The article considers the foreign experience of stimulation of innovation activity in the business sector. The direct and indirect incentive mechanisms are considered. The great attention is given to the analysis of tax incentives, such as tax privileges and the tax credit. They play an important role in enhancing the innovative activity of enterprises, because provide a choice of priorities of innovation to the private sector and do not require large administrative costs. Methods of indirect incentives are widely used in the USA, Canada, Japan and most European Union countries. Each country forms its own combination of these mechanisms depending on the requirements of the economy and the priorities of innovation development.

In modern economy the innovative activity has great value because the competitiveness of the region directly depends on the ability of economy to generate and effectively use innovations. The analysis of world experience testifies that stimulation of innovative activity allows the states to create favorable conditions for scientific, technical and innovative activity of the enterprises, to increase efficiency of innovative systems.

The state support of innovative activity includes various forms of direct and indirect economic regulation. Direct methods include:

- the state investment in the form of target, subject-oriented or the problem directed financing, the state crediting, leasing, share operations with the purpose of increase of research and material means concentration on the most perspective directions and progressive types of production;

- planning and programming, state entrepreneurship;

- the measures intensifying cooperation of the industrial organizations in the field of scientific research, in particular with research and educational universities [1].

Unlike the direct methods which directly influence on the decisions made by economic subjects, indirect methods only create prerequisites for a choice of the directions of development answering economic targets of the state. Indirect methods of stimulation in modern conditions get the increasing distribution in foreign practice because they demand the postponed budgetary expenses in comparison with direct financing, and also create prerequisites for development of an enterprise initiative in the innovative sphere. They include the formation of legislative and legal base in the sphere of science and innovations, tax incentives, development of venture financing system, formation of the state innovative infrastructure and development of the scientific and technical products market, formation of innovative clusters (informal associations of the small, medium-sized and large enterprises, and also the research organizations operating in a certain sector and the geographical region) [2].

It is necessary to distinguish active application of certain tax modes among the indirect methods of stimulation. The economic sense in using of tax incentives lies in interest of taxpayers in development of their activity in the directions which correspond to public requirements. In relation to stimulation of science and innovations sphere the particular tax treatments are generally urged to stimulate increase in financial investments to this sphere from non-state actors of managing.

As world practice shows, tax privileges act as the main type of tax incentives for development of scientific and innovative activity. Depending on an element of structure of a tax (object of the taxation, tax base; tax period; tax rate; order of calculation of a tax; an order and the term of payment of a tax) on which change the privilege is directed, there are distinguished tax allowances and tax credits. In world practice the concept «tax allowance» is used for designation of the sum which is subject to the complete or partial elimination from tax base at calculation of the sum of a tax. Concerning stimulation process tax discounts allow the firms investing in R&D to receive deductions from their taxable income in the size which is actually exceeding expenses on R&D. The concept «tax credit» designates deductions in a percentage ratio to costs of R&D from final tax obligations of the subject which made these expenses [2].

In the early eighties of the XX century in the USA a number of the acts was adopted directed on stimulation of innovative activity, acceleration of commercial use of results of scientific activity of certain researchers and the organizations. During this period the USA faced the problem of increasing of expenses on R&D with simultaneous decrease in efficiency from use of the R&D executed on budgetary funds. Within the law «The Small Business Innovation Development Act» (of 1982) there was developed a number of the national programs financed from the state budget, and stimulating development of innovative economy on the basis of the private sector. The Bayh-Dole Act provided to the research organizations, businessmen the property right to the inventions created within the research financed by the federal government. The Stevenson-Wydler Technology Innovation Act defined the property rights to the inventions created in the course of joint scientific researches of the state laboratories and private enterprises. Adoption of new laws in the sphere of technologies transfer provided to universities and national laboratories the property right to patents and stimulated commercialization of the researches results financed from the federal budget. Previously no more than 5% of the state patents were commercialized, but at the beginning of new legislation application the third part of inventions were commercialized. Tax revenues in the budget from sale of license products were estimated in 5 billion US dollars [3].

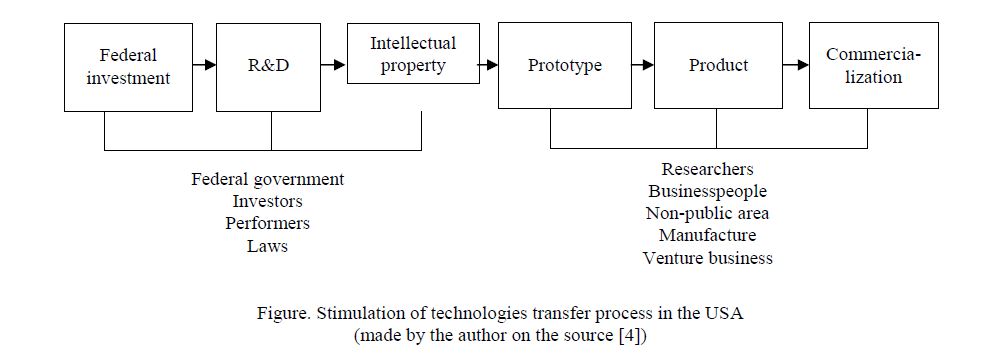

In the process of technologies transfer the government participates only at the first stages: investment, R&D, creation of intellectual property (Fig.). At the subsequent stages the government transfers the rights for intellectual property to performers of R&D — to universities, the research organizations, private firms.

Figure. Stimulation of technologies transfer process in the USA (made by the author on the source [4])

Direct methods of the state support of innovative activity in the USA include:

- financing of fundamental science;

- protection of intellectual property, copyright and trademarks and system of the courts specializing on protection of these rights;

- adoption of technical standards;

- services of knowledge and experience dissemination in the sphere of the industry and agriculture, for the purpose of small business support;

- government order for

The U.S. Government developed a number of innovative business support programs: «The Small Business Innovation Research — SBIR», «The Small Business Technology Transfer — STTR», «The Advanced Technology Program» [5].

Indirect methods of the state support of innovative activity actively used in the USA. In particular, they are the tax credits in the form of a discount for already added tax payment, and also the special mode of depreciation charges within tax depreciation [6].

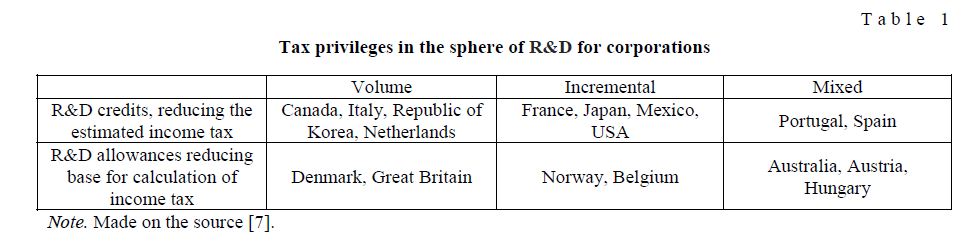

The scientists distinguished two types of tax allowance: volume and incremental. The volume discount provides a privilege in proportion to volumes of expenses. In the USA 100% is subtracted for R&D from the taxable income of the company. Similar practice is used in Canada, Great Britain, Belgium, Sweden, and Italy. The incremental tax allowance is defined proceeding from the increase in costs of R&D reached by the company in comparison with the base year or average value for a certain period. The allowance works after expenses were made on research. Its size is 20% in the USA, however there are some restrictions. The incremental tax discount is applied only to those expenses on R&D which are directed on development of new technological processes or production. This discount doesn't extend on the expenses connected with change of a look or type of production, cosmetic and other changes (Table 1).

Tax privileges in the sphere of R&D for corporations

T a b l e 1

Note. Made on the source [7].

The Canadian government has developed a number of programs aimed at stimulation of innovation. As an example, the program «Scientific research and experimental development» was developed, which is open to all Canadian organizations engaged in various sectors of the economy. Participants of the program receive tax incentives in the following sizes: the first 2 million $ — in the amount of 20 to 35%, provided that this amount was spent on research work conducted in Canada. The goal is stimulation of the development of new, more advanced in terms of technology, products and processes.

As part of the above program, the Federal Government of Canada provides tax incentives as a measure of the state support of private companies. Businesses can write off of 100 per cent of taxable income of its current R&D costs and the costs of purchasing the equipment used for that purposes. In addition, business can use targeted tax credits for R&D investment within the territory of the country. In this case, the companies are entitled to deduct from the amount of taxes up to 20% of the costs of their own innovations. For small and medium businesses the rate of the tax credit for R&D investment is 35%.

The UK Government is considering the acceleration of scientific and technological development as a basis for sustainable economic growth.

Executive authority, authorized by the state policy to encourage innovation in the country is the Ministry of State for Business, Enterprise and Regulatory Reform in the area state regulation.

Royal service of taxes, fees and customs provides tax incentives for innovation through two schemes: for small and medium-sized enterprises and large companies. As part of the state policy on innovation companies grants for research studies can be given. If innovation activity of the company was financed by the state in the form of grants, tax incentives for such activities do not apply in terms of the size of the grant [8].

An important tool to stimulate the technological development of the industry is using of the state order. Direct and indirect results of research and development carried out on the instructions of government agencies tend to use by private companies for development of new products and services. Additional support of innovative processes is provided by reducing the regulatory functions of the state, facilitation of administrative supervision and control of tax incentives for R&D and promotional activity.

The UK has strong intellectual, human and industrial resources. The country is a leader in the field of technology for the collection, transmission, storage, analysis, and data protection in a networked environment. In this regard, it attaches great importance to acceleration of the turnover of intellectual property. Annual public spending for creation nationwide network of scientific and technological information, which aims to combine the electronic libraries of national research organizations and industrial enterprises, is estimated in 40 million pounds.

Extending the interaction between science and industry is expected through the implementation of the concept of «technology platforms». Important features of this form of innovation activity are the leading role of business in determining objectives, focus on the creation of innovative commercial products, facilitation of bureaucratic procedures, and diversification of funding sources. It has already begun work on the formation of two national technology platforms that will be the basis for coordination of the work of government departments, universities, industry and financial institutions in the development of «intelligent transport» and systems for the protection of information infrastructure.

The state economic policy of Japan is closely connected with innovative policy. The creation favorable conditions for development of innovative activity are based on the following principles:

- The state financial support of priority industries by means of subsidies and the credits (a rate of 2–4%) issued by the financial organizations through Japanese development bank and Japanese export-import

- Assistance to the enterprises in acquisition of the latest foreign technologies, creating favorable conditions for technical cooperation of Japanese firms with the foreign

- Creation of system of the accelerated depreciation of the knowledge-intensive equipment that reduces the taxation of Japanese firms and does possible an investment of financial resources in the new industrial enterprises and projects [9].

Because Japan has no large amount of natural resources, the government of the country considers scientific and technical policy as the most important stimulant of economy growth and increase of the international competitiveness of the country. In Japan for the first time in the world there were developed and applied tax discounts for the purpose of involvement of the private sector to research activity. Rates of development and structure of scientific sector of the country are regulated by the law «On Special Tax Measures» [6]. First of all they include regulations on tax discounts (the tax credit) with a growth of research costs in the private sector, and also the provision on the measures for the taxation aimed at the development of fund of small and medium business technologies.

The legislation of Japan provided a number of incentives for the organization of joint research in the private sector. The taxable sum is estimated on a special depreciation scale at the taxation of research cooperatives members regarding acquisition of fixed assets for carrying out researches. Since the end of the 80th years of XX century and to the present time the special measures for acquisition stimulation of the hi-tech equipment by the enterprises in the sphere of biotechnologies work. These measures provide reduction within 3 years for 75% of taxable base for expenses on acquisition of the research and experimental equipment.

In 2003 in Japan approved the project on stimulation of industrial investments into science within which it is accepted the special tax discount (the tax credit) of 10–12% for research expenses of firm. However volume of credit cannot exceed 20% of a corporate tax in the current year. Since 2006 any company could obtain 5% the tax credit charged at increase in number of research divisions of the company. At increase in reporting year of costs of R&D of the firm over a similar indicator in two previous years, the corporate tax can be reduced by the sum which equivalent to 5% of the reached excess [6].

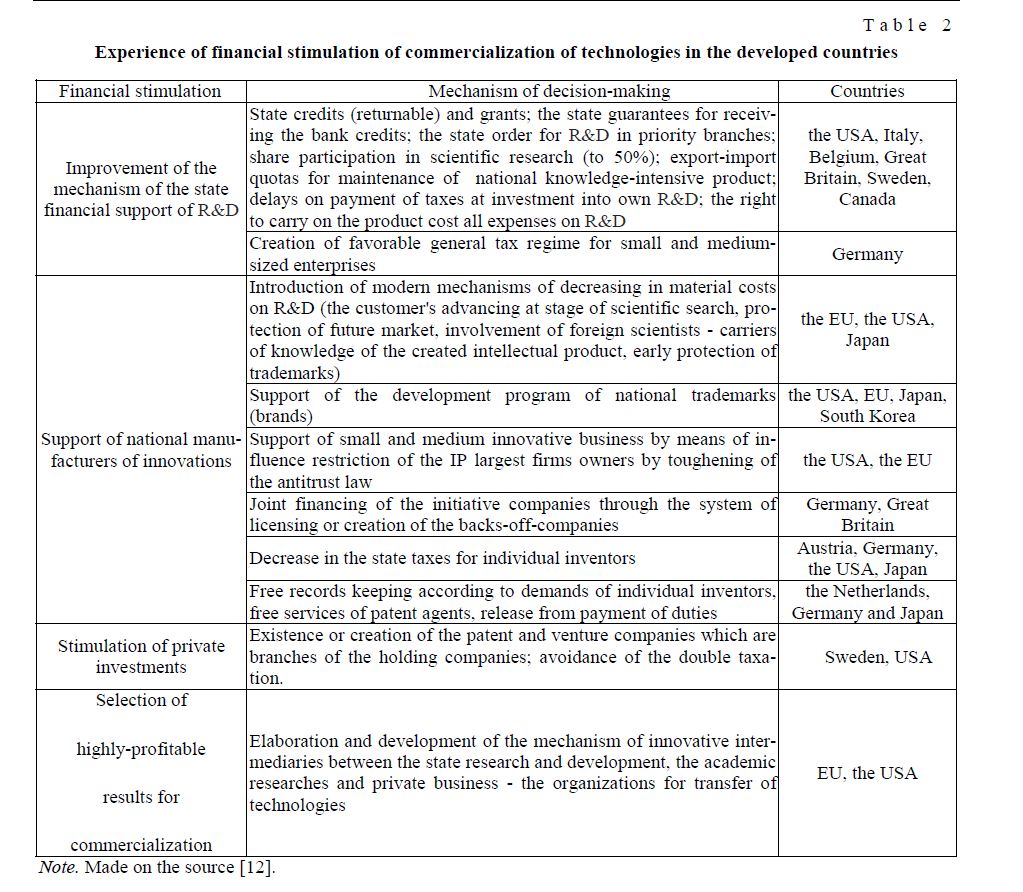

The tools of innovative policy used to R&D stimulation are various in different EU countries. The majority of the countries apply a package of measures of direct and indirect stimulation, however the degree of the value given to each of methods in different EU countries, differs radically. For example, in Spain the wide set of fiscal incentives is applied to all companies, irrespective of their size while in Great Britain such measures are applied only in relation to the companies of small and medium business [10] (Table 2).

In Germany, as well as in some other countries with the high level of scientific and technological development (Sweden, Finland) the great value is given to measures of direct financial support that allows the state to define, what sector of economy or what technologies need to be developed first of all. In this country almost completely there are no measures for tax incentives of scientific-technological and innovative activity of business sector. The preference is given to improvement of the general tax regime for the enterprises.

In France the tax credit for research is spread widely. That privilege allows the enterprises which carried out research works to subtract part of expenses from the accrued income tax. According to the mechanism of the tax credit application, the French enterprises can subtract from the tax 50% of the difference between the costs of research realized in the current year and an arithmetic average of the last two years. Thus, the following principle is realized: the more the enterprise carries out research works next year, the more sum of the corresponding will be tax privilege.

Much attention is paid in France to creation of «superiority poles» (science and technology parks, the research centers, etc.), to development of small business, support of the enterprises having more than 15% of commodity turnover as costs of R&D (release from social, local taxes and income taxes). The largest scientific park «Sophia Antipolis» includes the companies in the field of computer facilities; electronics, pharmacology and biotechnology, there are created more than 25 thousand workplaces in park. Since 1979 the French agency of innovations (ANVAR) is in function, which main activities are commercial, marketing, technical and financial support of activity of small and medium-sized enterprises (up to 2 thousand people) [11].

T a b l e 2

Experience of financial stimulation of commercialization of technologies in the developed countries

Note. Made on the source [12].

Methods of stimulation of innovative activity in different countries have their specific features; their choice is caused by economic, political and other conditions of the country development. However, as the analysis showed, many tools are similar in many aspects and are effectively used by groups of countries. The wide range of mechanisms of stimulation of innovative activity which used abroad have common features among which it is possible to distinguish:

- active participation of the state in innovative process: the state crediting of the innovative companies at the preferential rates, placement of the state order for research and development in priority branches of economy, participation in financing of scientific

- creation of tax privileges system for the innovation-active enterprises among which there are most actively used deductions from the taxable income of expenses on R&D, the tax credits;

- a huge role of private business in innovative development of the leading foreign countries of the The considered indirect methods of stimulation of innovative activity abroad are generally directed on intensification of innovative processes as well as the creation of favorable economic conditions and sociopolitical climate for scientific and technical development. In spite of the fact that tax methods of innovative activity regulation are applied by the increasing number of the countries, the question of efficiency of different types of tax privileges remains open. The choice of methods of stimulation is defined first of all by national factors of the country: the level of development of national innovation system, features of the taxation system and priorities of innovative development.

References

- Shardin I.V. World of man, 2008, 3, р. 3–14.

- Mel'nikova I.N. Journal of International law and international relations, 2010,

- Bazhenova V.S., Pivovarov N.A. State regulation of innovative-technological development in modern conditions, Ulan-Ude: house of ESSTU, 2006, 200 р.

- Wang M. et al. Innovation, 2003, 8, [ER]. Access mode: http://stra.teg.ru/lenta/innovation/1879

- Beljakova A.A. News of Irkutsk state economic Academy, 2010, 5, р. 279–285.

- Tax incentives of innovation processes, edit. N.I. Ivanova, Moscow: IMJeMO RAN, 2009, 160

- Raising EU R&D Intensity. Report of European Commission by an Independent Expert Group. Luxembourg, 2003, 62

- Zverev A.V. Bulletin of the financial University, 2008, 4, p. 35–56.

- Krasnov A.I. Russian foreign economic Bulletin, 2010, 7, p. 11–19.

- Mizhinskij M.Ju. Accounting and statistics, 2005, 7, p. 163–168. 11 Pavlov Ju.V. Innovation, 2005, 4 (81), p. 43–49.

- Komkov N.I., Bondareva N.N. Problems of forecasting, 2007, 1, p. 4–26.