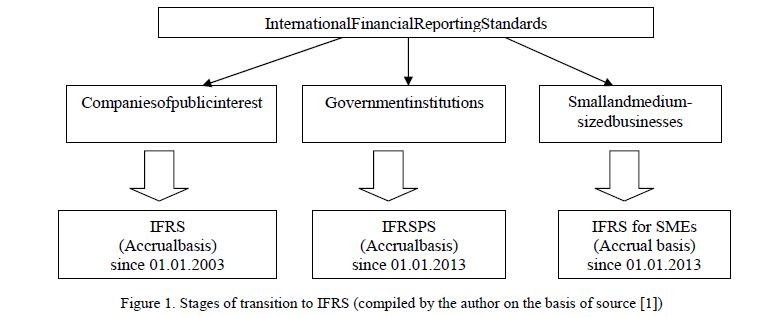

International Financial Reporting Standards for small and medium enterprises: the transition, the features, the advantages and disadvantages

The article describes the main stages of the transition to international financial reporting standards of domestic enterprises. Also it disclosed in detail the transition to international accounting standards for small and medium-sized businesses. The complete description of the definition of small and medium-sized businesses from the perspective of the Committee on International Financial Reporting Standards and the law on private enterprise is given. The main differences of IFRS for SMEs as compared with full IFRS are analysed. The advantages and disadvantages of international accounting standards for small and medium-sized businesses are showed.

2016

S.S.Shakeyev