The article gives a general description of Russian and Kazakh auditing market. Audit as an integral part of socio-economic change is an essential feature of the market economy. The quality of audit services largely affects the successful financial and economic activity, the effectiveness of economic reforms in Russia and Kazakhstan. A comparative analysis of the stages of formation of audit activity in Russia and the Republic of Kazakhstan legal framework has been done. These were conventionally allocated into four stages.

Auditing is historically one of the most important elements in the infrastructure of the market economy, promoting the development of business and economy as a whole. At the present stage in the Russian Federation, a public regulation system as part of self-regulatory audit organizations has received a significant development. At the same time, a number of problems associated with the legal regulation of auditing activities, has not received solution. For example, they include enough full study of the theoretical foundations of auditing, namely, the definition of its legal nature, as well as what needs to be scientific justification and clarification of the conceptual apparatus as audit activities.

The UK is considered the founder of the audit. Already in 1884, in England, a law on companies would establish the necessity of auditor's invitation to verify the accounting for shareholders [1].

The Institute of Chartered Accountants of Scotland (ICAS) was established later and today rightfully is the first in the list of authorized auditing bodies, with the dignity of preserving its more than 150-year history. Department of Russian Ministry of Finance audit activity supports the long-term and, safe to say, a constructive relationship with the Scottish Institute. It is very important that the draft federal law «On Auditing» passed the examination in Scotland, where it received a high appraisal of our Scottish colleagues [2].

An auditor’s rank in Russia was introduced by Peter I.One of the first mentions of the audit is contained in the Charter of the 1698 by general Adam Weide presented to Peter I by his order of studying military affairs in several countries [3].

By the nominal decree of Peter I, in 1719, for record keeping of the military ship affairs within the Office of the Military Collegium of Auditors, was established an Audit office. In 1763, it was converted into the Audit (General audit) Expedition of the Military Collegium Office. Audit office led military clerical board on military-judicial part, to record all court cases that arose in the army regarding officers, and had the right to audit conducted litigation. Institute of auditors was inducted into the army, while the auditors were engaged in matters related to the investigation of property disputes.

The end of the XIX century through the beginning of XX century was marked by the emergence in many large and medium cities of public accountancy bodies conducive to the spread of knowledge, employment of accountants, but the auditing as a profession at this time has not been formed. Assuming that the emergence of modern Western audit is primarily due to the emergence of joint stock companies, in Russia in 1836 there were only 10 joint stock companies, and at the beginning of the XX century around 2500 [4].

After the October Revolution of 1917 in the period of state regulation of economy in the USSR, the audit did not exist. In its economic essence, the audit, as an independent financial check is in contradiction with the fundamental principles of the national economy construction based on central planning, public financing and supply, total price regulation. In the Soviet Union, the state control has been developing, there were no prerequisites for the audit development [5].

In 1889, 1907–1912 and 1929–1930, some unsuccessful attempts to organize the education and certification of auditors have been taken. In Russia, the auditors have been referred to as Chartered Accountants, but they did not get the recognition, although auditors have always existed.

The concept of auditing activity and auditor profession in the Russian Federation appeared and started to develop only recently, with the transition to a market economy. The audit came to Russia in the era of restructuring, i.e. after 1985, but nevertheless in this relatively short period of time there were big changes in the approach to the audit activity, in the designation of the role of audit, in shaping the company's image and thereby increasing their investment and financial attractiveness in modern conditions.

The need for the appearance of the audit, both in the Russian Federation and the Republic of Kazakhstan was due to the following factors:

- the emergence of joint ventures, financial and economic activities of which, in accordance with international standards, should be monitored by audit organizations;

- the active development of entrepreneurship and private ownership, which led to the urgent need for an independent evaluation of the property and financial situation of the organizations;

- permission to attract foreign investment in the economy, and therefore the investors’ demand in the independent opinion;

- the formation of a modern financial market, which, in accordance with the adoption of new specific legislation, set their requirements for conducting audits;

- the emergence of joint stock companies, which led to the separation of administration and owners’ interests, and this in turn also determined the need for financial control of their activitieы;

- the adoption of new rules of accounting and financial (accounting) statements in accordance with international accounting

The above-mentioned reasons contributed to the fact that the need for the appearance of audit has become an objective reality.

The history of development of audit in Russia and Kazakhstan has shown that for the establishment and further development of such an institution as the auditing a government intervention is required. According to the established requirements of civil law only if there is a resolution of the state, which is represented by the relevant state authorities, a certain kind of activity in our case, the audit activity is entitled to a legal existence. If there is no government approval, it leads to the fact that even if the audit activity is objectively necessary, it cannot get the so-called «residence permit» in the legislation.

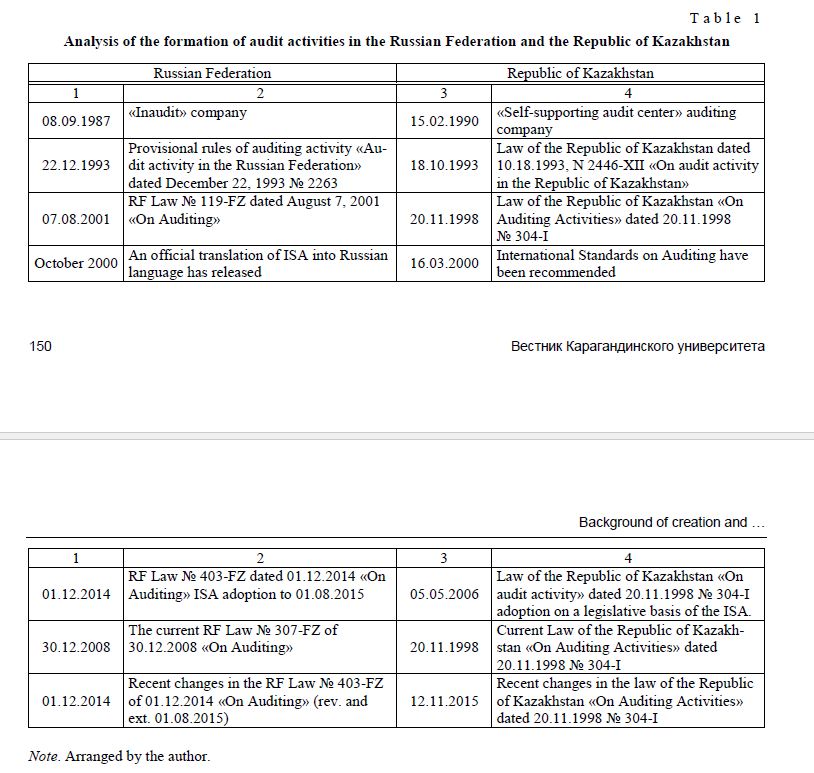

Accordingly, in the periodization of the stages of development of audit activities it would be appropriate to consider in terms of rights (approval of relevant normative legal acts) and its functions. Formation of the law is the result of economic development of society. The most important social relations are always governed by the established rules of law that are necessarily contained in the regulations. Table 1 presents an analysis of the formation of audit activities in the Russian Federation and the Republic of Kazakhstan, the main stages which we noted above — is a «residence» in the legislation.

The first phase (1987–1993) was held in the complete absence of regulatory and legal framework of the audit activity. This period of development of audit in Russia and Kazakhstan had the following differences: on the one hand, the audit organizations have been created with the legislative nature, and on the other, a spontaneous nucleation of audit activity (training auditing staff, unordered delivery of the first of certificates and licenses).

T a b l e 1

Analysis of the formation of audit activities in the Russian Federation and the Republic of Kazakhstan

Note. Arranged by the author.

According to the USSR Council of Ministers Decree dated 08.09.87 № 1033–245 «About the creation of the Soviet auditing organization» on the basis of the Main Administration of Foreign Exchange Control of the USSR Ministry of Finance a joint stock company «Inaudit» was established. The authorized capital of «Inaudit» was defined at 800 000 rubles, and the main shareholders were: the USSR Ministry of Finance — 55 %, the Ministry of Foreign Trade — 10 %, the State Bank of the USSR — 5 %, all-union association «Autoexport», «Stankoimport», «Sovfraht», «Sovrybflot» and others — 5 %. 10 departments have been formed within «Inaudit», which, having a large staff of qualified personnel, provided a comprehensive range of services to joint ventures, which operated in the USSR and abroad. But maintaining «Inaudit» as the above-mentioned structure turned out impossible. In a short time, all the major shareholders sold their share capital to the only receiver of «Inaudit» joint-stock company, which in 1992 was transformed into several independent organizations.

In the Republic of Kazakhstan, the history of formation and development of the audit began in 1989, when at KRU (Audit Office) of the Ministry of Finance audit self-supporting group was organized. Then, in accordance with the Decree of the Kazakh SSR Council of Ministers of 15 February 1990 number 60, a selfsupporting audit center «Kazakhstan audit» was created with territorial offices of the Ministry of Finance. Since 1992, a self-supporting audit center «Kazakhstan audit» has become a major independent joint-stock company, which nowadays provides audit services to organizations of all forms of ownership.

In Russia, the first draft of the law on auditing was developed in 1992, but at this moment in Russia prevailed the political crisis, and it wasn’t adopted. Provisional rules of auditing activity in the Russian Federation were adopted by presidential decree of 22.12.1993 № 2263. Thus, it was the first legal document that regulated the auditing activities in Russia. It worked as a full statute, even though the title of «Temporary Regulations» was clear that this document was for the transition period, the assumption meant that the document was to be temporary and wasn’t supposed to be for long. However, time has shown that in fact these rules were a guide for almost eight years and have not been amended and changed.

In Russia, the further development of the audit activity was due to the need for its unification and standardization through the development and approval of audit standards.

In the Republic of Kazakhstan for the first time among the countries of the former Soviet Union, was developed and adopted the Law «On audit activity in the Republic of Kazakhstan.» However, after the adoption of the first law «On Auditing Activities in the Republic of Kazakhstan» dated October 18, 1993 there have been significant changes in the economic and socio-political life of the country.

The second stage (December 1993 — August 2001) was a period of active development of Russian audit, the process of which influenced the formation of Provisional rules of auditing approved by Presidential Decree of 22.12.93 number 2263 «On Auditing Activities in the Russian Federation» as well as other regulatory documents.

Provisional rules of auditing activity entrench the concept of auditing, set the rights, duties and responsibilities of auditors (audit firms) and economic actors, to define the basis of state regulation of audit activities, including licensing and certification of auditors [6].

State regulation of audit activities in Russia was carried out by the Audit Commission under the President of the Russian Federation, which was established and carried out its activities in a given period. Since 1996 until 2000 the Commission has developed and approved 37 rules (standards) of audit activity, as well as the general methodology of audit activities, which constituted the methodological basis of Russian audit.

The active work on certification and licensing of auditors auditing activities started during this period, the audit associations and accounting firms have been established, work began in the conduct of the statutory audit and the provision of related services in the audit field. Analyzing the period from 1994 to 2001, it should be noted that the organization TSALAK of the Russian Ministry of Finance has issued 23,600 licenses to licensees, including audit organizations — 14 700 licenses and 8900 licenses for individual auditors. The license number for that period was about 8900, including on general audit — 7700. During this same time TSALAK of the Russian Ministry of Finance has approved the issuance of approximately 36 500 auditor qualification certificates. During this period, it was formed by acting on the present stage of the working structure of auditors and audit firms.

In the Republic of Kazakhstan, taking into account the changes taking place, led to the development of the new Law «On audit activity», adopted November 20, 1998. Compared to the «old» law dated 18.10.1993 it has consistently been more fully disclosed the fundamental concepts, principles types, entities, competence of the authorized bodies, the rules of certification of candidates in auditors, licensing and implementation of audit activity.

Timely adoption of the second current Law on Audit promoted the consolidation of de facto independence of auditors and audit firms in the country.

In accordance with the requirements of the Law «On audit activity» have been carried out activities to create regional chambers and the Republican Chamber of auditors, the election of the audit commission and the formation of the qualification commission of auditors for certification.

The third phase (August 2001 — December 2008) continued its formation of audit after coming into force of the Federal Law of 07.08.2001 number 119-FZ «On Auditing». The Act finally confirmed the establishment of audit in Russia, and this legislation has created a basis for the development of a number of new regulations on the management of audit activity in Russia, and thus a step on the path of integration of the Russian audit in international audit system has been made. Audit firmly took its place among the other types of financial control.

Audit as an integral part of socio-economic change is an essential feature of the market economy. The quality of audit services largely affects the successful financial and economic activities, the effectiveness of the economic reforms in Russia.

After the 1998 crisis, the development of audit activity was held in a sufficiently stable conditions of economic development: a stable and steady GDP growth (an average of about 7 % per year) and industrial production, the transition from deficit to the proficient budget. For members of the audit market in Russia and Kazakhstan, this means the expansion of extensive growth opportunities, stable development of Russian companies at the same time maintaining the leading position of the «Big Four» companies.

Since 2000, the Russian audit activity shows a steady growth of the share of consulting (services on tax, financial, insurance, etc. Audit).

This period was also characterized by the appearance on the market self-regulating organization of auditors (ASO auditors) the functions of which were related to the control of the activities of its members.

At the same stage, the audit companies have begun to actively develop their networks of branches and set up regional offices. Established network of branches mainly focused its operations on providing audit services, as companies that were in the field, on the basis of which to establish branches, specialized in this field. At the same time, audit companies began to exert greater related services (consulting) in the central regions of Russia than the audit. Thus, until 2008 the Russian and Kazakh accounting firms operating in stable conditions favorable development of the audit market. This has contributed in the first place to:

- Formation of structured regulatory framework (development and adoption of the Federal Law «On audit activity»);

- Expansion of the list of services provided in relation to the provision of advice on reporting, IFRS, training seminars, with the result that the proportion of audit services began to decline;

- Improving the skills of audit firms by enhancing the minimum requirements for candidates for the position of auditor;

- Expansion of the geography of the market, which resulted in the development of regional companies, subject to statutory audit, as a consequence of which the audit firms began to open their own branches and representative for the statutory audit [7].

The fifth conference of the Republican RK auditors was held on March 16, 2000 in Almaty, where have been reviewed and accepted «International Standards on Auditing in Kazakhstan.» The International Auditing Practices Committee (IAPC) issued regulations, consisting of the International Standards of Auditing (ISA) and related services standards (RSS).

Thus, an audit in the Republic of Kazakhstan has initially been carried out on the basis of Kazakh standards for audit, developed on the basis of international standards. At the fifth conference of the Republican Chamber of Auditors of the Republic of Kazakhstan, in March 2000, a decision was made on transition to international standards of auditing and accepting as national. This position then obtained legal support by the Law of the Republic of Kazakhstan «On Auditing». According to this regulation, the audit in the country is carried out in accordance with international auditing standards, which do not contradict the legislation of the Republic of Kazakhstan, published in Kazakh and Russian languages, the organization has a written authorization of their official publication by the Committee on International Auditing Practices of the International Federation of Accountants. That right has the Chamber of Auditors of the Republic of Kazakhstan, which in 2007 published a collection of International Standards on Auditing, assurance and ethics.

Law of the Republic of Kazakhstan «On Auditing Activities» dated 5 May 2006 has ascertained that the audit of Kazakhstan is carried out in accordance with International Standards on Auditing that do not contradict the legislation of the country, published in Kazakh and Russian languages, the organization has a written authorization of their official publication the Republic of Kazakhstan from the Committee on International Auditing Practices of the International Federation of Accountants. This right is fully owned by a professional auditing organization — the Chamber of Auditors of the Republic of Kazakhstan, which is a full member of the International Federation of Accountants.

In late 2008, a new federal law was passed in Russia dated 30.12.2008 № 307-FZ «On Auditing». The basic idea of this regulation is the gradual liberalization of the audit activity regulation [8].

Coming into force of the new law on auditing announced the beginning of a new stage of development of audit in Russia. The new law has made great reforms in the audit control system, revised the status of the audit activity of subjects, gave a new interpretation of the types of audit services, amended in respect of the statutory audit, changed the procedure for the adoption of certain regulations, has made changes in the financial and regulatory audits.

So, starting here we can speak of the fourth stage of development of auditor activity in the Russian Federation and the Republic of Kazakhstan.

Starting January of 2009 is the fourth stage in the development of audit activity that is associated with the adoption of the Federal Law of 30.12.2008 № 307-FZ «On Auditing», the characteristic features of which are connected with a complex of measures aimed at the gradual transition from the state regulation of auditing activities to self-regulation.

At this stage, in 2010–2011 by Ministry of Finance of Russia, new federal standards of auditor activity (FSAD) as a basis were approved, which have been based on international auditing standards.

A little later, the Russian Finance Ministry prepared Explained practice of application of legislation of the Russian Federation and other normative legal acts, which regulate the auditing activities (approved by the Board of the Audit March 26, 2013, protocol № 8) «Determining the type of service, requirements to order of provision of which are determined by the federal auditing standards FSAD and FSAD 8/2011 9/2011» [9]. Based on these explanations, the audit organization (the individual auditor) provides services for the audit reports prepared in accordance with special rules, as well as a separate part of the accounts in accordance with federal auditing standards FSAD and FSAD 8/2011 9/2011.

With regard to the concept of professional competence and ethics in the work of auditors, auditors' liability, namely, civil, financial, to third parties, criminal, professional still there are many disputes and problems. For the unification and standardization of these terms March 22, 2012 the Board of the Audit adopted the Code of professional ethics of auditors [10].

The Code is a set of basic rules of conduct that must be observed by all audit firms and auditors in the course of their audit activities.

The underlying principle of audit activity is the principle of independence, and it is reflected in the detailed regulation «Rules of the independence of auditors and audit organizations» (approved by the Board of the Audit September 20, 2012, protocol number 6) [11].

According to the Federal Law of 30.12.08 № 307-FZ «On Auditing», the function of state regulation of audit activities is assigned to the authorized federal agency — the Ministry of Finance.

At the same time audit of the professional control functions are assigned to the self-regulating organizations of auditors (ASO). These are non-profit organizations that are created on the conditions of membership in order to ensure the conditions for the exercise of the audit activity. The Act provides that the audit firm and individual auditors must necessarily consist in one of SROA (compulsory from 1 January 2010).

Council on Auditing Activities March 26, 2013 has approved «The main principles of the Russian translation of the international standards applied in the audit activity on the territory of the Russian Federation.» This document outlines the basic principles of the Russian translation of the international standards applied in the audit activity. According to the Federal Law № 403-FZ of 01.12.2014 «On Auditing» starting August 1, 2015 on international auditing standards came into force [12].

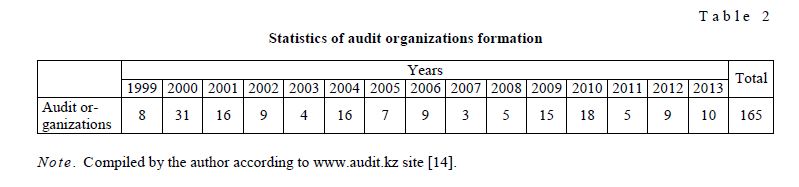

Currently, in Kazakhstan market of audit services there are 165 Kazakhstan organizations and 513 individual auditors, as well as foreign companies, including intercontinental audit and consulting corporations: «Deloitte», «Ernst & Young», «KPMG», «PricewaterhouseCoopers». Of particular note is that according to the Ministry of Finance of RK, in the whole country the share of services in auditing accounts for only about 44 % of all volume of audit services, and the rest of the share of the so-called other services defined by the Law of the Republic of Kazakhstan dated November 20, 1998 № 304-I on auditing (revised and extended 11/12/2015) [13].

Only those entities who have been granted a license to perform audit activities have the right to carry out audit activity. Ministry of Finance of RK as the licensing authority in the respective state register takes into account issued licenses to perform audit activity. The number shows how many audit firms of auditors had the right to audit activities.

Statistics of audit organizations formation

T a b l e 2

Note . Compiled by the author according to www.audit.kz site [14].

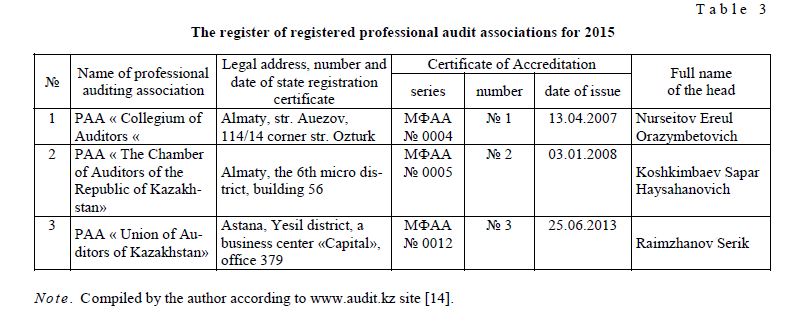

According to the Law of RK «On Auditing», a prerequisite of the audit activity for firms is to become a member of professional association of audit organizations (PA) (Table 3).

The register of registered professional audit associations for 2015

T a b l e 3

Note . Compiled by the author according to www.audit.kz site [14].

In 2009 in Kazakhstan, there were two such associations: PA «The Chamber of Auditors of Kazakhstan» (uniting 82 organizations and 402 auditors) and PA «RK College of Auditors» (50 and 111 respectively). In 2013, another professional organization PAA «Union of Auditors of Kazakhstan» received the accreditation certificate.

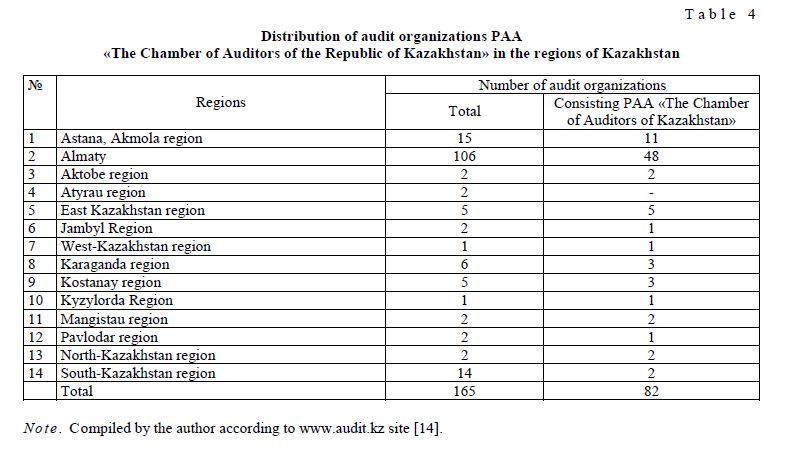

Distribution of audit firms by region in 2014 was characterized by the data reflected in Table 4. Analyzing the distribution by region of audit organizations should be noted that the main share of 64 % is in Almaty, this is explained by the fact that at the time of formation of audit activity, in 90s Almaty was not only the capital of Kazakhstan, but also an intellectual center where the intellectual potential of the country was concentrated.

Distribution of audit organizations PAA «The Chamber of Auditors of the Republic of Kazakhstan» in the regions of Kazakhstan

T a b l e 4

Note . Compiled by the author according to www.audit.kz site [14].

Development and adoption of normative legal acts of the Republic of Kazakhstan relevant to market relations contributes to the proper definition of the development prospects of the audit of the case and the active involvement of our country in major international audit companies.

When creating audit organizations it is appropriate to use different forms of audit companies in the form of:

- Representative offices of foreign audit firms;

- Joint audit companies;

- Joint-stock companies and companies;

- Small, private and individual enterprises;

- Auditing and counseling

The first type of audit organizations are representative offices of foreign companies in the so-called «Big Four»: «KPMG»; «Deloitte & Touche»; «Ernst and Young»; «Price Waterhouse Coopers». The members of the «Big Four» have years of experience and high image.

The second type is the creation of joint ventures with foreign firms (except for the «Big Four») and audit firms of the CIS countries. This type of audit organizations in our country is worthy represented by «BDO Kazakhstan audit», which in 2000 was made a full member of the world's largest independent international auditing firms association — «BDO international».

The third type are a cross-sector auditing companies serving the oil and gas sector companies, metallurgy and other industrial and commercial complexes. They work on specific topics, are action-oriented, provide a wide range of professional audit services to domestic enterprises.

The fourth type of organizational form are small independent auditing firms, which include some auditors. In Kazakhstan, the following organizations belong to this group: NAC «Centeraudit-Kazakhstan», LLP «Erzhanov and Co.» LLP «Ai-Audit» and others.

The fifth type of organizational form is auditing and counseling alone.

The development of professional standards at the international level are engaged in several organizations, including the International Federation of Accountants (IFAC), which includes representatives of 158 organizations from 115 countries [15].

As part of IFAC's auditing standards are a direct work of the International Auditing Practices Committee (IAPC), acting on the right of permanent autonomous organization.

It is important to emphasize that the Court of Auditors of the Republic of Kazakhstan, which for the past 20 years has been closely involved in the development of audit activities in the country and has played a significant role in enhancing the prestige of Kazakhstan in the world in the context of the implementation of the results of international reporting and validation of foreign experience.

Thus, we have been given a general description of the Russian and Kazakh market auditing. Given the above information by a brief description of the activities of Russian and Kazakh audit firms, may be noted that the audit activity is steadily growing and is characterized by a number of successes in its development.

References

- Ablenov D.О. Audit: theory and practice: textbook, Almaty: Economy, 2005, 419

- Azhibaeva Z.N. Audit: textbook, Almaty: Economy, 2004, 527

- Ostashenko Y.G. Audit, Omsk: Publ. of Omsk State University, 2009, 207

- Pyatenko S.V. Organization of the work of auditors and consultants: Educational and practical guide, Мoscow: FBK-Press, 2001, p.

- Scobara V.V. Audit: Methodology and organization, Мoscow: Business and Service, 1998, 389

- Temporary rules of auditing activity «Audit Activity in the Russian Federation», dated December 22, 1993 № 2263, [ER]. Access mode: http://pravo.gov.ru/ipsdata/?doc_itself=&backlink=1&nd=102027783&page= 1&rdk=2#I0.

- Suyts V.P. Audit, Мoscpw: KnoRus, 2012, 168

- On Auditing // Federal Law № 307-Federal Law of 30.12.2008, [ER]. Access mode: http://www.consultant.ru/ document/cons_doc_LAW_83311.

- Clarification of the Ministry of Finance of Russia from 03.13 № PPZ 2–2012 / 8 «Explaining the practice of law of the Russian Federation and other normative legal acts that regulate the audit activities (approved by the Council on Auditing Activity 26 March 2013, Minutes № 8), [ER]. Access mode: http://www.consultant.ru/document/cons_doc_LAW_144800.

- Code of Professional Ethics approved by the Council Auditors on the audit activities of the Russian Federation 03.2012, Minutes № 4, [ER]. Access mode: http://www.consultant.ru/document/cons_doc_LAW_130160.

- «Rules of the independence of auditors and audit organizations» (approved by the Council on Auditing Activity September 20, 2012, Minutes № 6), [ER]. Access mode: http://online.zakon.kz/Document/?doc_id=31278599.

- Federal Law № 403-Federal Law of 01.12.2014 «On audit activity» (as amended, entered into force on 08.2015), [ER]. Access mode: http://www.consultant.ru/document/cons_doc_LAW_83311.

- Law of the Republic of Kazakhstan «On Auditing Activities» of 11.1998 of № 304-I (as amended and supplemented on 11.12.2015), [ER]. Access mode: http://online.zakon.kz/Document/?doc_id=1011692.

- [ER]. Access mode: audit.kz.

- Musaipkanova J.D. Banks in Kazakhstan, 2012, 12, p. 21–23.