Effectiveness of the insurance market development is largely determined by the level of its infrastructure, which should act as a well-functioning mechanism with a developed system of information and analytical support, in combination with public authorities, insurance market entities and stakeholders. The insurance market infrastructure is a set of professional participants of the integration insurance space, who serve insurance activities, which contributes to the effective functioning of insurance and the quality provision of insurance services. The basis of the insurance market infrastructure consists of such entities as insurance companies, insurance intermediaries, government, self-regulatory organizations, the insurance payments guarantee fund, professional participants of the insurance market: surveyors, actuaries, adjusters, insurance ombudsman, etc. This article considers the actual features of the institutional structure of Kazakhstan's insurance market, which affect the strengthening of the country’s competitiveness. In this context, the analysis of the existing Kazakhstan’s insurance market infrastructure was conducted. Based on the results of the study, the main directions of improvement of Kazakhstan's insurance market infrastructure were proposed: creation of a single information center, improvement of the national reinsurance system, development of the insurance market in general. The authors developed a model of the infrastructure of the national insurance market, that meets the modern requirements of competitive markets – sales and the mechanism of social protection of the population, in the conditions of integrative interaction.

In modern conditions of integrative relations, the competitiveness of a national insurance market is largely determined by the level of development of its infrastructure, which should constitute an effectively working mechanism in cooperation with developed system of information and analytical support, public authorities, insurance market actors and stakeholders. Let’s consider the institutional structure of the insurance market of Kazakhstan.

According to the National Bank of Kazakhstan data of January 1st, 2017, the following participants of insurance market are presented in Kazakhstan: 32 insurance organizations including 7 life insurance organizations, 15 insurance brokers, 59 actuaries, insurance payments guarantee fund as well as other professional market participants (surveyors, adjusters, underwriters etc.) [1].

T a b l e

The institutional structure of the insurance sector in Kazakhstan

|

Structure of the insurance market |

2012 |

2013 |

2014 |

2015 |

2016 |

|

The number of insurance organizations |

35 |

34 |

34 |

33 |

32 |

|

Including life insurance organizations |

7 |

7 |

7 |

7 |

7 |

|

The number of insurance brokers |

13 |

14 |

15 |

15 |

15 |

|

The number of actuaries |

82 |

72 |

71 |

62 |

59 |

|

Insurance payments guarantee fund IPGF |

1 |

1 |

1 |

1 |

1 |

|

The number of insurance companies of the Republic of Kazakhstan with foreign participation |

3 |

3 |

3 |

3 |

3 |

Note. Based on statistical data of the National Bank of Kazakhstan.

As it can be seen from the table, there have been no significant changes in the number of insurance companies for the five years, however each year there has been a reduction of operating insurance organizations. According to experts, the institutional structure of the domestic insurance market has been influenced by several objective factors such as the slowdown in the growth rate of Kazakhstan's economy – the result of growing crisis in the world trade due to fall of prices on energy and sanctions against Russia. At the same time, the requirements of the state regulator to ensure financial stability and solvency of insurance companies are growing.

One of the elements of the insurance market infrastructure is government regulation. Kazakhstan adopted an effective system of government regulation, based on operation of remote and inspectional supervision, in accordance with the principles of the legislative framework of the European Union.

State regulation of the insurance market is associated with the implementation of a set of economic and legislative functions in this area, among which:

- Conducting a targeted state policy in the field of insurance as a strategic sector of the economy through the formation of a legislative framework and the provision of a public climate conducive to the activation and popularization of insurance activities;

- formation of a competitive environment and an orientation towards increasing the competitiveness of national insurers and protecting the interests of policyholders;

- formation of an effective structure of the national insurance business and stimulation of its sustainable economic growth

The analysis of the activities of insurance organizations is an integral part of remote supervision and is carried out in order to identify the risks inherent in their activities, verify the requirements of the legislation of the Republic of Kazakhstan on insurance activities. When drawing up conclusions on the financial status of insurance organizations, based on the analysis of information provided in the conclusions on the financial status of insurance organizations, the rating of the insurance organization is determined according to the Financial Reliability Matrix.

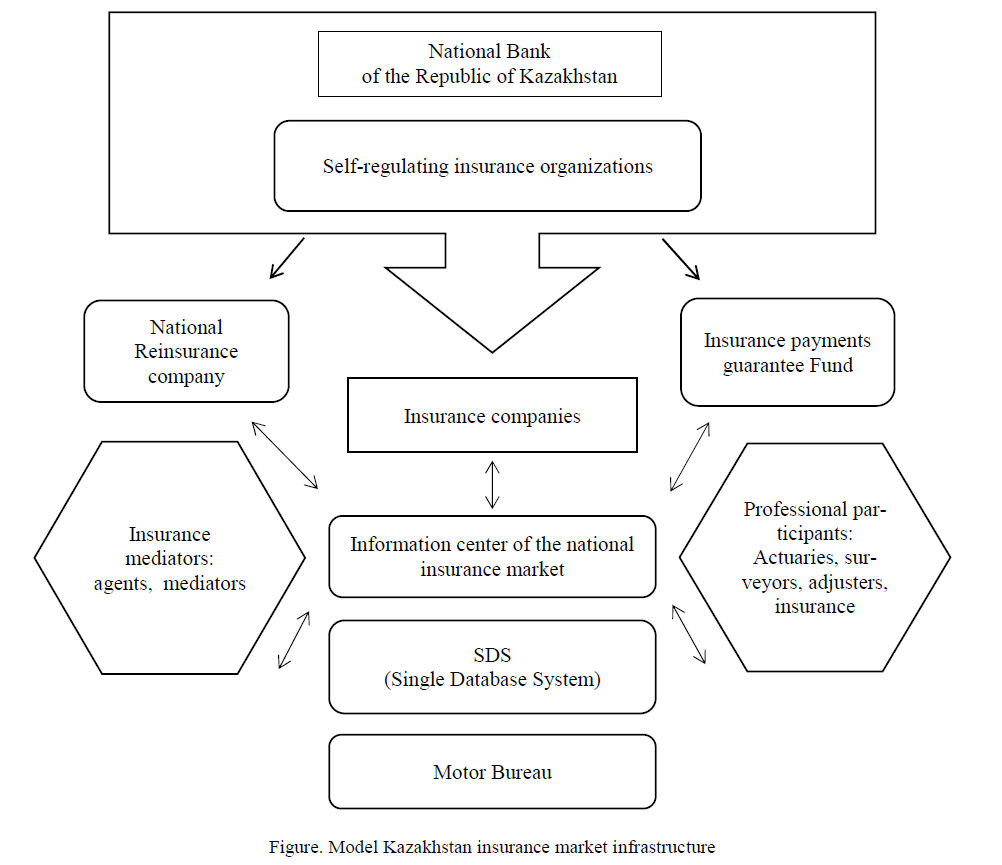

With the development of the insurance market, the active role belongs to self-regulating organizations. Along with the state regulatory body, the main self-regulating organization of the Kazakhstani insurance market is the Insurers Association of Kazakhstan.

The Association took the role of coordinating the activities of its members, to represent and defend their common interests in relations with the authorities, foreign organizations and other participants of the insurance relationship.

In total, there is an extensive system of infrastructure institutions operating in Kazakhstan. However, in order to overcome the problems of development of the Kazakhstani insurance market and strengthen its competitive advantages in the Eurasian Economic Space, the need to build anew infrastructure and upgrade existing institutions arises.

An important role in forming the insurance market infrastructure play insurance intermediaries. However, the activities of insurance agents in Kazakhstan are poorly regulated. Requirements for Kazakhstani insurance agents do not create conditions for their professional development and establishment as an independent infrastructure unit of the insurance market. In many developed countries, insurance agents must go through the stage of professional training and examination.

In case of successful completion an insurance agent is enlisted in the insurance agents register. Kazakhstan introduced a requirement for training and certification of insurance agents, and to increase the personal responsibility of each agent the National Bank should introduce a single center, where agents of all companies would obtain specific knowledge and undergo certification. The National Bank should also create a special website with data on all certified agents.

Regarding the insurance brokers, today they account only for 5 % of sales, which mainly represent the contracts with large companies that require serious risk assessment and integrated approach. At the same time, in Germany, in the United States and in France 40 to 70 % of insurance transactions are made through brokers. In the UK – over 85 %, in Mexico and Brazil – 50 % and 72 % respectively. Licensing, the prohibition on combining brokerage and agency activities has become a major challenge for these professional participants of the insurance market. Judging by this reason, according to the data from table 1, the number of insurance brokers did not change significantly [2].

As for the actuary. In Kazakhstan, actuarial activity is carried out in accordance with the Law of the Republic of Kazakhstan dated December 18, 2000 "On Insurance Activity" on the basis of the rules for the introduction of actuarial activity, the issuance of a license for the right to perform actuarial activity, the passing of an actuarial qualification examination, the involvement of an independent actuary to verify the activities of the actuary An independent actuary of the results of verification of the accuracy of calculations carried out by an actuary in the state of an insurance (reinsurance) organization uu".

An important element of the modern insurance market infrastructure is the secondary insurance institute The main objective of the creation of a single reinsurance market is to reduce the flow of reinsurance premiums outside of the national insurance market.

Thus, the minimum required reinsurers rating in Russia is at satisfactory reliability level. The legislation of the Russian Federation limits the share of reinsurers in insurance reserves and restricts combining reinsurance operations on life insurance and risks reinsurance of property insurance. In 2016 Russian State Duma approved a law on establishment of a National reinsurance company which is an effective step towards the formation of a full-fledged insurance system.

There is one reinsurance organization operating in Belarus – Belarusian National Reinsurance Organization (BNRO). According to the year 2015 results, the Belarusian National Reinsurance Organization concluded 9737 reinsurance contracts on 49 kinds of insurance.

There is no reinsurance market as an infrastructure element of the insurance system in Kazakhstan. The reinsurance organizations which hare non-residents of the country are required to have high ratings of financial stability, are limited in the amount of reinsurance risks, belong to the category of prudential norms. Thus, most of the reinsurance premiums occur in the countries of the European Union, which have high insurers ranking respectively. Unlike its neighbors, Kazakhstan did not create a national reinsurance company. This reduces the competitive opportunities of insurance business in the country. The internal reinsurance operations are being addressed through the availability of additional license on reinsurance, which direct insurance companies have [3].

Thus, a necessary element of the national insurance market infrastructure model, designed to solve the problem of premiums outflow abroad, is the improvement of the national insurance system by creating a domestic reinsurance company.

In international practice, one of the basic infrastructure elements of the insurance market is the insurance payments guarantee Fund. In Kazakhstan there is a system guaranteeing the insurance payments. Currently 30 insurance organizations are members of the insurance payments guarantee Fund. The main objective of the Fund is the implementation of insurance payments on obligations of insurance companies in liquidation of compulsory classes of insurance. It should be noted that from all the member countries of the Eurasian Economic Union, Kazakhstan is the only country having the institute of insurance payments guarantee fund. This infrastructure has proved its effectiveness and Insurance guarantee mechanism.

Regarding modernization of existing participants of the insurance market, the Insurance Ombudsman Institute continues to develop in Kazakhstan. The Insurance Ombudsman is an individual who is recognized to be independent in his activities, who carries out the settlement of disputes between insurance organizations and insures. Currently, there is a possibility for insures to resolve disputes with insurance organizations using online insurance disputes settlement system, which was developed and implemented by the Insurance Ombudsman.

The online system repeats the approved dispute resolution procedure, fully moderates the process of the settlement of disputes, ranging from filling a notice of intention to appeal to the Insurance Ombudsman and its automatic referral to the insurance organization and to monitoring the enforcement of the decision of the Insurance Ombudsman. The system allows to make queries, guide and get acquainted with documents, annotate documents and explanations, to virtually participate in the meetings, give explanations, ask questions and involve experts [4].

Among the core issues of the insurance market development is the improvement of the insurance culture, which is associated with increase of insure s’ trust to insurance companies. Consequently, there is a need to create an information center of the national insurance market. Establishment of the information center should be based on the program «Informational Kazakhstan-2020» and the Message of the President of the Republic of Kazakhstan dated January 31st, 2017 “Third modernization of Kazakhstan: global competitiveness – «The digital Kazakhstan».

In accordance with the adoption of the course «Digital modernization», the objectives of the national insurance market information center should include:

- free distribution of information about insurance companies and the services they provide via the Internet;

- fast and free comparative information on insurance rules and tariffs, set by various market insurers;

- confirmation of the reliability of the insurance company through the transparency of its work;

- receipt of a new effective sales channel for insurers, organization of online insurance purchase mechanism.

Users of the information portal will, first of all, be participants of the national insurance market, potential insurers, research institutes – researchers of this industry. Moreover, this information will be useful outside of the State as well.

The establishment of this infrastructure institute will solve the problem of mistrust of potential insurees to insurers, problem of provision of financial literacy to the population, increase in demand for insurance services.

Considering the experience of the United States, it was found out that there is an electronic data bank on all insurance companies widely used to distribute the insurers by risk, premium volume, size of the authorized capital, etc. With its help potential insurers may become familiar with information of interest to them at any time.

It should be noted that the availability of the information center should necessarily be, on the one hand, as an indicator of the reliability of insurance companies and ways to combat unscrupulous representatives, on the other, as an incentive to increase public confidence in the insurers, and therefore the demand for insurance services [5].

Figure. Model Kazakhstan insurance market infrastructure

One of the main directions of improving the competitiveness of the national insurance market is the creation of «Motor Insurance Bureau». According to the concept «Implementation of National Motor Insurance Bureau» proposed by Association of financiers of Kazakhstan, the establishment of this infrastructure institute will facilitate:

- coordinated work of the insurance market infrastructure;

- substantial cost savings in the provision of the necessary infrastructure of the insurance market;

- expansion of functions in evaluation of adequacy of tariffs on motor insurance. There is an opportunity to assess the risks of insurance companies by the market concentration and weighted portfolio (antiselection risks) through access to nationwide statistics;

- the absence of public funding for infrastructure development of the insurance market, the transfer of risks lack of funds for provision;

- functioning of insurance infrastructure directly on of the insurance market participants;

- the possibility of mobile integration in international motor insurance system «as a green map» and representation of the interests of the citizens of the Republic of Kazakhstan abroad. Considerable flexibility in matters of integration within the Eurasian Economic Union, reduce the cost of insurance products to consumers of insurance services through cost savings of insurers on service infrastructure’s content and its coordinated activities, as well as due to the provision of decrease of time and financial costs associated with closing of contracts and settlement of losses [6].

To achieve higher penetration of insurance services, it is necessary to develop public partnership of the insurance market and other socially important sectors of the economy, such as, for example, agriculture and construction. This will make it possible to use budget funds directed to the development of industries more efficiently.

The most important direction of development of the insurance market is the adoption of a set of measures to further increase the capitalization of insurance organizations. Capital accumulation will allow local insurers to retain most of the insurance risks currently inefficiently transferred to reinsurance.

It is necessary to take measures aimed at the participation of the state in the work of collecting statistics, creating mortality tables, strengthening the requirements for automating the processes of insurance and other activities. This will allow to form adequate and justified amounts of insurance tariffs by types of insurance and the formation of adequate reserves, taking into account the general statistics on insurance cases and payments. In this connection, it is necessary to further improve the internal processes of information systems of the Single Insurance Database, which allow collecting statistics on all parameters of the insurance contract. In addition, there is a need to interact with insurance databases with government databases, as personal data on individuals are used to enter into property and personal insurance contracts. In this regard, the possibility of providing access to state databases on the registration of individuals with the possibility of obtaining information in real time will be considered.

Thus, the proposed model of the infrastructure of the insurance market of Kazakhstan aims to provide:

- Development of the national market in general, namely to ensure its competitiveness in the face of integrative cooperation;

- Creation of additional investment resources for the economy, through the creation of the National reinsurance organization institute;

- Improvement of the system of national reinsurance;

- Enhancement of social stability and the sustainability of economic

- Development of a specialized infrastructure of the insurance market: underwriters, adzhasters, insurance

- Making proposals for optimizing the supervisory function of the regulator, analytical and information systems, ensuring transparency, completeness and accessibility of statistical data in order to timely identify problems in insurance organizations and systemic risks in the insurance industry as a

References

- Ofitsialnyi sait Natsionalnoho Banka Respubliki Kazakhstan [Official web-site of the National Bank of the Republic of Kazakhstan]. http://www.nationalbank.kz/?switch=rus [in Russian].

- Astakhov, A. (2012). Puteshestvie po kanalam prodazh [Through the sales channel]. Rynok strakhovaniia (Decabr) – Insurance market magazine, 12(99). [in Russian].

- Dyuzhikov, E.F. (2015). K obshchim podkhodam k rehulirovaniiu i edinomu strakhovomu rynku EAES [Towards the common approaches to regulation and the single EEU insurance market]. Finansy – Finance, 9, 37–38 [in Russian].

- Pervaia i samaia vazhnaia zadacha natsionalnoho strakhovoho rynka — povyshenie eho konkurentosposobnosti [The first and most important objective of the national insurance market — enhancement of its competitiveness]. Retrieved from http://allinsurance.kz [in Russian].

- Alekhina, E.S. (2008). Model infrastruktury rehionalnoho strakhovoho rynka [Infrastructure model of the regional insurance market]. Vestnik Iuzhno-Uralskoho hosudarstvennoho universiteta. Seriia Ekonomika i menedzhment – Bulletin of the South Ural State University. Ser. Economics and management, 20(120) [in Russian].

- Sozdanie Natsionalnoho motornoho biuro-novyi shah k povysheniiu konkurentosposobnosti kazakhstanskoho strakhovoho rynka [Establishment of the National Motor Insurance Bureau – a new step to competitiveness enhancementof Kazakhstani insurance market]. Retrieved from http://allinsurance.kz [in Russian].