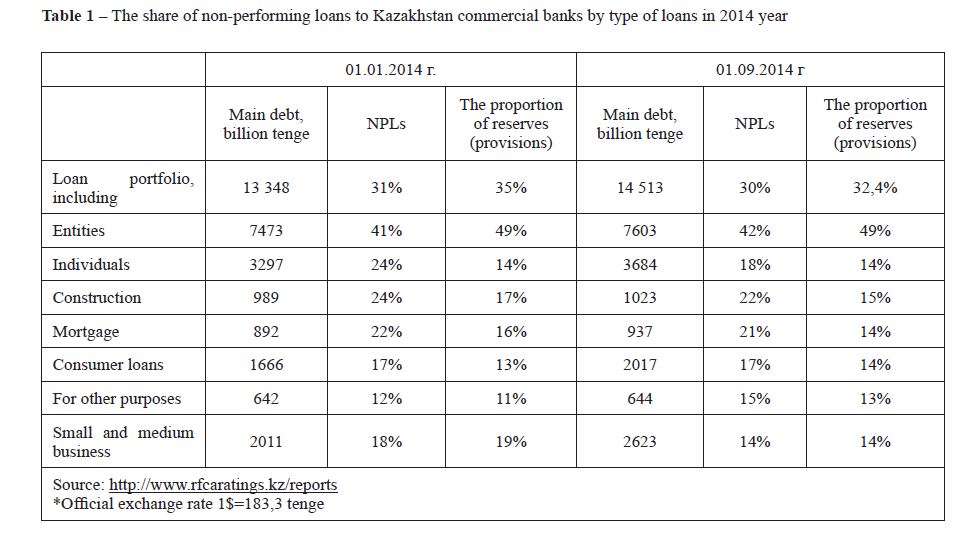

Nowadays the banking system of Kazakhstan is experiencing difficulties. The main problem is the decrease in the quantity of loans of domestic banks. The cause lies largely in the credit boom that emerged in Kazakhstan, before the global financial crisis. In that time banks, attracting «depreciating» external credit, began to lend, disrupting the necessary requirements. The negative consequences were unavoidable. Moreover, losses are growing because of the increase in a share of the non-standard and problem credits. The quality of a loan portfolio of second level banks is reflected in next table.

According to the Table 1 absolute sum of the overdue credits in 9 months of 2014 year increased for 388,4 billion tenge (2,134 billion US dollars). The main share from this sum accounts for legal entities. Respectively, also provisions were increased, which narrows the volume of credit resources.

Table 1 – The share of non-performing loans to Kazakhstan commercial banks by type of loans in 2014 year

It should be noted that the share of doubtful and hopeless credits is increasing in the structure of the overdue credit, which causes growth of losses of banks and decrease in level of liquidity.

Deterioration of a loan portfolio of second- tier banks of Kazakhstan is caused by a variety of reasons.

The Czech Republic became the member of European Union in 2004 and in 2005 year was published the first Financial Stability report. The Czech financial system proved resilient to the effects of the global financial crisis. During the last three years, banks further strengthened capitalization levels, with total capitalization increasing to 15,9% by June 2011. Hence, the Czech-banking sector was one of the few in Central and Eastern Europe (CEE), which, so far, did not require public support (International Monetary Fund, 2012).

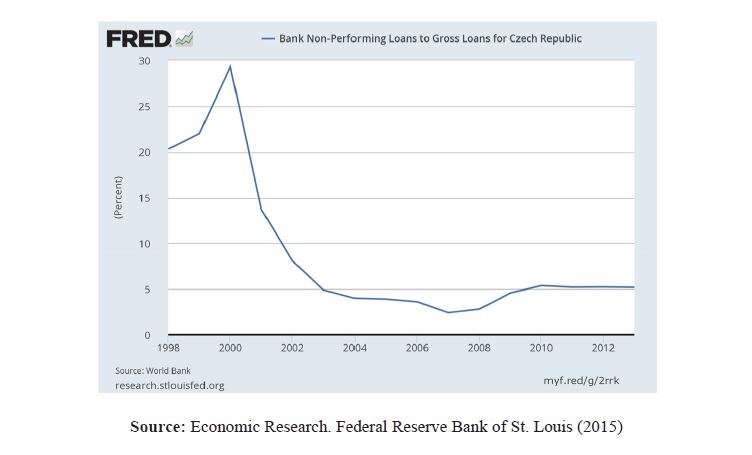

Table 2 – Bank Non-Performing Loan to Total Gross Loans in Czech Republic

Source: worldbank.org

In 2009 and 2010 years there wasn’t strong growth in Non-Profitable Loans according to the Czech National bank and the ratio of NPLs to Total Loans slightly decreased in 2011 year to 6%, which was 6.3% in 2010 year. According to the comparison between European Union countries Non-Profitable Loans ratio in Czech Republic is higher than in Belgium (2,8%) and Austria (2,7%), lower than in Poland (8,2%) and Slovenia (11,8%), and similar to the Slovakia ratio (5,6%). There was a decline in credit risk because of the evolution of the restructuring of loans in non-financial corporations and household segments.

Corporate Non-Profit Loans was 7,51 of total loans in 31.10. At the end of January in the year 2002 the Non-Profit Loans were in the peak of 17,7 and after that never increased to this level. In 2008 year Q2 NPL house were in the lowest level of 2,9 of total loans, but after that started to constantly grow.

In this article is shown one of the main problems, which seem that systematically important banks, which excessively were fond of non-expensive foreign credits in 2003-2005 years, allowed violation of the prudential standards established by National Bank of Kazakhstan.

Source: Economic Research. Federal Reserve Bank of St. Louis (2015)

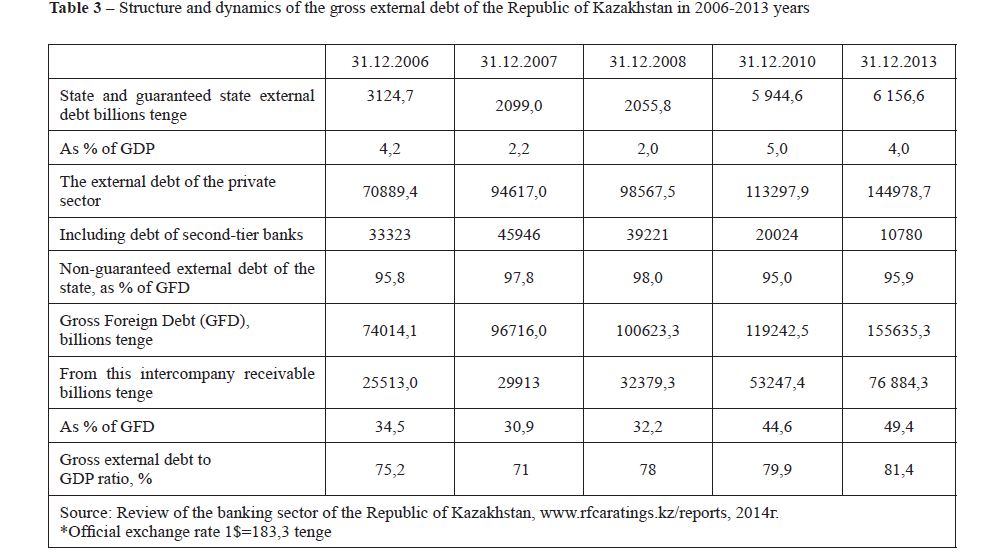

The followed devaluation in 2009 led to the growth of share of the unprofitable credits issued in foreign currency. As a result in 2010 four systematically important banks appeared on the brink of bankruptcy. The gross external debt of Kazakhstan came nearer to a critical threshold (Table 2).

Table 3 – Structure and dynamics of the gross external debt of the Republic of Kazakhstan in 2006-2013 years

The government of the country, in order to avoid a default, «rescued» these banks by granting them a soft loan from National fund of Republic of Kazakhstan, besides that banks repaid debts by attracting new loans from abroad. In 2011 the National Bank of Kazakhstan introduced restrictions on attraction of the foreign credits by commercial banks that reduced their share in a gross external debt. The intercompany debt of the Kazakh multinational companies continues to increase.

In the Czech financial sector only few large banks are dominated. This banks accounts 84% of the whole financial assets sector. The balance sheet of the banking system stop to grow in 2009 because of the crisis, but the banking system’s assets significantly increased in 2000-2008 years. In Czech Republic the 5 largest banks control more that 70 percent of total assets of the banks, the 3 largest banks about 60 percent. (International Monetary Fund, 2012)

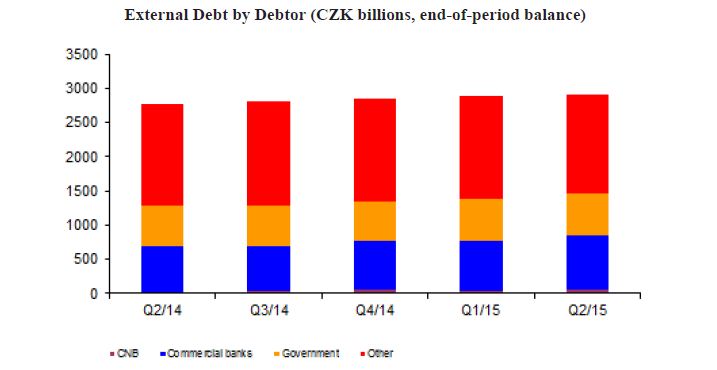

Table 4 – Gross External Debts in Czech Republic 2014

Source: Czech National Bank (cnb.cz)

External Debt by Debtor (CZK billions, end-of-period balance)

There is the risk of some problems for households in payment loan obligations because of the increase in the unemployment rate in 2012 year Q3. Which can lead to the growth of default rate because a lot of people can lose their jobs and their creditworthiness will decrease. The lowest unemployment rate in Czech Republic according to the ministry of labor and social affairs reached 5% in 2008 year Q3 and 8,4% in the year 2012 Q3. The pick of unemployment was 9,6% in 2010 Q4 according to the Czech National Bank, 2015.

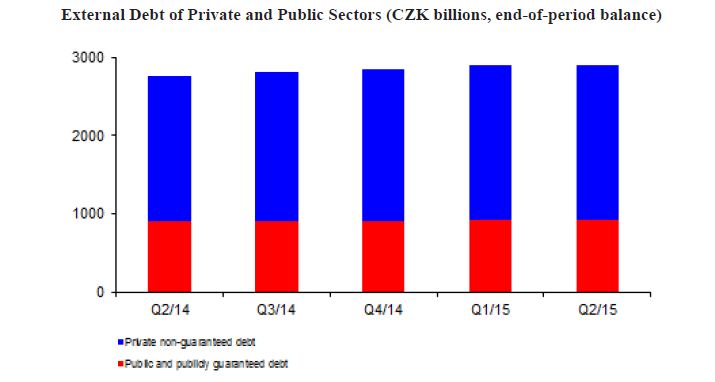

In 30 of June 2015, debt service on medium-term and long-term liabilities, which was planned in the rest of 2015 were equal to 148,2 billion CZK, of which principal amounted to 110,1 billion CZK and interest to 38,1 billion CZK. (Czech National Bank, 2015).

Domestic banking sector according to the Czech National Bank is stable and profitable. The excess of deposits over loans to banks in the system provides a sufficient reserve of cash and ensures that the domestic banking system is not dependent on external financing. The ratio of loans to deposits in the Czech banking sector has long been around 75 percent, which is among the lowest in the European Union. In an international comparison, the Czech banking system is well capitalized. And the results of stress tests of the Czech National Bank show that it is able to withstand even a very adverse economic developments. Czech banks have a very good long-term liquidity position. And currently achieve coverage of all client deposits of banks’ very liquid assets of more than 48%. CNB conducted annually rigorous tests banks’ liquidity, which demonstrate the ability of banks to withstand very adverse shocks to liquidity.

External Debt of Private and Public Sectors (CZK billions, end-of-period balance)

Also an important problem of commercial banks became the decline in quality of the personnel. Shareholders of banks started to forget that their main asset is the personnel, and human resources management is the most important task for banks. Meanwhile, supervisions show that CEO of some banks doesn’t have basic education in banking sphere and if they have there are the knowledge gained as a result of short-term business education or finishing master degree program abroad. Often this knowledge doesn’t answer conditions of the development of national economy, doesn’t connected with its structure and the mentality of the population. As a result the effective management of the assets and liabilities of banks decreases.

According to the director of the department of inspection of financial institutions National Bank of Kazakhstan, in financial sector it is possible to identify «Achilles’ heels» of banking in the country. They were the lack of adequate supervision by the board of directors over the executive bodies; low level of regulation and enforcement of risk management procedures; procedures for monitoring compliance by the bank with legal requirements; the operational procedures of action in dealing with emergency situations in the banks. It is also noted that the distressed look and procedures for interaction with clients as the Department of Consumer Protection receives numerous complaints on the second-tier banks. In addition, banks noted a discrepancy risk management procedures size and nature of the complexity of the control activities.

Near term objective is the share reduction of problem loans. In this regard application of new forms of ensuring return of the credit default, sale of debts with discount, factoring is obviously possible.

At the same time, banks should conduct a consistent policy of diversification of structure of a loan portfolio, expanding financing of small and medium business in real sector of economy. This sector of economy allows forming steadier branch structure of national economy, to create new workplaces, to raise the income, to expand the market.

The developed tendency of priority financing of trade brings in fast incomes, however promotes development of the branches creating a value added a little. We believe that the project financing aimed at the development of real sector of economy would provide steady profit, allowing increasing capitalization level.

Incaseof insufficiency ofownfinancialresources for production investment, it is recommended on a business basis together with the partner to carry out the syndicated financing of projects, and in proportion to share profit on realization between producers and investors. It is expedient to allow a loan for the long-term period, on favorable terms, to stimulate producers, to give them the chance to adjust production, and then full and timely repayment of loan debt and payment of percent that is obtaining the considerable income will be provided to bank.

It is known that for the Kazakhstan economy dollarization process that amplified after each devaluation is characteristic (1999, 2009, 2014 years). Banks give preference to foreign currencies. The volume of the credits in foreign currency began to increase systematically in the last quarter 2012. Loans in foreign currency mainly were in demand for corporate borrowers at whom they made more than 90% of a loan portfolio.

In 2014-2015 years the National bank of Kazakhstan limited delivery of the dollar credits.

Restriction of loans in foreign currency is directed more not so much on improvement of quality of a loan portfolio, how many on prevention of its further deterioration. Restrictions and on delivery of the consumer credits are introduced. The effect of these measures is contradictory as they not only will protect banks from future risks, but also will contain growth of consumption of the population and profit of banks.

Czech financial sector has strengthened the already high resilience to potential adverse shocks. Banks, an essential part of the financial system, increased capital and liquidity reserves and fulfilling new European regulatory rules. The main risk for the financial sector remains a renewed recession leading to a drop in profitability.

Thus, the phase of crisis of a modern business cycle in the countries of an emerging market will have long character since it is caused not only market fluctuations, and is caused by deep structural deformations of economy.

In this situation heads and shareholders of banks of the second level have to realize that in Kazakhstan as in the country with an emerging market, representation that banks can prosper against a depression of real sector of economy, is illusory and not perspective. It is expedient to lift personal responsibility of board members, Board and credit committee of bank for quality of a loan portfolio. And also to increase the responsibility of shareholders for growth of capitalization of banks.

References

- Statistical Bulletin National Bank of Kazakhstan №8, http://www.nationalbank.kz, 2013

- The Civil Code of the Republic of Kazakhstan, Article 51 (with amendments and additions as of 29.12.2014 )

- Guidance on credit scoring, edited by Elithabeth Mays. Editors: Elizabeth Mays, D.Voronenko. Publisher: Grevtsov Pab- lisher ISBN 978-985-6569-34-3, 1-888998-01-8; 2008

- The banking sector. Current position. http://www.afn.kz; 2006, 2007, 2008, 2009, 2010, 2011, 2012

- Abisheva G.A. «The financial crisis in Kazakhstan: experience and prospects», 2012

- National Bank revealed the «Achilles’ heels» http:// matritca.kz/other-sites/19736-nacbank-vyyavil-ahillesovy-pyaty- kazahstanskih-bankov.html. 18 March 2015

- International Monetary fund. Available online: imf.org

- Czech National Bank. Available online: cnb.cz

- Economic Bank NPLs to Gross Loans for Czech Republic. Federal reserve bank of St. Louis, DDSI02CZA156N- WDB; 2015.

- World Available online: www.worldbank.org

- European Central Working Paper Series NO 1329/ April 2011. Available online: www.ecb.europa.eu