Article is devoted to a problem of improvement of the financial analysis at the domestic enterprises, in particular to modeling of a financial condition. The dependence equations between separate indicators of accounting financial statements by means of use of economic-mathematical tools on the example of one of the largest industrial enterprises of the North Kazakhstan area — JSC «Munaymash» are considered. The author makes recommendations about forecasting of a financial condition of the enterprise by means of its modeling by means of which probably in due time to make changes to the program of development of the enterprise and effectively to operate resources for achievement of the maximum financial result.

Economic transformations in Kazakhstan, accounting transformation paid again attention of science and practice to such major element of analytical work, as the financial analysis. The financial analysis is a component of financial management, as its performers financial managers and accountants act, and the main users are the legal entities and individuals interested in activity of this enterprise, including not having direct access to its internal information base.

In modern economy the role of the financial analysis not only amplified, but also qualitatively changed. It is connected, first of all, by that the financial analysis from an ordinary link of the economic analysis turned in the conditions of the market into the main method of an assessment of all economy of the enterprise. Increase of a role of the financial analysis is caused, first of all, by that its main and final task is to provide competitiveness of the concrete enterprise. Achievement of a good financial condition and competitiveness demands, among other factors, systematic carrying out the financial analysis as complex analysis of all financial and economic activity. In the conditions of market economy it is necessary to develop and improve such direction of analytical work as modeling of a financial condition of the enterprise which allows to create the strategic activities of the enterprise relating to its financial policy. Modeling an existing and desirable financial situation, it is possible to analyze distinctions of existing and desirable model and to develop concrete measures for elimination of these distinctions.

It should be noted that this model has to meet such requirements, compliance which would allow entering carrying out the financial analysis in structure of corporate information system of the enterprise easily. When developing model it is necessary to consider specifics of the Kazakhstan economic relations and possibility of integration with world economic communities, the international standards concerning reporting forms, and also the standard terms. All this led to emergence of need of increase in scientific researches in the field. The modern concepts existing within the theory of the economic analysis don't satisfy to the tasks facing the domestic enterprises. The stated circumstances predetermined relevance of a subject of the scientific article. We will consider process of modeling of a financial condition of the enterprise in aspect of realization of the following stages:

- The analysis of influence of factors on a financial position of the

- Creation of matrixes of influence of indicators of accounting financial statements on solvency and financial stability of the enterprise, influence of indicators of accounting financial statements on business activity of the enterprise, influence of indicators of accounting financial statements on financial results and efficiency of activity of the

- Calculation of creation of the equation of dependence between separate indicators of accounting financial statements by means of use of economic-mathematical

- Mechanism of realization of information models of the analysis of a financial

In the course of modeling of a financial condition of the enterprise, first of all, it is necessary to consider influence of factors on a financial position, such as money, stocks, receivables, non-current assets, accounts payable, loans and the credits, own capital, proceeds from sales of goods, production, works, services, prime cost of the sold goods, production, works, services. Within this article it isn't possible to describe in full the mechanism of impact of change of factors on a financial position of the enterprise. We will bring it in a summary:

- the size of stocks influences on: current assets, cost of property of the enterprise, liquidity of balance, coefficient of security of stocks own sources, indicators of sufficiency of sources of formation of stocks, type of a financial situation on degrees of financial stability, coefficient of security with own means, coefficient of a ratio of the mobile and immobilized means, liquidity coefficients;

- the size of receivables has impact on: current assets, cost of property of the enterprise, liquidity of balance, coefficient of security with own means, coefficient of a ratio of the mobile and immobilized means, liquidity coefficients;

- change will be a consequence of change of size of non-current assets: costs of property of the enterprise, liquidity of balance, indicators of sufficiency of sources of formation of stocks, type of a financial situation on degree of financial stability, coefficients of security with own means, ratios of the mobile and immobilized means, maneuverability of own capital;

- change of size of accounts payable will effect on: short-term obligations, loan capital, sources of financing of property, liquidity of balance, liquidity coefficients, coefficient of a ratio of own and borrowed funds, financing coefficient, autonomy coefficient, coefficient of financial dependence;

- the size of loans and the credits influences on: the loan capital, sources of financing of property, liquidity of balance, surplus (lack) of own and long-term loan sources of formation of stocks, surplus (lack) of the total value of the main sources for formation of stocks, type of a financial situation on degrees of financial stability, liquidity coefficients, coefficient of a ratio of own and borrowed funds, financing coefficient, autonomy coefficient, coefficient of financial dependence;

- influence of change of own capital: sources of financing of property, liquidity of balance, financing coefficient, coefficient of a ratio of own and borrowed funds, indicators of sufficiency of sources of formation of stocks, type of a financial situation on degrees of financial stability, autonomy coefficient, coefficient of financial dependence, coefficient of security with own means, coefficient of security of stocks own sources, coefficient of maneuverability of own capital;

- influence of change of revenue from sales of goods, production, works, services and prime cost of the sold goods, production, works, services on financial results and efficiency of activity of the enterprise: cumulative revenue, income from sales, taxable income, net income, profitability of sales, profitability of noncurrent assets, profitability of current assets, profitability of own capital, profitability of assets, profitability of a production activity [1; 19].

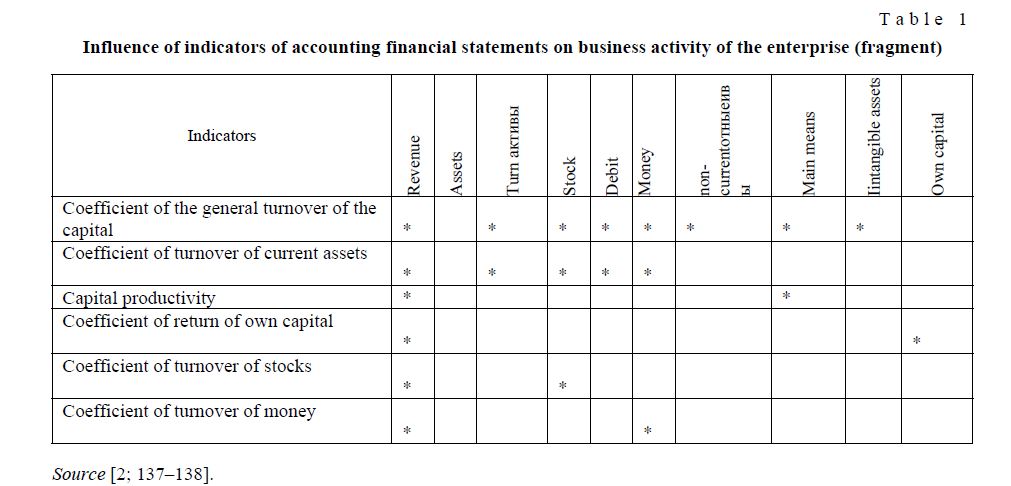

On the basis of the carried-out analysis possibly creation of matrixes of influence of indicators of accounting financial statements on solvency and financial stability of the enterprise, influence of indicators of accounting financial statements on business activity of the enterprise and influence of indicators of accounting financial statements on financial results and efficiency of activity of the enterprise. In view of a large number of data we will give a fragment of a matrix of influence of indicators of accounting financial statements as an example on business activity of the enterprise (Table 1).

At the following stage of modeling of a financial condition of the enterprise by means of use of economic-mathematical tools it is necessary to carry out calculation of creation of the equations of dependence:

- own capital from the size of current assets, non-current assets, net income

- between the size of the loan capital and current assets;

- the short-term credits and loans from short-term receivables;

- between the period of a turn of current assets and the period of a turn of own capital;

- income from sales and net income,

This list remains open as other options of creation of the equations of dependence are possible also.

T a b l e 1

Influence of indicators of accounting financial statements on business activity of the enterprise (fragment)

Source [2; 137–138].

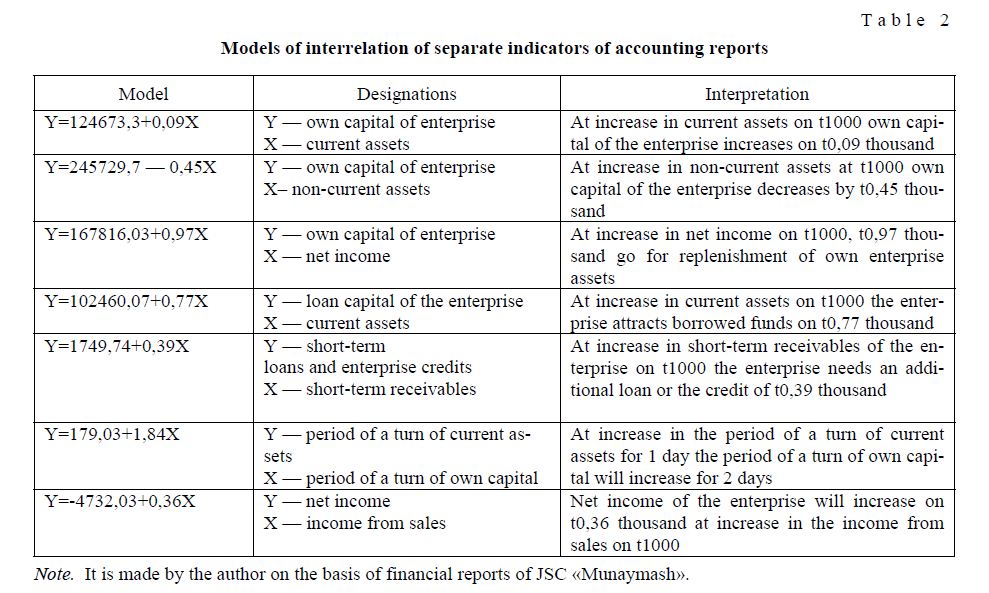

On the basis of the analysis of data of accounting financial statements for 2010–2012 of one of the largest industrial enterprises of the North Kazakhstan area — JSC «Munaymash» which primary activity is the production of borehole bull pumps and other production for the large oil companies conducting oil production on the fields of the Western Kazakhstan, constructed the linear models of pair regression describing the above dependences which values are presented in table 2.

Taking into account a certain degree of an error it is possible to use the developed models of interrelation of separate indicators of accounting reports in forecasting of a financial condition of the enterprise. Owing to limitation of volume of this article as an example we will consider one of aspects of the analysis.

Models of interrelation of separate indicators of accounting reports

T a b l e 2

Note. It is made by the author on the basis of financial reports of JSC «Munaymash».

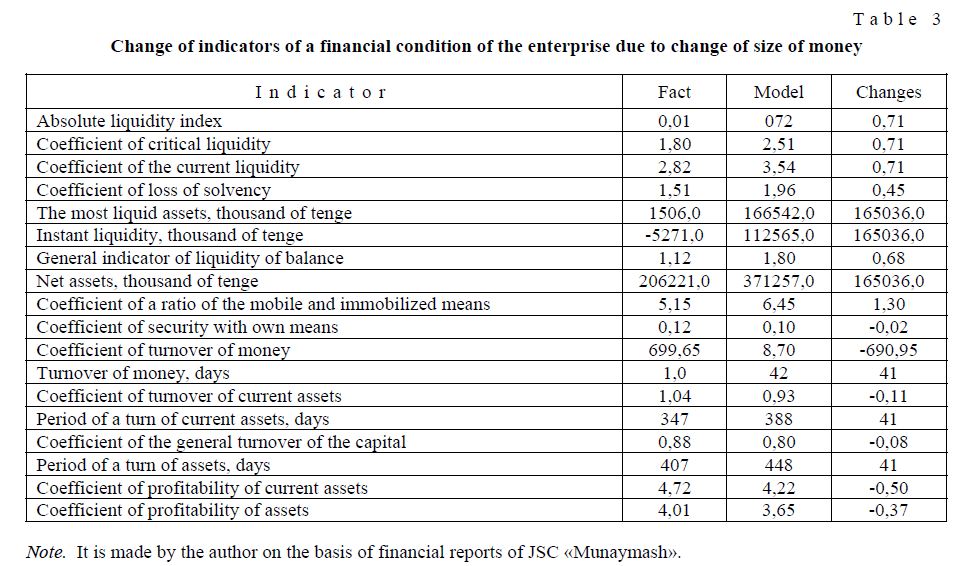

The analysis of a financial condition of JSC «Munaymash», carried out on the basis of accounting financial statements for the period 2010 for 2012, allowed to reveal problem zones of the enterprise which can significantly influence solvency, financial stability, business activity and efficiency of activity [3]. By means of modeling it is possible to define how the financial condition of the enterprise will change at improvement, deterioration and an invariance of data.

One of the reasons of decrease in solvency and financial stability of object of research is the lack of money. In the fourth quarter of 2010 the enterprise sharply reduced the volume of free money by the considerable sum, thus, having reduced the instant liquidity. If the enterprise left this sum on the settlement account, other things being equal, indicators of a financial condition would have the appearance presented in table 3.

At increase in money the absolute liquidity index to 0,72 considerably will increase, standard value of this indicator will be observed. The enterprise will be able to cover the short-term obligations at the expense of the most liquid assets, including money, in the shortest terms. Coefficients of critical and current liquidity will increase, and at the expense of the last at the enterprise opportunity to lose the solvency in the next 3 months will decrease. The enterprise will cover the accounts payable with available money and short-term financial investments.

T a b l e 3

Change of indicators of a financial condition of the enterprise due to change of size of money

Note. It is made by the author on the basis of financial reports of JSC «Munaymash».

As the volume of current assets will increase, the ratio of the mobile and immobilized means will change. The coefficient of a ratio of the mobile and immobilized means will increase on 1,3.

Turnover of money will be slowed down, and the turn period respectively will increase for 41 days, i.e. efficiency of use of money will decrease. Decrease in efficiency of activity of the managing subject will be observed also, coefficients of profitability will decrease.

Thus, on the basis of analysis data the management of the enterprise should make a choice: to improve the solvency, i.e. to make a choice for financial security and stability, or to increase efficiency of use of money due to their investment.

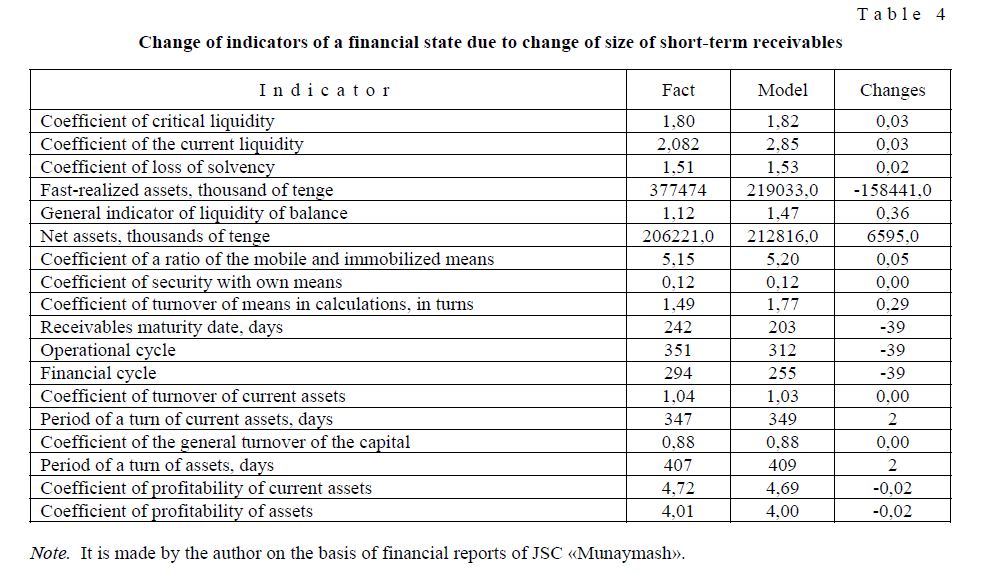

Amount of money can be filled up due to collecting receivables which is «sick» article in the reporting of the enterprise and has essential impact on a financial condition. Thereof it is necessary to consider influence of short-term receivables on a financial condition of the enterprise.

The enterprise has opportunity to reduce short-term receivables. Under the influence of this factor and taking into account increase in money, i.e. without refusing the previous assumption, the financial condition of the enterprise (Table 4) will change.

Change of indicators of a financial state due to change of size of short-term receivables

T a b l e 4

Note. It is made by the author on the basis of financial reports of JSC «Munaymash».

Under such circumstances there will be an acceleration of means in calculations on 1,77 turns and reduction of a maturity date of receivables and, respectively, operational and financial cycles for 39 days at simultaneous preservation of solvency, financial stability and efficiency of activity at approximately same level, as before changes. However receivables maturity date still considerably exceeds an accounts payable maturity date. Therefore it is necessary to consider other factors which have impact on financial stability of the enterprise.

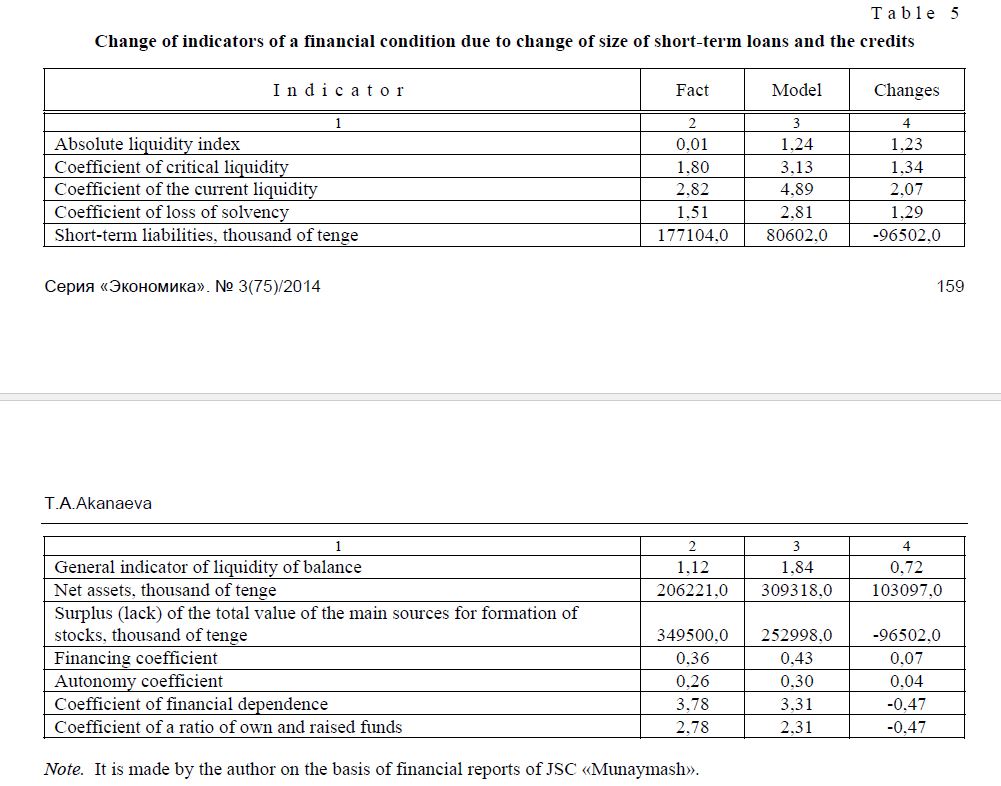

Analyzing financial activity of JSC «Munaymash», it was revealed that the enterprise strongly depends on loan sources of financing; generally it is the credits of banks. From the model describing dependence of size of the short-term credits and loans from short-term receivables, it is visible that when collecting shortterm receivables for the sum of t158 441 million the size of short-term loans and the credits can be reduced by t96 502 million. Then taking into account these changes indicators of a financial condition will assume the view presented in table 5.

Due to decrease in size of short-term loans and the credits and according to short-term obligations of the enterprise indicators of liquidity will increase and become much more standard value. The positive moment is improvement of liquidity of balance.

The financial condition as financial stability also is characterized as normal, the enterprise is able to form stocks at the expense of own current assets, long-term loans and the credits and the corrected sum of short-term loans and the credits while own current assets for this purpose at the enterprise don't suffice. Considering change of coefficients of financial stability, it is possible to speak about decrease in a share of borrowed funds in enterprise financing.

T a b l e 5

Change of indicators of a financial condition due to change of size of short-term loans and the credits

Note. It is made by the author on the basis of financial reports of JSC «Munaymash».

Forecasting of a financial condition by means of its modeling in relation to JSC «Munaymash», it is possible to continue and further depending on existence of problems and desirable results. But also this fragment of the analysis of a financial condition allows to draw a conclusion on the importance of modeling for an assessment of a financial situation as one of enterprise management system elements.

Summing up the result of the above, it should be noted that modeling of a financial condition allows objectively and to define possible options of development of the enterprise comprehensively. By means of modeling probably in due time to make changes to the program of development of the enterprise and effectively to operate resources for achievement of the maximum financial result. Thereof we consider necessary further improvement of one of methods of control over the enterprise as modeling of a financial condition.

References

- Bogatko А.N. Bases of the economic analysis of the managing subject, Мoscow: Finance and statistics, 1999, 206

- Varfolomeev V.I. Algorithmic modeling of elements of economic systems, Мoscow: Finance and statistics, 2000, 208

- http://www. Audit of financial reports of JSC «Munaymash» for 2010–2012.