In the article the genesis and the potential of the Kazakh and Russian economic industrial cooperation are analyzed, as well as limiting factors and perspectives of its further development. In the article the dialectical relationship and the dualistic nature of cooperation and competitiveness are revealed. The authors' hypothesis is based on the idea that the dominant purpose of industrial cooperation is a model of the active participation of the consolidated group of countries in the region eliminating the possibility of a drift towards the periphery. The authors used the concepts of methodological possibilities of the «theory of the new regionalism», «competitiveness theory» and geopolitical doctrine of Eurasianism tried to explain the background and development of the industrial capacity of the Kazakh and Russian economic cooperation, that allow to evaluate the quantitative and qualitative parameters of the functioning of the Kazakh and Russian economic and industrial cooperation, its limiting factors and perspectives for its further development. Modern features and problems of economic cooperation of Kazakhstan and Russia on macro - and meso-levels are revealed and ways of their decision are offered. Comparative analysis of the level of economic development of the Republic of Kazakhstan and the Russian Federation are assessed. The specificity of the Kazakh- Russian cooperation in the industrial (fuel and energy, transport, industrial), trade and investment spheres is studied and the author's assessment of the prospects of their development is given.

I. Introduction

Competition is a necessary condition for the formation and development of market relations. It helps to improve the economy, reduce production costs, improve product quality. Competition also contributes to the renewal of fixed assets, helps to meet the needs of consumers, improve the socio-economic standard of living of the population. The concept of «competitiveness» covers a wide range of economic characteristics that determine its position in the industry market. This complex includes the qualitative characteristics of the goods, the quality of the equipment and technology, the level of organization of production, labor, management and marketing.

Within the framework of economic globalization, a high level of competitiveness is a priority for the success of the enterprise, industry and country. As part of the competitiveness of the economy is understood concentrated expression of social opportunities realized in goods and services, both in domestic and foreign markets. The competitiveness of the industry is determined by the presence of competitive advantages that allow to produce high quality products that meet the requirements of specific groups of consumers according to the market segment. Characteristics, evaluation criteria and indicators, as well as factors affecting the level of competitiveness of an enterprise, industry or country have their own specifics in the industry market [1].

The American school (M. Porter, M. Enright, M. Storper, P. Krugman, G. Gereffi) is focused on the most practical aspects of the implementation of programs to improve the competitiveness of economic entities; the main research topics are the analysis of the development of industrial and regional clusters as the basis of the competitiveness of countries and regions.

M. Porter's developments were continued by another American scientist M. Enright, concerning the regional aspect. He developed the theory of regional clusters. According to its definition, «a regional cluster is an industrial cluster geographically close to each other by cluster member firms» or «a regional cluster is a geographical agglomeration of firms operating in one or more similar industries». The main determinants of improving the development of regional clusters are the four sides of the diamond of competitive advantages defined by M. Porter. M. Enright noted three levels of competitive advantages of the regional cluster: supranational, national and local.

Experts, based on the theory of M. Storper, developed a scheme of «ideal development» of the regional cluster, consisting of six stages:

- Creation of pioneer firms based on local specific production skills;

- Creation of a system of special service providers of firms and a specialized labor market;

- Creation of new (often governmental) organizations to support firms working in 3rd grade;

- Attraction of external domestic and then foreign firms, highly skilled labor force as incentives for the organization of new cluster firms in the cluster;

- Creation of non-market assets between firms that stimulate diffusion of innovation, information and knowledge;

- The stage of the fall of the 6th cluster, when the cluster has exhausted its innovation potential, and the closed one does not allow it to confuse innovations from the external market.

Hettne Bjorn stands out from researches in this area, claiming that the main action of the elements of modern globalized economic system serves the region. Werein, this new regionalism, firstly, is formed in a multipolar world, and secondly, is the result of movement within the region, thirdly, the region is more open and multilateral concept, fourthly, it also includes non-governmental players (Hettne & Soderbaum, 2002) [2].

The main arguments of the representatives of the «new regionalism theories» are the following: firstly, regionalism as a purely endogenous process in each region has its own specific model, deterministic set of specific socio-economic, industrial, socio-cultural, political and historical characteristics of the region; secondly, the economic reality of the second half of the 20th century, in which European integration was born, is fundamentally different from the modern picture of the world, in which similar situations are reproducible (Baikov, 2010) [3].

The author's hypothesis comes from the fact that there are significant features of the typological similarity in the set of the original motivations of the integration of EU and CIS groups. Thus, the prerequisites for the formation of the integration of these associations are: firstly, the fear of intraregional conflicts, as well as the need to unite in the face of the larger, first of all, non-regional players; secondly, the desire to simplify the conditions for intra-regional economic exchange and to create conditions for improving the competitiveness of the integration group as a whole in relation to the «outside» of the state; thirdly, efforts to create a common identity symbols based on a common historical and cultural heritage and common historical and economic destinies in the future; fourthly, the predominance of the intergovernmental approach to strategic decision-making relating to regional development [4].

- Data, Analysis, and Results

All these years the Kazakh-Russian relations were developing steadily and dynamically, important issues were solved, consistently, in the economic, political, humanitarian and other spheres. Countries have developed partnerships, for which stability, mutual trust and openness are fully characteristic. The high level of cooperation has objective reasons, connected not only with the huge total length of the borders of more than 6,000 km, the active interaction of adjacent regions, but also the common historical, economic and spiritual values of the two largest Eurasian peoples — Kazakhs and Russians.

Now legal base includes more than 300 documents. It has become more political trust and understanding. The culmination of the political will of the two countries was the adoption of a declaration on eternal friendship and cooperation oriented to the 21st century, which has political importance for the future of Kazakhstan and Russia.

In terms of socio-economic development, Kazakhstan and Russia are developing countries with new economies. Kazakhstani foreign policy gives priority to the Russian Federation. Kazakhstan and Russia are committed to preserving the common economic, defense, humanitarian and information space and are equally interested in strengthening each other's security, stability and prosperity. Both states have all the necessary conditions and prerequisites for such interstate cooperation (Table 1).

Table 1

Necessary conditions and prerequisites for interstate cooperation of Kazakhstan and Russia

|

№ |

Option |

Kazakhstan |

Russia |

|

1 |

2 |

3 |

4 |

|

1 |

Geographical proximity |

The presence of a jointly created infrastructure |

The presence of a jointly created infrastructure |

|

“2“ |

Area |

2 724 900 км2 (the 9th place) |

17 125 191 км2 (the 1st place) |

|

1 |

2 |

3 |

4 |

|

3 |

GDP in terms of PPP |

460 bn.$ (the 41st place) |

3800 bn.$ (the 6th place) |

|

ɪ |

GDP per capita |

25 669 $ (47th place) |

25 411 $ (48th place) |

|

5 |

Population |

17 963 900 bn. (64th place) |

146 804 372 bn. (9th place) |

|

ɪ |

Human Development Index |

0,788 (high, 56th place) |

0,804 (very high, 49th place) |

|

7 |

Natural resources |

Oil, natural gas, coal, rare earth elements, ferrous and non-ferrous metal ores, etc. |

Oil, natural gas, coal, rare earth elements, ferrous and non-ferrous metal ores, etc. |

|

¯8¯ |

Industrial potential |

high |

high |

|

9 |

Cooperation |

close |

close |

|

10 |

Agriculture |

Production of cereals and livestock products |

Production of cereals and livestock products |

|

ɪ |

Transport corridors |

5 |

3 |

|

12 |

Education, culture, science |

Close connected |

Close connected |

|

13 |

Technological structure in the economy |

3,4,5 |

4,5 |

Note. Source [5].

Necessary conditions and prerequisites for interstate cooperation between Kazakhstan and Russia:

- Russia and Kazakhstan have rich natural resources: oil, natural gas, coal, rare earth elements, ores of ferrous and non-ferrous metals, etc.;

- the presence of a strong industrial potential in the fuel and energy, metallurgical and chemical industries, engineering and metalworking, enterprises which have operated for decades in close cooperation;

- both States have great opportunities for the development of agriculture, especially for the production of grain crops and livestock products;

- Russia and Kazakhstan have a well-developed transport system, which is traditionally interconnected with similar European systems, Caucasian, Central Asian and far Eastern regions and countries;

- most of the fixed assets of industry, agriculture and housing and communal services were created under the same conditions and standards;

- the main transport and communication industries, energy of the Republic of Kazakhstan worked in a single technical and technological mode with Russian structures, received scientific and regulatory and material and technical support also from Russia. Thus, rail transport was 80 % satisfied with supplies from Russia, for aviation this percentage was even higher, the same is in the field of communications;

- education, culture, science of Kazakhstan had a close relationship with the relevant areas of Russia; training of specialists and highly qualified personnel in all sectors of the economy was carried out according to common norms and standards;

- both states have large and underutilized potential reserves for economic recovery and increasing export potential, primarily for manufacturing and agricultural products, as well as transport system services;

- Kazakhstan and Russia are facing similar tasks today, in particular, building a competitive economy by diversifying the sectoral structure, creating new and developing existing knowledge-based industries, including export-oriented ones, working in the manufacturing industries for the production of goods and services with high added value [6].

Russia is the second largest economy in the middle surrounded by Kazakhstan, and a common border with it is 7591 km away. There is a significant difference between countries in population: RK — 17.6 million, Russia — 143,7 million. Economically, Russia significantly outweighs Kazakhstan. By a large margin from Kazakhstan, it dominates the Eurasian integration Union (EAEU). Russia's share in its total GDP is 82.7 percent. The high degree of disproportion between the members of the Association distinguishes it from other integration blocks in the world.

But there are obvious differences between these two countries and, first of all, the incompatibility of the size of economies.

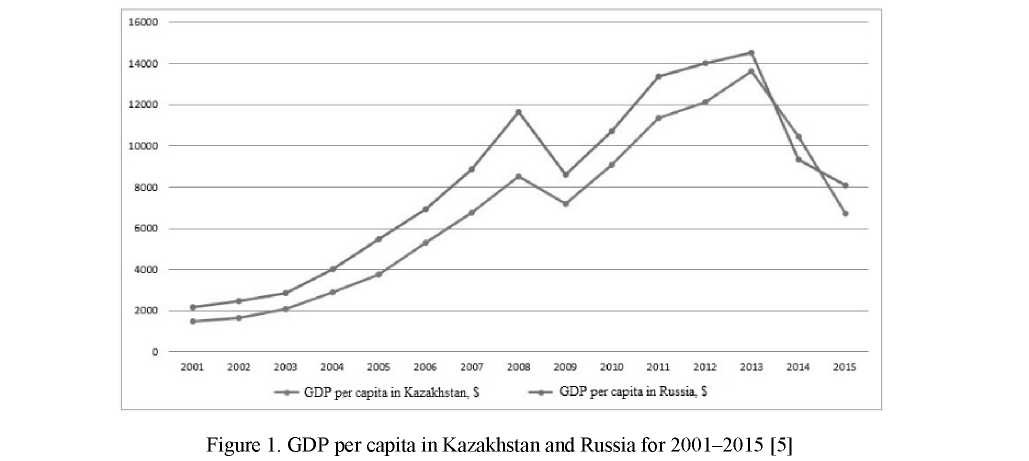

After the devaluation of the national currency, Kazakhstan lost its primacy and ceded to Russia in per capita GDP, which was $10344 by the end of 2016 and $9346 — in the Russian Federation (Fig. 1).

The main reason for the decline in GDP per capita in Kazakhstan was the fall in prices the country's main export product — oil, which brings about half of the revenues to the budget. The result was almost 100 % devaluation, when in August 2015, the price for 1 US dollar rose from 188 tenge to 384 in January 2018. Despite the fact that the Russian economy continues to experience difficulties from Western sanctions, its budget depends less on world oil prices than on Kazakhstan, but the less dramatic devaluation of the ruble remains the main factor.

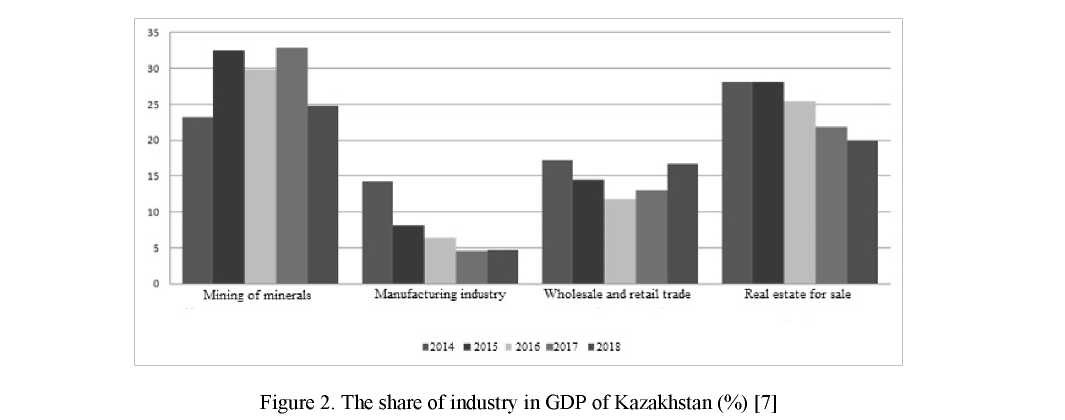

The structural changes made during the years of independence did not yield any significant results. The dependence of the country on the import of industrial products is still an actual problem for Kazakhstan. About half of the imports are products of the heavy and transport industries, engineering.

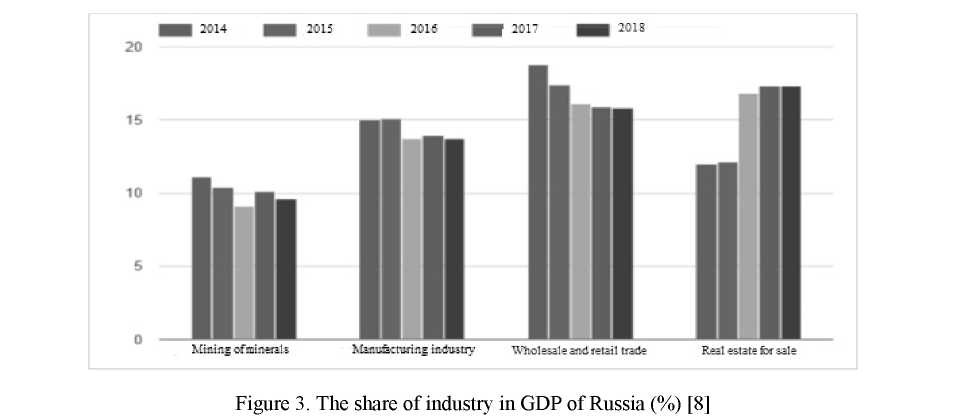

Despite the focus of the Russian economy on the extraction and sale of minerals, their contribution to Russia's GDP is gradually declining. For 4 years, their share decreased by almost 4 percentage points. It is caused by a surge in activity in the services market. According to Rosstat, this type of activity for 2018 brought Russia's GDP 9.2 trillion rubles, increasing from 2012 to 3.1 trillion rubles.

Analysis of the sectoral structure of the GDP of both countries shows the following: the economy of Kazakhstan shows a direct dependence on the extraction of minerals (oil, gas, metals), while the Russian economy is gradually moving away from this, its economy shows an increase in operations with real estate and other services.

In Kazakhstan today, when the current crisis affected almost all industrial enterprises, there is a weak activity of enterprises in the creation and distribution of innovations. According to the Statistics Committee of the Ministry of Economy of the Republic of Kazakhstan, the share of innovation-active enterprises in the country was 8.1 % of the total number of respondents (24,068 units). In previous years, it had the following level: from 2.1 % in 2003 to 8.1 % in 2018.

In Russia the situation is the same as in Kazakhstan. According to Rosstat, the share of innovationactive enterprises in Russia was 9.7 %. In previous years, it had the following level: from 10.3 % in 2003 to 9.7 % in 2018.

Two countries are currently not priority partners for each other, especially Kazakhstan for Russia. For 2012-2016, the level of mutual trade fell by 2.2 percent.

The results of any structural changes should be directly reflected in the sectoral structure of the national economy, GDP and the balance of payments, as well as in the structure of employment by economic sectors. In 2015, the gross domestic product (GDP) of Kazakhstan decreased to 1.5 %, and in 2016 decreased to 2 %. The suspension of GDP growth was due to a decrease in oil prices around the world, the fall in the level of investment in the economy of the post-soviet states, a decrease in oil demand from China and Russia, the impact of anti-Russian sanctions on the economy of Kazakhstan.

The Russian-Kazakh Agreement and the program of long-term economic cooperation between the Government of the Republic of Kazakhstan and the Government of the Russian Federation (until 2020) provide a large field of activity for the production cooperation of our countries.

The priorities of bilateral economic cooperation most fully reflect the complementarity of the economies of our countries, which are components of the once unified economic complex — fuel and energy and agro-industrial complexes, metallurgy, engineering and transport, outer space (Table 2).

Table 2 Priorities of bilateral economic cooperation between Kazakhstan and Russia in the industrial sphere

Note. Compiled by the author.

|

№ |

Priorities of the national economy of Kazakhstan |

Priorities of the national economy of Russia |

|

1 |

2 |

3 |

|

1 |

Oil refining and oil and gas infrastructure |

Energy efficiency |

|

2 |

Mining and metallurgical industry |

Space technology and telecommunications |

|

3 |

Chemical industry |

Medical technology and pharmaceuticals |

|

4 |

Nuclear industry |

Information technology and software |

|

5 |

Engineering |

Nuclear energy |

|

6 |

Pharmaceutical industry |

|

|

7 |

Agribusiness |

|

|

8 |

Information technology |

|

|

9 |

Biotechnologies |

|

|

10 |

Space activity |

|

|

11 |

Alternative energy |

The structural changes carried out during the years of independence did not yield significant results. The country's dependence on imports of industrial products is still an urgent problem for Kazakhstan. About 1/2 of the imports are products of heavy and transport industries, engineering (Fig. 2).

Despite the focus of the Russian economy on the extraction and sale of minerals, their contribution to Russia's GDP is gradually declining. In 2016, mining and processing accounted for 23.3 %, in 2017 — 24 %, and in 2014 — 26.1 %. For 4 years, their share has decreased by almost 4 percentage points.

This is caused by a surge in activity in the service market. According to Rosstat, this type of activity in 2018 brought Russia's GDP 9.4 trillion rubles, an increase from 2014 to 3.1 trillion rubles (Fig. 3).

The analysis of the sectoral structure of the GDP of both countries shows the following: the economy of Kazakhstan shows a direct dependence on the extraction of minerals (oil, gas, metals), and the Russian economy is slowly moving away from this, its economy shows the growth of real estate transactions and other services.

Also, the devaluation of national currencies played a decisive role in reducing the figures, which followed the strongest fall in oil prices in early 2016. In January quotes for Brent crude oil fell below $30 per barrel due to excess supply in the market, as well as a reduction in demand from China.

The dependence of the Kazakh and Russian economies on the extraction of raw materials continues (Table 3). In the Russian Federation, the share of mining in GDP (in terms of value added) increased from 9.33 % in 2008 to 9.76 % in 2018. The share of mining in Kazakhstan tended to decline (from 38.81 % in 2008 to 18.28 % in 2018). The main factor of this decline was the fall in prices for metal and hydrocarbons on the world market. At the same time, the share of manufacturing in GDP is also declining. Thus, for the period from 2008 to 2018 it decreased: in the Republic of Kazakhstan — from 20.93 to 14.11 % (or 6.82 percentage points), in the Russian Federation — from 17.52 to 14.15 % (or 3.37 percentage points).

Table 3 Structure of industrial production of the Republic of Kazakhstan and

the Russian Federation by types of economic activity, %

Note. Sources [7] and [8].

|

2016 |

2017 |

2018 |

|

|

The share of manufacturing in GDP: |

|||

|

Republic of Kazakhstan |

15,78 |

14,95 |

14,11 |

|

Russian Federation |

13,41 |

13,68 |

14,15 |

|

Share of mining industry in Kazakhstan |

28,84 |

27,14 |

18,28 |

|

Share of mining in Russia's GDP (in terms of value added) |

9,37 |

9,12 |

9,76 |

In the Republic of Kazakhstan the degree of reduction of this indicator was much smaller compared to the share of industrial production in GDP (6,82 p.p. versus 27.61 p.p.) that allows to assess structural changes in GDP as positive.

Cooperation between Russia and Kazakhstan in priority sectors of the economy, such as the fuel and energy complex, engineering, metallurgy, transport, space exploration, is increasing. For example, the share of the fuel and energy complex in the total volume of industrial production in Russia is 29.5 %, in Kazakhstan — 38.7 %.

The direction of cooperation between the two countries in the fuel and energy complex is one of the promising.

We can note the growth of investments in recent years, the general markets are still developing.

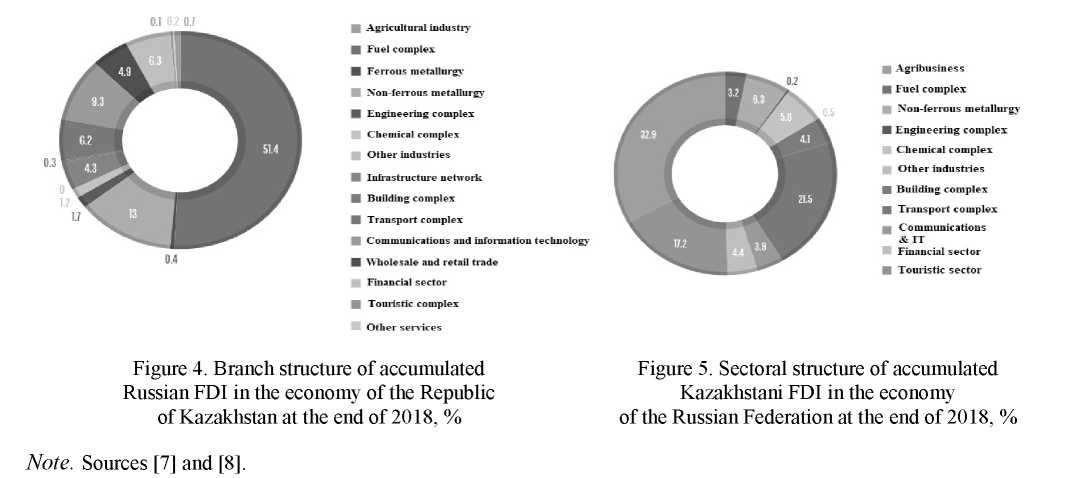

The main participants of mutual investment ties in the region are Russia and Kazakhstan. At the end of 2018, the Russian Federation accounted for 81.5 % of the exported volume of accumulated FDI and 15.1 % of imported FDI (Russia is considerably inferior to both Kazakhstan and Belarus in terms of incoming direct investments). Similar indicators for Kazakhstan were 17.4 % and 30.2 %, respectively.

In 2018, the gross inflow of direct investment from the Russian Federation to the Republic of Kazakhstan was 9,856 million US dollars. The leading sectors of Russian FDI in Kazakhstan are the fuel complex and non-ferrous metallurgy. The specific weight of these sectors was 51.4 % and 13.0 % at the end of 2018 (Fig. 4 and Fig. 5).

In general, the sectoral structure of accumulated Kazakh FDI is very different from the structure of Russian FDI in the region. The leading sector is the agro-food complex (32.9 %) due to the investments of Ivolga-Holding in plant growing and Meridian Capital in the dairy industry in Russia. In the second place is the transport complex (21.5 %), where Meridian Capital is leading thanks to investments in Russian airports, but notable FDI is also associated with the Caspian Pipeline Consortium (Kazakhstan's share is 20.75 %, the bulk of the pipeline passes through Russia). A tourist complex is also allocated due to Kazakhstan investments in hotels in Russia and Kyrgyzstan.

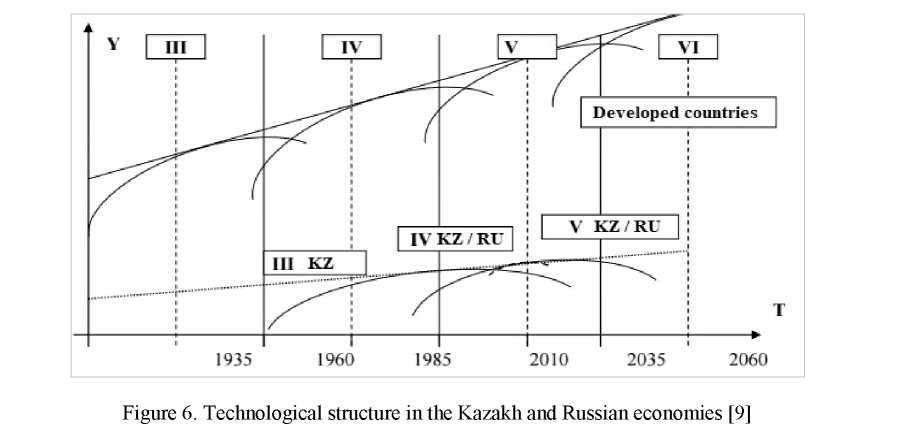

According to expert estimates, the specific weight of the fifth technological structure in Russia is 3 %, the fourth — 48 % (prevails in civil engineering, raw materials industries), third and relic (prevail in agribusiness, services, households) — 49 % (Fig. 6).

According to other estimates, in Russia the third way occupies 55 %, the fourth way does not exceed 30 %, and the fifth way — 5 %. In the US, the share of the fifth technological order is 60 %, the fourth — 20 %, the sixth mode occupies about 5 %.

Degradation and de-industrialization of the technological structure of Kazakhstani economy are associated with negative trends in structural changes in the economy. They were manifested in the course of the economic recovery that began at the turn of 2000 on the basis of a commodity factor. As a result, the structure of the economy was dominated by the production of oil, non-ferrous metals, that is, industries belonging to the fourth technological order. Their share in the volume of industrial production is more than 60 %. It can be said that Kazakhstan lags behind the world economy more than one technological structure.

Conclusion

From the analysis presented above, we can make an unambiguous conclusion: in order for Kazakhstan and Russia to reach a new level of economic development, having overcome the prevalence of raw dependence, it is necessary to continue to follow the previously adopted benchmarks for innovation in the economy. In an economic crisis, there is simply no alternative to scientific and technological development. However, this process should be based on the concept of intensification of innovation activity, which involves the correlation of its results with the resources expended.

Of course, today's level of economic integration does not meet the needs of the national economies of Kazakhstan and Russia. The existing facts of economic interaction between the two countries should be assessed as insufficient and in need of correction. Priority of development of Kazakh-Russian economic relations can be supported by existing numerous perspective directions of development:

- cooperation and development of fuel and energy complexes;

- cooperation in the field of transport;

- cooperation between Kazakhstan and Russia in the development of the Baikonur cosmodrome;

- cooperation in developing the natural resources of the Caspian Sea;

- scientific and technological cooperation;

- cooperation in the agricultural products market

Economic topics, especially the prospects for bilateral cooperation in the oil and gas sector, energy and transport, were the subject of discussion during the regular official visits of the Presidents of Russia and Kazakhstan.

Concluding each negotiation, the heads of state confirm that our countries have entered a new millennium under the sign of unshakable friendship and strategic partnership [10].

Kazakhstan and Russia as the main middle states of Eurasia should become important elements of the global economy, as they are in a favorable position, have rich natural resources and ample opportunities. The present century opens for both countries, which see a strategic goal in strengthening the indestructible friendship of their peoples, the broadest prospects for comprehensive development, economic and cultural growth in the conditions of lasting peace, stability and guaranteed security.

References

- Asanbekov, M.K. (2012). Evraziiskii ekonomicheskoi soiuz — prahmaticheskaia realizatsiia evraziiskoi idei. Proekt «Vremia Vostoka». Institut stratehicheskoho analiza i prohnozirovaniia [Eurasian Economic Union — the pragmatic realization of the Eurasianism idea. The Project «The Time of the East». The Institute of the Strategic Analysis and Forecast]. easttime.ru. Retrieved from http://www.easttime.ru/analytics/tsentralnaya-aziya/evraziiskii-ekonomicheskii-soyuz-pragmaticheskaya-realizatsiya-idei-evr [in Russian].

- Hettne, B., Inotai, A. & Sunkel, O. (bds.) (1999). Globalisation and the New Regionalism: the Second Great Transformation. London: Macmillan.

- Katzenstein, P. (2003). European Enlargement and Institutional Hypocrisy. Oxford: Oxford University Press.

- Baikov, A. (2010). Formy intehratsionnykh vzaimodeistvii v Vostochnoi Azii: opyt proverki Evraziiskoim soiuzom [Forms of integration interactions in the East Asia: the experience of testing by the European Union]. Sravnitelnaia politika – Comparative Politics, 1(1), 166-187 [in Russian].

- Otchet Evraziiskoho ekonomicheskoho soiuza (2015) [The Report of the Eurasian Economic Commission]. eurasiancommission.org. Retrieved from http://www.eurasiancommission.org/ru/act/integr_i_makroec/dep_stat/econstat/Documents /Indicators201512.pdf [in Russian].

- Mansurov, Т.А. (2013). Kazakhstan i Rossiia: suverenizatsiia, intehratsiia, opyt stratehicheskoho partnerstva [Kazakhstan and Russia: sovereignization, integration, experience of strategic partnership]. Moscow [in Russian].

- Ofitsialnyi sait Komiteta statistiki Ministerstva natsionalnoi ekonomiki Respubliki Kazakhstan [Official Internet resource of Committee on statistics of the Ministry of national economy of the Republic of Kazakhstan]. stat.gov.kz. Retrieved from: www.stat.gov.kz [in Russian].

- Ofitsialnyi sait Federalnoi tamozhennoi sluzhby Rossiiskoi Federatsii [Official Internet website of the Federal Customs Service of the Russian Federation]. customs.ru. Retrieved from: www.customs.ru [in Russian].

- Kovalkin, V. (2016). Rossiia v novykh heopoliticheskikh realiiakh na porohe ХХІ veka [Russia in new geopolitical realities on the dawn of ХХІ centuries]. Moscow [in Russian].

- Tokayev, K.K. (2015). Kazakhstansko-rossiiskie otnosheniia v kontekste vneshnei politiki Kazakhstana [Kazakhstan-Russian relations in the context of a foreign policy of Kazakhstan]. The Kazakhstan-Russian relations. 1991-1995: Sbornik dokumentov i materialov – Collection of documents and materials. Almaty-Moscow [in Russian].