Here the essence of cost management to ensure product quality is revealed. The feature of grouping the quality expenses developed by an American scientist A. Feigenbaum is examined. A particular attention is given to the classification of expenses by F. Crosby, which is based on the pursuit of zero level of defects in the organization (enterprise). We generalize the specific experience of the Japanese company «Toyota» in managing costs in general, including the costs of providing quality products. Given is the characteristic of the process of managing expenses associated with providing quality of products at Russian enterprises and companies. There is also a conclusion that within the international standard ISO 9004, the classification of expenses for quality is built on the basis of different methods of data collection, presenting and analysis of financial information elements.

The essence of quality costs and increasing interest in this category

Quality of products determines the extent of the company survival in market conditions, the pace of scientific and technological progress, the growth of production efficiency, saving all types of resources used in the enterprise.

Quality is a philosophical category expressing the inner certainty of an object, through which it is precisely this and not another. Economic definition of quality is set of properties that show the extent to which the object satisfy our needs [1; 51].

The quality expenses are determined primarily by the costs associated with the implementation of product life cycle stages. This is the cost of marketing, research and development, manufacturing, delivery and installation, support. The quality expenses can be both internal and external. The first are defined by the internal activities and the costs associated with production. The second are the costs associated with suppliers, consumers, agents, dealers, etc. [2; 158].

The quality expenses are of great importance, as they are almost always quite high and represent a decrease of profit and loss of orders. The expenses associated with quality, have a wide range and are determined by system failures, defective goods, overtime work, late delivery, complaints about service and warranty, product reviews, etc.

At present time, the interest in this category of costs has increased dramatically. This is due to the ever increasing competition, which is forcing manufacturers to take various measures to minimize expenses. Numerous studies and information survey conducted by companies show that the expenses associated with quality, typically range from 5 to 25 % of a total turnover [2; 159].

Products become more expensive because of extra costs that can be avoided. Determination of unnecessary costs is possible using the the measurement. Measuring costs allows selecting activities related to the product quality at different stages of the product life cycle. This makes it possible to consider quality as a parameter of business activity. Measuring the quality expenses focuses on high-cost areas, and offers the potential to reduce expenses. It allows evaluating the activities and provides a basis for comparative evaluation of different products (goods or services), processes and departments. Measurement is the first step on the path to management.

Stages of expenses on product quality formation

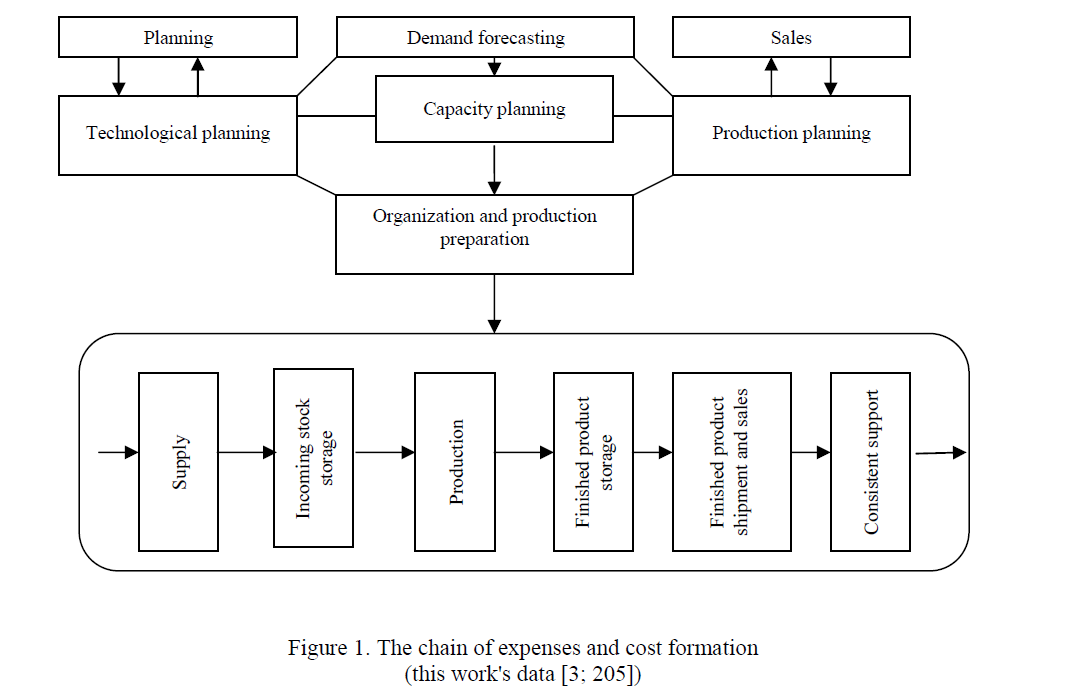

It is known that the quality of products must ensure consumer satisfaction with his requests, their reliability and cost savings. These properties are formed in the course of the entire reproductive activity of the enterprise, at all stages and at all levels. Together with them, the cost value of the product is born, which characterizes these properties, ranging from product development to the planning of its realization and aftersales service. Figure 1 shows the chain of formation of expenses and the cost of goods (or services).

Figure 1. The chain of expenses and cost formation (this work's data [3; 205])

The chain of expense formation allows specifying the principle of quality assurance and seeing when, that is, at what stage of activity, and where, in what unit it is realized. Thanks to each stage and unit head responsibility, it is clear who is responsible for product quality. What do we mean by guarantees, are the technical, technological, environmental, ergonomic, economic and other indicators of quality, which provide customer satisfaction.

These indicators have a qualitative expression and include planned, actual and criterialproduct qualities.

Classification of product quality expenses developed by A. Feigenbaum

Before proceeding to the analysis of modern classification of expenses on quality, let us focus on the different approaches of foreign scholars in the field of quality management.

Abroad, in the theory of quality management, there are two main classifications of product quality expenses [4; 175]:

- Classification by A. Feigenbaum;

- Classification of the F. Crosby

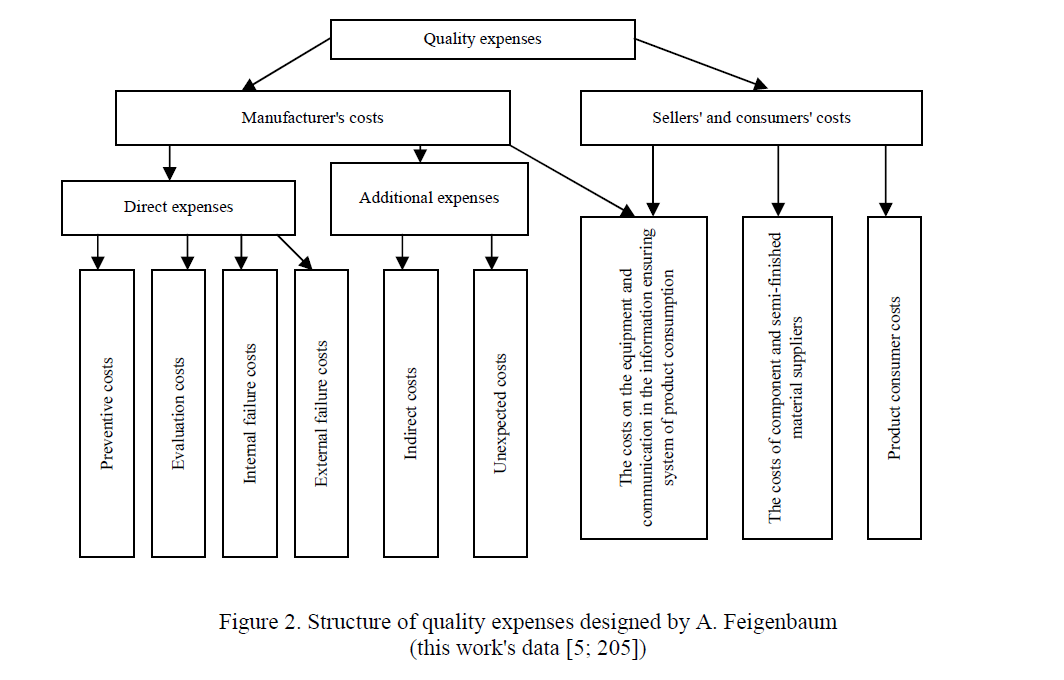

One of the most complete structures of the quality expenses developed by the American scientist

- Feigenbaum is shown in Figure

As can be seen from Figure 2, Feigenbaum has classified the manufacturer's quality expenses into four groups (direct expenses):

- The expenses on monitoring and quality inspection (estimation costs);

- Theexpenses on preventive actions;

- The expenses onremoval of internal defects;

- The expenses on removal of external

- Feigenbaum was able to formulate the general problem of the expense allocation between the groups, which minimizes their overall value. In special cases it gives useful results, but also leads to the logical difficulties, as in the process of solving this extreme problem some «economically feasible» level of defective product or inconsistencies appears, which seems absurd in principle. In addition, this approach poses a false dilemma of classifying certain types of expenses (ambiguous in nature) to one or another of the four groups. But the most important is the separation of quality expenses from the total costs of the enterprise, leading to the assigning of a quality controlin to an independent function and the loss of a direct link of this activity with the results of the business.

Figure 2. Structure of quality expenses designed by A. Feigenbaum (this work's data [5; 205])

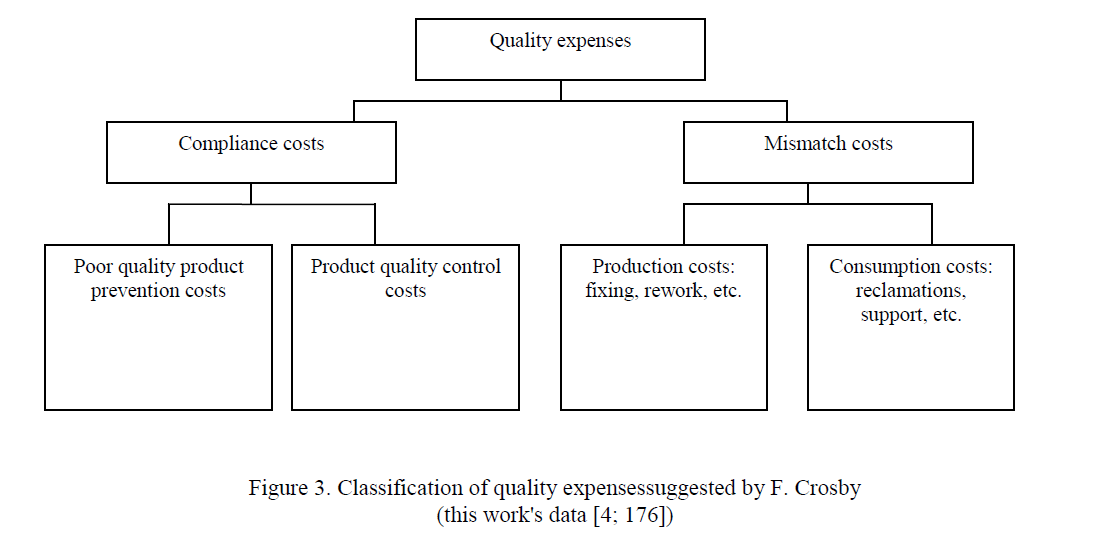

Classification of quality expensessuggested by F. Crosby

A renowned specialist F. Crosby has suggested a different approach, which consists in dividing the expenses into two categories. It is based on the pursuit of zero level of defects in the organization (Fig. 3).

Figure 3. Classification of quality expensessuggested by F. Crosby (this work's data [4; 176])

As seen from Figure 3, Crosby distinguishes the expenses associated with the production of the «right product at the first time» (the price of compliance), and the expenses caused by the need to correct that inconsistency or defective goods (the price of mismatch). For the diagnosis of the level achieved by the organization in relation to understanding the problems of quality, Crosby has introduced the so-called maturity grid. However, practical implementation of Crosby's approach due to a number of reasonsdid not always lead to the desired results. For example, while aiming for «zero defects» in meeting the demands of consumers, we can easily get stuck in today's understanding of «what is a zero level of defects» and overlook the unstated or emerging requirements. We will feel that we have achieved «zero defects» and all is well, but in fact the business is in grave danger. In addition,in order to make the slogan stop being just a slogan, a specific mechanism is needed, to bring to each employee's attention individual criteria of his activities in terms of achieving «zero defects».

Summarizing the experience of a Japanese company «Toyota» on production cost management

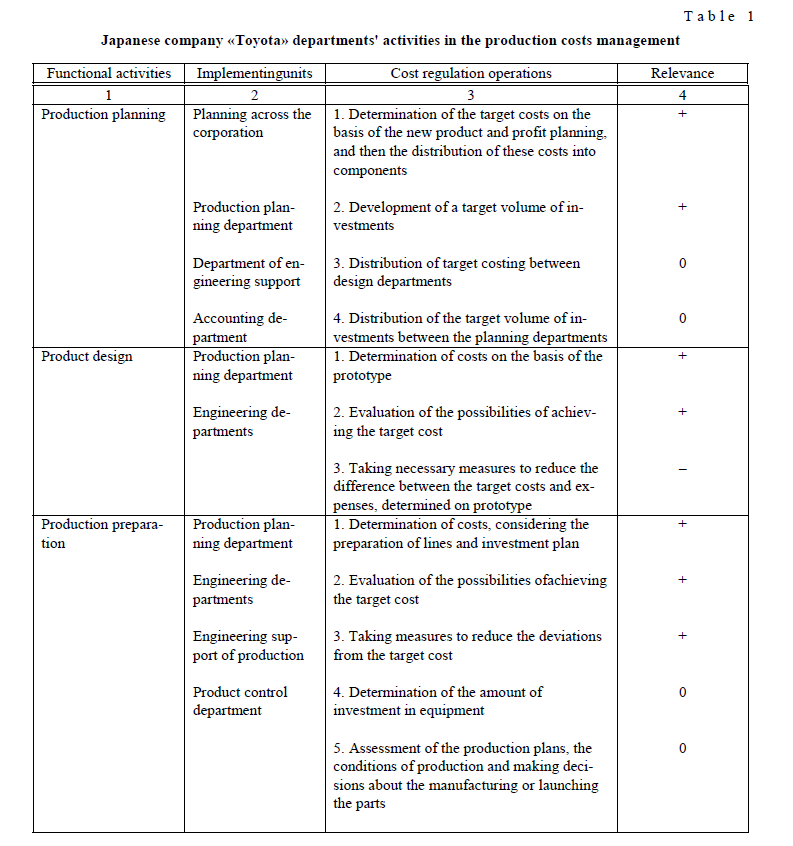

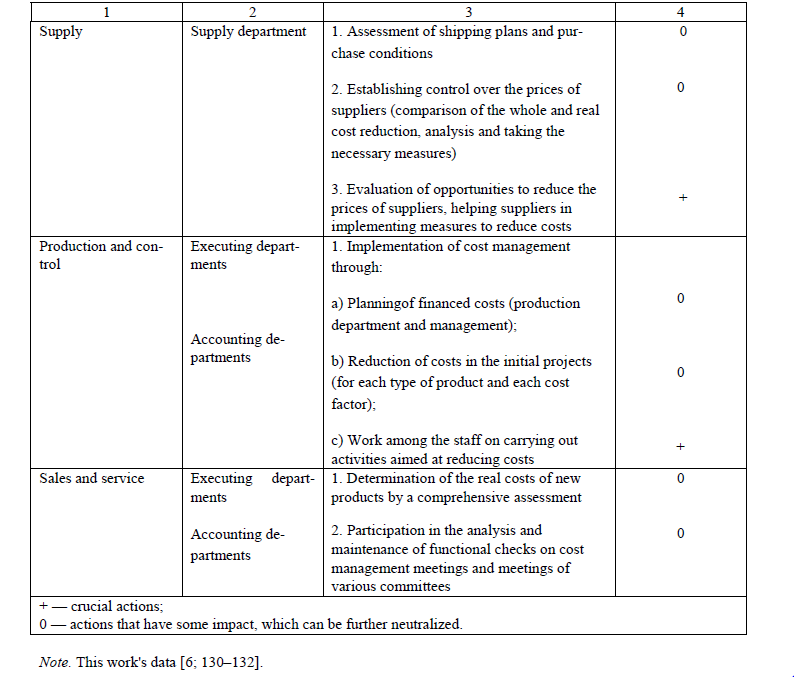

The famous Japanese company «Toyota» highlights the following stages of activities in the field of quality assurance: production planning, product design, production preparation, production, production control, sales and service, service quality control. At the same time, the defined responsibilities and actions of each department guarantee the quality at these stages (Table 1).

T a b l e 1

Japanese company «Toyota» departments' activities in the production costs management

Note. This work's data [6; 130–132].

Table 1 shows that all phases of the company's activity include elements of cost management.

Russia's experience in managing the costs associated with ensuring product quality

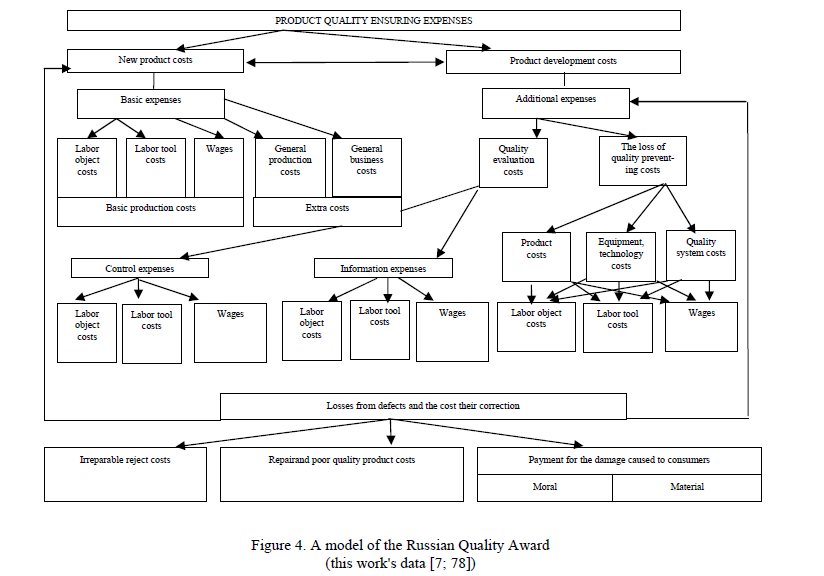

According to Russian experts [6; 77], the costs associated with quality are (Fig. 4):

- the costs of providing and guaranteeing the proper level of production quality (new product costs);

- the costs associated with losses in case of failure to achieve the proper level of quality (product development costs).

During the development, production mastering and the direct release of new products, the so-called core costs reveal, much of which reflects the cost value of the various factors of production, as well as overhead and general economic expenses attributable to the production through an estimate of the costs and additional costs due to the improvement of production and restoration of the product quality to the proper level in case of failure to achieve it.

One of the items of the additional expenses is the costs of quality assessment, including:

- the cost of supervisory staff;

- the cost of special testing equipment;

- checking department's or quality service's extra costs;

- the costs of information in the field of trade;

- the costs of organizing and carrying out sample surveys of consumer opinions about the product quality.

The expenses for quality loss prevention consist of the following items:

- the costs of reworking products that don't meet the requirements of consumers and the standards;

- the costs of verification, repair and modernization of professional tools, equipment, technology;

- the costs of implementing the quality system within the organization (its equipment, staff), development of standards, and other

Figure 4. A model of the Russian Quality Award (this work's data [7; 78])

There is another group of expenses that should be attributed to the basic or additional depending on the novelty products when they occur. These are the costs of defects and their correction. Their value may fluctuate dramatically and consist of the costs of products identified as defective in the future if there is irreparable reject, or, in addition to this, the costs of correcting them if the defect is not final. This may also include payment of moral and (or) physical damage caused to a consumer by a defective product. In the latter case, the costs associated with product quality, or rather lack of it, can be very high.

Classification of quality expenses in the ISO 9004

A variety of different approaches to the estimation of the quality expenses, an understanding that for a successful business, assessing the need for financial planning and control, have been reflected in the second version of ISO. Thus, in the ISO 9004, a classification of quality expenses is built on the basis of different methods of data collection, reflecting and analysis of financial information elements.

In the international standards for quality systems noted is the importance of assessing the effectiveness of the quality system from a financial (external) point of view. An effective quality system (QS) may have a critical impact on a profitability of the organization, in particular, by improving the economic activities, which leads not only to a decrease in defects and the costs of manufacturing products, but also to reducing the costs associated with the using the product.

International standards provide, for the purposes of uniformity, matching and synthesis of economic data, recommendations only on certain methods of calculation the quality expenses for the external (financial) reporting on the activities of the manufacturer within the quality system [8; 25, 26]:

- The method of calculating the quality expenses. This method determines the quality expenses that are a result of internal economic operations and external work. It is recommended to analyze the components of expenses basing on a RAҒ model (prevention, evaluation, defects). The prevention and evaluation expenses are a good investment, while the defect costs are considered

- The method of calculation of expenses associated with the processes. This method is used to analyze the cost of compliance. Expenses to meet all the consumers' demands in the reliability of the existing process are related to the costs of mismatch, that is, with costs due to violation of the existing process. Detection of inconsistencies is the source of

- The method of determining the losses due to poor quality. The main attention is paid to internal and external losses due to poor quality and the definition of tangible and intangible losses. Examples of external and intangible loss are the reduction in future of sales volume due to customer dissatisfaction. Typical internal intangible losses are the result of loss of productivity due to a rework, poor ergonomics, missed opportunities, etc. Material losses are the internal and external costs resulting from

These methods do not exclude the use of other ones, their improvement or a combination.

Financial aspects of the quality system reflected in the ISO 9000are the most complete characterization of approaches to determining the quality expenses that are currently in use abroad.

References

- Yeskerova А. Bulletin of Karaganda University, Ser. Economy, 2015, 2 (78), p. 51–57.

- Gerasimov I., Zlobina N.V., Spiridonov S.P. Quality Management: textbook, Moscow: KNORUS, 2005, 272 p.

- Tepman L.N. Quality Management: textbook, Moscow: UNITY-DANA, 2007, 352

- Rozova N.K. Quality Management, Saint Petersburg.: Vector, 2005, 192

- Aristov O.V. Quality Management: textbook, Moscow: INFRA-M, 2004, 240

- Ilyenkova D., Ilyenkova N.D., Mkhitaryan V.S. et al. Quality Management: textbook, Moscow: Banks and stock exchanges, UNITY, 1998, 199 p.

- Rozova N.K. Quality Control, Saint Petersburg: Piter, 2002, 224

- Okrepilov V. Quality Management: textbook, Moscow: Economy, 1998, 639 p.