Annotation. The coronavirus outbreak and the ensuing isolation policy both in cities and interregionally have triggered a health, economic and social crisis in Kazakhstan. The sharp acceleration of sales markets and the breaking of chains, the cancellation of air travel and the restriction of the free movement of citizens, the massive transition to a regime of self-isolation provoked a sharp movement of business in different industries. It is cost effective to analyze targeted monetary fiscal policy responses that reduce long-term economies and save lives.

The coronavirus outbreak and subsequent policies of lockdowns both in cities and on interregional scales has brought about immense, and simultaneous, public health, economic, and social crises in Kazakhstan. This is particularly due to the COVID-19 induced negative supply shock, quarantine measures that have affected the service sector disproportionately, thus driving economic activity in certain industries down to zero. Due to the potentially long-term sluggish structural adjustment of the economy, a large proportion of workers employed in those industries (both formal and informal) are facing the grim perspective of a prolonged period of lost-incomes and possible mass layoffs with lasting depressing effects on aggregate demand, which can further depress the economy. Consequently, Kazakhstan will likely experience the adverse impact of the lockdown from medium to long-term perspectives with a high chance of prolonged scenarios of recovery. Thus, it is also vital to analyze pointed monetary and fiscal policy responses, which will help to mitigate long-term economic losses and save human lives.

Kazakhstan’s oil and gas industry traditionally has been the engine of its economy. As a result, the recent OPEC+ developments and the reduced demand for oil and gas represent additional challenges for Kazakhstan, increasing the impact of the pandemic on the economy. Kazakhstan has implemented measures to support businesses struggling with the effect of the pandemic. This includes a USD 13.4 billion rescue package (around 8.6% of GDP), as well as certain initiatives being proposed by President Kassym-Jomart Tokayev to help businesses avoid insolvency proceedings due to the COVID-19 disruption. This article discusses those government support measures, along with the President’s insolvency initiatives.

Economic consequences of COVID-19

The impact of the imposed lockdown on business operations to slow down the spread of the COVID-19 is not uniform to all sectors of the economy. Some industries are more exposed to the nature of the lockdown than others. Thus, for instance, those sectors of the economy that produce essential goods and services, such as food or communication technologies are less exposed to total quarantine measures since they can continue operating both in real and virtual realms. Additionally, the jobs in those sectors are more secure. Other types of industries, requiring nonessential production of goods and services and not fit for telework, such as retail stores, restaurants, hotels and construction which are more directly vulnerable to general shutdown policies and also face greater demand shortages in the future as people are likely to reduce their activities in high-physical contact trades, at least for a time being. According to the data from the Committee of Statistics, in 2019 the share of service sectors contributed for about 55.5 percent in the total value added in Kazakhstan, while the production of goods generated only around 37.5 percent of GDP (Nakipbekov 2020). Thus, the improvement of service sectors in the aggregate economy activity is immensely important.

At the same time, service sectors, informal employment, and small firms are at a greater risk of business failures and voluntary closures due to blanket lockdown policies. Informal jobs are often not covered by employment protection instruments, which among other things include firing restrictions and severance payments. Thus, informal jobs are much more flexible both in terms of separation and hiring decisions, and so they are likely to get destroyed first as soon as the shutdown hits, but also recover more rapidly than those in formal employment. In addition, the firm size determines the likelihood of the business’ survival and the jobs attached to those sectors. Hence, larger firms can rely on greater cash reserves and easier, cheaper credit lines, which can preserve employment for longer periods of time. On the other hand, smaller firms operate on much more limited reserves and frequently have a constrained access to emergency loans, such that it is harder for them to keep people employed.

In the case of Kazakhstan, the share of small- and medium-size firms employment is significant, which means high economic risks for short-term destruction of jobs in these sectors. Figure 2 shows that for about the last five years, the share of small- and medium-size firms employment comprise about 40 percent out of total labor force. In addition, as seen in Figure 3 the value added in aggregate output (national GDP estimates) is also substantial. Recently, the share of small and medium firms has risen (2015-2018), and small and medium enterprises steadily contribute about 30 percent of Kazakhstan’s GDP. The aggregate statistics demonstrate that strict lockdown policies can seriously damage the economic activity, both in terms of income losses and jobs preservation schemes, which can start demand-induced business failures in the longer-term.

It is also important to analyze the regional distribution of small- and medium-size firms employment in Kazakhstan. Thus, as the Figure 4 reports, the average employment and lower bound of small and medium enterprises employment in all the regions is between 20 and 30 percent. In particular, the southern regions (Almaty oblast, Zhambyl oblast, Kyzylorda oblast, Turkistan oblast) exhibit a lower share of small-size firms’ employment on average than other regions. The natural resource-rich regions of West-Kazakhstan (Atyrau oblast, Mangystau oblast, and West-Kazakhstan oblast) employ about 40 percent of the entire regional workforce in small and medium enterprises. This can be explained by the prevalence of service sectors responding to a greater demand for the development of large mining industries. At the same time, a larger need for service sector employment might attract workers from the southern regions as well. Apart from regional disparities, the two largest outliers are the cities of Nur-Sultan and Almaty, which both account for more than 60 percent in small and medium business employment. Thus, we can conjecture that small-size firms’ employment is mostly concentrated in large cities and administrative centers of oblasts, and strict lockdown measures pose a potential risk of lost incomes and jobs for workers employed in these larger urban areas.

Unemployment

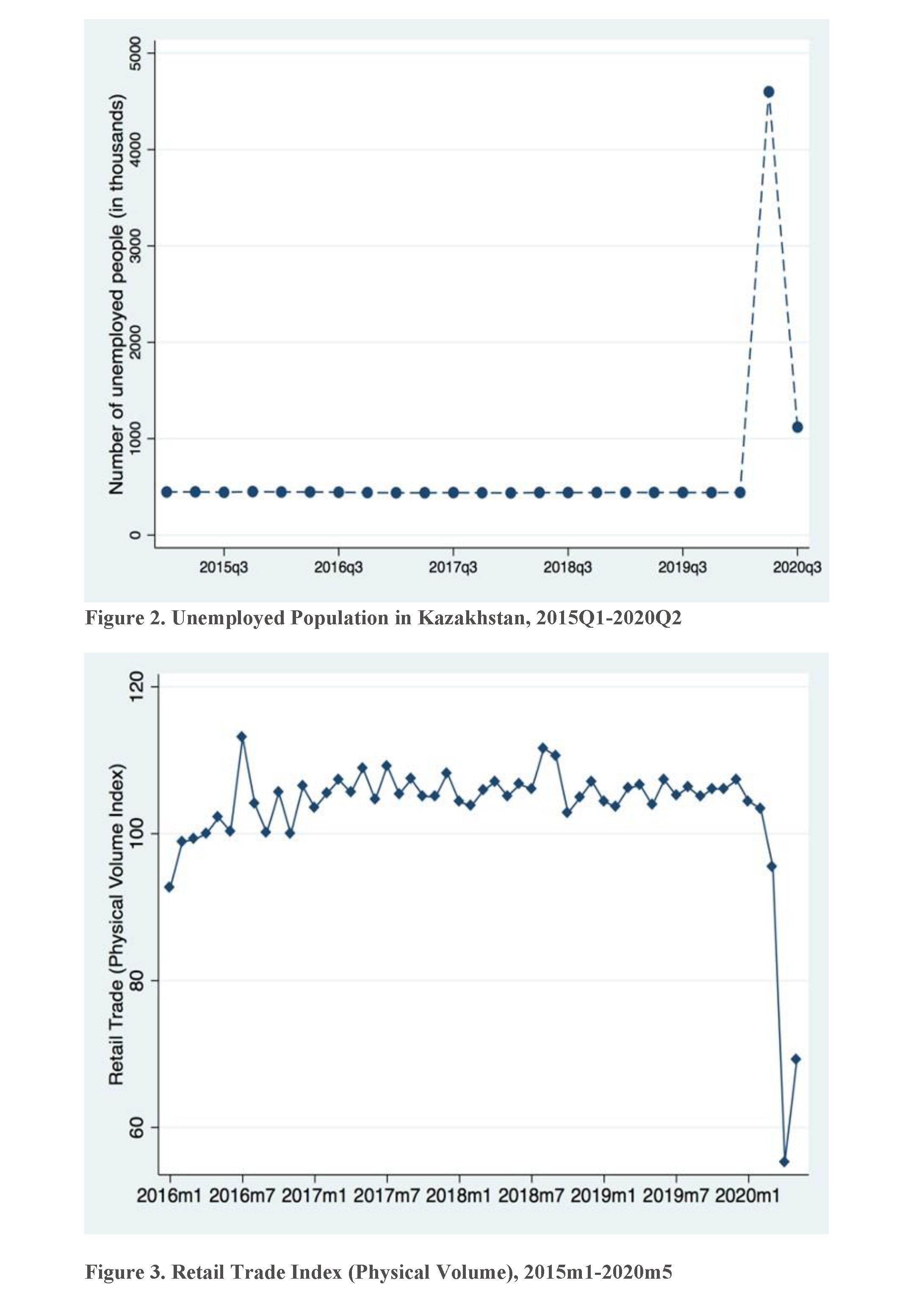

With the launch of the state of emergency measures and subsequent general lockdown policy, the government shortly afterwards started to issue direct social payments, equal to one minimum monthly wage (42,500 tenge or about $100), to all those who lost jobs and sources of income due to the coronavirus pandemic (Ministry of Labor and Social Protection 2020). The majority of the population quickly responded to the call, massively applying online to the financial assistance. Since the state of emergency lasted two months, the Ministry of Labor and Social Protection has scheduled to transfer funds two times, for the months of March and April, to all those who applied in a timely manner. The scope of the program proved to be unprecedented, and in addition for obvious social aid purposes, this is used as an indicator to sketch out the depth of the economic downturn and estimate the relative magnitude of real-time unemployment caused by COVID-19 disruptions.

According to the data from the Ministry of Labor and Social Protection, 8 million people applied for social assistance (out of 9.2 million people in total labor force as of Q1 2020 as shown in Table 3). A total of 4.6 million people received the payments, with 2.9 million people collecting the payment in the second month as well. Therefore, it is possible to derive the hypothetical effects of the unemployment rate in Kazakhstan. Thus, as it is clear from Figure 5, for a significant period of time before the COVID-19 pandemic, the number of unemployed people fluctuated around 400,000-500,000 people quarterly, which corresponds to about 4.9 percent of the unemployment rate. We assume that those who applied for the direct social assistance program temporarily lost their jobs and were technically out of employment for the period of the lockdown. Hence, as the Ministry of Labor and Social Protection has later reported, after relaxing some strict lockdown measures on 20 April, 2020 (the state of emergency and blanket lockdown ended on 11 May, 2020) a considerable part of the population was able to return to work. Thus, according to the estimates from the Ministry of Labor and Social Protection, in the period of May-June 2020, there were approximately 1,140,000 unemployed people (Ministry of Labor and Social Protection 2020). The agency is forecasting a 6.1 percent unemployment rate by the end of the year, which is equivalent to about 700,000 people out of employment. Overall, 4.6 million people who received the social payment from the government during the lockdown (around 50 percent of total labor force) is nearly 10 times greater than the typical structural unemployment numbers of 450,000 people before the pandemic, which principally represents the sheer economic cost of the pandemic-induced supply shock. While the effect may rapidly be reversed to a degree, the economic scar is likely to have long-term depressing impacts on jobs and aggregate income in Kazakhstan.

|

Table 3. Total Labor Force in Kazakhstan (number of people 15+), 2015Q1-2020Q2 |

|

|

2017Q1 |

8,893,360 |

|

2017Q2 |

8,980,289 |

|

2017Q3 |

9,013,097 |

|

2017Q4 |

8,980,623 |

|

2018Q1 |

8,976,709 |

|

2018Q2 |

9,078,885 |

|

2018Q3 |

9,169,455 |

|

2018Q4 |

9,151,635 |

|

2019Q1 |

9,175,422 |

|

2019Q2 |

9,204,749 |

|

2019Q3 |

9,215,323 |

|

2019Q4 |

9,214,796 |

|

2020Q1 |

9,236,463 |

Another source of statistics on economic activity, which helps grasp the depth of the coronavirus-induced economic downturn, is the dynamics of the retail trade, measured by the physical volume index, presented in Figure 6. As we have mentioned earlier, the production of services accounts for about 55.5 percent of total value added in the country, so the impact on retail trade capacity bears a significant adverse impact on the overall potential economic output. In particular, the index first fell 7 percent in March of 2020, with a staggering 42 percent crash in the month of April. Nevertheless, the retail index rose by 25 percent in the following month of May, which simultaneously signaled the lowest point of the trade statistics. Again, the retail trade index dynamics illustrates that the effect of a strict lockdown contributed for around half of lost output (aggregate income) in a given period of 1.5 months, which is roughly identical to 8 percent of annual GDP. The economic consequences of such magnitudes imply that in the shortterm people can consume less, which will cascade down on the negative ability of firms to recover and restart their businesses.

Exchange Rate and Inflation

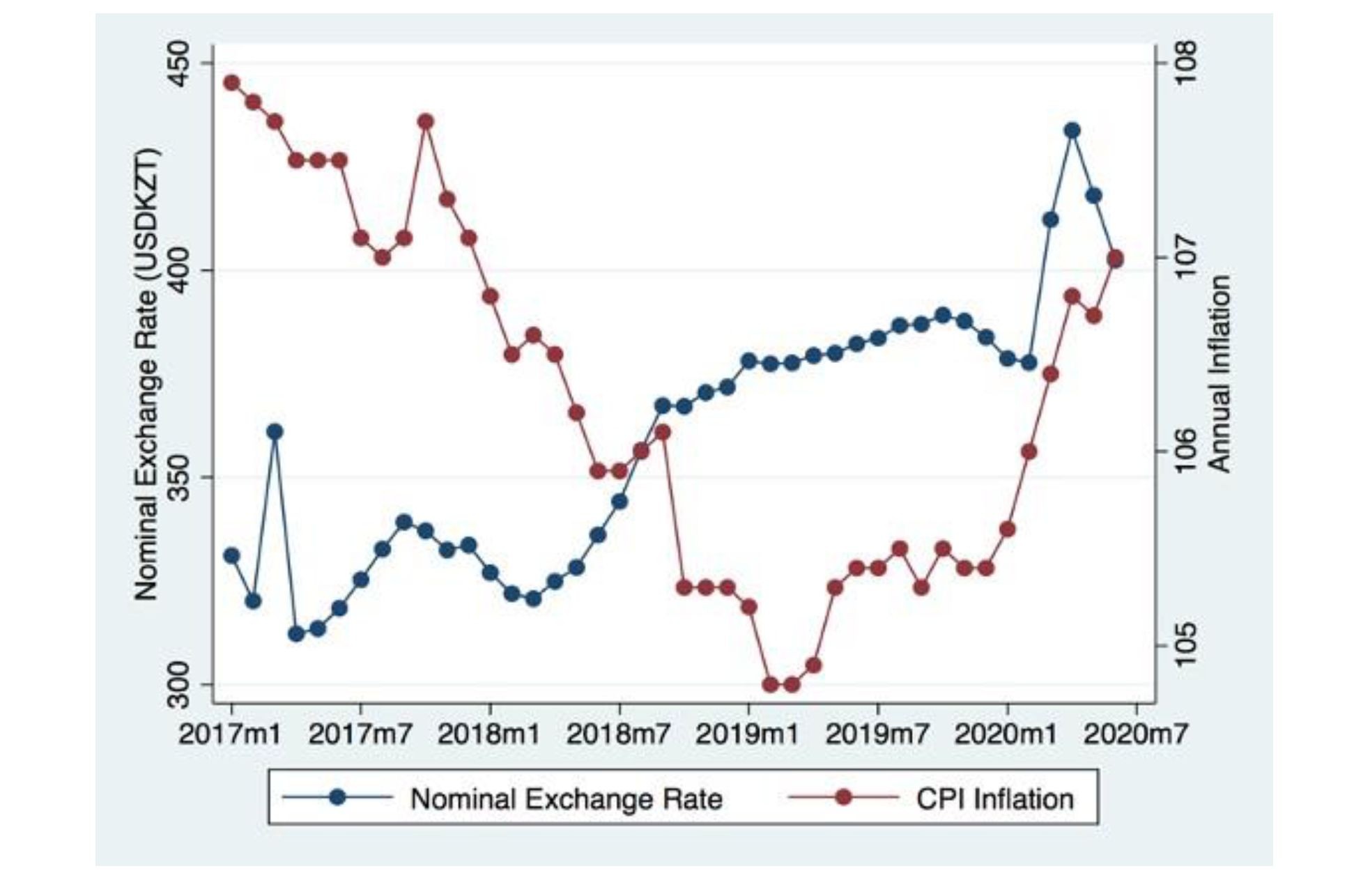

A set of major macroeconomic effects of the double-mixed oil and coronavirus shock has its impact on the exchange rate and inflation (Figure 7). The effect on the aggregate demand in Kazakhstan is typically transferred through the value of currency as a large share of the domestic consumption, and contains imported goods and services. Following the drop in oil prices, the domestic currency, tenge, initially depreciated rapidly, reaching 450 tenge to 1 USD at its lowest point in March 2020, which accounts for about a 20 percent decline from its previous average trend value. However, subsequently in the months of April and May, the national currency bounced back to the level of around 400 tenge per 1 USD and remained relatively stable around this newly elevated level. This level now represents about a 5 percent decrease in the international value of the national currency, and has some important implications for domestic prices.

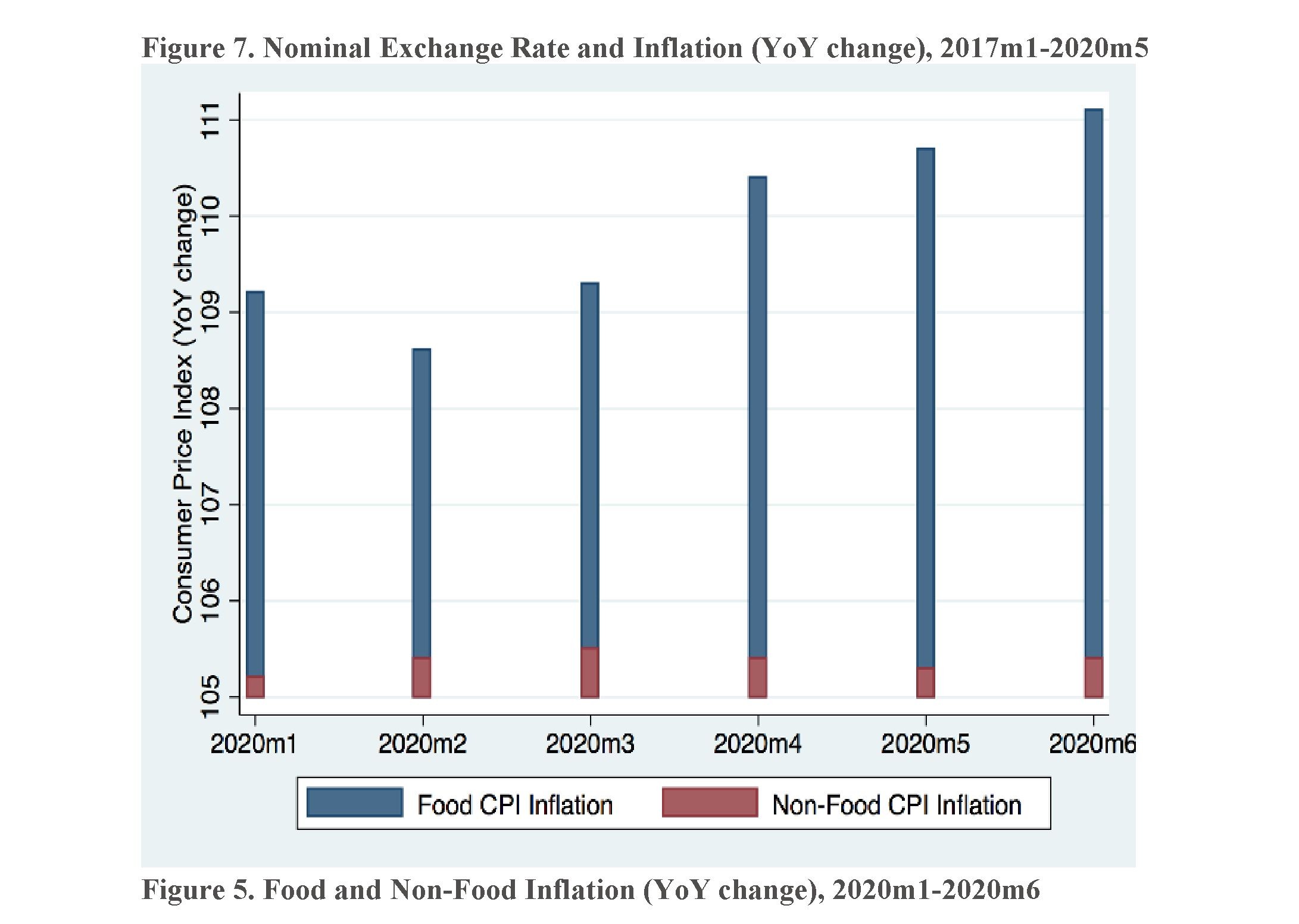

Inflation, a general increase in prices of goods and services, started to accelerate since the beginning of the pandemic, which by decreasing the purchasing power of wages will ultimately lead to a deterioration of economic well being for Kazakhstani citizens. Interestingly, as shown in Figure 8, within the headline of CPI inflation (consumer price index), there is a noticeable pattern of divergence between food and non-food inflation. Thus, since February 2020, food inflation increases sharply, leading to a maximum of 11.1 percent annual increase in June, while the non-food inflation raised only to a relatively modest extent of 5.4 percent. Thus, we can conjecture that the overall increase in domestic prices is primarily driven by food-inflation, a major spending item for low-to-middle income groups of population. The source of higher foodinflation might reflect both an increased excess demand for food products during the lockdown and a decrease in the value of the domestic currency as a substantial amount of food commodities is imported. Thus, to tackle the economic threat from the COVID-19 pandemic on rapid worsening of people’s economic conditions, the government’s fiscal response should also take into account accelerating food-inflation.

Kazakhstan’s government announced a relief package to help both businesses and workers emerge from the lockdown period, and reportedly designated around $13 billion dollars on pandemic response, which accounts for about 8 percent of GDP. On 25 June, 2020 the Asian Development Bank approved a $1 billion assistance package to help Kazakhstan mitigate the health, social, and economic impacts of the coronavirus pandemic. In particular, ADB is aiming to support a comprehensive COVID-19 health policy response, social protection and employment protection measures, and an economic stimulus plan introduced by the government to alleviate the adverse impacts of the pandemic (ADB 2020).

Due to the increased number of infections and deaths, on 29 June, 2020 the government adopted additional measures to mitigate the spread of COVID-19, which includes a significant improvement of mass testing capacities and an increase in domestic production of medical supplies. Also, Kazakhstan ultimately imposed a second national lockdown starting 5 July, 2020 until 2 August, 2020.

Executive Summary

- It is highly likely that the current situation with COVID-19 will result in the onset of one of the deepest crises in Kazakhstan since the break-up of the USSR, as COVID-19 has caused a global economic crisis whose scope is still difficult to fully assess.

- Based on the comparative analysis with other countries, the lockdown period in Kazakhstan may last 2-2.5 months.

- In today’s market, the most vulnerable industries are SMEs, non-food retail, aviation, oil and gas, mining, transport, the power and utilities sectors.

19

19

- Measures to reduce administrative expenses have been taken by 74% of respondents. About half of respondents are working proactively on optimising procurement (restructuring of accounts payable, optimisation of logistics, reviews of order books, and the deferral of some procurements to a later date).

- Companies operating in all sectors of the economy (other than telecoms) have put on hold implementation of capital-intensive investment projects or are considering “less costly” options for the implementation of such projects.

- Most market players are developing and deploying an anti-crisis action plan and intend to revise their development strategy. Virtually all companies are focused on the accelerated digitisation of their sales channels, and interaction channels with clients in the near future.

- The representatives of major Kazakhstani businesses consider the announced government support measures to be insufficient and expect assistance in the form of tax breaks (including VAT refunds to export-oriented enterprises and companies operating in the aviation sector), the reimbursement of some expenses and preferential loans.

- About 86% of respondents believe that a gradual return to pre-crisis positions will occur no earlier than in three to four quarters (or later), which suggests that the consequences of the crisis may also be observed in 2021.

- The crisis will lead to significant changes in behavioural responses and the need for the government to rethink approaches to maintaining health safety. In addition, the crisis will result in a significant change in the business landscape and adjustments to strategic goal setting by both the government and business.

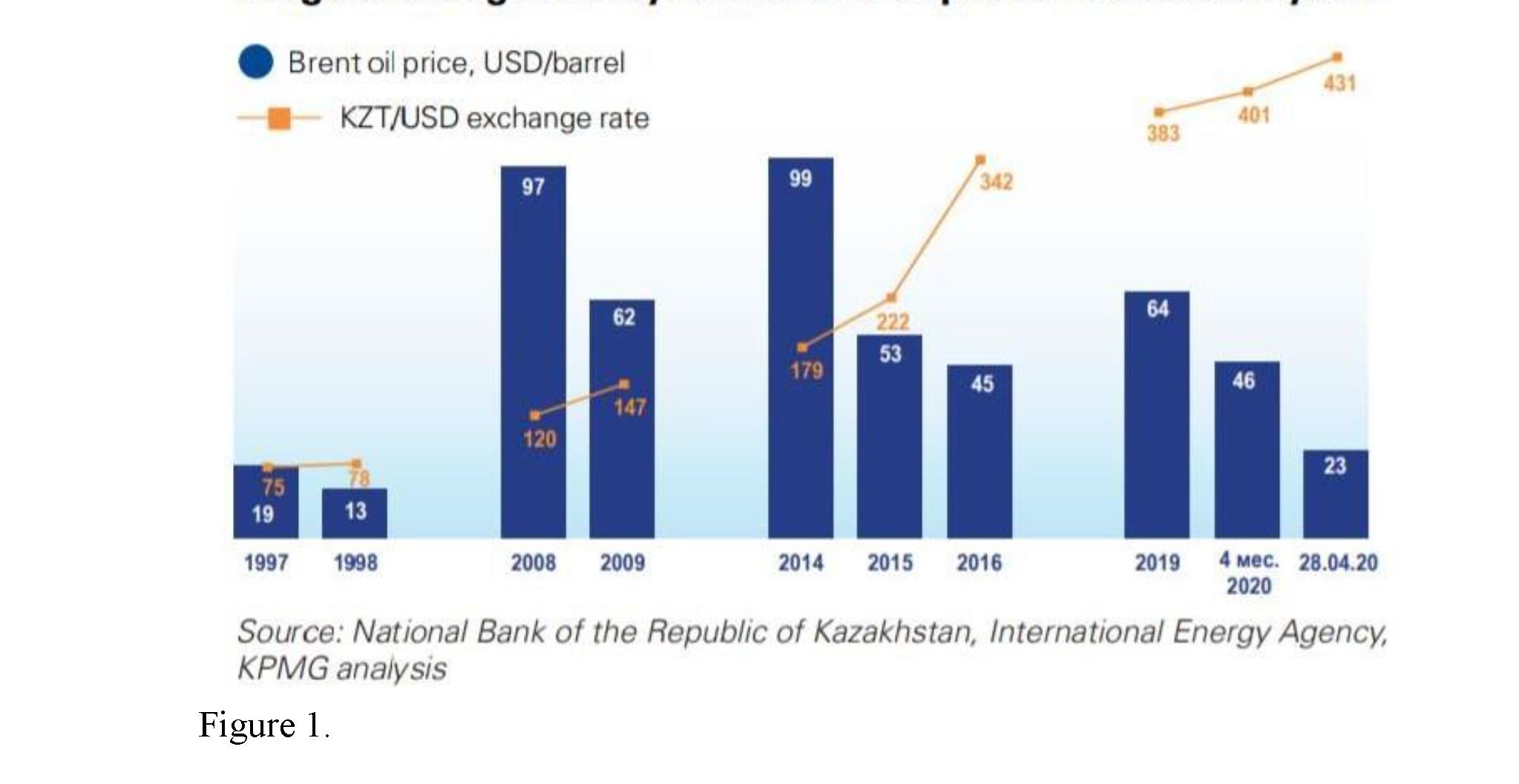

The devaluation of the tenge caused by falling oil prices and decreasing demand for base metals will have an adverse impact on consumer demand, but will also strengthen the competitive positions of enterprises operating in the export-oriented industries of Kazakhstan.

- 1 https://centralasiaprogram.org/archives/16542

- 2 https://assets.kpmg/content/dam/kpmg/kz/pdf/2020/05/Impact-of-COVID-19-on-the-key-economic-sectors-of-Kazakhstan.pdf

- 3 https://www.oecd.org/eurasia/competitiveness-programme/central-asia/COVID-19-CRISIS-IN-KAZAKHSTAN.pdf