Abstract

Object: to determine the main directions of strengthening the financial base of local self-government in modern conditions in the framework of the implementation of national policies in the field of socio-economic development of territories.

Methods: The scientific abstraction method supported with information analysis and grouping.

Findings: The results of the analysis of the main characteristics of budgets of the fourth level and the proposed ways to strengthen the revenue base of local self-government contribute to the improvement of the theory of the budget process and inter-budget relations, as well as the development of methodological foundations for the formation of local budgets. The main factor limiting the independence of local governments in the formation of the local budget is the high level of concentration of the country's income (tax) potential at the stage of its primary distribution due to the model of budget-redistributive relations used.

Conclusions: By analyzing the problems of the fourth-level budgets, the directions of strengthening the financial base of local self-government were identified, the main of which are increasing the interest of rural districts in building revenue potential, improving medium-term planning, introducing progressive forms and methods of managing local finances.

The existence of territorial entities in the state structure of the country makes it necessary to give them certain responsibilities and the amount of financial resources to ensure life in them (Tysiac, 2018). In this connection, the structure of the financial system allocates a special link in the local budgets, uniting the revenues and expenditures of the local entity.

Increasing the level of financial independence of territorial entities is considered one of the areas of modernization in the modern financial management system. To address issues of local importance the authorities are obliged to make the most complete use of budget resources.

On the one hand, the use of all the designated means guarantees the local self-government bodies the full exercise of their powers, on the other hand, a system of direct and inverse relationships is formed in the performance of all tasks.

The local budget represents a monetary fund of an administrative-territorial unit and is approved by a decision of the relevant maslikhat. It is formed at the expense of revenues and financing the deficit (use of surplus) of the budget and intended to finance local budget programs that are determined by the local executive body to perform its functions (Schwartz et al., 2014).

The role of local budgets, their composition and structure are fully determined by the content and nature of functions and tasks assigned to local government bodies, as well as by the administrative and territorial structure of the state and its political and economic orientation (Sponem & Lambert, 2016).

One of the most important principles of any democratic system is the system of state governance, and the world practice of this very governance reforming shows that the specificity of local self-government largely predetermines the limits of decentralization (Mahlendorf et al., 2015). At the same time, the general trend of the reforms carried out is that they are aimed at eliminating a number of circumstances, first of all those that negatively affect the development of local self-government (Shajhraziev, 2012).

Referring to the essence of local self-government, it should be noted that it represents a certain way of organizing and implementing local government, providing for independent resolution of local issues by the population (Luca et al., 2016).

The latter is due to the fact that local self-government is implemented directly by the residents as well as through elected and other local self-government bodies established in rural and urban communities of citizens. These communities, in their turn, represent associations of citizens who compactly live within a certain territory (Vasiliev, 2015).

Modern world practice shows that there are many models of local self-government, but it is undeniable that local relations in the world have evolved in different ways, and in the current environment these relations acquire new features.

Some steps in this direction have already been taken by now. In the Message of the President of Kazakhstan, the Leader of the Nation N.A. Nazarbayev to the people of Kazakhstan “Strategy Kazakhstan-2050 New political course of the established state” the goal of forming a new type of public administration was set. Herewith, one of the tools to achieve this goal is decentralization and local self-government development.

In accordance with this task the Republic of Kazakhstan has developed and approved the “Concept of development of local self-government in the Republic of Kazakhstan”. Mainly, it is aimed at both defining the main conceptual directions of development of local self-government in Kazakhstan, and improving the effectiveness of the current system of public administration. It should be noted that this Concept absorbed all universally recognized values of local self-government, democracy and predetermined further stages of development of self-government in Kazakhstan.

Thus, according to the Concept, the development of local self-government in Kazakhstan is carried out in two consecutive stages. The first stage, covering the period of 2013–2014, was aimed at expanding the existing system at lower levels of government. At this stage, norms determining the powers of local authorities, activity of meetings of local community, the order of election of akims of cities of district importance, villages, settlements and rural districts were fixed. The expansion of the financial independence of village akims included the right to form revenue sources and open cash control accounts.

To date, elections of akims of cities of district importance, rural districts, towns and villages have become a reality in Kazakhstan. Thus, local self-government has received a legislatively fixed basis for its further development. The scale of this project testifies to the readiness of the state for more significant actions aimed at modernization of the state administration system. The election of local akims should give an impetus to the transition of state administration to a new qualitative level.

The goal of the second stage, covering the periods of 2015–2020, was to further delineate the functions of local government and self-government, budget formation and local self-government property.

Taking into account that the creation of an effective system of local self-government bodies is based on expanding economic and financial independence of rural districts, certain steps have been taken at this stage of local self-government development. Thus, in January 2001 the Law of the Republic of Kazakhstan “On amendments and additions to some legislative acts of the Republic of Kazakhstan on the development of local self-government in the Republic of Kazakhstan” was adopted (was amended on 08/01/2019), providing for the expansion of the revenue base of cash control accounts through the transfer of taxes on transport and land tax on legal entities to local governments.

Moreover, it is envisaged to expand the powers of the local community meeting to coordinate the candidacy of the local akim to participate in the elections and initiate his release. It became possible to create public structures for interaction between the akim and the population, to expand the akim's powers to control the targeted use of land plots, and to involve residents in the process of managing communal property.

The most important thing is that the new draft law prescribes the implementation of an independent budget and communal property. The solution of various issues of local importance within the framework of the Concept of Local Self-Government Development acquires new qualities that are adequate to the modern principles of the budget system. The availability of a budget for each of them strengthens their economic independence, activates economic activity, and allows them to design their own development programs and implement them in practice.

Local self-governance implies the resolution of issues of local importance with the participation of the population living on the territory. Financing of decisions of questions of local value, sources of formation of financing are the most important for development of local self-government.

As the world practice shows, today certain conditions of financial support of local government bodies have been formed, among them the following (Stammerjohan et al., 2015):

- the possibility of independent management of financial resources, enshrined in the legislation;

- the volume of financial resources of local authorities corresponds to their functions provided for by the Constitution and legal acts of the country;

- ability to form their own sources of income and local taxes and set rates of local taxes and fees;

- compensation of missing funds by the central government bodies;

- independent decision-making related to the management of financial resources and local government property;

- the possibility of issuing securities and obtaining loans and credits.

The Law of the Republic of Kazakhstan “On Amendments and Additions to Some Legislative Acts of the Republic of Kazakhstan on Development of Local Self-Government” dated 11 July 2017 specifies some changes related to the introduction of an independent budget and communal property of local selfgovernment in cities of district significance, villages, settlements and rural districts.

It should be noted that in many cases the introduction of an independent budget of rural districts is caused primarily by an apparent imbalance in fiscal policy and inter-budgetary relations, which resulted in the fact that tax revenues from various enterprises entering the republican budget were redistributed among all regions of Kazakhstan without taking into account their contributions. Moreover, as practice has shown, the previous system of distributing financial aid to lower budgets had a disincentive effect on local selfgovernment development. As a result, budgets with a low level of own income were in a better position compared to donor budgets. The authorities of the latter were interested in a decrease in their own revenues, the income tendency of which was characterized by temporary unevenness, while financial aid is received regularly and in the prescribed amounts. Thus, there was no motivation to develop entrepreneurship, small and medium businesses in their regions, as local authorities received a guaranteed transfer in any case.

The effectiveness of local self-government is largely determined by the availability of financial resources necessary to solve local problems, as well as to participate in the implementation of national policies in the field of socio-economic development of territories. At the same time, the local budget is a key form of formation of financial resources of local self-government bodies, which is a set of monetary relations arising in connection with the formation and use of funds of local self-government in the process of redistribution of national income. A wide range of various sources of official information was processed, including normative legal and strategic policy documents, statistical data, scientific and specialized publications, information and reference materials of international organizations.

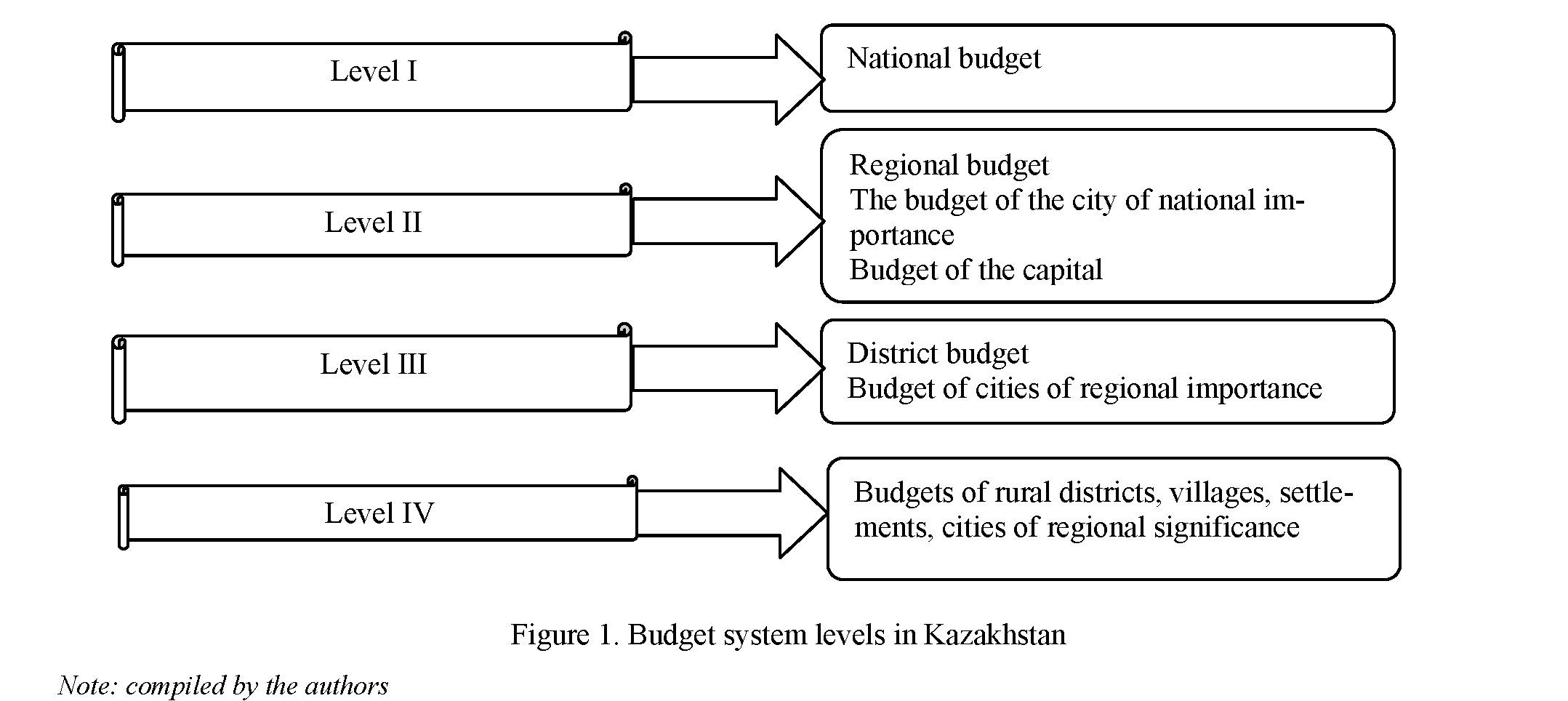

The developed system of formation of a profitable part of local budgets did not provide financial independence of regions, in particular local self-government (Schoute & Wiersma, 2011). Thus, it became necessary to narrow the scope of redistributive processes in interbudgetary relations by increasing the responsibility of local self-government bodies for developing their own tax potential in the territories of the respective territorial entities and strengthening the financial foundations of local self-government. From January 1, 2018, an independent budget of local self-government was introduced at the level of a rural district, aul, village, settlement or city of regional significance, corresponding to Level IV of the budget system schematically shown in Figure 1.

When developing legal acts on the implementation of the fourth level of the budget in Kazakhstan, the experience of implementing an independent budget of local self-government in individual countries of the Organization for Economic Cooperation and Development (OECD), in particular Poland, in which the administrative-territorial division is generally similar to the conditions of Kazakhstan, was studied. In the early 1990s, the Polish government implemented a good reform to strengthen local government units (gminas) and give them some financial independence. Eventually, in 1997, a certain independence in the competence of municipalities was introduced into the Polish Constitution. Currently Polish gminas are well-functioning administrative units that are positively evaluated by the population. They are also an example of gradually developing institutions that provide a good quality of life to their residents.

27

The experience of Poland corresponds to the conditions of Kazakhstan. In the years before the reform of local self-government, Poland endured systematic transitions, both political and economic, very similar to what happened in Kazakhstan after the collapse of the USSR. Before the reform, Poland had four administrative levels, three of which had an independent budget, just like Kazakhstan. Poland and Kazakhstan have almost the same number of local administrative-territorial units (2479 gminas in Poland, 2445 auls, districts and cities of district significance in Kazakhstan).

The formation of the Level 4 budget expands the akims’ capacity to solve topical issues of community development. Moreover, the local authorities will be interested in maximizing the timely receipt of local taxes, increasing the taxable base, and developing business activities (Murphy, 2017). All this will increase the revenue part of the district’s budget and provide more opportunities for the implementation of community development programs. Such innovations allow the population to solve local problems on their own, since akims of aul (villages), settlements and towns of significance are.

- Permitted the right to form their own revenue sources, including income from paid services; voluntary and earmarked fees; contributions of charitable foundations and sponsors; fees for trade in specially designated places; fines for violations of the rules of improvement, damage to infrastructure facilities and greenery, trade in unidentified places and other sources not contrary to law.

- Permitted the right to open special accounts within the treasury bodies that reflect income and expenditures aimed at implementing local self-government functions;

- A part of the district communal property (clubs, libraries, nurseries, etc.) has been transferred in order to use them effectively, meeting the needs and demands of the local population and generating additional income.

The local self-government budget at the level of a city of regional significance, a village, a settlement or a rural administrative district shall be introduced as the fourth level of the state budget from 2018 in administrative territorial units with a population of over 2,000. In the future similar events are planned to be held throughout Kazakhstan.

In general, the state budget of the IV level was implemented in 1062 rural districts with population exceeding 2000 citizens. Among them is Kalkaman rural district, belonging to the rural zone of Aksu city of Pavlodar region, by the example of which let's consider the mechanism of formation of local government budget and sources of their income.

Kalkaman rural district is subordinated to Aksu city akimat, which is an industrially developed region of Pavlodar region. Economic specialization of Aksu city has industrial character and in the long term has high potential for development.

In accordance with the paragraph 2 of Article 75 of the Budget Code of the Republic of Kazakhstan dated 04 December 2008, subparagraph 1) of paragraph 1 of Article 63 of the Law of the Republic of Kazakhstan dated 23 January 2001 “On local government and self-government in the Republic of Kazakhstan”,

Aksu City Maslikhat approved the budget of the Kalkaman Rural District for 2018–2020 in the amount of 113251 thousand tenge.

According to the data of Table 1, this is the largest budget size among rural districts of Aksu city, which 3.1 times exceeds the budget size of Kyzylzhar rural district, which is the minimum. Thus the largest part of a profitable part of the budget of Kalkaman rural district for 2018–2020 — 94,1 % from total amount is formed at the expense of receipt of transfers in the sum of 106588 thousand tenge.

Table 1. Budget volumes of rural districts of Aksu city on January 1, 2018, thousand tenge

|

The name of the rural district |

Total amount of budget |

including |

Transfers |

In total, including transfers |

|

|

own resources |

subvention |

||||

|

Apparatus of the Akim of Kalkaman Rural District |

113251 |

6663 |

106588 |

3750 |

117001 |

|

Apparatus of the Akim of Kyzylzhar Rural district |

36491 |

4978 |

31513 |

3750 |

40241 |

|

Apparatus of the Akim of Yevgenyevskiy Rural district |

48683 |

6253 |

42430 |

3750 |

52433 |

|

Apparatus of the Akim of Dostyk Rural District |

42869 |

5885 |

36984 |

3750 |

46619 |

|

Apparatus of the Akim of Algabas Rural District |

54759 |

5218 |

49541 |

3750 |

58509 |

|

Apparatus of the Akim of rural district named after M. Omarov |

50606 |

4878 |

45728 |

3750 |

54356 |

Note: compiled by the authors based on data of Department of economy and budget planning of Aksu city, 2018

The above-mentioned Law determines the revenue sources of the local government budget, consisting of tax revenues:

- individual income tax on income not taxed at payment sources;

- property tax on individuals;

- transport tax on individuals and legal entities;

- land tax from individuals and legal entities on the lands of settlements;

fees for the placement of outdoor (visual) advertising on the freeway right-of-way passing through the territories of towns, villages, settlements and rural districts;

non-tax revenues (income from property hire (rent) of state property);

voluntary fees of individuals and legal entities;

fines levied by akims for administrative offences under the Code on Administrative Offences;

revenues from the sale of communal property; transfers from the raion budget.

As can be seen from the data in Table 2, the tax receipts determining the revenue part of the budget of Kalkaman Rural District generate property taxes, including property tax, land tax and vehicle tax.

Table 2. Budget of Kalkaman Rural District for 2018–2020, thousand tenge

|

Indicators |

2018 |

2019 |

2020 |

|

1. Revenues |

113251 |

116635 |

116935 |

|

Tax revenue |

6663 |

7000 |

7300 |

|

- personal income tax |

1922 |

1922 |

1922 |

|

- taxes on property |

130 |

130 |

130 |

|

- land tax |

298 |

290 |

298 |

|

- vehicle tax |

4313 |

4650 |

4950 |

|

Transfer receipts |

106588 |

109635 |

109635 |

|

2. Expenses, including: |

113251 |

116635 |

116935 |

|

Public services of general nature |

22340 |

22407 |

22467 |

|

Education |

54053 |

55819 |

55939 |

|

Social assistance and social security |

8223 |

8617 |

8677 |

|

Housing and communal services |

8130 |

8130 |

8130 |

|

Culture, sport, tourism and information space |

17518 |

18675 |

18735 |

|

Transport and communications |

1500 |

1500 |

1500 |

|

Others |

1487 |

1487 |

1487 |

|

Note: compiled by the authors based on data of Department of economy and budget planning of Aksu city, 2018 |

|||

The budget of Kalkaman Rural District is balanced, the social profile of the budget will be kept, the budget deficit in 2018–2020 is not expected.

The priority areas of budget spending in the medium term are further development of the social sphere, utilities and transport infrastructure, and drinking water supply.

Budget planning and execution are the responsibility of the Rural District Akim’s Office. In other words, the akimat plans expenditures that will be used to support pre-school education and training organizations, cultural institutions, landscaping and sanitary purification of settlements; create infrastructure for sports activities for individuals; build, reconstruct, renovate and maintain roads; provide water to settlements.

As can be seen in Table 3, the majority of planned expenditures — almost half of the total — are in the education sector.

Table 3. The structure of Kalkaman rural district budget expenditures, percentage for 2018–2020

|

Indicators |

2018 |

2019 |

2020 |

|

Public services of general nature, % |

19,7 |

19,2 |

19,2 |

|

Education, % |

47,7 |

47,9 |

47,8 |

|

Social assistance and social security, % |

7,3 |

7,4 |

7,3 |

|

Housing and communal services, % |

7,2 |

7,0 |

7,0 |

|

Culture, sport, tourism and information space, % |

15,5 |

16,0 |

16,0 |

|

Transport and communications, % |

1,1 |

1,1 |

1,1 |

|

Others, % |

1,5 |

1,4 |

1,6 |

|

Note: compiled by the authors |

|||

As national and foreign practice shows, the existence of a mechanism of responsibility and effective control over targeted spending of local government budget funds is a guarantee of stable development of the territorial entity (Nikias, 2019).

At the same time, the strategy for creating and effectively using the financial base of local selfgovernment should include three interrelated structural components:

– First, the formation of prognostic and analytical documents providing a justification for the goals and objectives and priorities of community development (Parker et al., 2014). In addition, the requirements to the size of the financial base sufficient to address social and economic problems of local self-government are defined (Libby & Lindsay, 2019).

– Secondly, the choice and substantiation of the most preferable from the standpoint of the local community main directions and ways to strengthen the financial base of its self-government. Herewith, the key element at this stage is the construction of constructive relations between the budgets of different levels: the budget of local self-government, the budget of the region, the state budget, between the budget of local selfgovernment and the financial and economic potential of economic entities of the territory. The latter is due to the fact that the sufficiency of the financial base of the rural district is largely determined by the resource potential of entrepreneurship in its territory.

– And thirdly, according to data of SF Center for economic research, forecasting and monitoring about financial and economic foundations of local self-government in the Republic of Kazakhstan, the formation and functioning of an effective mechanism for redistribution of financial resources between the budgets of different levels, taking into account the accumulated territorial potential.

The introduction of the local government budget by receiving taxes directly into its budget has really expanded the financial capacity of rural districts and strengthened the role of local government in solving local issues. At the same time, the period of implementation of the fourth level of the budget shows a low provision of expenditures of rural budgets with their own income.

With the granted independence, the budgets of rural districts, villages and settlements remain subsidized by more than 75 %, and in some regions — by more than 90 %. It is also necessary to note the gap in the indicators of the provision of local government budgets with their own revenues, which ranges from 1 % of the provision with their own revenues to the 25 % stated in the Minister's report. For example, the budget of the village with the population of more than 10 thousand people is 320 million tenge, of which own income is 24 million tenge, or 7,6 %. Moreover, due to the tax holidays for small businesses since the beginning of 2020, the financial independence of villages has significantly decreased.

Naturally, in these conditions an additional transfer of a number of separate types of taxes and payments from the higher budget to the rural level is necessary. For example, the transfer of fees for the use of land plots, a single land tax, proceeds from the sale of land plots and the right to lease land plots will increase the share of own revenues of local government budgets by 10–15 %.

The Ministry of Finance and other government bodies do not publish information on the implementation of the fourth-level budgets and the current norms for the distribution of tax revenues established by the regional authorities. Nevertheless, it is obvious that the filling of the budgets of district centers and villages depends on the regional authorities to no less extent than the filling of regional budgets depends on the decisions of the central government.

This approach to the distribution of income largely discourages the activity of local authorities in the implementation of economic policies aimed at the development of regions and individual localities. Stimulating regional business activity largely loses its meaning in the eyes of local authorities due to the fact that it does not lead to an increase in revenues to the local treasury. At the same time, the current budget policy causes hidden disapproval among the regional elites in the regions where the highest volumes of tax payments are collected. On the other hand, the rejection of the distributional system can seriously increase the level of economic and social inequality between different regions.

At the same time, the coronavirus pandemic has a serious negative impact on the filling of local budgets. As a result of the quarantine measures, the receipts of the IIT and taxes paid by SMEs, which account for the lion's share of tax revenues to local budgets, have sharply decreased. Perhaps, in the current conditions, it is necessary to change the budget system in such a way as to leave more taxes in the regions and thereby encourage local authorities to develop the economy in the territories entrusted to them.

To increase the level of security of rural budgets and strengthen their revenue base it is also very important to introduce a unified information base of state bodies. It is advisable to build a management system of financial resources in such a way as to increase the interest of local authorities in finding internal sources of budget revenue, as well as to reduce additional costs.

In general, summarizing the above, it can be concluded that the interbudgetary relations are based on a clear division of functions and authorities between the levels of public administration, a single distribution of revenues and expenditures between the levels of budgets.

The policy of interbudgetary relations in the medium term will be aimed at ensuring public availability and quality of public services.

Effective financial management of local self-government involves several steps:

- Forecasting the amount of financial resources that will be available in the current year and the local issues to be addressed.

- Assessing the needs and requirements of the local community. Needs assessment allows planning local government expenses correctly. The issues that should be solved in the first place, and what issues can be solved by the local community.

- Defining priorities. Identification of current and future priorities makes it possible to create an actual plan for financing local self-government costs and to finance issues that are primarily expected to be addressed by community members.

- Evaluation of the achieved results. Evaluation results can help in the future to plan more effectively, avoid repeating past failures and make timely corrective decisions.

References

- Biudzhetnaia politika goroda Aksu (2018). Budget policy of the city of Aksu]. Aksu. Otdel ekonomiki i biudzhetnogo planirovaniia goroda Aksu — Department of economy and budget planning of Aksu city. economica.aksu.pavlodar.gov.kz. Retrieved from http://economica.aksu.pavlodar.gov.kz/index.php/ru/budgetpolitic. [in Russian].

- Biudzhetnyi kodeks Respubliki Kazakhstan (2020). Budget Code of the Republic of Kazakhstan. akorda.kz. Retrieved from https://online.zakon.kz/document/? doc_id=30364477 [in Russian].

- Finansovo-ekonomicheskie osnovy mestnogo samoupravleniia v Respublike Kazakhstan (2015). [Financial and economic foundations of local self-government in the Republic of Kazakhstan]. Astana. OF “Tsentr ekonomicheskikh issledovanii, prognozirovaniia i monitoring” — SF “Center for economic research, forecasting and monitoring”. ermec.kz. Retrieved from http://ermec.kz/wp-content/uploads/2015/02/rukovod2_.pdf. [in Russian].

- Libby, T. & Lindsay, R. M. (2019). The effects of superior trust and budget-based controls on budgetary gaming and budget value. Journal of Management Accounting Research, 31(3), 153–184. https://doi.org/10.2308/jmar-52238

- Luca, M., Kleinberg, J. & Mullainathan, S. (2016). Algorithms need managers, too: Know how to get the most out of your predictive tools. Harvard Business Review, 1, 96–101. https://doi.org/10.1787/34907e9c-en

- Mahlendorf, M. D., Schaffer, U. & Skiba, O. (2015). Antecedents of participative budgeting — A review of empirical evidence. Advances in Management Accounting, 25, 1–27. https://doi.org/10.1108/S1474–787120150000025001

- Murphy, M. L. (2017). Using surplus budgeting to advance and sustain your mission. Journal of Accountancy, 2, 40–43. https://doi.org/10.1186/s41937–017–0017–4

- Nikias, A. D. (2019). An experimental examination of the effects of information control on budget reporting with relative project evaluation. Journal of Management Accounting Research, 31(2), 177–196. https://doi.org/10.2308/jmar- 52172

- O mestnom gosudarstvennom upravlenii i samoupravlenii v Respublike Kazakhstan. Zakon Respubliki Kazakhstan (2020). Law of the Republic of Kazakhstan “On local government and self-government in the Republic of Kazakhstan”. online.zakon.kz. Retrieved from https://online.zakon.kz/document/? doc_id=1021546 [in Russian].

- O vnesenii izmenenii i dopolnenii v nekotorye zakonodatelnye akty Respubliki Kazakhstan po voprosam razvitiia mestnogo samoupravleniia v Respublike Kazakhstan. Zakon RK (2019). Law of the Republic of Kazakhstan “On amendments and additions to some legislative acts of the Republic of Kazakhstan on the development of local selfgovernment in the Republic of Kazakhstan”. online.zakon.kz. Retrieved from https://online.zakon.kz/document/? doc_id=38280611 [in Russian].

- Parker, R. J., Kohlmeyer, J. M., Mahenthirian, S. & Sincich, T. (2014). Procedural justice and information sharing during the budgeting process. Advances in Management Accounting, 23, 93–112. https://doi.org/10.1108/S1475– 148820140000017003

- Schoute, M. & Wiersma, E. (2011). The relationship between purposes of budget use and budgetary slack. Advances in Management Accounting, 19, 75–107. https://doi.org/10.1108/S1474–7871(2011)0000019010

- Schwartz, S.T., Sudbury, A. & Young, R. A. (2014). A note on the benefits of aggregate evaluation of budget proposals.

- Journal of Management Accounting Research, 26(1), 145–164. https://doi.org/10.6007/IJARBSS/v6-i9/2321

- Shajhraziev, V.G. (2012). O ponjatii funkcii mestnogo samoupravlenija [On the concept of local government functions].

- Gosudarstvennaja vlast’ i mestnoe samoupravlenie — State power and local self-government, 12, 3–5 [in Russian].

- Sponem, S. & Lambert, C. (2016). Exploring differences in budget characteristics, roles and satisfaction: A configurational approach. Management Accounting Research, 3, 47–61. https://doi.org/10.1016/j.mar.2015.11.003

- Stammerjohan, W. W., Leach M. A. & Stammerjohan, C. A. (2015). The moderating effects of power distance on the budgetary participation-performance relationship. Advances in Management Accounting, 25, 103–148. https://doi.org/10.1108/S1474–787120150000025006

- Strategiia Kazakhstan – 2050. Novyi politicheskii kurs sostoiavshegosia gosudarstva (2012). [“Strategy Kazakhstan- 2050. New political course of the established state”]. Stratehii i prohrammy Respubliki Kazakhstan. Ofitsialnyi sait Prezidenta Respubliki Kazakhstan — Strategies and programs of the Republic of Kazakhstan Official website of the President of the Republic of Kazakhstan. akorda.kz. Retrieved from http://www.akorda.kz. [in Russian].

- Tysiac, K. (2018). The benefits of 'budgeting for results’: Beginning with detailed, specific outcomes when building the budget can help not-for-profits attracts impact-driven donors. Journal of Accountancy, 11, 28–32. https://doi.org/10.1080/23311975.2020.1786315

- Vasiliev, V.I. (2015). Mestnoe samoupravlenie: istorija i sovremennaja praktika [Local self-government: history and modern practice]. Zhurnal rossijskogo prava — Journal of Russian law, 3, 5–15 [in Russian].