The article is devoted to theoretical approaches to the definition of social audit. The article is based on the method of comparative analysis. The authors analyze the various definitions of social audit and summarize the views of researchers in this field. Two main approaches are highlighted that reflect the content of the category.

Background research is determined by the fact that in today's economy become important resources represented in the labor market. No production is impossible without a man, as the effective use in the production of knowledge, innovation and creativity becomes a decisive factor of economic growth, which is a precondition for social progress. It is essential that economic policy and social policy are mutually reinforcing, creating conditions for sustainable development of enterprises.

Quality personnel, its ability and willingness to solve problems in the conditions of reforming, largely determine the efficiency of the subjects. The formation of a competent staff of an appropriate level of professional competence is an important condition for the successful implementation of the challenges facing businesses.

Each manager strives to maintain the pace of development and stability of the enterprise. Competitiveness and increase productivity is only possible with the effective use of human resources of the organization and a clear system of management. Therefore, in addition to traditional forms of control over the enterprise is gaining growing importance of human resource control. Entities must use all their available reserves to the staff really played a major factor in improving the competitiveness of the organization, productive and motivated worked. Identify unused reserves and develop ways to improve the personnel management system will help the social audit. Thus, in a market economy, the need for audit is felt not only in finance, but also in the sphere of social relations.

On the staff of the term «audit» has come from the financial activities of enterprises. Audit gradually transformed into a large interconnected system of integrated control activities in the company. It is divided by industry, sub-sectors, areas such as, for example, management audit, operational audit, human resources, intellectual property audits, audit quality management, etc. But for all kinds of general audit is its essence as a systemic form of implementation of the diagnostic study, which suggests the effectiveness of the organization and how to improve them.

So, in a modern market economy cannot be the normal functioning of the companies without a developed system of social partnership, because it is the human factor ensures the effectiveness of the company.

Management of social development at the level of the organization is aimed at creating conditions for the effective implementation of the labor potential of the team and the formation of a high level of motivation of human resources, which in its totality allows to increase productivity and improve financial performance. Accordingly, there was a need for a tool of analysis and evaluation of the effectiveness of the control mechanism of social development organization. According to scientists, it is the social audit is a major instrument for regulating the state of social and labor relations.

Formulation of the problem. Social audit is a new phenomenon in the modern social sciences and social practices of the global market economy. Formation of a new category requires its theoretical understanding and defining its place in the system of economic categories of modern economics.

Undeniable contribution to the development of social audit issues brought many scientists. However, appreciating the contribution of scientists, is to recognize that to date no-one comprehensive definition of social audit. Therefore, the purpose of this article is to review and synthesis of approaches to the definition of social audit.

Research methods. The paper used methods such as description of procedures, building schemes, the method comparisons.

The main part. From the middle of the XX century in Western countries there is a change in the perception of the social aspects of the market economy. Social audit appears, and becomes effective and relevant technologies of regulation of social and economic relations in countries with developed market economies [1].

In the scientific literature, the concept of social audit appeared in the 1940s. It was introduced in the scientific revolution professor of economics at Stanford Business School Kreps T.J., the term is used to describe methods of verification (verification) of companies talking about their social responsibility. Also questions, allows the audience to appreciate the significance and role of the human factor for the company, have been considered in the «Social Audit on Service Management survival» (Umblija J.) [2].

In 1953, an American researcher Bowen H.R. in his writings describes the concept, according to which «social responsibility can be extended to business, and the firm receives income is a factor in the development of the state's economy».

In the 1960s, British economist Goyder D. considering the social audit as an effective tool for the management, which will allow the public to influence the policy of the company [3].

In the future, this trend developed a number of French researchers such as J.-M.Peretti, J.-L.Vachette, P.Candau, A.Couret, J.Igalens.

In 1984, J. -M.Peretti and J. -L.Vachette in the book «Social Audit» address issues of economic, technical and social efficiency of organizations in terms of the methodology of social audit [4].

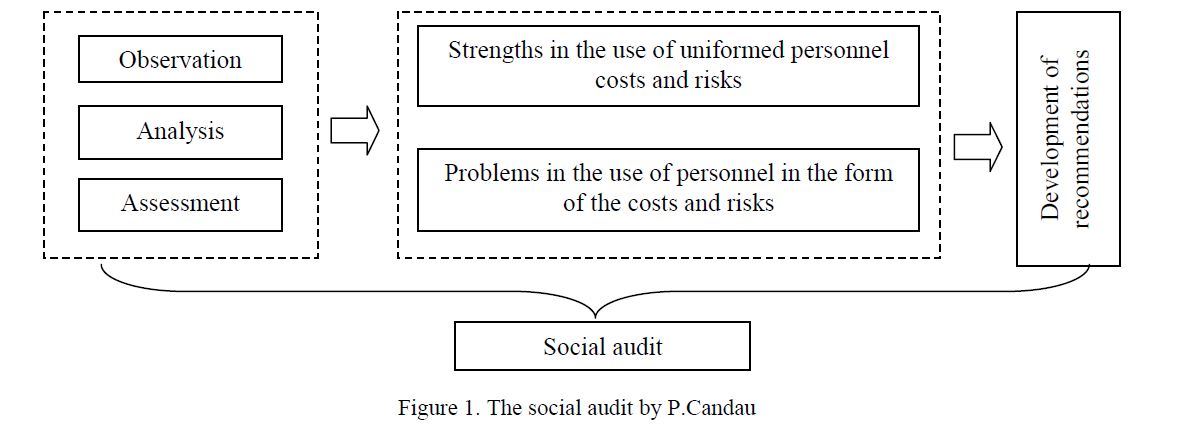

In 1985, the work is published P.Candau, in which social audit is considered as «independent monitoring activities, analysis, evaluation and recommendations. The activities are based on the methodology and use the method allows a comparison with a reference book to determine first the strengths and challenges in the use of uniformed personnel costs and risks. This makes it possible to diagnose and identify the causes of these problems, assess their significance and, finally, to make recommendations for the implementation of specific actions, which, however, never implemented by the auditor» (Figure 1) [5].

Figure 1. The social audit by P.Candau

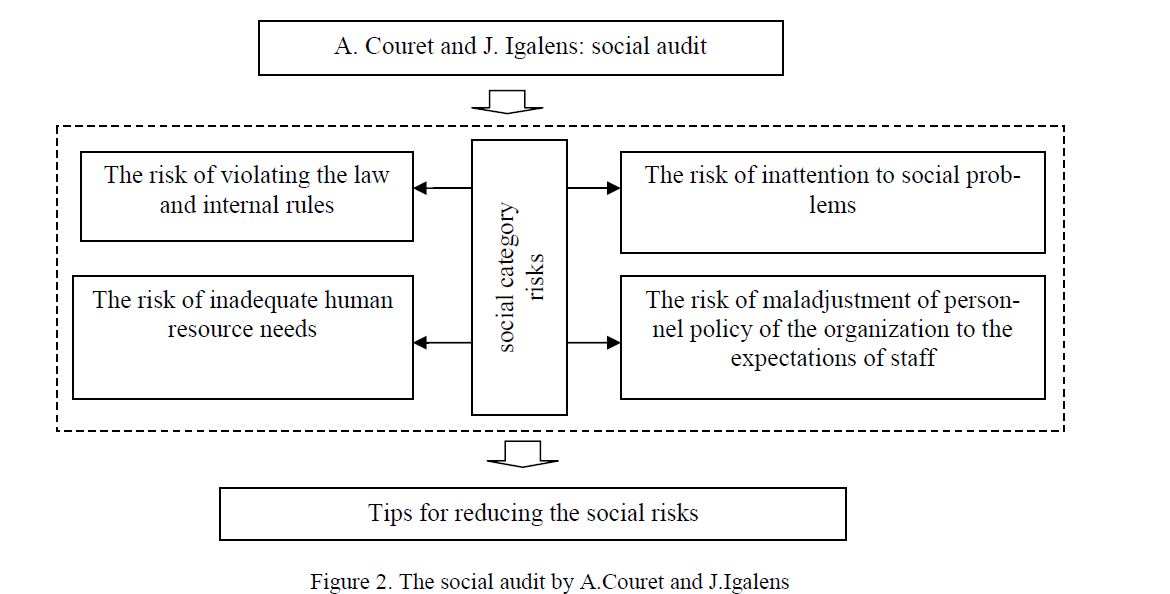

A.Couret and J.Igalens consider social audit (Figure 2) as a tool for the analysis of each factor of 4 categories of social risks, based on which the recommendations offered by the method of reduction [6].

Figure 2. The social audit by A.Couret and J.Igalens

In 1988 the President of the International Institute of Social Audit Vatue R. published a monograph «Audit of social control». In his opinion, «social audit — management tool and a method of observation, which by analogy with the financial and accounting audit provides an opportunity to assess the ability of a business or organization to manage emerging human or social problems caused by professional activities».

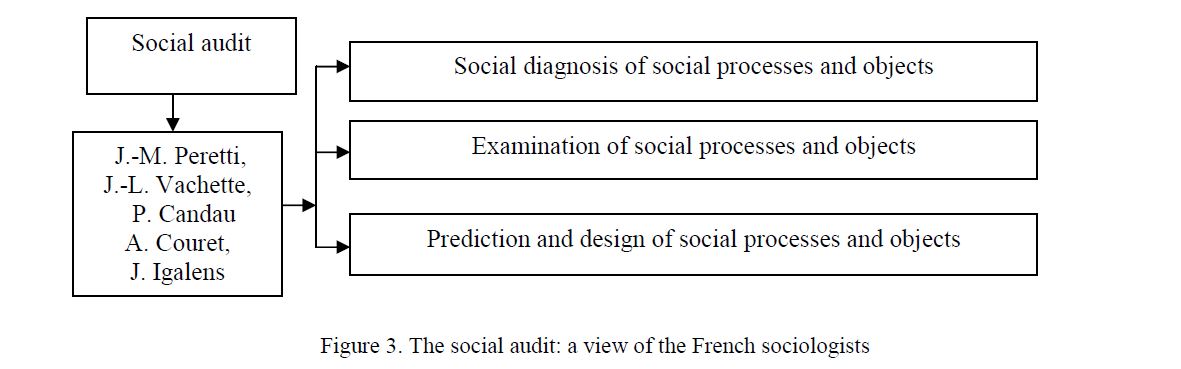

Thus, in the work of the French sociologist social audit is seen as a complex technology, some research procedure, which includes social diagnosis, assessment, prediction and design of social processes and objects (Figure 3).

Figure 3. The social audit: a view of the French sociologists

At present, the social audit has become a stable system, with its characteristic features, procedures, technologies, and with specific methods of analysis and is considered by many scholars. In modern literature in the most general form of social audit — a process evaluation, preparation of the report, to enhance the functioning of the organization and style, a means of measuring its impact on society as a whole.

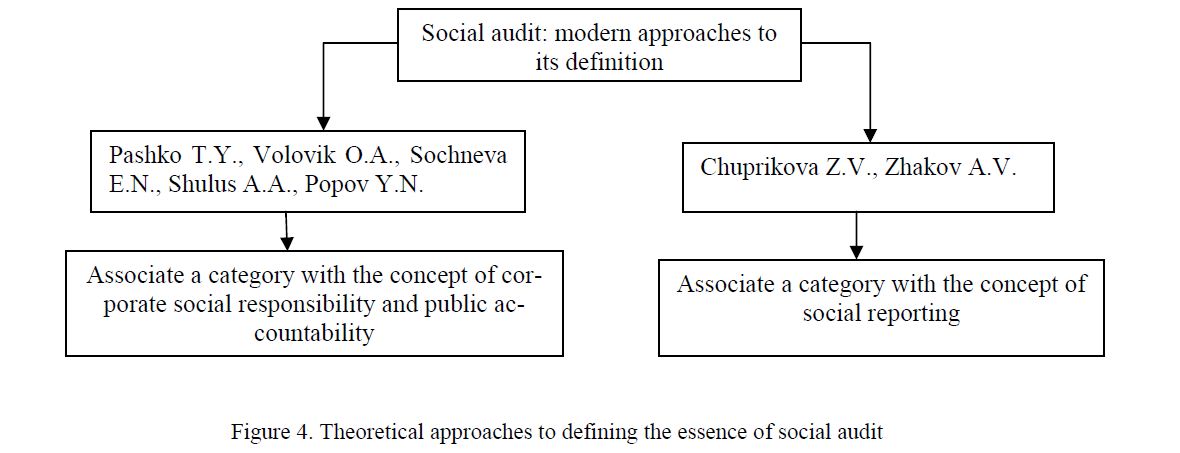

Pashko T.Y. considering the social audit as «a procedure of information and analytical support for performance management of modern (market-oriented) businesses in the field of regulation of social and labor relations in order to identify areas of imbalance and tension, to maintain a stable climate in the workplace, the development of social partnership and the effectiveness». According to the author, the determining factor of a qualitatively new system of social and labor relations is the social responsibility of all actors, based on a modern legal regulation in the sphere of labor [7].

Volovik O.A. under the social audit understands «category, reflecting the process of diagnosis of social space, which includes a multi-dimensional evaluation, systems analysis and forecast the state of the object under study scenarios. According to the author, in a complex form of «social audit is an assessment of the material, social and spiritual conditions for the reproduction of social capital territorial community. Under conditions of inequality of socio-economic development of territories (depressive, donors, and other oneindustry towns.), topical, natural-climatic, socio-cultural factors in the development and indicators can be more specific and detailed. Human and cultural capital determines the capabilities of civil society, the key determinant of the development of the vector are partnerships of public organizations with authority. The degree of public trust in the authorities is one of the criteria for its effectiveness [8].

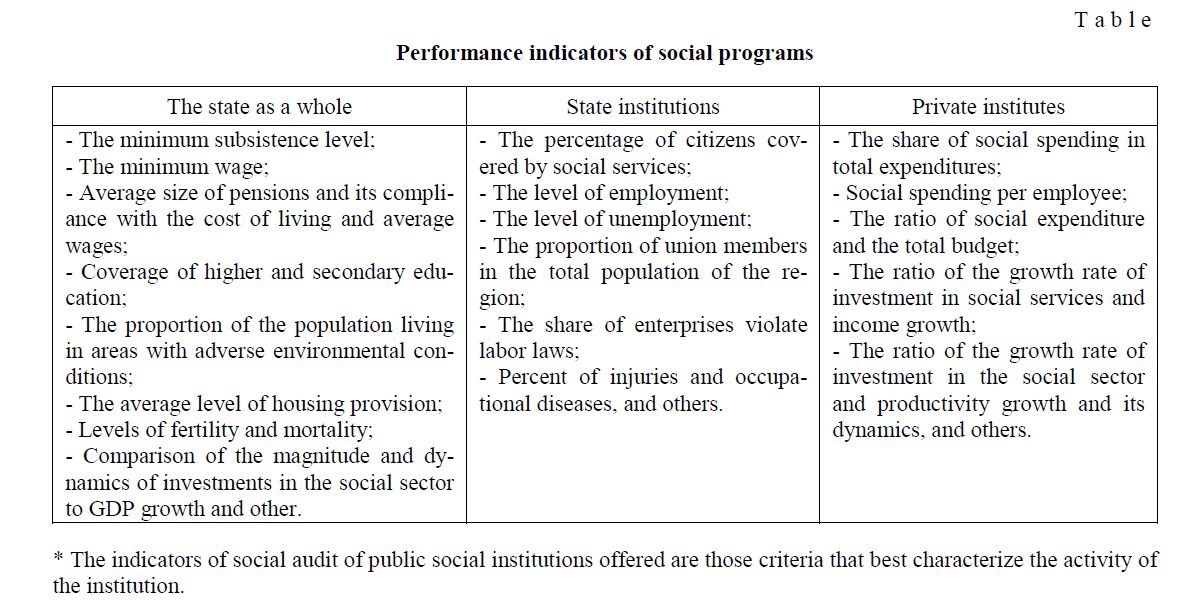

According to Sochneva E.N. «Social audit is analysis of the effectiveness of social programs of the institution and the verification of their compliance with the selected standards. It is a measure of the degree of corporate social responsibility. Social audit system may be used as public institutions, both private institutions, and in general to the state. «In this regard, the author suggests in conducting social audit applied to each institute its own criteria for evaluating the effectiveness of which are presented in Table [9].

Performance indicators of social programs

T a b l e

* The indicators of social audit of public social institutions offered are those criteria that best characterize the activity of the institution.

In theory of Shulus A.A. and Popov Y.N. the social audit is based on the concept of socioeconomics — interdisciplinary scientific discipline, the center of which is the reproduction of human resources. According to them the social audit in the broadest sense — an analysis of the effectiveness of social programs of the company and check their compliance with the selected standards in a narrow — verification of social accountability or «a specific form of analysis, audit conditions of social environment of the organization in order to identify social risk factors and develop proposals for reduce their interaction». Like the financial or accounting audit, social audit is a unique management tool. The essence of it is reduced to diagnose the causes of social problems, multifaceted assessment of the importance, urgency and opportunity to resolve them, the development of specific recommendations for the prevention of social tension in the organization, improve the management of personnel [10].

Thus, the authors examine the social audit «as an effective tool for regulating socio-economic relations, can significantly increase the level of human resource management — critical factor production in a modern market economy».

Chuprikova Z.V. and Zhakov A.V. associated social audit with the evaluation process, the preparation of the report, to enhance the functioning of the organization and style, a means of measuring its impact on society as a whole. With the help of social audit can be measured by the degree of corporate social responsibility. They are evaluated primarily formal and informal rules of behavior within the organization, the views of the parties interested in the company, in order to select an environment conducive to quality management and human resource development. Like the internal financial audit, social audit requires a clear statement of research criteria: what kind of results the company aims to achieve, which groups the public opinion affect the success of its business and public performance will be measured by its effectiveness [11].

Concept of social audit is reflected in the works of local researchers.

Taspenova G.A., Kaldybaeva T. describe the social audit as a specific form of analysis, audit social environment of the organization in order to identify social risk factors and develop proposals to reduce their exposure [12,13].

Thus, according to the analysis of the theoretical aspects of social audit are two basic approaches to the nature of this category (Figure 4).

Figure 4. Theoretical approaches to defining the essence of social audit

The term «human resources audit» is now also widely spread, which refers to «a kind of diagnostic tool and the conformity assessment of personnel potential of the organization to its objectives and strategies». Abdurakhmanov K.H. and Y.G.Odegov develop this definition, adding personnel audit identifying strengths and weaknesses of the team, its trends and possible variants of behavior in the changed situation. Some authors introduce the concept of organizational and personnel audit and evaluation include not only qualitative and quantitative characteristics of the staff, but also the analysis of HR processes, organizational structure.

In North America, the term «audit of human resources» is «range of services in a systematic, formalized and extensive examination (evaluation system of personnel management», «assessment is carried out in the organization of the management of personnel», «total quality control management of human resources individual division or company as a whole».

Conclusion. Thus, the approach to personnel as a resource management system changes qualitatively. The leaders formed an understanding of what is needed to make personnel decisions, appropriate development strategy of the organization and designed for long-lasting effect, invest in search and retain high-quality staff to shape generalists, which take responsibility for the decision to not only current, but and strategic objectives.

In response to the substantial increase in volume and complexity of personnel management emerged as a kind of social audit management tool, similar to financial accounting or auditing. Specificity of social audit is based mainly on the nature and character of the audited entity, which dictate the use of certain methods suitable to this type. Area of human resources is mainly qualitative characteristics, therefore, insufficient to offset the quantitative information, the auditor uses the methods and techniques peculiar to the social sciences.

Its essence is to diagnose the causes of problems arising in the organization, assess their significance and possible solutions, formulate specific recommendations for the management of the organization. In other words, the social audit is an analysis of social risk factors and developer of proposals to reduce their impact. Its aims are evaluate the ability of the organization to resolve social problems that arise inside and outside, and manage those of them that have a direct impact on an individual's career. Thus, the purpose of social audit is examination of the work of enterprise management in the improvement of employment, reduction of stress and absenteeism, increase job satisfaction among employees.

At present, the social audit is a tool of management and control, as well as the method of observation, which is similar to financial accounting or auditing, designed for a specific area — labor relations.

The analysis presented in the scientific literature approaches to the definition of social audit showed the prevalence of these socio-economic criteria to be considered a social audit in relation to the study of social and labor relations at the company, the management of human resources in the enterprise. An important feature is the representation of social audit as a tool of social partnership. There was developed the idea of communication of social audit and social responsibility.

References

- Meshkov V. Social audit: the Russian practice // [ER]. Access mode: finanal.ru

- Contact the audit organization's management system // [ER]. Access mode: allrefs.net

- Tulchinsky L., Terentyeva V.I. Integrated brand management: every employee is responsible for the brand, Moscow: Vershina, 2006, p. 352.

- Peretti J.-M. & Vachette J.L. Audit social, editions d 'Organisation, Paris,

- Candau P. Audit social, Vuibert, 1985, p.

- Couret A., Igalens J. L'audit social, Paris: Presses Universitaires de France, 1988, p.

- Pashko T.Yu. Bulletin of the University, Moscow, 2011, № 4, p. 77–79.

- Volovik A. Bulletin of the Pomeranian University, series «Humanities and social sciences», Archangelsk, 2010, № 5, p. 39–42.

- Sochneva N. The role of social policy in the construction of the welfare state // [ER]. Access mode: www.dissercat.com

- Shulus A.A., Popov Yu.N. The social audit, Moscow: ATIS, 2008, p.

- Kuznetsova N.V. Proceedings of the Irkutsk State Academy of Economics, 2011, №

- Taspenova G.A. Prerequisites of formation and development of social audit in Kazakhstan // [ER]. Access mode: rusnauka.com

- Kaldybaeva T. Sayasat-Policy, 2008, № 9, p. 45–50.