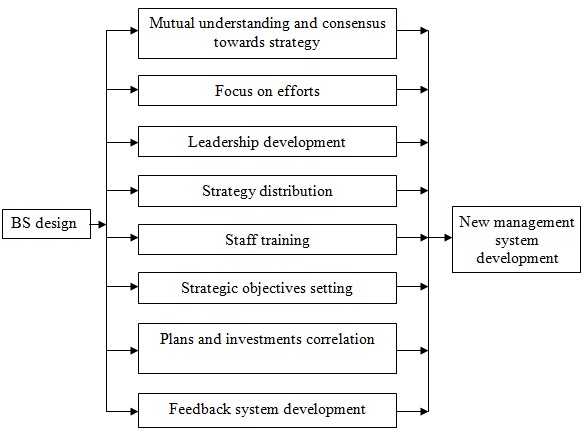

Balanced scorecard development is a wide scale change of the whole process of corporate strategy implementation. This concept in strategic management is not just a system of indicators; it is a basis for a new management system development. Robert Kaplan and David Norton, the authors of “Translating strategy into action. The balanced scorecard”, emphasize the system aimed toward success must accept the fact that this project is flexible and can be changed.

Picture 1. BSC – basis for a new management system

Source: drawn up by the authors

BSC development must be based on the following key principles:

- Company top managers are those who must implement the changes.

- The process of strategy transformation must be persistent.

- Every employee should be involved in the process of strategy implementation by its routine administrative functions.

- Company transformation for the purpose of corporate strategy implementation.

- Balanced scorecard implementation and development process include the following four stages:

- Preparation for BSC development;

- BSC development;

- BSC transferring;

- Strategy implementation supervision [1].

At the first stage of Balanced Scorecard implementation it is necessary to carefully work out the corporate strategy, determine the prospects for company development and decide which of the organizational units and levels a balanced scorecard needs to be developed

for. It is important to take into account that the BS is the concept of implementation of the existing policies and not the development of absolutely new ones. So the corporate strategy design has to be completed first, and only then the process of constructing a balanced scorecard begins.

In order to achieve balance one should avoid one-sided formulation of the strategy. Often companies focus on the financial side. However, if the organization is consumeroriented its financial goals are left neglected. Some companies are business-oriented, and pay little attention to market conditions. Only an equal consideration of a few prospects helps to avoid such imbalance.

The preparatory stage for the BSC construction also includes a selection of units for which balanced scorecard will be developed. It should be remembered that the greater the amount of the structural divisions of the company which are managed strategically through a single system of indexes, the easier the goals of upper levels can be transferred to the lower ones.

Thus, the initial prerequisites for the BSC design include:

- prospects;

- informed and motivated team of company management;

- clearly defined corporate strategy.

The second stage of the Balanced Scorecard implementation in the company is a stage of the BS construction. At this stage, the construction of an integrated system of indexes for the selected organizational unit is carried out. It can be the whole company, division or a department.

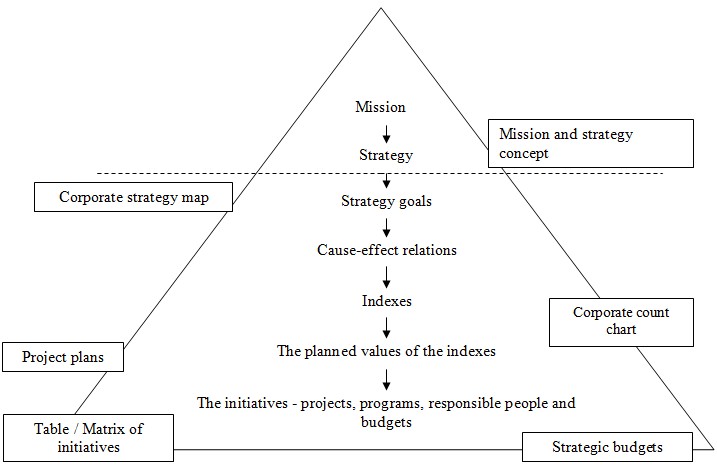

The process of the BSC design includes

the consecutive fulfillment of the following series of steps:

- concretization of the strategic goals;

- corporate strategy map construction(i.e., linking strategic goals through causeeffect relations);

- corporate count chart construction (i.e., selection of indexes and their targets);

- development of a set of strategic activities.

Picture 2 presents an outline of the process of a balanced scorecard design for an enterprise:

Picture 2. BSC designs cheme

Source: drawn up by the author

The first objective the BSC design is a breakdown of the corporate strategy to the specific strategic goals, showing different aspects of the company (the projection of the "finance", "market", "processes" and "potential"). Due to the connection between each strategic goal to one of the prospects of the company development, none of the important aspects of corporate strategy is missed. The number of projections can be increased up to five or six by clarifying the aspects of the organization on the market (for example, "Suppliers", "Customers" projection can occur) or detailed projections (as part of the "Potential" projection two components can occur: "Staff" and "Information systems"). However, the growth in the number of projections to seven or more is undesirable because it can lead to the breakdown of the single strategic vision on particular tasks [2].

The next step is critical examination of the strategic goals and the selection of those which deserve to be included in the BSC. This selection should be based on the following criteria:

- goals must be measurable;

- the achievement of objectives can be influenced;

- goals are acceptable to different groups of people in the company;

- goals meet the objectives of the corporate strategy.

It is necessary to point out, that there should not be too many strategic goals, both for corporate level of the company and in the design of corporate strategy maps for individual units. Recommended number of goals in the balanced scorecard is 20-25.

Strategic goals should not be independent and separated from each other, on the contrary, they must be closely linked and have significant mutual influence. Achievement of one goal should influence the implementation of the other, and so on, up to the main strategic goal of the company. Links between various goals must be clearly traced through the causal chains, and for their graphical display such tool as a corporate strategy map is used, the building of which is the second important step of balanced scorecard design process in the company. In the process of building the corporate strategy map the analysis of each goal of the company and all essential links are revealed.

After the completion of building causeeffect relations all the strategic goals must be connected to each other, and in this case a chain of dependencies should be built from each of them, which leads to the upper goal shown in the diagram. If this rule is not followed for some goals, then it shows that goals are "unnecessary" and should be removed from the corporate strategy map or supplemented by intermediate goals, allowing link the dead-end branch of the diagram with its apex.

Properly compiled corporate strategy map is the first result in the development of a balanced scorecard, representing the independent value. It should serve as a powerful communication tool, explaining to all stakeholders (shareholders, employees, partners) the essence of the company's strategy.

The next step of balanced scorecard design process in the company is the selection of indexes, which allows to assess the degree of the strategic goals achievement and the establishment of target values of these indexes. At this stage of the project for the balanced scorecard implementation from the entire set of indexes for each component of a balanced system ("Finance", "Customers", "Internal Business Processes", "Education and Development") only those that do not duplicate each other within the meaning and accurately reflect the essence of the company's strategy can be selected.

Let’s consider the basic indexes selection criteria for inclusion into the balanced scorecard:

- Connection with the strategy. Balanced Scorecard is a tool for translating corporate strategy into action through the use of efficiency indexes. The choice of indexes, which don’t affect the implementation of the strategy can lead to confusion, as the company will expend resources to achieve results that do not depend on the realization of goals.

- Quantitative measure. The balanced scorecard should avoid indexes, implying activity assessment in immeasurable categories because of the uncertainty and subjectivity of such concepts (for example, "good", "average" and "bad"). The index of «good level of sales growth» can be replaced with the index "sales growth of more than 25%", the index "the average level of staff sickness rate" can be formulated as "the number of absences through the disease from one to two weeks per year", and the index of "poor quality level " as "the number of products with defects of more than 5 per 1000 units."

- Availability of selected indexes for monitoring.

- Clarity. Balanced Scorecard will not operate until the company's staff understands the operational and strategic values of the selected indexes.

- Balance. In the process of selecting indexes for inclusion in balanced scorecard one should avoid systematic errors, leading to a so-called sub-optimization effect, i.e., the improvement of one index at the expense of others. For example, if the company management decides to increase the staff number and reduce prices for improving customer satisfaction, it is necessary to remember that prices reduction and increase in staff will affect the profitability level of the company. Therefore, one need to provide the situation in which, despite the prices reduction and increase in staff, the rationalization will be able to fulfill

income norms.

After the approval of the balanced scorecard composition is necessary to determine its targets values for the future periods.

Picture 3 shows the main information sources that can help in setting target values of the selected indexes:

Picture 3. Reasons for setting targets

Source: drawn up by the author

The result of the design of a complex interrelated indexes should be the corporate count chart construction – structured table containing the list of indexes included into the balanced scorecard, its targets and information about the responsible persons.

The final step of the development stage of the BSC is the determination of the comprehensive set of implementation measures of the strategic goals of the company with the indication of the person in charge, times limit for projects performances and resource requirement.

The process of developing a set of strategic actions should include:

- formulation of ideas and proposals;

- organization of ideas and proposals;

- assessment of the costs and ranking of strategic activities in order of importance;

- specification of the selected strategic activities.

It should be noted that at the stage of preparation for the BSC construction there is a large number of initiatives which can later be turned into strategic actions. Moreover, during the DSC construction the company can carry out a set of projects and programs. Thus, the first step here is to check their correspondence to the BSC goals. Analysis of the ideas, appeared on the previous stages of the work, must be conducted as well. The list of further strategic initiatives is supplemented by the new ones. They can be revealed with help of brainstorming techniques. All the ideas come through thorough analysis, specification and update before joining the final list of strategic actions.

Having built the full list of strategic actions the matrix of activities is constructed. It allows visualizing which goal contributes to the implementation of which action. An important element in developing a set of strategic actions of the process is to estimate the costs of the implementation. From this point of view, all the actions can be divided into three groups:

- actions, that are planned to be fully implemented;

- actions, that are to be implemented with limited resources;

- actions, that are to be postponed to a later date.

The development of the strategic budget is a determination of the costs plan: how much money, to whom, when and what for to pay when performing strategic actions. Budgeting application gives the ability to control the cost of the implemented strategic actions of the BSC at each stage.

The third stage of the implementation of a balanced scorecard for the enterprise – transferring the BSC. By transferring one means the process of building a balanced system for each level of the company. System data are consistent with the system of indexes for the higher level of the organization by defining strategic goals and indexes that will be used by units and departments of the lower levels to monitor the implementation of their contribution to common corporate goals. Despite the fact that a part of the applicable indexes will remain the same as at the level of the BSC across the enterprise, the majority of the lower levels of management systems will include indicators that reflect the specific problems and prospects of the level [3].

In the process of transferring corporate strategy is transmitted to all levels of management: strategic goals, indexes and their target values, measures to improve the activities specified and adjusted to the divisions and departments. The result of this process is the linkage of corporative BSC with BSC of a division and individual staff work plans.

Picture 4 shows a scheme of the process of transferring the BSC, allowing to establish a link between different levels of the organization hierarchy:

Picture 4. Transferring SB process

Source: drawn up by the author

The final stage of the BSC implementation in an enterprise is controlling the implementation of the strategy. In order to ensure long-term implementation of the corporate strategy, formulated within the framework of the balanced scorecard, it is necessary to integrate the BSC into the company management system, to provide it constantly with updated data and maintain in operating condition, implement regular monitoring of the compliance to the chosen strategy.

The result of the work must be effective balanced scorecard, ensuring the implementation of the corporate strategy through the formation of a clear link between the strategic decisions of the company’s senior management and the current activities of its business units and divisions.

REFERENCES

- Atkinson A., Epstein M. Measure for measure: Realizing the power of the balanced scorecard // CMA Management.-September 2000. – P. 22-28.

- Kaplan R.S., Nerton D.P. The Strategy – Focused Organization: How Balanced Scorecard Companies Thrive in the New Business Environment.-Boston (Ma.USA): Harvard Business School Press, 2001.

- Combining EVA with the Balanced Scorecard to improve strategic focus and alignment: 2GC Discussion Paper.UK: 2GC Active Management. 2001.