The article examines the role of the pension sector in the country's economy, its role in shaping the country's economic security. This part also analyzes the investment directions of pension savings of the Russian Federation and pension resources of the Republic of Kazakhstan for the period under study. The study showed that the following points underlie the identified problem moments of investment activity in the portfolio of the Unified Accumulative Pension Fund (hereinafter – UAPF) as a single operator of the pension system: in general, an inefficient and conservative low yield of the structure of investment portfolios is ob- served, as well as lack of quality investment instruments. The largest part of pension assets is directed to finance the deficit of the state budget of the country, thereby pension savings of citizens are exposed to general economic risks. In order to solve the above problems, the article proposes to apply more actively the progressive world experience in the transition to the active investment strategy of the UAPF. The article proposes measures to increase the activation of the infrastructure direction in the investment activity of the Unified Accumulative Pension Fund of the Republic of Kazakhstan, and also make changes in the Investment declaration of the UAPF, to expand the use of pension assets in the financing of infrastructure projects to increase investment income of the UAPF portfolio with the subsequent transition to an active investment strategy. A list of measures is also proposed, the implementation of which would create conditions for the activation of the AUPF in this direction.

In modern conditions, when the state of the country's economic development is exposed to various risks, the issues of effective use of pension savings of citizens of the country, not only from the point of view of profitability, but also from the standpoint of their safety, transparency and security acquire very important socio-economic significance. In this connection, modernization processes, ways of further improvement of the pension systems of Kazakhstan and the Russian Federation are underway.

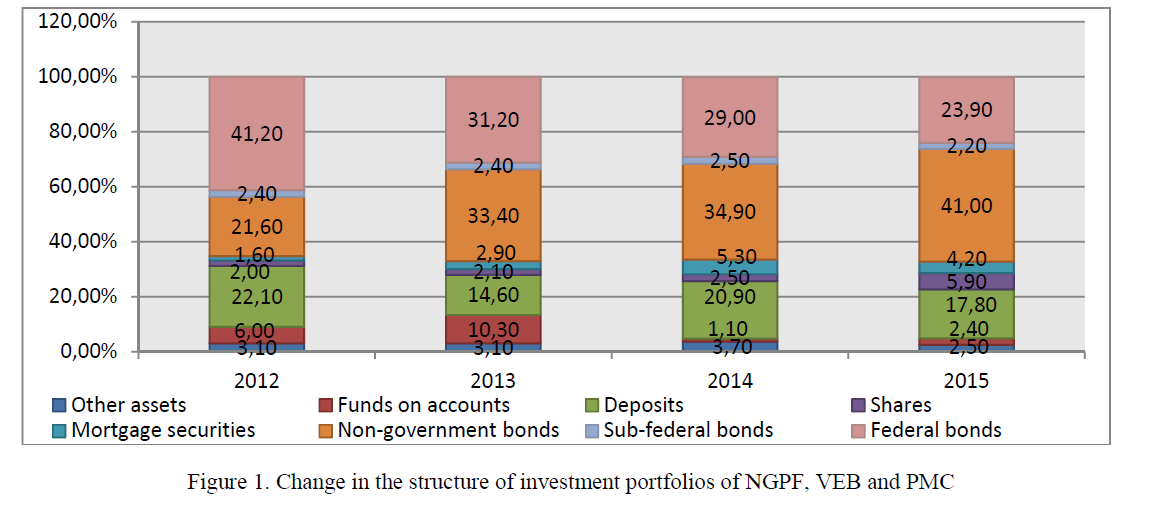

In Russia, pension savings over recent years have truly become one of the key elements of support of the Russian stock market, despite the «freeze» of new contributions to a funded pension and other restrictions. This is especially evident in the bond market, where the long-term and conservative nature of investing of pension funds plays its role. The change in the structure of investment portfolios of NGPF, VEB and PMC for the period under study is presented below (Fig. 1).

Figure 1. Change in the structure of investment portfolios of NGPF, VEB and PMC

But, despite the overall stability of the share of bonds, the structure of this segment changes significantly every year towards decreasing of state (primarily federal) and increasing of non-government bonds. E.g., at the end of 2012 the federal loan bonds (hereinafter - OFZ) were 41.2 %, and non-government bonds – 21.6 % in the structure of the aggregate investment portfolio, whereas with the end of 2015 the situation changed to the opposite. This is largely due to the limited growth of the federal bond market. In particular, according to the National Association of Stock Market Participants (NAUFOR), in 2015 the OFZ market, although grew in nominal terms by 18.8 % (up to 5.6 trillion rubles) – 9.2 % of GDP, but showed Reduction in the part of the exchange turnover. The secondary market (at actual cost, without REPO transactions and placements) fell by 6.7 % down to 3.6 trillion rubles. Thus, NGPFs, VEBs and PMCs together hold up to 15 % of all federal bonds (0.9 trillion rubles).

The bond market of the constituent entities of the Russian Federation since the times of the financial and economic crisis of 2008-2009 has been in an unstable state. According to NAUFOR, the share of subfederal bonds in the structure of the ruble bond market of Russia since the end of 2005 has declined from almost 11 % to 4 % in ten years. Recently, as the budget situation worsens, regions often prefer relatively cheap budgetary loans to more expensive borrowings in the public market. As a result, at the end of 2016, according to NAUFOR, the volume of the subfederal market of government bonds amounted to 576 billion rubles. However, despite this, investments from pension savings are still very significant and account for about 15 % of all bonds of the constituent entities of the Russian Federation.

On the one hand, the corporate bond market, estimated at 8.1 billion rubles, remains the main supplier of instruments for investing in pension savings. On the other hand, pension funds become the key domestic holder of Russian non-government bonds. By the end of 2015 pension investors acquired about 20 % of cor- porate bonds for almost 1.6 billion rubles of pension savings.

Another two main classes of fixed-income assets are various types of mortgage securities, including mortgage participation certificates (hereinafter – MPCs) and deposits. The volume of investments in mortgage securities exceeded the 2 % threshold in the total investment portfolio of pension investors in 2012 and reached 4 % by the end of 2015. In the horizon of 2-3 years, we see no reason for a significant increase in the share of mortgage securities due to the regulatory pressure on this instrument by the Bank of Russia. Most likely, the value of the MPC for portfolios of NGPFs and MC will fall, and the demand of pension investors for investing in real estate will be increasingly met through closed-end unit real estate funds.

Investments in deposits also have negative dynamics: negative 3.1 percentage points down to 17.8 %for the year. On the one hand, in 2015 it was possible to earn more on the same bond market, where, for example, the yield of OFZ in the first quarter of the previous year was 15-17 %, while the weighted average interest rate on ruble deposits of non-financial organizations for a period of more than 1 year, according to the Bank of Russia, in January 2015was 13.6 % per annum. On the other hand, the Bank of Russia introduced a number of new restrictions on investment of pension savings. In particular, the limits on investing in deposits of credit institutions with a maturity of more than 3 months have been reduced. Their maximum share since 2015 has been set at 60 %, and since early 2016, even lower - at 40 %. In addition, at the beginning of last year the Bank of Russia introduced additional restrictions on investing in related parties. The new rules were also established with respect to the placement of pension savings in the settlement accounts of banks that are members of related financial holdings.

Thus, pension funds faced significant restrictions, among which:

- Investing in conditions of a limited volume of the bond market (in addition to insufficient market growth, the deficit of securities admitted to investment continues to be a constraining factor);

- weakening of the ruble due to the fall in currency prices for energy;

- jumps in interest rates (falls in January, in August-September and December 2015);

- decrease in investment ratings, including governmental ones;

- reduction of profitability due to the lowering of the key rate of the Bank of Russia and the preservation of demand for ruble-denominated bonds. Solving these problems, as well as expanding the market for debt securities protected from inflation, may encourage pension investors to increase the share of bonds in their portfolios in the future [1].

As is known, the newly created Unified Accumulative Pension Fund of Kazakhstan is the only player in the pension services market and it is this entity which has the entire volume of pension assets in the country. The Unified Accumulative Pension Fund is currently the largest domestic institutional investor. As a result of the merger of the pension assets of all the country's accumulative pension funds, the huge amount of financial resources, in the scale of national economy, was concentrated in it. The main objective in creating aunified accumulative pension fund was to ensure a higher efficiency of operations, transparency and reliability, as well as certain guarantees from the state for the safety of deposits. The UAPF's assets are of great investment importance for the economic development of Kazakhstan, as they are an important component of domestic investment resources [2].

According to the National Bank of the Republic of Kazakhstan (hereinafter – NB RK), which in ac- cordance with the Law of the Republic of Kazakhstan «On pension provision in the Republic of Kazakhstan» is also the only organization managing pension assets (hereinafter – PA), UAPF, as of 01.01.2017, had 9.82 million individual pension accounts of depositors, pension savings of citizens concentrated in the UAPF amounted to KZT 6,685.3 billion, which increased by KZT 2,167.5 billion during the period under review. The table below shows the main information about the amount of pension savings in dynamics for three years 2014-2016. (Table 1).

Dynamics of pension assets of JSC «UAPF»

T a b l e 1

Billions KZT

|

Indicators |

2014 y. |

2015 y. |

2016 y. |

Growth (in %) |

|

Pension savings |

4 517,8 |

5 828,2 |

6 685,3 |

47,9 |

|

Pension contributions |

3 686,3 |

4 375,2 |

4 927,1 |

33,6 |

|

Pension payments |

529,6 |

670,7 |

840,4 |

58,6 |

|

«Net» investment income |

990,5 |

1 751,9 |

2 224,3 |

124,5 |

|

Share of «net» investment income in the amount of pension savings |

21,9 % |

30,1 % |

33,3 % |

52,05 |

Note. Сompiled by the authors based on data from the National Bank of the Republic of Kazakhstan for a number of years.

Retirement savings at the end of 2015 and 2016 show an increase over previous periods: by 29 % and 15 %, respectively. This growth is primarily due to the regular pension contributions of depositors, but also, to a lesser extent, the investment activity of the Fund. In this regard, it is necessary to note the dynamics of the «net» investment income in pension savings, which by comparison with 2014, increased by KZT1,233.8 billion, by 2016 amounted to KZT2,224.3 billion, where its share in the amount of pension Savings increased by 11.4 % [3].

Thus, the issues of effective use of these resources are of great importance, both for the purpose of solving social problems related to preserving and increasing the savings of depositors of pension funds, and for the purpose of ensuring economic growth in the country. In this connection, it is necessary to know that the funds of the UAPF are the money of citizens. And they must work, earn income to the owners of accounts. The income for assets is formed by investing in various instruments, including securities. The goals of investing the UAPF pension assets are to ensure the safety of pension savings of depositors and to receive investment income. The strategy of investing the pension assets of the EPPF is aimed at obtaining real profitability in the long term, by ensuring an increase in investments at a risk level that will ensure the safety of the value of the UAPF pension assets with a high probability, due to the optimal combination of various types of financial instruments. The investment of the UAPF pension assets is carried out in accordance with the list of financial instruments permitted for purchase from pension assets approved by the Government of the Republic of Kazakhstan and investment limits in accordance with the Investment Declaration of the single funded pension fund (hereinafter - the Declaration).

Profitability of the pension assets of the UAPF, distributed to depositors' accounts in 2016 as compared to the yield of 2014, having increased by 1.64 %, amounted to 7.95 %. In the structure of the investment portfolio of the UAPF, almost half of the investments are in government securities of the Republic of Kazakhstan (hereinafter – GS of the RK), and this ratio persists for the last three periods: 2014 - 2016. Their volume for the analyzed period increased by KZT 943.5 billion and amounted to KZT 2,910.8 billion.

It is also noteworthy that almost 40 % of the investment portfolio of the UAPF falls on securities of quasi-public companies and second-tier banks (hereinafter – STB). And if you take into account that about 6 % of investments are deposits in deposit accounts in commercial banks, the total amount of funds placed by the UAPF in STB allows you to talk about the Fund as one of the key sources of funding STB (more than 8 % of total liabilities of the banking Sector of the Republic of Kazakhstan).

In turn, the volume of investments in securities of foreign issuers for 2016 amounted to KZT 639.5 billion (including non-government securities of foreign issuers, securities of international financial organizations (hereinafter – IFO securities) and government securities of foreign issuers) Or 9.6 % of the volume of pension assets. Consequently, for the period under study the growth was 331.4 billion tenge. The detailed structure of the investment portfolio is presented in Table 2.

T a b l e 2

Dynamics of changes in the AUPF’s total investment portfolio

|

Financial instruments |

2014 y. |

2015 y. |

2016 y. |

|||||

|

Sum, billions KZT |

Share (in %) |

Sum, billions KZT |

Share (in %) |

Sum, billions KZT |

Share (in %) |

|||

|

GS of the Republic of Kazakh- stan, including: |

1 967,3 |

45,3 |

2 683,17 |

46,7 |

2 910,8 |

43,5 |

||

|

securities Finance |

of |

the Ministry of |

1 961,8 |

42,1 |

2 328,23 |

40,6 |

2 681,3 |

40,1 |

|

notes of the National Bank of the Republic of Kazakhstan |

0,0 |

0,0 |

354,94 |

6,1 |

229,5 |

3,4 |

||

|

securities bodies |

of |

local executive |

5,5 |

0,1 |

0,0 |

0,0 |

0,0 |

0,0 |

|

Non-government securities of foreign issuers |

151,3 |

3,5 |

232,8 |

4,1 |

187,9 |

2,8 |

||

|

shares |

9,0 |

0,2 |

13,6 |

0,3 |

18,3 |

0,3 |

||

|

bonds |

142,3 |

3,3 |

219,2 |

3,8 |

169,6 |

2,5 |

||

|

IFO securities |

82,5 |

1,9 |

84,9 |

1,5 |

86,6 |

1,3 |

||

|

GS of foreign issuers |

74,3 |

1,7 |

50,7 |

0,9 |

365,0 |

5,5 |

||

|

Affined gold |

0,0 |

0,0 |

0,0 |

0,0 |

0,0 |

0,0 |

||

|

Non-government securities of the Republic of Kazakhstan issuers including: |

1 364,9 |

31,4 |

2 325,6 |

40,5 |

2 561,8 |

38,3 |

||

|

Shares |

145,5 |

3,3 |

113,1 |

2,0 |

127,5 |

1,9 |

||

|

obligations, including: |

1 219,4 |

28,1 |

2 199,9 |

38,3 |

2 428,2 |

36,3 |

||

|

Nominated in foreign currency |

271,9 |

6,3 |

549,3 |

9,6 |

469,1 |

7,0 |

||

|

Nominated in KZT |

947,6 |

21,8 |

1 650,6 |

28,8 |

1 959,1 |

29,3 |

||

|

Notes |

- |

- |

12,6 |

0,2 |

6,1 |

0,1 |

||

|

Deposits in second-tier banks |

710,2 |

16,3 |

363,9 |

6,3 |

399,9 |

6,0 |

||

|

Derivative financial instruments |

-4,5 |

-0,1 |

0,0 |

0,0 |

0,0 |

0,0 |

||

|

Cash and other assets |

173,53 |

3,84 |

93,5 |

1,6 |

177,5 |

2,7 |

||

|

Total |

4 346,0 |

100,0 |

5 834,57 |

100,0 |

6 689,5 |

100,0 |

||

Note. Compiled by the authors based on data from the National Bank of the Republic of Kazakhstan for a number of years [4].

Thus, the reason for maintaining a low level of profitability of the investment portfolio of JSC «AUPF» is, in our opinion:

- the policy of the National Bank of the Republic of Kazakhstan as the managing organization of the PA AUPF to invest assets in government securities to maintain the coefficients determined with the list of financial instruments permitted for purchase from pension assets approved by the Government of the Republic of Kazakhstan and investment limits in accordance with the Declaration approved by the Board resolution The NB RK of March 17, 2016 No. 86;

- also in low-yield government securities, which are simply a source of financing the country's budget deficit;

- Ineffective structure of the investment portfolio and passive moderately conservative investment strategy, which continues to be used by the NB RK as a management company;

- lack of quality investment

According to the assessment, if the main goal of the AUPF is to multiply the contributions of its partici- pants, rather than ensure financing of Kazakhstan's public debt, the structure of the portfolio of the AUPF, can be considered excessively directed to the benefit of Kazakhstan issuers. In order to solve these problems, the article proposes to apply more actively the progressive world experience when moving to the active in- vestment strategy of the AUPF.

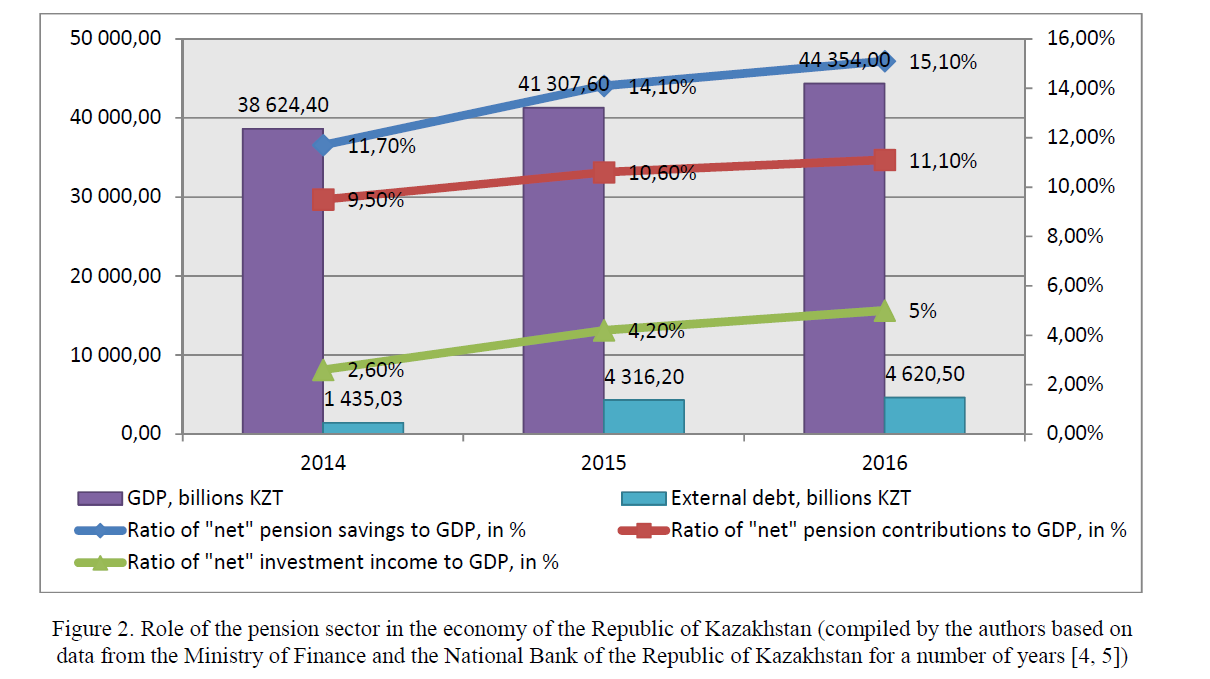

Thus, the issues of improving the investment activity of the AUPF and finding ways to effectively invest pension assets, taking into account the amounts of the amounts accumulated in the AUPF, acquire a strategic character for the state and determine the role of the pension sector in the economy of the country (Fig. 2)

Figure 2. Role of the pension sector in the economy of the Republic of Kazakhstan (compiled by the authors based on data from the Ministry of Finance and the National Bank of the Republic of Kazakhstan for a number of years [4, 5])

The old pension system in recent years has managed to accumulate financial resources that can easily cover the state's costs of repaying the external debt. If the pension assets were properly placed, problems with external borrowing could be alleviated. We draw such a conclusion on the basis of processing data on the values of external public debt and its comparison with the value of pension assets.

One of the main tasks of the state today is to keep pension savings in the domestic economy and work for it, bringing a sufficient investment income. It is necessary to make every effort to develop the securities market in the framework of economic development programs in general and expand the range of financial instruments of the pension assets of the AUPF pension fund.

To do this, it is necessary to consider the main points of the AUPF Investment Declaration approved by the National Bank of the Republic of Kazakhstan, where there are a number of characteristics that prevent the conclusion of the investment activities of the AUPF to new more efficient ways. As before, the high bar was set for the government securities of the Republic of Kazakhstan, their share may reach 60 %, while domestic issuers' shares can be invested not more than 5 % of the investment portfolio. Such a tight level of investment restrictions does not lie at all, in our opinion, in line Global trends and does not meet the interests of both the AUPF and the national economy as a whole. Already at this stage it is necessary to abandon this approach to investing in infrastructure projects of the AUPF pension assets and to make appropriate changes to the investment strategy of the AUPF in such a way as to be able to make wide use of the investment resources of the Single Accumulative Pension Fund in the interests of the entire national economy. In this connection, it is necessary to prescribe the AUPF a new regulation, which will consider issues with a decrease in the state's share in the economy, since while it is high, we will always have the risk that state money is used inefficiently. Also, in the AUPF Investment Declaration, the strict limitation of no more than 5 % of the investment limits on non-government equity securities, with the exception of equity securities of the quasi-public sector entities and second-tier banks of the Republic of Kazakhstan, included in the first category of Kazakhstan Stock Exchange's official list, Pension assets in instruments with a higher degree of risk. Therefore, it is necessary to consider the issues of the rigid system of controlling the own funds of the Unified Accumulating Pension Fund, and the organizational and legal form of the participants in the deal with the PA, and the monitoring system for these financial transactions [6, 2].

Thus, observing the effectiveness of investment in combination with the economic safety of pension savings, the role, importance and prospects of such a direction of investment activity as investing pension accumulations of citizens in infrastructure projects immeasurably increase. The creation of opportunities for using the AUPF pension assets for the development of the domestic economy through investment in infrastructure projects requires a whole range of activities. The following are among the main ones:

- it is necessary to revise the Investment Declaration of the Unified Accumulative Pension Fund by lim- iting five percent of investments in infrastructure projects;

- elaboration of legislative conditions and adoption of such documents that would not hamper the pro- cess of investing in infrastructure projects;

- stimulation by the state of cooperation between public and private sectors in the process of imple- menting infrastructure projects;

- creation of an attractive investment climate in the sphere of implementation of infrastructure

Investments in infrastructure projects, provided all the necessary conditions are met by the state, can, in our opinion, ensure, first, the safety of pension savings of citizens, and secondly, sufficient profitability for these investments. The implementation of infrastructure projects is associated with the creation of large and largest facilities of industrial and social infrastructure, which are mainly key socio-economic and strategic importance for the state. The functioning of infrastructure facilities is able to bring a stable income in the long term, and therefore these objects are most attractive for pension funds in terms of optimal and efficient placement of the so-called «long» resources that they have.

An important factor in the attractiveness of infrastructure for the Single Accumulation Pension Fund is that these facilities are sufficiently shielded from market fluctuations, as they operate in the conditions of natural monopolies and are protected by the state. As already mentioned above, infrastructure facilities have long service lives and bring a stable income. Besides, of course, large volumes of investment resources of the AUPF, aimed at financing infrastructure projects, can give a serious impetus to the growth of economic growth in the country. At the same time, the creation of infrastructure is a necessary link in ensuring the economic development of the country and has a beneficial effect both on the growth rate of the national economy and on raising the standard of living of the population and on the growth of its well-being. Already in the process of construction of infrastructure facilities, the development of a number of accompanying branches of the national economy is given a boost, new jobs are created, and the incomes of the population are increasing. As a result, there is a reverse positive effect in general on the country's pension system [7].

To date, the National Bank of the Republic of Kazakhstan has proposed a scheme for a two-stage modernization of the pension system, which includes the following:

- the first stage - the transfer of pension assets under the management of professional management companies on the basis of the mandate. This stage will ensure a uniform distribution of income from the management of pension assets among all depositors of the AUPF; Opportunity to identify the most effective management companies; Operative regulation and supervision of pension asset

- The second stage is the choice directly by the depositor of the management company that received the license of the National Bank of the Republic of Kazakhstan based on the results of the management of pension assets within the framework of the first

Thus, the goal of modernizing the pension system for transferring pension assets to the management of private management companies is to restore competition, where each investor could choose his own management company, which he trusts to manage his pension savings, and, accordingly, the choice of investment strategy appears. Also, the depositor may enter into an additional agreement with the AUPF, where his savings will be transferred to the management of the National Bank of the Republic of Kazakhstan, and the managing company - at the choice of the depositor. To implement this proposal, it is necessary to introduce certain measures in the Declaration to tighten the regulation of such kind of participants who will take the citizens' money for management. Form the market only for stable, high-capital players who will take on a high responsibility for managing the pension money of our citizens.

Also, it should be noted that, in the opinion of some experts, considering some of the main problems such as high inflation, undeveloped stock market and insufficient level of financial literacy of pension fund assets, some concerns are raised about the measures proposed by the National Bank, which do not sufficiently take into account the interests of depositors and the safety of savings.

References

- Sait OOO «Pensionnye i Aktuarnye Konsultatsii» [The LLC «Pension and Actuarial Consultations» web-site]. p-a-c.ru.Retrieved from http://www.p-a-c.ru [in Russian].

- Tobataev, D.Ch. (2015). Investitsionnaia deiatelnost Edinoho nakopitelnoho pensionnoho fonda Respubliki Kazakhstan [Investment activity of the single accumulative pension fund of the Republic of Kazakhstan]. Vestnik KazEU – Bulletin KazEU, Almaty. Retrieved from http://www.articlekz.com [in Russian].

- Sait AO «ENPF» [UAPF JSC web-site]. kz. Retrieved from http://www.enpf.kz [in Russian].

- Sait Natsionalnoho Banka Respubliki Kazakhstan [National Bank of the Republic of Kazakhstan web-site]. kz.Retrieved from http://www.nationalbank.kz [in Russian].

- Sait Ministerstva finansov Respubliki Kazakhstan [Ministry of Finance of the Republic of Kazakhstan web-site].minfin.gov.kz. Retrieved from http://www.minfin.gov.kz [in Russian].

- Respublikanskaia ekonomicheskaia hazeta – Delovoi Kazakhstan (2017). [The Republican Economic Newspaper – Business Kazakhstan]. No. 5(552), 12. [in Russian].

- Tobataev, D.C. Vlozheniia v infrastrukturnye proekty kak odno iz perspektivnykh napravlenii investitsionnoi deiatelnosti Edinoho nakopitelnoho pensionnoho fonda Kazakhstana [Investments in infrastructure projects as one of the promising areas of in- vestment activity of the Unified Accumulative Pension Fund of Kazakhstan]. group-global.org. Retrieved from http://www.group- global.org [in Russian].