Abstract

Object: To analyze background and implementation conditions of national digital currency in Kazakhstan in the conditions of digitalization and forecast the development of digital money in Kazakhstan using economic and statistical modelling. To develop the electronic money circulation system, second-tier banks, which are the main subjects of the financial market, provide remote services, develop strategies for general development, which prescribe rational ways to attract customers to remote service, apply modern technologies and improve the system of cashless money circulation, both nationally and internationally.

Methods: Statistical resources of the Committee of statistics of the Ministry of National economy of the Republic of Kazakhstan were used in the paper. Methods of deduction and systematization were applied. In this study an extrapolation forecast was made for the indicator “the volume of payments in the interbank money transfer system and the interbank clearing system” for 2021-2023.

Results: Nowadays financial ecosystems based on digital technologies are being actively implemented. This trend is noticed in different countries of the world. It opens new possibilities for development of national currencies. Commercial banks are creating new types of digital money by incorporating them into traditional economic interactions.

Conclusion: Kazakhstan is a perspective region for the implementation of its own digital currency. The country's unique geographical position, economic relationships with China, Russia and the West, the presence of international technology giants in the country make the electronic tenge a popular financial instrument that will significantly improve the competitiveness of the Kazakhstani economy, increase its attractiveness with similar projects from other countries at the global level. The concept of introducing digital currency and its transition to widespread use in Kazakhstan will ensure not only the creation and development of completely new ecosystems of financial products and services, but also the modernization of existing “traditional” ones.

The introduction and widespread use of new generation of digital currencies will help to change payment, clearing and interbank settlements significantly, increasing their efficiency, security, instant settlements and reducing financial transaction risks.

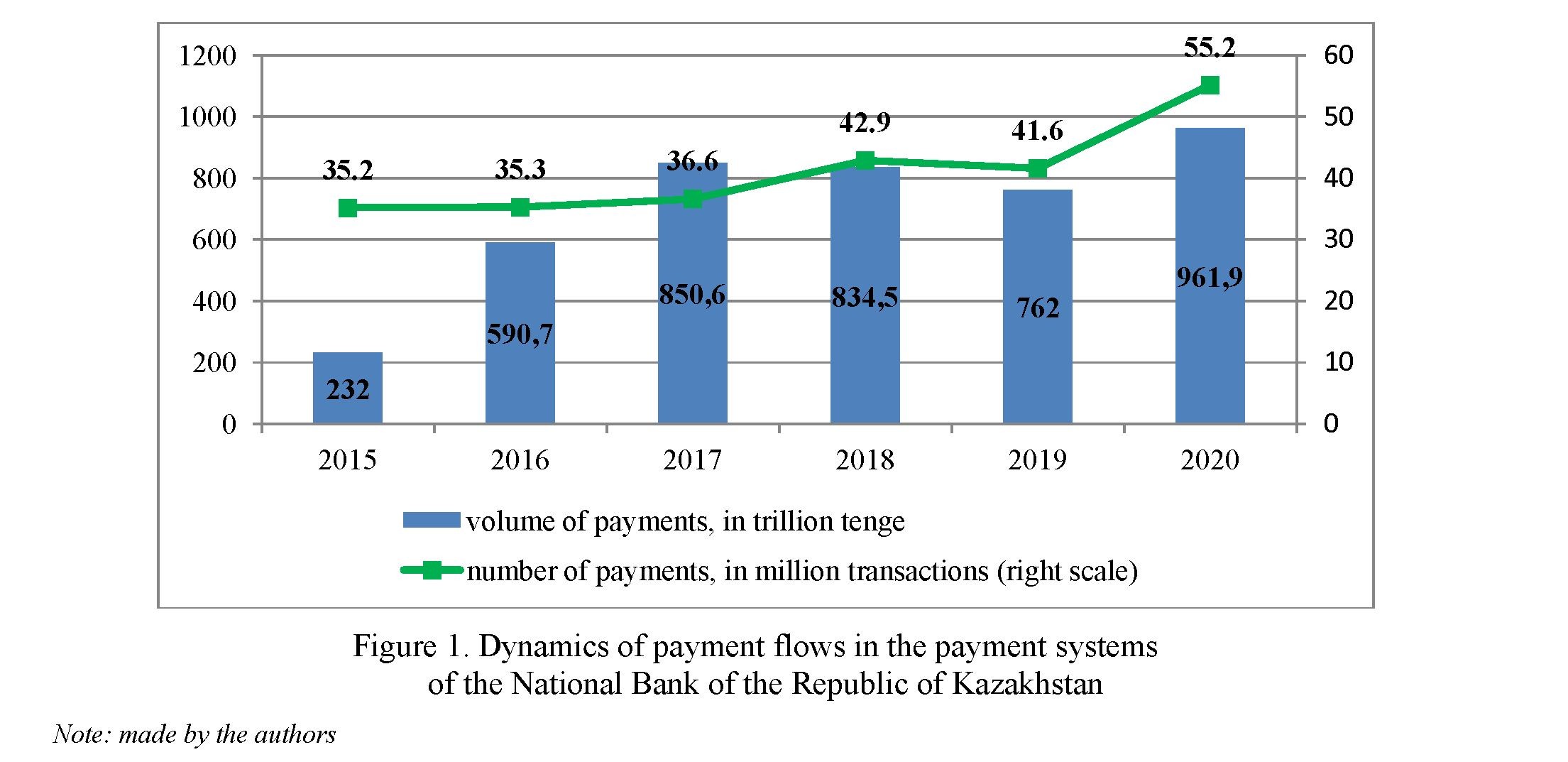

The increase in the level of digitalization of services in Kazakhstan stimulates an increase in the system of online payments and money transfer among population.

In general, for the analyzed 2020, 41.6 million transactions amounting to 538.8 trillion tenge were carried out through the Interbank Money Transfer System (IMTS) and the Interbank Clearing System. Compared to the same period in 2019, the number of payments in these payment systems increased by 21.4% (by 7317.5 thousand transactions), the amount of payments decreased by 16.9% (by 109.4 trillion tenge).

29.6 million electronic payment messages in the amount of 5.9 trillion tenge were sent through the specified system in 2020. Compared to 2019, the number and amount of payment messages in the QMS increased by 32.5% (by 7259.0 thousand documents) and 2.2% (by 124.0 billion tenge) respectively.

In general, 144.5 thousand payment messages in the amount of 28.6 billion tenge were passed through the Interbank Clearing System per day in 2020, which is 33.1% more than in 2019 in terms of the number of payments (by 35.9 thousand transactions) and 2.7% (by 0.7 billion tenge) on the amount of payments.

During the pandemic, the number of online transfers and payments in mobile and Internet banking had increased by 18%. It is interesting to note that after the weakening the regime of pandemic, the indicator decreased slightly — to 16%. Thus, the population of Kazakhstan continues to use online services actively.

The volume of non-cash payments in 2020 amounted to 18.7 trillion tenge (43.6 billion dollars). According to analytical data, this is 2.7 times more than at the same period in 2019. Also, there is an increase in the share of non-cash payments from card turnover for the year from 40.1% to 64.2%.

A significant volume of non-cash payments are performed through Internet and mobile phones: 15.1 trillion tenge (35.2 billion dollars) – it is 3.2 times more than last year.

POS terminals account for 3.5 trillion tenge (8.1 billion dollars), an increase over the year by 59.4%. Other systems for conducting non-cash transactions account for less than 1%, or 99.3 billion tenge (over $ 232 million) — minus 19.1% per year.

Having analyzed the possible forms and instruments of payments, we think, despite the ongoing digital transformation in Kazakhstan, there is one official form of the monetary unit which is enshrined in law — tenge. However, payment instruments are both cash and non-cash money (including electronic), which is established by the legislation and rules of the National Bank of the Republic of Kazakhstan. From the point of view of the implementation of the technology of payment instruments, the continuation of the development of electronic forms can be presented by forms of payments in digital currency.

Despite the widespread consolidation by national legislation of the monopoly right to issue money by the National Bank, there is a tendency towards the formation of private digital money and decentralized payment systems (Ali R., Clews R., Southgate J., Barrdear J., 2014).

Already there are several thousand different digital currencies, which may differ from each other in their characteristics. For example, they may depend on the presence of an emission limit. As you know, the most popular cryptocurrency Bitcoin has a release limit. At the same time, for example, Novacoin, PPCoin have no emission limit (Zvyagin L., 2018)

Digital money can be not only private, but also national. The issuer can be represented by the National Bank or different financial institution with monetary functions. Digital currencies are understood as “a new form of money that is issued electronically by a central bank and which is intended to serve as legal tender. It differs from other forms of money issued by central banks: cash and reserve balances and is intended for a wide range of people” (T. Mancini-Griffoly, Martinez Peria М., Agur I., Ari A., Kiff J., Popescu A., Rochon C., 2018).

Head of the Bank for International Settlements thought that central banks and regulators should pay special attention to cryptocurrencies and regulatory requirements (Carstens A., 2018). US Federal Reserve experts A. Berentsen and F. Shar (Berentsen A., Schar F., 2018) investigated different currencies, especially cryptocurrencies. They had found a huge demand on this asset among households and business entities for serving private sector’s needs.

Bank of Canada economists B. Fung and H. Galaburda (Fung B., Halaburda H., 2014) point out that digital currency will be accepted by market participants only if it is more attractive to use or better suited to meet their payment needs than existing alternatives.

Modern financial technologies use “block chain” for recording transactions with securities and confirming ownership of them. That is, each financial transaction is recorded in an unbreakable chain of blocks in the form of a distributed ledger, which ensures the safety and immutability of information. The National Bank issued electronic money for settlements on operations with securities.

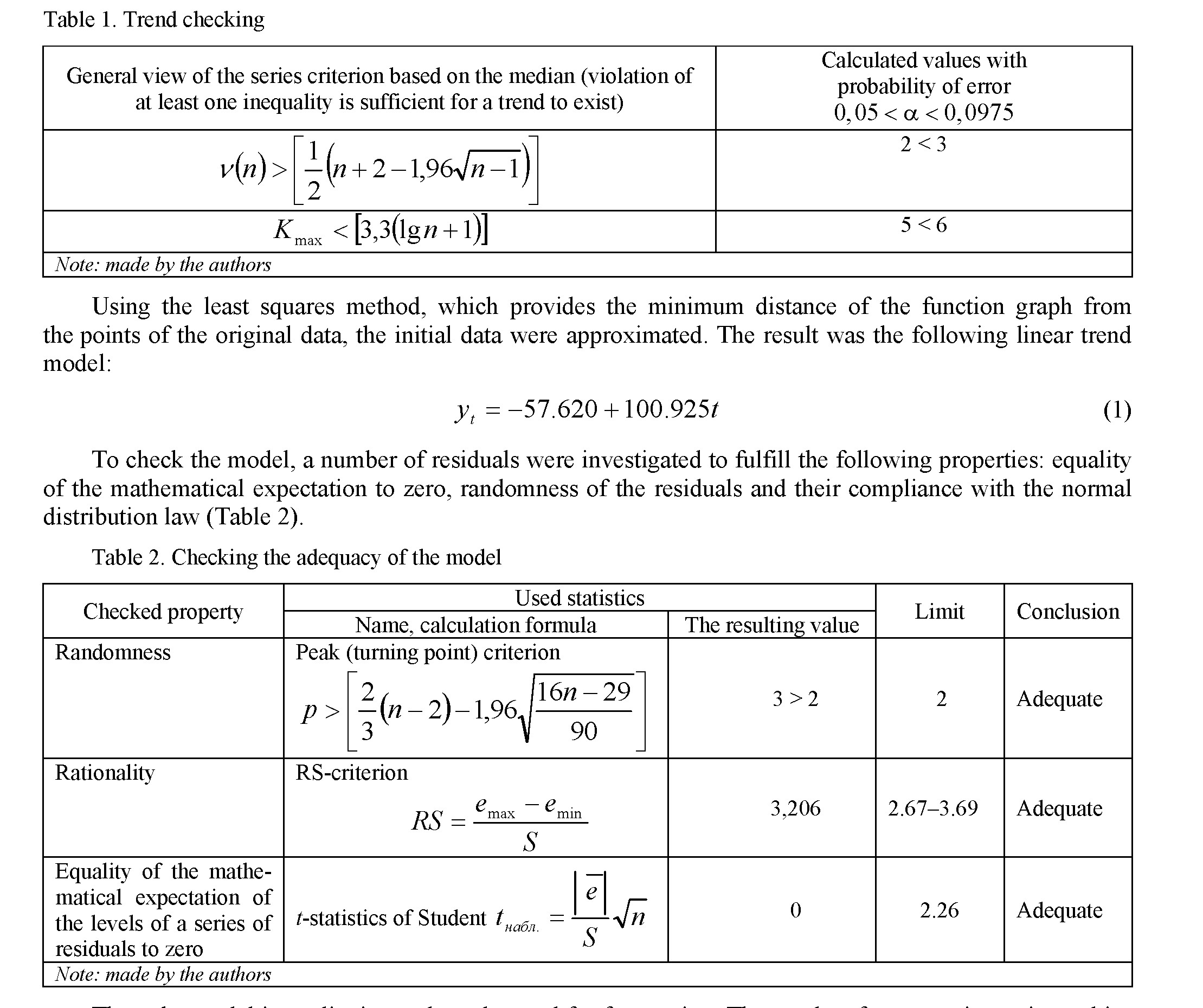

In this study, an extrapolation forecast was made for the indicator “the volume of payments in the interbank money transfer system and the interbank clearing system” for 2021–2023 years.

Initially, using Irwin's criterion, it was found that the initial time series does not contain anomalous observations, but using a series criterion based on the median that the series contains a trend component (Table 1).

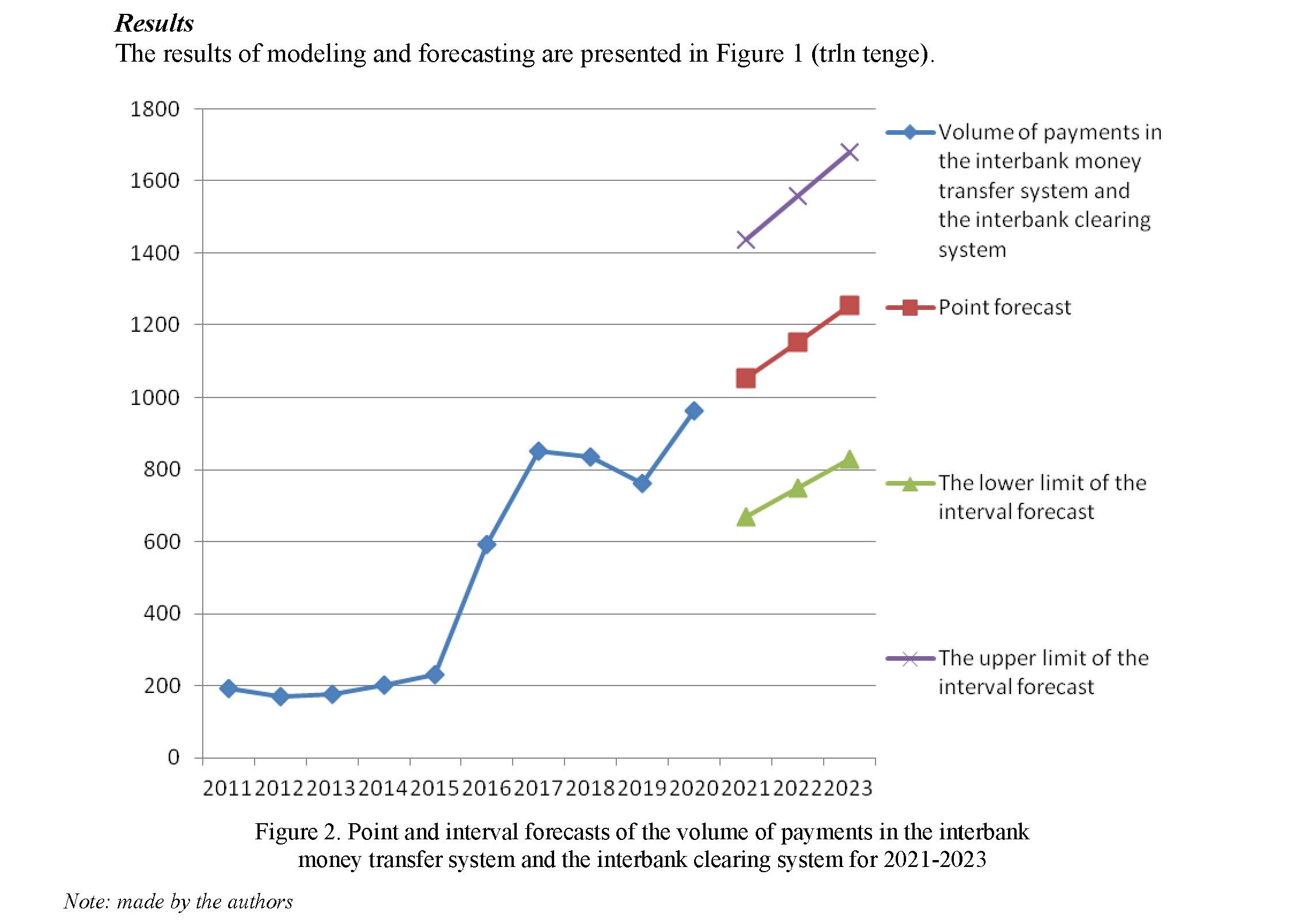

Thus, the model is qualitative and can be used for forecasting. The results of constructing point and interval forecasts for 2021–2023 are presented in Table 3.

Table 3. Point and interval forecasts of the volume of payments in the interbank money transfer system and the interbank clearing system for 2021-2023

|

Year |

Point forecast, trillion tenge |

Interval forecast, trillion tenge |

|

|

Upper limit |

Lower limit |

||

|

2021 |

1052.560 |

667.516 |

1437.604 |

|

2022 |

1153.485 |

749.800 |

1557.171 |

|

2023 |

1254.411 |

830.010 |

1678.812 |

|

Note: made by the authors |

|||

The forecasting results obtained using the linear trend model allow us to assume that with a 95% probability the volume of payments in the interbank money transfer system and the interbank clearing system will be in the range of 667.516 trillion tenge to 1,437.604 trillion tenge in 2021, in 2022 from 749.800 trillion tenge up to 1,557,171 trillion tenge; in 2023 from 830.010 trillion tenge up to 1,678.812 trillion tenge. The point forecast for the same period of time will be: for 2021 1052.560 trillion tenge; for 2022 1153.48 trillion tenge; for 2023 1254.411 trillion tenge.

Thus, the indicator “volume of payments in the interbank money transfer system and the interbank clearing system” has a linear increasing trend of development.

Kazakhstan is a perspective region for the implementation of its own digital currency. The country's unique geographical position, economic relationships with China, Russia and the West, the presence of international technology giants in the country make the electronic tenge a popular financial instrument that will significantly improve the competitiveness of the Kazakhstani economy, increase its attractiveness with similar projects from other countries at the global level. The concept of introducing digital currency and its transition to widespread use in Kazakhstan will ensure not only the creation and development of completely new ecosystems of financial products and services, but also the modernization of existing “traditional” ones.

References

- Ali R., Barrdear J., Clews R., Southgate J. (2014). Innovation in payment technologies and the emergence of digital currencies. Bank of England Quarterly Bulletin. Retrieved from https://www.bankofengland.co.uk/-/ me- dia/boe/files/quarterly-bulletin/2014/innovations-in-payment-technologies-and-the-emergence-of- digitalcurrencies.pdf

- Berentsen A., Schar F. (2018). The Case for Central Bank Electronic Money and the Non-case for Central Bank Cryptocurrencies. Federal Reserve Bank of St. Louis. Retrieved from https://research.stlouisfed. org/publications/review/2018/02/13/the-case-for-central-bank-electronic-money-and-the-non-case-forcentral-bank- cryptocurrencies

- Borzenko O., Kropova A. (2020). The role of clusters in the modern economy, their advantages and world experience. Vestnik of Karaganda University. Economy Series. № 4(100)/2020. DOI 10.31489/2020Ec4/24-32

- Carstens A. (2018). Money in the Digital Age: What Role Central Banks? BIS. Retrieved from https://www.bis.org/ speeches/sp180206.htm

- forklog.com (2020). The future of the fintech industry: main trends and forecasts. Retrieved from https://forklog.com/budushhee-finteh-industrii-osnovnye-trendy-i-rognozy

- inform.kz (2020). When central banks can implement digital currencies. Retrieved from https://www.inform.kz/ru/kogda-central-nye-banki-smogut-vnedrit-cifrovye-valyuty_a3667543

- Kumar A., Smith C. (2017). Crypto-currencies — An introduction to not-so-funny moneys. Reserve Bank of New Zealand. Analytical Note Series AN2017/07 Retrieved from https://www.rbnz.govt.nz

- Mancini-Griffoly T., Martinez Peria М., Agur I., Ari A., Kiff J., Popescu A., Rochon C. (2018). Casting light on central bank digital currency. IMF Staff Discussion Note. Retrieved from https://www.imf.org/en/Publications/StaffDiscussion-Notes/Issues/2018/11/13/Casting-Light-on-Central-Bank-Digital-Currencies-46233

- N. Salkova. (2018). Digitalization of the banking sector will make getting financial services more accessible. Kursiv.kz. Retrieved from https://kursiv.kz/news/finansy/2018-11/cifrovizaciya-bankovskoy-sfery-sdelaet-poluchenie- finansovykh-uslug-dostupnee?page=50

- nationalbank.kz . (2019). Review of the results of supervision (oversight) of payment systems and the development of the payment services market. Retrieved from https:// nationalbank.kz

- Ruziyeva E.A., Nurgaliyeva А.М., Yessymkhanova Z.K., Chaykovskaya L.A. (2020). Modeling and analysis of the mutual influence of the RUB / KZT and USD / KZT exchange rates: the period before the pandemic and as a result of the impact of COVID-19. Vestnik of Karaganda University. Economy Series. № 4(100)/2020. DOI 10.31489/2020Ec4/122-130

- zakon.kz. (2019). Law of the Republic of Kazakhstan “On payments and payment systems” Retrieved from http://zakon.kz