Article presents a research of methodology of the state audit providing formation of high-quality information on activity of the governments for its subsequent assessment. The governments have few incentives for disclosure of accurate and transparent information. Effective methods of the state audit have to promote increase in the accountability of executive power, transparency of the budgetary processes and, as a result, improvement of an assessment of activity of government. The importance of work is defined to justification of need of involvement of the state audit in an assessment of reliability of the reporting of executive authorities, efficiency of the budgetary procedures, by need of introduction of modern methods of the reporting of state bodies on the basis of the analysis of world practice, the relevant institutional structure of the state audit, to definition of spheres of further improvement of activity of bodies of the state audit. The International practice presented in article regarding theoretical and methodological bases, can be applied with success in the Republic of Kazakhstan in case of its creative transformation, with its obligatory legal and methodological adaptation to conditions of our country. Increase in transparency of the budgetary processes will become the major step to increase in efficiency of activity of public authorities.

As a result of the global financial crisis and the subsequent crisis of a sovereign debt, the government and other organizations of public sector around the world, especially in the countries of OECD, have faced essential pressure because of the limited budget, considerable debts and stagnation in economy. At the same time the economy grows very quickly in the countries of Asia, South America and Africa, showing increase in demand for the public benefits and services, investments into infrastructure.

This context creates a direct call to the governments for increase in effective management of resources and formation of high-quality information for interested parties (citizens and parliament, donors, investors and the financial markets, etc.).

Though the state account in itself doesn't lead to high-quality management of public finances, it is a necessary component. The advanced account leads to the best reporting which contains information necessary for adoption of more reasonable decisions that in turn has to lead to more effective use of the state resources.

The auditor company «PriceWaterhouseCuppers» has conducted a research among 100 countries about the current situation and the expected tendencies concerning the state account. According to these data, practice of the state account differs in a variety around the world. The cash method is the main method used in public sector for many years [1].

Auditors play an important role in ensuring the quality of financial information of public sector. Besides that auditor reports increase trust to financial statements, strengthen the accountability and transparency of the government, recommendations of auditors stimulate public authorities on continuous improvement of quality of financial statements.

Experiment of Australia on implementation of audit of financial statements of the government is of special interest as transition of system of accounting to a charge method in the Republic of Kazakhstan was carried out taking into account practice of this country.

According to the requirements of paragraph 55 of the Law on financial management and the accountability of 1997, the consolidated financial statements of the Government of Australia (further – CFS) are formed by the Minister of Finance and are represented within 5 months after the termination of financial year [2].

CFS join nation-wide reports and reports on the main public sector (further – MPS). CFS includes the following reports:

- the financial statement of the Government of Australia (the nation-wide report) which includes:

- report on results of operating activities of the Government of Australia;

- balance sheet of the Government of Australia;

- report on cash flow of the Government of Australia;

- report of the Government of Australia on changes in assets / net capital;

- explanatory notes to financial statements, including the statement for the basic principles of accounting

- the financial statement on MPS of Australia which includes:

- the report on results of operating activities of the Government of Australia on sectors, including the financial statement on MPS;

- the balance sheet of the Government of Australia by sectors, including MPS;

- the report on cash flow on sectors, including MPS;

- the report of the Government of Australia on changes in assets / net capital, including MPS;

- explanatory notes to financial statements, including the statement for the basic principles of accounting statement of the Minister of Finance for compliance to requirements:

- «that financial statements:

- are prepared according to the Law on financial management and the accountability of 1997 and applicable standards of accounting of Australia;

- authentically reflect the financial position of the government as of June 30 of 20xx year and results of operating activities and cash flow of the government of Australia in a year …» [3].

Examples of the above-named reports are given below, in Tables 1-3.

T a b l e 1

Sample of the Report on results of operating activities of the Government of Australia, doll.

|

Report on results of operating activities of the Government of Australia for the period, ended June 30, 2011 |

Remark |

2011 y. |

2010 y. |

|

Operating profit |

|

$m |

$m |

|

Tax revenue profit |

2 |

288,838 |

267,962 |

|

Marketing of goods and services profit |

3 |

19,098 |

18,399 |

|

Interest income |

4 |

6,792 |

5,945 |

|

Dividend yield |

4 |

2,031 |

1,492 |

|

Others |

5 |

5,530 |

5,099 |

|

Total profit: |

|

322,289 |

298,897 |

T a b l e 2

Sample of the Report on results of operating activities of the Government of Australia by sectors, including the financial statement on MPS

|

|

MPS |

Public nonfinancial corporations |

Public financial corporations |

Exception and set-off of operations |

Government of Australia |

|||||

|

Remark |

2011 y. |

2010 y. |

2011 y. |

2010 y. |

2011 y. |

2010 y. |

2011 y. |

2010 y. |

2011 y. |

2010 y. |

|

Profit |

|

|

|

|

|

|

|

|

|

|

|

Tax revenue2 |

289,004 |

Х |

- |

Х |

- |

Х |

(166) |

Х |

288,838 |

Х |

|

Marketing of goods and services3 |

7,680 |

Х |

7,354 |

Х |

5,237 |

Х |

(1173) |

Х |

19,098 |

Х |

|

Interest4 |

5,169 |

Х |

100 |

Х |

2,173 |

Х |

(650) |

Х |

6,792 |

Х |

|

Dividend4 |

2,562 |

Х |

- |

Х |

64 |

Х |

(595) |

Х |

2,031 |

Х |

|

Others5 |

5,473 |

Х |

108 |

Х |

154 |

Х |

(205) |

Х |

5,530 |

Х |

|

Total profit |

309,888 |

хх |

7,562 |

хх |

7,628 |

хх |

(2,789) |

хх |

322,289 |

хх |

T a b l e 3

Model of Interpretation of the article of the Report on results of operating activities of the Government of Australia by sectors, including the financial statement on MPS

|

Remark 3: Marketing of goods and services |

MPS |

Government of Australia |

||

|

|

2011 |

2010 |

2011 |

2010 |

|

|

$м |

$м |

$м |

$м |

|

Marketing of goods |

1,125 |

1,201 |

6,565 |

6,200 |

|

Service rendering |

4,234 |

4,276 |

10,172 |

10,040 |

|

Operating leasing |

51 |

31 |

91 |

69 |

|

Other collections from rendering of regulatory services |

2,270 |

2,090 |

2,270 |

2,090 |

|

Total profit from Marketing of goods and services |

7,680 |

7,598 |

19,098 |

18,339 |

Depending on the subjects, included in the consolidated financial statements, the Australian national office of audit (further – ANAO) prepares up to 259 auditor reports, including nation-wide consolidated. The checked subjects are a part either MPS, or sectors of the state finance corporations, or sector of the public non-financial corporations and include the state departments, departments, the state companies and the state trade enterprises.

The specified departments submit the financial statement to the auditor till September 30, audit comes to the end till October 31. At the same time about 60 % of audit reports are issued in the same day in which ANAO receives the approved financial statements (90 % – within 2 days).

The consolidated financial statements are submitted to the auditor till November 30. The auditor report on CFS is submitted in December of the same year.

In 2010-2011 ANAO has to carry out 258 audits. For this purpose subjects of audit were classified by portfolios. 19 portfolios are selected. For example:

- agricultural, fish and timber industry enterprises;

- broadband frequencies, communications and digital economy;

- defense;

In addition to these checked subjects, there are 12 subjects on which the Government of Australia has no significant effect. The cost of the general net assets of such subjects is shown as investment (for example, the Australian national university).

The review on branch portfolios is provided in Table 4.

T a b l e 4

Sample of the Review on sector of broadband communication, communications and digital economy

|

Reporting subject |

Essential subject |

Auditors report |

Date of signing the financial statement |

Date of issue of auditors report |

Disclosed incompliance |

|

1 |

2 |

3 |

4 |

5 |

6 |

|

Ministry of broadband communication, communications and digital economy |

Yes |

√ |

30.08.2011 |

30.08.2011 |

- |

|

Television and radio broadcasting of Australia |

Yes |

√ |

28.07.2011 |

28.07.2011 |

- |

|

1 |

2 |

3 |

4 |

5 |

6 |

|

Communication and mass media Department of Australia |

Yes |

√ А* |

14.09.2011 |

14.09.2011 |

- |

|

Post corporation of Australia |

Yes |

√ |

25.08.2011 |

25.08.2011 |

♦ |

|

National DAB License Company Limited |

No |

√ |

05.08.2011 |

05.08.2011 |

- |

Note. Private audit.

Process of financial audit of ANAO carries out in 2 steps – intermediate and final.

The intermediate stage is devoted to an assessment of internal control systems of key departments, including mechanisms of management, information systems and procedures of control in 27 departments of which about 95 % of the income and expenses of MPS are the share.

The report on results of intermediate audit is called «The intermediate stage of audit of financial statements of the largest departments which are a part of MPS for the period which is coming to an end on June 30, 20xx year» (about 230 p.) and it is represented in Parliament and to responsible ministers.

The opinion is expressed in the report that systems, the elements of management and processes existing in large Australian departments of the government work in such a way that allow them to prepare financial statements which give a reliable and objective idea of the financial performance and financial position on ending date of financial year.

At this stage such violations as control system shortcomings in a number of areas, in particular concerning management of personnel can be revealed; processes of management of assets; management of exclusive access to key financial systems and management of IT safety.

At a final stage of audit which is applied to all persons, ANAO finishes its assessment of efficiency of key control devices for all year, check on the substance of significant account balances and the disclosed information which is contained in financial statements and generalizes results by the audit report about financial statements of the subject.

For example, the general questions defined in the final stage of audit in 2011-2012 were in the relation: information technologies in the management, such as access for users and division of duties; processes of management of assets, including the accounting of objects of incomplete construction, management of assets with shares holders, integrity of registers of assets and management of system of processing.

The final report under the name «The Audit of Financial Statements of Subjects of Public Sector of Australia Which, ending on June 30, 20xx year» (about 270 p.) is submitted in Parliament in December. The audit report is attached to the report (on 2 p.).

Indicator of good financial management at the subject is:

- timely approval of financial statements;

- unconditional positive audit report [2].

It should be noted that most of auditors of ANAO are professional accountants, and transition to the account by a method of charge hasn't demanded from them the retraining and professional development. Moreover, the General auditor of Australia is a member of Institute of the certificated accountants and the Australian society of the certified public accountants, and also the vice-chairman of Council for standards of accounting of Australia.

For ensuring the high-quality carrying out audit, foreign auditor offices develop methodologies for carrying out annual financial audit.

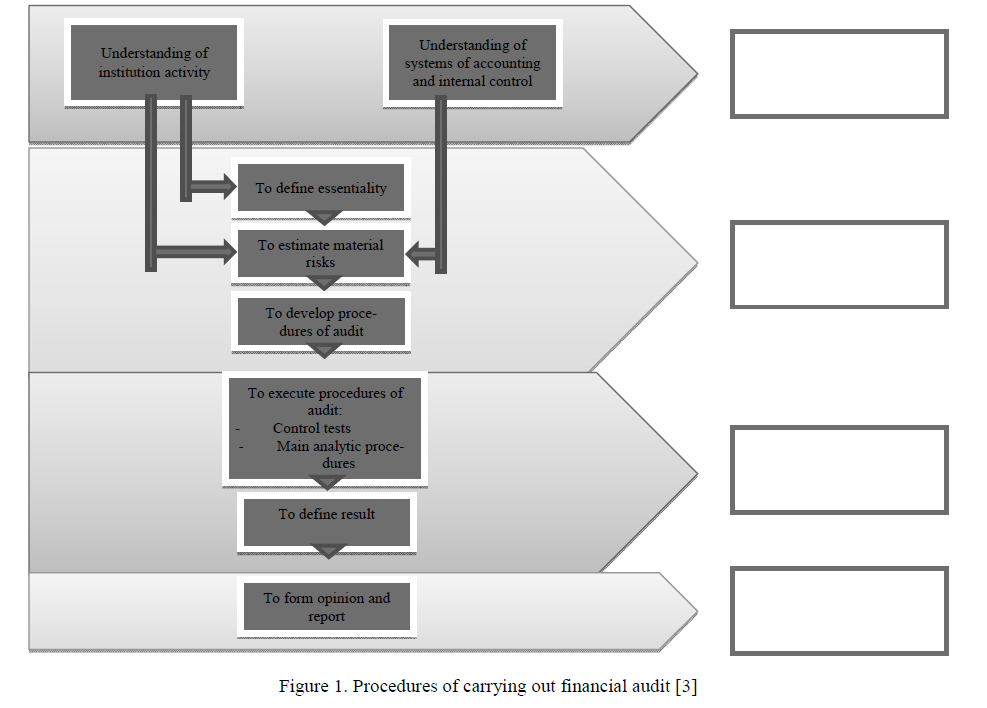

For example, at Office of the General auditor of Canada (further – OAG) the methodology under the name «Guide to Carrying Out Annual Audit» consists of 171 pages.

The guide contains an explanation of procedures of carrying out financial audit of OAG, which are schematically submitted in the Figure 1.

Figure 1. Procedures of carrying out financial audit [3]

It should be noted that OAG carries out the annual audit inspections for decades, and the personnel involved in conducting such checks consist of the qualified accountants or students who are going to become professional accountants, therefore, all of them are very well familiar with accounting by a charge method, standards of accounting and audit.

Special interest regarding development of the methodical management and transition to financial audit represents the experience of the Republic of Turkey.

In the country during the long period more attention was paid on check of where budgetary funds have been spent and at the same time paid not enough attention to financial statements. The court of Accounts of the Republic of Turkey within 145 years carried out the audit on compliance and, only in the last 5 of them, the emphasis is placed on financial audit to which now all subjects involved in execution of the State Budget annually are exposed.

Transition to financial audit has begun since 2005 with the joint project with National control administration of Great Britain which has also given practical help in carrying out the educational program for transition of Court of Accounts to financial audit.

Bases and principles of carrying out the financial audit have been developed by Court of Accounts in «The guide to the regulatory (ordered) audit».

From 2005 to 2007 the pilot projects of carrying out the financial audit are executed. After that the Management assessment is carried out by results of which its adjustment is executed.

Then the Court of Accounts has started the 2nd pilot project – practical works in which a large number of auditors and the audited subjects has been involved.

2008–2009 years have been devoted to preparation of the training material «The Guide to the Regulatory (Ordered) Audit» and training of auditors.

After that the work on evaluating and analysis of the Guide, and definition was coming – whether new adjustments are required.

After all this the Guide has been submitted for consideration of General council and approved by it.

For implementation of financial audit the computer support and certain professional programmers were necessary together with whom the program support of financial audit was developed.

In 2010 the process on transition to financial audit has been complete.

In May, 2012 the Court of Accounts has carried out practical work on improvement of the Guide. 180 auditors and heads of divisions under the general leaders of the Center of development and training of Court of Accounts of the Republic of Turkey (DEGEM) [4] took part in practical work.

Especially it should be noted problematic issues of Court of Accounts of the Republic of Turkey upon transition to financial audit.

In Court of Accounts there was a traditional auditor culture of carrying out audit having a 145-year experience, and in this regard the transition to a new type of audit was very difficult. Among auditors there were people who didn't trust in new type of audit and trusted more in audit on compliance at which it was necessary to carry out audit of all procedures. At financial audit check on a selective basis becomes and such method wasn't acceptable by older auditors. They didn't study new standards, and the new method of carrying out audit wasn't clear to them. Only after carrying out the educational program, their belief have begun to change, then, as there were no problems with young specialists.

Financial audit is a command type of audit, i.e. it is necessary to collect the team consisting not less of 3 people. Transition from individual audit to group work was difficult too. Therefore the principles and rules of work in team have been developed.

The audited subjects (public institutions, bodies, subjects of quasi-public sector) also have been forced to get used to new methods of work of Court of Accounts. In connection with what the problem of SAI was to acquaint the audited subjects with new requirements and to carry out explanatory work with them. The number of requests for many documents has increased.

Carrying out financial audit requires knowledge of accounting. In this regard at employment in Court of Accounts existence of the diploma about accounting education – is obligatory. Who had no such education, for example, earlier accepted workers, have completed a course. Also the Center of development and training began to train auditors haw to estimate work of system of internal control and information systems. Auditors have to be able to use software products on accounting and financial audit [4].

Experience of Estonia is demonstrative example of support of quality of carrying out audit.

The summary annual reporting of Estonia is formed according to the International standards of accounting and consists from:

- the state reporting and the summary reporting of the state (including the companies, funds belonging to the state);

- data on local self-government institutions;

- data on public and sector

The data necessary for compilation of the summary reporting are in one database. Each accountable organization shall enter quarterly its test balance into the database [5].

According to the Law on the state budget, the State control of Estonia (further – SC) shall carry out audit of the summary annual report of the state. In this case the SC shall make the auditor report which is submitted in Parliament together with the summary annual report of the state. The auditor report shall contain the conclusion on reliability of the summary report and validity of operations.

Support of quality in the course of carrying out audit is reached at the expense of:

- professional competence (in the field of accounting, audit, management of projects, );

- domestic policy in writing (guides), samples of documents and the software for

At the end of stages of planning and writing of reports the auditor team has an opportunity to form the group consisting of audit managers who carry out the analysis of the plan or the report as third-party experts.

Certification of auditors is considered as plan activities for improving of quality of audit of SC (the minimum requirement to the manager on audit and director at the levels of departments) [5].

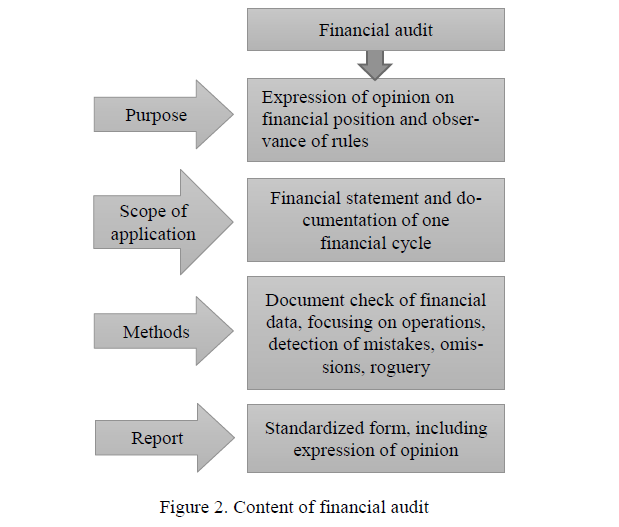

Generalizing the international experience, it is possible to mark that financial audit has the features which are schematically provided in the Figure 2:

Figure 2. Content of financial audit

SAI attaches equal significance to financial audits and audits of efficiency. For improvement of audit of reports of public sector and bodies of the state financial control have to increase significantly the competence in financial audit. In the majority of the countries the reforming of system of accounting according to the international standards has defined need of development of training and professional development of experts in the field of accounting, audit and financial statements, studying of information systems and methods of detection of sources of roguery or inefficient processes.

The governments bear moral responsibility before the citizens for transparency in the handling of taxpayers money [6]. Budgets of the governments represent financial plans which define how the state resources will be used for achievement of political objectives (The Organization for Economic Cooperation and Development [7]. The budget plays the central role in life of each citizen. The citizens especially poor and needy, are the main beneficiaries of the state programs financed by the budget. Therefore it is very important that citizens understand the state budgets and have access to information which will allow them to bring to responsibility of government for use of public funds. The principle of rule of law and the theory of the agencies define ways of transparency of the governments [8]. On the one hand, rule of law considers compulsory publicity and transparent management of cornerstones of public administration. On the other hand, the theory of the agencies affirm that the principal (citizen) and the agent (politician) can't pursue identical preferences as characters have own interests which not always maximize welfare of citizens. Thus, citizens have to distribute information as a way to weaken asymmetry of information and to allow the first to control activity of characters [9]. Premchand defines transparency of the budget as general availability of information on procedures and transactions of decision-making by the governments [10]. Kopits and Craig add that this information has to be reliable, comprehensive, timely, clear and internationally comparable [11]. Besides, Blondal considered that the budgetary transparency has three basic elements: (a) release of the budgetary data (systematic and timely publication of all relevant fiscal information); (b) effective role of legislature (careful analysis and independent analysis of the budgetary reports, discussion and influence on the budgetary policy, and also accountability of the government); and c) an effective role of civil society through the mass media and non-governmental organizations (influencing the budgetary policy, bringing to responsibility of government) [12]. As for a role of legislature and its influence on civil society, legislators have large powers on use of the resources that in certain cases brings benefit to their own voters and/or participants of a campaign. However the supervising role is the public benefit in legislature that brings benefit to all population [13]. Actually, transparency of the budget depends on that role which is played by legislature concerning the budgetary supervision [14].

Today in Kazakhstan unprecedented attempts on ensuring publicity of the budgetary processes are carried out. Within the Electronic Government project the platform for placement of the budgetary plans by public authorities is created. It is planned to carry out work of a platform in 2017 in the test mode and by 2018 will be provided the full start of all opportunities. By the Decree of the President since January 1, 2017 the Calculating committee on control of performance of the republican budget will carry out preliminary estimate of the draft of the republican budget that in fact is strengthening of legislative budgetary supervision and expansion of functions of the state audit. Earlier state financial control executed only verifications of the budget by a post factum.

According to the [15] budgetary process it is subdivided into four stages: drawing up, approval, execution, audit and assessment. The role of legislature at each stage differs from the country to the country. In Kazakhstan as a part of Parliament the Committee on finance and budget within which scope of interests fall including questions of the state budget functions. The legislature is focused on preliminary process of acceptance and the adoption of Laws on the budget. However in Parliament there is no special committee for consideration of results of the state audit. This kind of activity is necessary for increase in efficiency of public administration. As the state audit, in essence, is engaged in consulting activity, that is informs the authority on quality of work of government. Further decision-making has to be based on qualitative information of institute of the state audit. Only such form of government can be effective.

Thus, transition to the state audit means consolidation of information concerning activity not only public authorities, but also subjects of quasi-public sector, and also other assets of the state. Work on audit and assessment of financial statements of public sector has to become the most important step of improvement of activity of the state audit in Kazakhstan. Further on an annual basis the consolidated financial statements have to be submitted to "principal" at the time of the conclusion presentation to the budget of the country. As shown above, it is the best practices of foreign countries. Fundamentals of methodology of carrying out consolidation can be taken from the private sector and adapted to state. It should be noted that this practice with success is applied in corporate management.

Today imperfection of methodology of an assessment of the state assets results in unauthenticity of estimates. Already recognized poor control of quasi-public sector is explained by it. That is the existing account doesn't allow to estimate fairly both assets, and obligations. On the one hand the quasi sector has passed to the international standards of the reporting long ago and is object of obligatory external audit according to the Law RK "About Auditor Activity". Data of reports are annually collected in Depositary of financial statements. On the other hand, the state account isn't able to estimate the number of such subjects, share in the market, the cost of this "portfolio", and following from here insufficient transparency, inefficiency and a number of problems today. Making decision on privatization is much caused to simmering of the matters. Today it is necessary to clear the state assets from non-core, to range them on "portfolios", to develop methodology of the state audit of financial statements, consolidation. Such information will provide adoption of effective solutions of public administration.

References

- «Na puti k novoi ere v hosudarstvennom uchete i otchetnosti» Hlobalnyi obzor PwC po bukhhalterskomu uchetu i otchetnosti tsentralnykh pravitelstv (Aprel 2013 hoda) [«On the way to a new era in the state account and the reporting» The global review of PwC on accounting and the reporting of the central governments]. pwc.com Retrieved from http://www.pwc.com/gx/en/psrc/united-kingdom/assets/pwc-leading-from-the-front-full-report.pdf [in Russian].

- anao.gov.au Retrieved from https://www.anao.gov.au/pubs/major-projects-report [in Russian].

- «Rol i znachenie MSFOOS v priniatii upravlencheskikh reshenii»: materialy seminara Ministerstvo finansov RK pri podderzhke proekta USAID v sfere makroekonomiki (MER) (Oktiabr 2013 hoda) [«Role and IPSAS Value in Adoption of Administrative Decisions»: seminar materials the Ministry of Finance of RK with assistance of the USAID project in the sphere of macroeconomic (MEP)]. kz Retrieved from https://uchet.kz/news/ministerstvo-finansov-respubliki-kazakhstan-provodit-regionalnyyseminar-rol-i-znachenie-msfoos-v-pr/ [in Russian].

- Bil Burnett, spetsialist po auditu v obshchestvennoi sfere i parlamentskomu kon-troliu [Bill Burnett, expert in audit in the public sphere and parliamentary control]. Proceedings from Materialy seminara MSFOOS – IPSAS seminar materials. (2012, 3-7 December). [in Russian].

- Budgeting in Estonia. Public Governance and Territorial Development Directorate Public Governance Committee. Working Party of Senior Budget Officials GOV/PGC/SBO (2008). 3. 31-Mar-2008.

- Transparency and participation in the budget process. Cape Town, South Arica: Idasa. Fölscher, A., Krafchik, W., & Shapiro, I. (2000).

- OECD budget practices and procedures database phase II: Final glossary. Paris, France: Author. Organisation for Economic Cooperation and Development. (2006).

- In P. B. Clarke & J. Foweraker (Eds.). (2001). Encyclopaedia of democratic thought (pp. 700-705). London, England: Routledge. Hood, C.

- Zimmerman, J.L. (1977). The municipal accounting maze: An analysis of political incentives. Journal of Accounting Research, 15(Suppl.).

- Premchand, (1993). Public expenditure management. Washington, DC: International Monetary Fund.

- Kopits, G., & Craig, J. (1998, February). Transparency in government operations (IMF Occasional Paper No. 158). Washington, DC: International Monetary

- Blöndal, R. (2003). Budget reform in OECD member countries: Common trends. OECD Journal on Budgeting, 2, 7–26.

- Benito, B., & Bastida, F. (2009). Budget transparency, fiscal performance, and political turnout: An international approach. Public Administration Review, 69, 403–416.

- Santiso, C. (2005). Budget institutions and fiscal responsibility: Parliaments and the political economy of the budget process (Working Paper No. 37253). Washington, DC: World Bank

- Lee, D., & Johnson, R.W. (1998). Public budgeting systems. Gaithersburg, MD: Aspen.