The article analyzes the role mortgage lending in the system of social policy of a state. For countries in transition like Kazakhstan, the problem of improving the living conditions is primarily important as on time meeting of housing needs may help to overcome social instability. The research presents that a mortgage lending has its own place in the system of social programs of the government. The state operates with the help of state legislative and executive power and provides socio-economic, organizational and legal conditions that regulate, facilitate and monitor social doctrine in the housing sector. In this system banks contribute to the realization of social programs through their objectives by using own tasks in the mortgage market. The research is concentrated on Kazakhstan’s case where the housing problem is resolved through active state participation using different supporting mechanisms. It reveals that the main driver on the housing market in Kazakhstan is the government, which actively fosters sector development by accepting the Regional Development Program until 2020. The research shows that 48 % of all mortgages during 2014–2016 provided with help of state support. This explained by lower interest rates and down payment for a mortgage loan as well as better lending terms. The results of the research showed that in the current situation the population increasingly relies to state support in mortgage lending.

The system of state support of the housing sector exists in most countries. The need for such support is dictated by the importance of the housing sector to the economy and the presence of multiple relationships that could have a decisive impact on the development of the country. The causes and the level of support varies depending on the degree of development of the economy and the conditions of the housing sector.

State policy in the housing sector is aimed mainly at removing possible inconsistencies and support socially vulnerable categories of citizens. One of the main areas of government support in the housing sector is the aid to citizens with low income to improve their living conditions. The resolution is impossible without forming scientific approaches of analyzing inconsistencies of the mortgage lending system in terms of state social support to overcome social instability on the one hand, and the other not to turn state support into an instrument that hinders the development of competition on the market.

Various aspects of mortgage lending are reflected in researches conducted by domestic and foreign economists. The most important works are devoted to the study methodology of mortgage lending and it includes the works of the next scientists: W.Buffett, D. O’Brien, A.Gent, L.Goh, J.Campbell, S. Myers, J.Marshall, R. Murray, R. Norton, A. Feldman, W.Sharpe and others. A significant contribution to the development of mortgage market research made by the next CIS authors as O.Bessonova, M.Solodilova, S.Mazhos, N.Nazarchyuk, S.Khachatryan, V.Loktionov, V.Kudryavtsev. Kazakhstani authors also carefully studies the problem. Features of the current state, problems and development of mortgage lending in Kazakhstan are represented in the works by A.Aryn, K. Beketova, B.Zhalinov, G. Dauliyeva, N.Kabasheva, A.Kemelbayeva, N.Dyusenbayev and others.

The methodological basis of the research is the dialectical method of cognition. The study used as scientific methods (analysis, classification, system approach), as well as special methods of cognition (statistical methods).

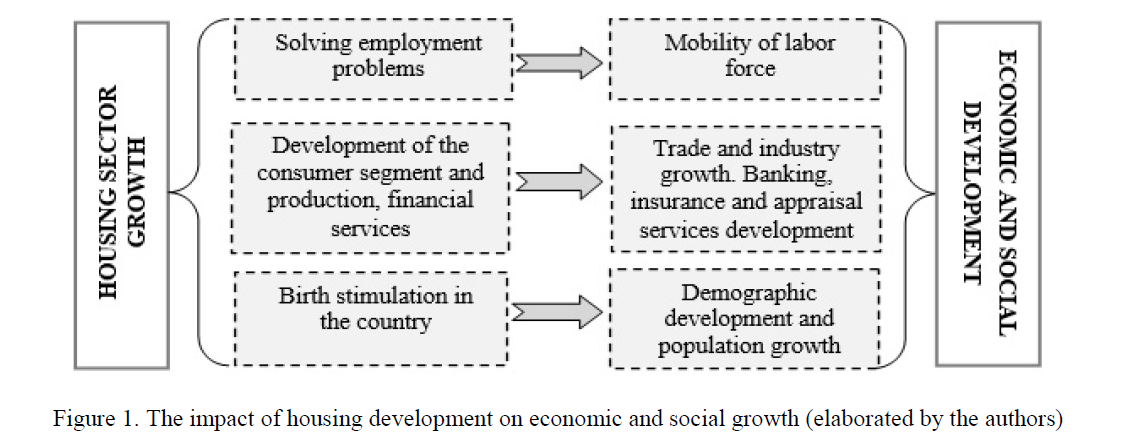

The undeniable truth of economic science is the housing sector growth leads to solving employment problems as the government develops mortgage programs in priority regions where new labor force required. In turn, this increases the mobility of the population in matters of employment. In addition, housing growth ensures the improvement of life quality and stimulates consumer demand for goods and financial services. Russian scientist O.Bessonova, for her part, declares that the housing sector development has a significant impact on demographic processes and increases the birth rate in the country [1] (Fig. 1).

Figure 1. The impact of housing development on economic and social growth (elaborated by the authors)

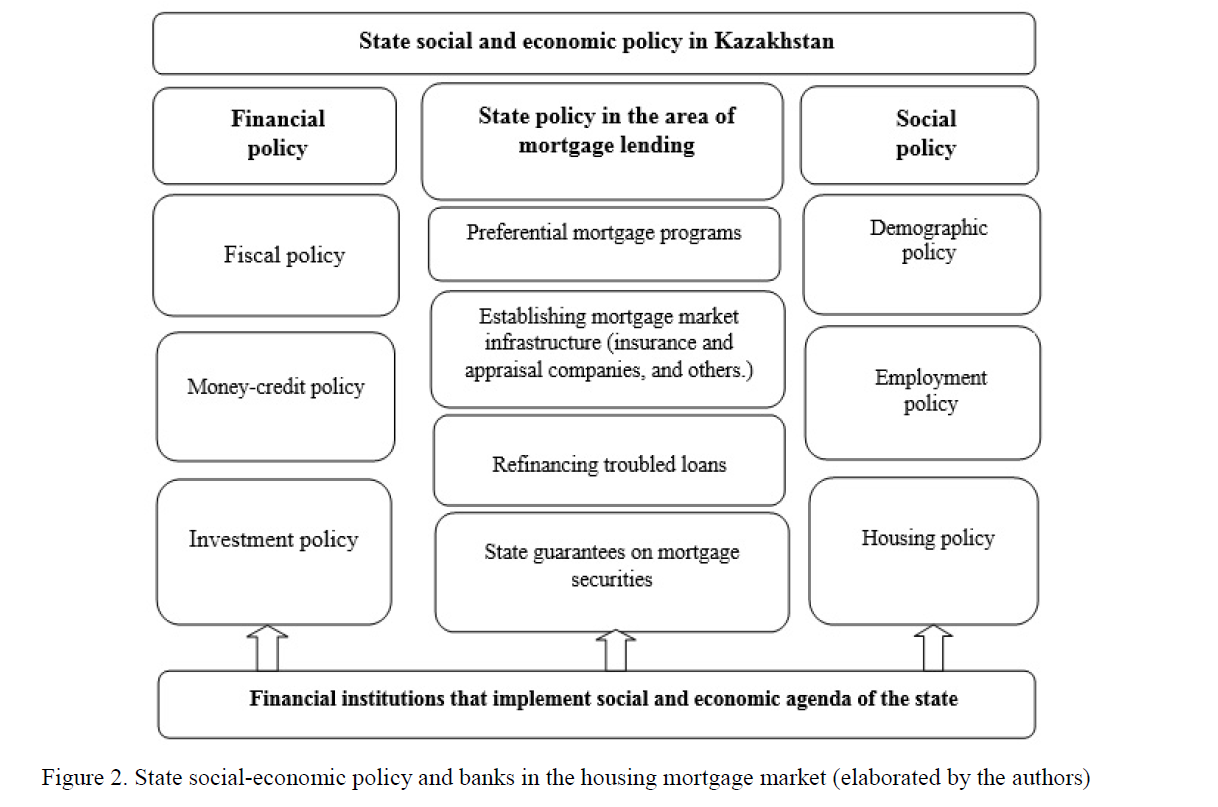

Like all markets, the mortgage market is the totality of interactions between suppliers (investors) and consumers (borrowers) with intermediaries (mortgage lenders and brokers) in between, in a framework set by law and regulation. Changes affecting any of these categories affect the characteristics and effectiveness of the market [2]. We can add to this list in transitional economies the government as a mortgage lending has its own vital place in the system of social programs. The government operates on the mortgage market with the help of state legislative and executive power. It provides socio-economic, organizational and legal conditions for the interaction of economic subjects of the housing mortgage system and regulation and supervision in order to implement the adopted social doctrine.

Figure 2. State social-economic policy and banks in the housing mortgage market (elaborated by the authors)

The social and economic policies aimed at providing the population with housing have a complex structure and banks contribute to the realization of their objectives by using their own tasks in the mortgage market.

The proclamation of the paradigm of socially oriented market type state determines the choice of priorities for the conduct of fiscal policy, which is an integral part of the credit policy in mortgage lending and forming directions of social policy (Fig. 2).

The main driver of developing housing market in Kazakhstan is the Regional Development Program until 2020 accepted in 2014. The program provides the following measures of state support in housing construction [3]:

- the allocation of prepared land in accordance with master plans, detailed planning projects and rules for the development of settlements;

- providing the engineering and communication infrastructure, including engineering networks of heating, water, gas and electricity, telephony, water disposal (sewerage) and engineering;

- the industrialization of construction, which will ensure the growth of volumes and the reduction of construction time, the reduction of prime cost based on the use of advanced

The state program identified four main directions in supporting the residential mortgage market and respective recipients of the state support:

- special Housing programs for people who are on the waiting list of local executive bodies;

- housing program for all categories of citizens using state mortgage agents;

- housing program for young families;

- rental housing program for certain categories of Kazakhstan citizens (Table 1).

T a b l e 1

The state participation in the development of the residential mortgage market in terms social support

|

State participation |

The mechanism of the state support |

|

1 |

2 |

|

Housing for people who are on the waiting list of local executive bodies |

Categories of citizens who can apply |

|

- Disabled people and participants of the World War II; - Socially vulnerable segments of the population in accordance with article 68 of the Law on Housing Relations of the Republic of Kazakhstan; - Civil servants, employees of budget organizations, servicemen, cosmonauts, employees of special state bodies and persons holding elective posts |

|

|

Process |

|

|

Local authorities (akimat): allocates a land plot for construction, chooses a developer, finances construction, puts it into operation, and provides apartments, organizes the list of applicants and distributes apartments among them. Client: collects all the documents and queue up for the provision of housing from the communal fund of the local executive body Centers of service of the population: reception of documents |

|

|

Housing from «House Construction Savings Bank» JSC for all categories of Kazakhstan citizens |

Process |

|

Local authorities (akimat): allocates a land plot for construction, chooses a developer, finances construction, puts it into operation, and sells apartments. Bank: forms pools of buyers and tenants from among its depositors, calculates solvency, and provides a loan for the purchase of housing. Client: signs an agreement on housing construction savings, regularly replenishes the deposit, submits an application for participation in the program |

|

|

Housing from «House Construction Savings Bank» JSC for young families |

Categories of citizens who can apply |

|

- a young married couple who have been married for at least two years; - the age of the spouse is under 29 years of age - an incomplete family in which one of the parents brings up children |

|

|

Process |

|

|

Local authorities (akimat): allocates a land plot for construction, chooses a developer, finances construction, puts it into operation, sells apartments and organizes the list of applicants and distributes apartments among the participants. Bank: calculates solvency and provides a loan for the purchase of housing. Client: submits an application for participation in the program to local authorities, signs an agreement on housing construction savings, regularly replenishes the deposit, takes a loan in the bank. |

C o n t i n u a t i o n o f T a b l e 1

|

1 |

2 |

|

Rental housing program from «Kazakhstan Mortgage Company» JSC for certain categories of Kazakhstan citizens |

Categories of citizens who can apply |

|

Large families, incomplete families, families with disabled children, orphans, children left without parental care, oralmans, civil servants, servicemen, employees of special state bodies, employees of budgetary organizations, disabled people of 1,2 groups. |

|

|

Process |

|

|

Local authorities (akimat): allocates a land plot for construction, chooses a developer, finances construction, puts it into operation, and organizes the list of applicants and distributes apartments among the participants. KMC: calculates solvency and provides a lease with the right of redemption after 20 years. Client: submits an application for participation in the program to local authorities; gets possibility of early repayment of rental housing after 5 years of lease. |

Note. Source elaborated by the authors.

Kazakhstan in its social policy orientates on building affordable housing conditions through different state programs and increasing the availability of housing to socially vulnerable people through developing renting mechanisms. Thus, the existing system of state support for housing market can be identified as follows:

- republican and regional programs of mortgage lending for priority categories of citizens;

- building low and middle class social housing by local executive bodies for citizens on the waiting list;

- construction of rental housing with the option to purchase after a certain time;

- allocation of land plots for individual

In 2017, the country begins the implement of a fundamentally new state program «Nurly zher», according to which 1.5 million families will get their homes in the next 15 years [4]. The central role is allocated to the state support of families by subsidizing up to 7 % mortgage rates which allows to decrease interest rates 8000 loans only in 2017 [5].

As of January 1 2017, the volume of mortgage market in Kazakhstan is estimated at 983 bln. tenge, which is higher for 9 % than at the beginning of 2016. However, the volume of mortgage loan portfolio in dollars has decreased for 40 % for the same period, due to series of devaluations of the national currency in 2015. Now in 2017 it is estimated at 2.8 bln. US dollars. The mortgage market stagnation in Kazakhstan is over since 2016 mortgage lending grew to 9 % compared with a year earlier (Table 2).

T a b l e 2

Dynamics of the volume of mortgage portfolio of Kazakhstan financial institutions

|

Portfolio volume |

2010 y. |

2011 y. |

2012 y. |

2013 y. |

2014 y. |

2015 y. |

2016 y. |

|

All mortgages, in mln.KZT |

684,964 |

734,196 |

806,021 |

863,765 |

912,018 |

900,779 |

983,349 |

|

Equivalent in mln. USD |

4,648,551 |

5,007,475 |

5,405,546 |

5,677,808 |

5,089,670 |

4,062,503 |

2,873,944 |

|

Official average exchange rate |

147.35 |

146.62 |

149.11 |

152.13 |

179.19 |

221.73 |

342.16 |

Note. Source elaborated by the authors based on Statistical Bulletin and official currency exchange rates of the National Bank of RK.

The mortgage market in Kazakhstan is presented by commercial banks, one state run «House Construction Savings Bank» and one specialized mortgage organization «Kazakhstan Mortgage Company». According to our estimations in 2016 only six banks out of 34 offered mortgage programs.

«House Construction Savings Bank» JSC is the only bank in the country, which implemented the system of housing construction deposits. Since the beginning in 2003 and as of March 1, 2017, the bank signed 1.2 million contracts on savings [6]. The terms of deposit programs range from 3 to 15 years, and the terms of housing loans from 6 to 25 years. The government provides financial support for the system of housing construction deposits by paying premiums for deposit owners. Annual state premium is set at 20 % of the amount of the deposit.

The second state run institution on housing market in Kazakhstan is «Kazakhstan Mortgage Company» JSC. It is specialized financial operator of the government policy in housing availability provision sphere for population of the republic thorough mortgage lending facility and provision of rental housing for solving of social-oriented targets. The difference of this company from «House Construction Savings Bank» that it executes its work by leasehold housing realization within state and own programs and mortgage loans liabilities buyout from the second tier banks.

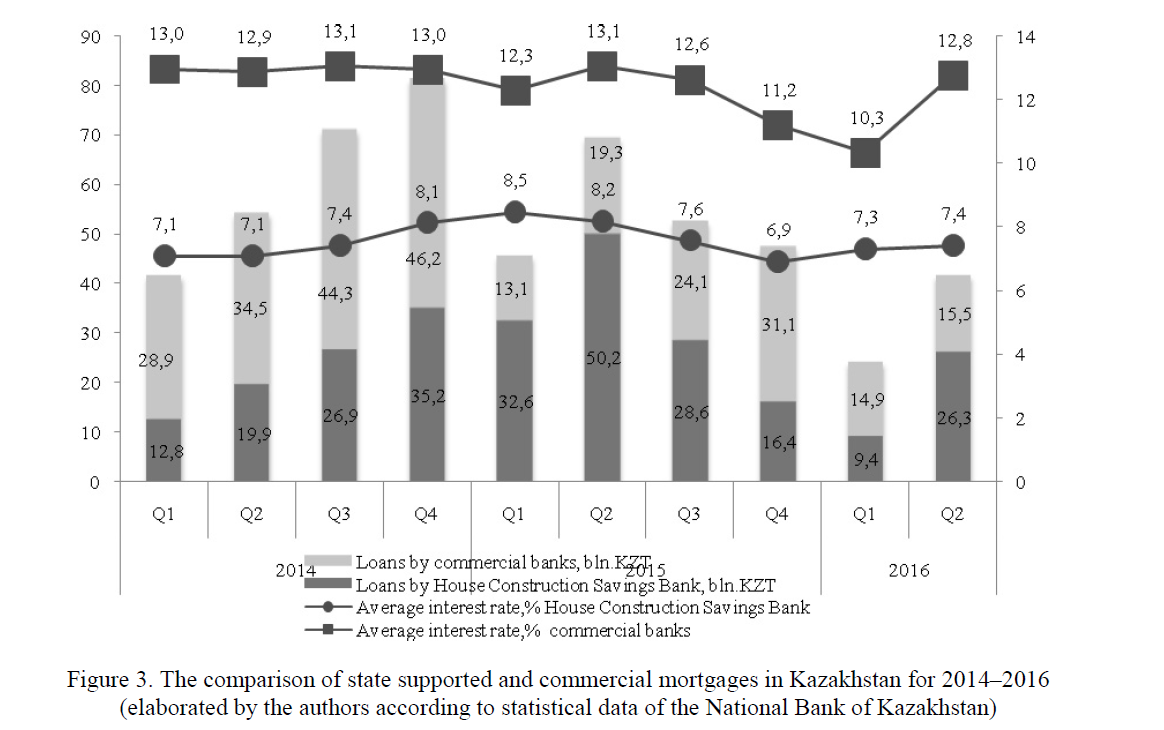

Analysis of state social participation in mortgage market can be presented by the next figures: state run «House Construction Savings Bank» for 2014-2015, and for the first two quarters of 2016 approved mortgage loans for KZT 258 billonion. For the same time commercial banks approved loans for KZT 271 billion.

This shows that 48 % of all mortgages provided with help of state support. It can be explained by lower interest rates and down payment for a mortgage loan as well as longer lending terms. For example, in the third quarter of 2016 the average interest rate for mortgage loans on commercial market was equal to 12.8 %, in the same time «House Construction Savings Bank» rate was 7.4 % (Fig. 3).

Figure 3. The comparison of state supported and commercial mortgages in Kazakhstan for 2014–2016 (elaborated by the authors according to statistical data of the National Bank of Kazakhstan)

Thus, we can conclude that the demand for mortgage lending is satisfied equally by the state and commercial banks. Nevertheless, it is necessary to note that commercial banks are cautious in lending now, especially by the results of 2015 when 59 % of all mortgage loans were approved by House Construction Savings Bank (127.8 billion out of 215.4 billion tenge). This proves not only the attractiveness of state support programs in housing sector, but also the emerging tendency of the redistribution on the mortgage market in the conditions of the crisis with the strengthening of the role of the state.

The analysis of the mortgage lending in the system of social policy allowed drawing the following general conclusions:

- the housing sector growth leads to solving employment problems, develops consumer segment, production and financial services. In addition, it can be a tool for demographic improvements;

- A mortgage lending has its own vital place in the system of state social programs in Kazakhstan. The government operates on the mortgage market with the help of state legislative and executive power. It provides socio-economic, organizational and legal conditions for the interaction of economic subjects of the housing mortgage system and regulation and supervision in order to implement the adopted social doctrine;

- Kazakhstan uses different financing schemes in its social policy, which include republican and regional programs, building social housing for selected population groups, construction of rental housing and market-based financing;

- For seven years since 2010, the mortgage portfolio of banks has grown by 31 % from KZT 684 billion to 983 billion at the end of 2016. Now the mortgage market recovers after the recession. In 2016 mortgage lending grew to 9 % compared with a year earlier. This is a good signal as in 2015 it dropped to 1 %;

- The government in the face of its mortgage bank House Construction Savings Bank became the biggest player on the market. Our research shows that 48 % of all mortgages provided in 2014-2016 approved by the state run bank. It is explained by better lending terms offered by the state bank and cautions for new lending from commercial banks. Therefore, the crisis strengthened the role of the state bank on the mortgage market.

The results of the research showed that in the current situation the population increasingly relies to state support in mortgage lending. The high level of interest rates on mortgage loans, tightened conditions for lending by commercial banks contribute to the redistribution of the market and the state becomes the main operator in the mortgage market. However, excessive concentration of mortgage services in public hands is another concern, as it does not promote competition and improve banking services.

References

- Bessonova, O.E. (2010). Novaia zhilishchnaia model kak antikrizisnaia mera [New housing model as an anti-crisis measure]. Rehion: ekonomika i sotsiolohiia – Region: Economics and Sociology, 2, 203–222 [in Russian].

- Scanlon, Kathleen and Lunde, Jens & Whitehead, M.E. (2011). Christine Responding to the housing and financial crises: mortgage lending, mortgage products and government International journal of housing policy, 11(1), 23–49.

- Postanovlenie Pravitelstva Respubliki Kazakhstan ot 28 iiunia 2014 hoda № 728 «Ob utverzhdenii Prohrammy razvitiia rehionov do 2020 hoda». Prilozhenie № 3 [Resolution of the Government of the Republic of Kazakhstan of June 28, 2014 728 «On the approval of the Program for the Development of Regions to 2020». Appendix N 3]. online.zakon.kz. Retrieved from http://online.zakon.kz/Document/?doc_id=31584094#pos=0;0 [in Russian].

- «Nurly zher» obespechit zhilem 1,5 mln kazakhstanskikh semei. [«Nurly zher» will provide housing for 1.5 million Kazakhstani families]. kz. Retrieved from http://bnews.kz/ru/redesign/special/modernizatsiya_30/view-nurli_zher_obespechit_zhilem _15_milliona_kazahstanskih_semei [in Russian].

- Novye usloviia ipoteki predlahaet zhilishchnaia prohramma «Nurly zher» kazakhstantsam [New housing conditions are offered by the housing program «Nurly zher» to the citizens of Kazakhstan]. kz. Retrieved from http://www.kazpravda.kz/news/ekonomika/novie-usloviya-ipoteki-predlagaet-zhilishchnaya-programma-nurli-zher-kazahstantsam/ [in Russian].Official website of the House Construction Savings hcsbk.kz. Retrieved from http://www.hcsbk.kz/about-the-bank/.