Purpose – Banking system is a central element of modern economy and thus requir regulation and supervision. Declining confidence in the banking sector leads to the reduction of private savings and inefficient fund allocation that have a negative impact on the state of the economy as a whole. Thus, there is a need to develop early-warning systems that are able to identify distressed banks before the moment their licences are withdrawn. The presence of weak financial institutions may result in dysfunction in overall banking system that significantly affects real economy. The determination of models that detect potential bankrupts allows management as well as regulator to take measures toward stabilization and improvement of banks timely, thus preventing their failure and further crisis in the system. In this way, the study is aimed at the assessment of Taffler’s model predictive ability in forecasting bankrupt banks in the banking system of Kazakhstan.

Methodology – Taffler’s linear regression model (Z-score or T-score) with four financial ratios for the evaluation of organizations’ financial state. The study also employs descriptive and comparative analysis to es strict assess the financial performance of Kazakhstan banks.

Originality/value – The focus of this study is to confirm the little predictive ability of Taffler’s Z-score model to forecast the failure of Kazakhstan banks. For this purpose, the author analyses the financial condition of twenty three Kazakhstan banks using Taffler’s model that has not been previously employed in Kazakhstan practice for banks health assessment.

Findings – the null hypothesis that Taffler’s Z-score model has little predictive ability to forecast the financial state of Kazakhstan banks is put forward and confirmed. The author infers that this model is not appropriate to the peculiarities of Kazakhstan financial system, since results are indicative of the fact that the majority of banks in the period between 2011 and 2015 have high risk of bankruptcy, whereas in reality the situation is quite different.

Introduction

The problem of financial distress prediction has a special place among theoretical and practical issues related to bank management. Being a country with developing economy, Kazakhstan tends to face certain degree of instability in many processes and factors that basically create “an external environment” of banks’ activity. Therefore, to ensure effective management, it is important to perform financial analysis of bank’s activity aimed at determination of its state at a given development stage, as well as to conduct diagnostics aimed at early detection of vulnerability and bankruptcy in future [1]. Thus, identification of unfavourable trends in banks’ development and forecasting crisis situation and bankruptcy become of paramount importance. There exist a large number of bankruptcy prediction models that are used in economic science as well as in practice. These models are different in terms of underlying principles and methods. In this way, the most popular assessment tool that is used by the researchers is the integrated assessment based on bank failure prediction models. This approach allows making a professional judgement with respect to maximum permissible parameters of financial relations using only one quantitative integral indicator. Thus, integrated assessment tests based on multiplicative discriminant analysis are available and easy to apply. Furthermore, financial ratios that are at the core of these models are estimated using the information from financial reports available to the public. These factors provide an opportunity to determine the degree of reliability of counterparties in financial relations with fairly high probability and effectively manage the parameters of financial operations of economic entities [2, 3].

Nowadays, an extensive methodological base for estimating integral indicators is developed on the basis of foreign research. The need to manage financial resources and capital in corporate finance causes the primacy of the emergence of discussed models in the countries with developed market economies [4, 5].

However, it is important to note that foreign models may not take into consideration the peculiarities of Kazakhstan economy and therefore be less accurate in forecasting. Thus, the aim of this study is to systematize and approbate the formalized approaches toward the assessment of the probability of banks’ failure using financial performance indicators based on real data. The application of relevant bankruptcy prediction methodologies should allow to introduce various anti-crisis strategies in advance, before commercial bank’s collapse in order to prevent crisis. In this way, the author tests the predictive ability and possibility of application of Taffler’s Z-score model to forecast financial state of Kazakhstan banks [6, 7]. Given model has not been previously employed in Kazakhstan practice for banks health assessment.

Literature review

The analysis of foreign models shows that the development of integral assessment became possible in the course of application of multiplicative discriminant analysis by the researchers engaged in the bankruptcy diagnostics, in particular by E. Altman, E. Brigham, R. Liss, Ch. Prassana and others [8].

The issue of bankruptcy prediction is more extensively reflected in the research of foreign authors: A. Claire and R. Priestly, J Kolari, M. Caputo, R. Wagner, P. Meyer and H. Pifer. Similarly, Russian authors including Golovan, A.M. Karminsky, V. Kopylov, A.A. Peresecky, A.M. Yevdokimov study the possibility to assess the likelihood of credit institutions failure. The factors determining the financial stability of the banks in post-Soviet countries are analysed in the research by Lanin and Vennet [9].

The model introduced by Richard Taffler (1977) bears his name and is known as Taffler’s test or Taffler’s bankruptcy model. It basically represents the linear regression model with four financial ratios for the evaluation of financial health of a company. In particular, it incorporates the leverage, profitability, liquidity, capital adequacy and other parameters that in aggregate provide an objective picture of company’s financial state [10]. Vineet Agarwal, Richard J. Taffler (2007) evaluate the predictive ability and effectiveness of Taffler’s model during fifteen-years period from the moment it has been initially developed. The findings indicate that

the model demonstrates accurate predictive ability during long period of time [11, 12].

Pavlović Vladan, Sasa Muminovic, Cvijanović Janko M. (2011) assess the predictive ability of Taffelr’s model in terms of forecasting the failure of Serbian banks. They use a sample of 62 companies that are included in the basket of Belex15 and Belexline indices for the period between 2006 and 2010. Since none of the companies in the research sample went bankrupt in the reviewed period, the analysis included companies that went bankrupt in years 2009 and 2010 and are at the same time which are classified as large legal entities [13]. Machek, O.(2014) conducts an analysis in order to determine the forecasting power of such well-known models as Taffler’s model and Altman’s model using a sample of Czech companies for long-term period (20072012). The results are indicative of the fact that Taffler’s model is less accurate, whereas Altman’s Z-score is a good approximation of reality [14].

The rationale behind constant attempts aimed at the development of the system of effective forecasting of credit institutions’ financial condition is the necessity to ensure the prudential supervision over the activity and performance of banks. The task is relevant not only to the countries with economies in transition, but also to relatively stable economies.

If one considers the experience of the USA, for the purpose of early warning of possible bankruptcies the specialists of controlling bodies regularly carry out inspections visiting the banks in order to study their documentation. As a result of such inspections, the banks are evaluated using CAMELS rating system. However, even though the inspections are viewed to be effective, they are not frequent enough, and hence cannot fully and quickly reflect the changes in the financial state of the banks in rapidly changing market conditions [15]. Thus, in order to develop more reliable and prompt forecasting of banks’ performance, it is important to have a system of early warning.

Research methodology and data collection

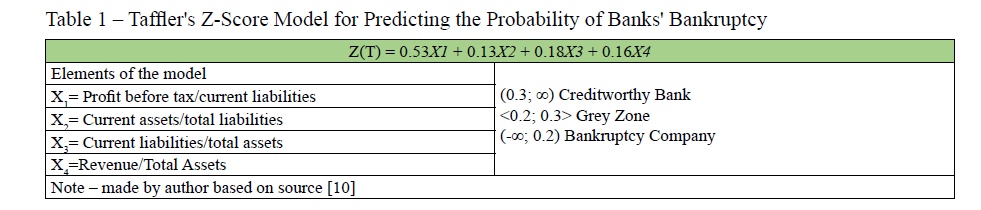

Taffler’s bankruptcy model (1977) is based on scoring approach and represents the linear regression model with four financial coefficients for the assessment of financial stability of 46 UK companies that default and 46 companies that are stable during the period between 1969 and 1975. Taffler’s model incorporate the ratios that are easily defined and reflect the most significant links to the solvency of companies [10].

The general economic meaning of the model is the function of several indicators that characterize the economic potential of bank and the results of its performance over the past period.

The bankruptcy prediction model that can be applied for second-tier banks of the Republic of Kazakhstan is Taffler’s Z-score model. (Table 1).

Table 1 – Taffler's Z-Score Model for Predicting the Probability of Banks' Bankruptcy

According to this model, if Z-score takes values of more than 0,3 it is assumed that there is a low risk of bank's bankruptcy during the year (creditworthy bank); if the value is less than 0,2, then bank is viewed to have a high risk of failure (bankruptcy bank); if the value is between 0,2 and 0,3, it means that bank is at risk (grey zone).

Financial ratios in Taffler's model are assigned the following weights based on the degree of impact on resulting Z indicator: X1-53%, X2-13%, X3-18%, X4-16%.

According to the results of conducted tests, given model identifies failure bank with probability of:

- 97% one year before bankruptcy;

- 70% two years before bankruptcy;

- 61% three years before bankruptcy;

- 35% four years before bankruptcy [11,12].

To conduct the analysis of banking system of the Republic of Kazakhstan, the author collects the secondary data from the statistical bulletin of the National Bank of the Republic of Kazakhstan, Rating Agency of the Regional Financial Center of Almaty and audited consolidated financial statement of commercial banks for recent five years (2011-2015).

On the basis of research's problem and objectives outlined above, the research’s hypothesis has been formulated as follows:

H0: Little predictive ability of Taffler's Z-score model to forecast the financial state of Kazakhstan banks.

Research results and findings

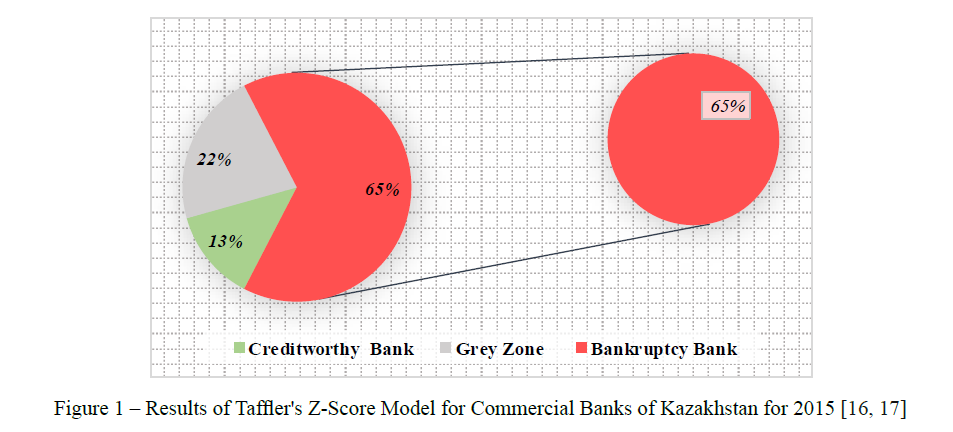

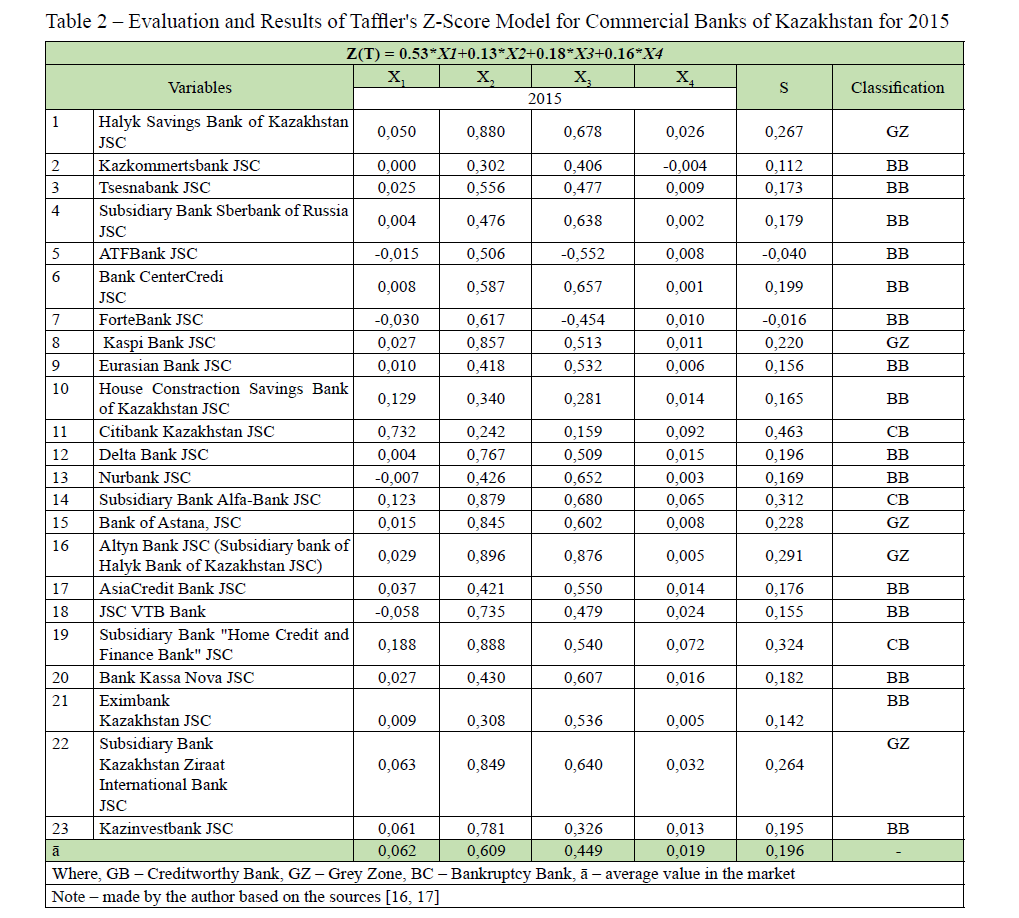

Calculating the value of Z-score and determining the bankruptcy criteria for 23 commercial banks of the Republic of Kazakhstan using Taffler's model (Figure-1 and Table-2).

The analysis further proceeds with well-known Taffler's model (1983) that is based on Z-score. It is important to note that this model is applied on the sample of Kazakhstan commercial banks for the first time.

For the purpose of implementing the Z-score model, 80 financial ratios are estimated. The data is analyzed for a number of solvent and bankrupt banks. To process the obtained information, various statistical methods are employed, as a result of which a multidimensional discriminant is constructed that allows developing a solvency model based on partial coefficients. The complexity of the model is motivated by the integration of separate dimensions weighted for the purpose of developing single efficiency indicator. It also specifies four main dimensions of bank's financial condition that are measured by selected ratios and reflect key parameters of bank's activity. In particular, the set of investigated ratios that are determined through the use of factor analysis includes profitability ratios, working capital ratios, financial risk indicators and liquidity ratios. In combination, the coefficients of this model provide an overall objective picture of bankruptcy risk in future and solvency to date.

The results of the analysis are indicative of the fact that in 2015, there are 3 commercial banks that can be named as "Creditworthy Banks", 5 banks are placed in "Grey Zone", whereas 15 banks are categorized as Bankruptcy Banks (Figure-1 and Table-2).

Figure 1 – Results of Taffler's Z-Score Model for Commercial Banks of Kazakhstan for 2015 [16, 17]

Through the factor analysis, X1 measures bank's profitability, X2 assesses working capital position, X3 outlines financial risk and X4 represents bank's liquidity.

X1 – is the ratio of profit before tax to bank's current liabilities. The ratio reflects the extent to which bank is able to fulfill its obligations using internal sources of financing. In other word, it assesses whether the

income generated during the accounting period or one year is sufficient to cover liabilities that must be paid out during the accounting period or one year. Higher ratios are attributable to the following banks: Citibank Kazakhstan (0,732), Subsidiary Bank "Home Credit and Finance Bank" (0,188) and House Constraction Savings Bank of Kazakhstan (0,129). Such indicators imply that for instance, Citibank Kazakhstan is able to cover approximately ¾ parts (73,2%) of its current liabilities using the income that it generates for a corresponding accounting period or year. Subsidiary Bank "Home Credit and Finance Bank" is able to cover 18,8% of its current liabilities, whereas for House Constraction Savings Bank of Kazakhstan the result is 12,9%. One should note that the average ratio for 23 banks under the study amounts 0,062. The lowest ratio is estimated for VTB Bank (-0.058), which implies that the ratio of its losses is 0,058 higher than its current liabilities.

X2 – is the ratio of current assets to total liabilities. The ratio indicates the ability of bank to cover its total liabilities using its current assets. To be more precise, it reflects the state of banks working capital as well as its liquidity. In general, a higher ratio is interpreted as a positive sign, since it is indicative of the fact that bank is more likely to meet its liabilities with current assets it owns. In particular, the ratio of 1,0 or more implies that bank can easily face its debt obligations. Interestingly that all banks in the sample exhibit the ratio of less than 1 with the lowest values recorded for the following banks: Citibank Kazakhstan (0,242), Kazkommertsbank (0,302) and Eximbank Kazakhstan (0,308).

Table 2 – Evaluation and Results of Taffler's Z-Score Model for Commercial Banks of Kazakhstan for 2015

X3 – is the ratio of current liabilities to bank's total assets, which is an indicator of financial risks. One can observe that the highest ratios are estimated for the following banks: Altyn Bank JSC (Subsidiary bank of Halyk Bank of Kazakhstan JSC) (0,876), Subsidiary Bank Alfa-Bank (0,680) and Halyk Savings Bank of Kazakhstan (0,678). It implies that the risk of illiquidity for these banks is higher, taking into account that the average ratio for 23 banks under the study amounts 0,449.

X4 – is the ratio of bank's revenue to its total assets, which determines the efficiency of bank in terms of its assets disposal in order to stimulate revenue. Therefore, a higher ratio is more favourable for banking sector, since it implies that bank is more efficient in utilizing its assets. A lower ratio, on the contrary, might be indicative of the fact that bank cannot manage its assets properly. As for the results of the analysis, the following banks have stronger positions: Citibank Kazakhstan (0,092), Subsidiary Bank Alfa-Bank (0,065) and Subsidiary Bank Kazakhstan Ziraat International Bank (0,032); whereas some banks tend to exhibit poor revenue to total assets ratio, including the following: Kazkommertsbank (-0,004), Bank Center Credit (0,001) and JSC Subsidiary Bank Sberbank of Russia (0,002).

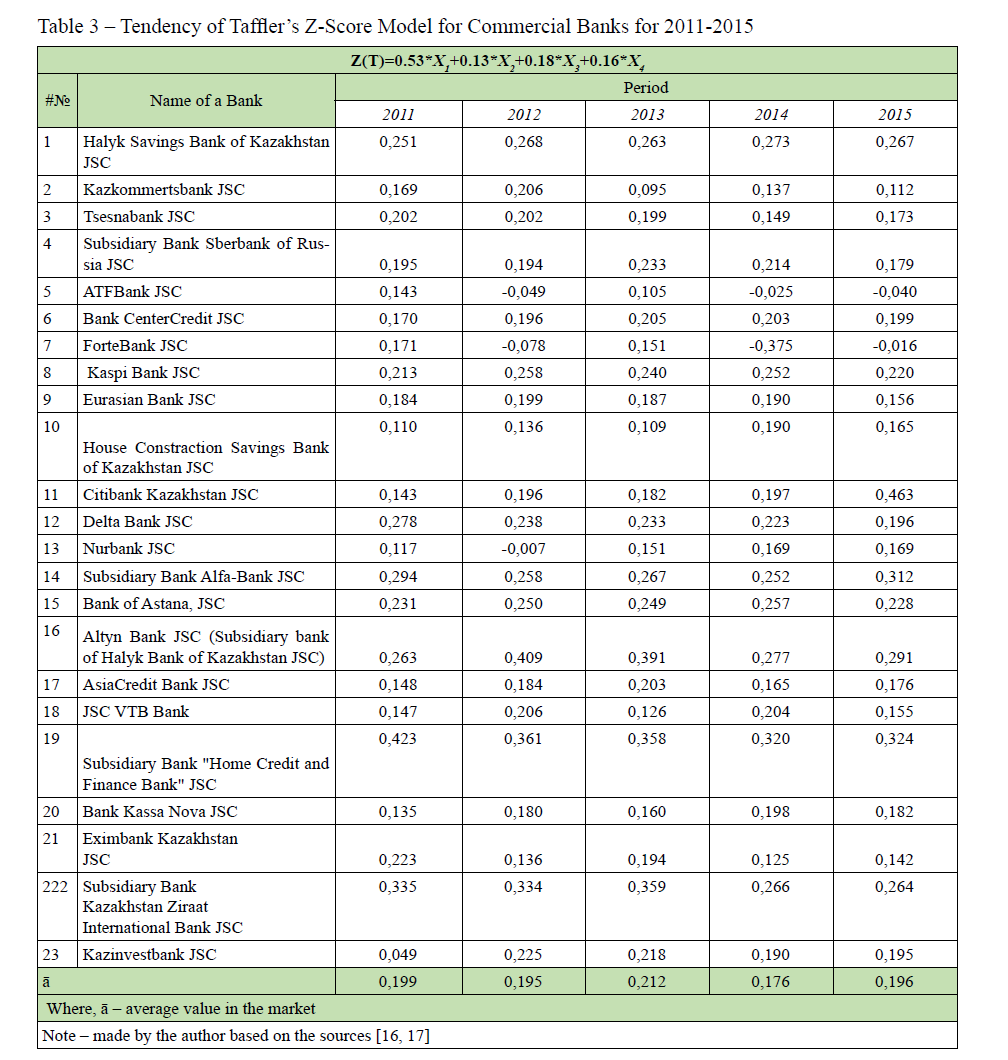

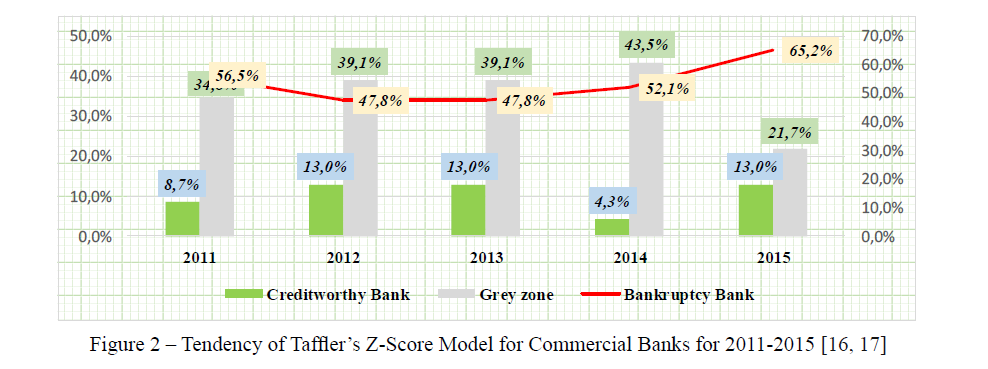

Table 3 – Tendency of Taffler’s Z-Score Model for Commercial Banks for 2011-2015

The results presented in Table-3 and Figure-2 suggest that in 2011, 2 banks have the status of "Creditworthy Banks", 8 banks are placed in "Grey Zone" and 13 banks are found to be "Bankruptcy Banks". In 2012, there are 3 commercial banks that can be named "Creditworthy Banks", 9 banks are in "Grey Zone" and 11 banks have the status of "Bankruptcy Banks".

The number of "Creditworthy Banks", banks in "Grey Zone" and "Bankruptcy Banks" does not change in 2013. In 2014, there is only 1 bank that is categorized as "Creditworthy Bank", 10 banks are placed in "Grey Zone" and 12 banks are defined as “Bankruptcy Banks".

Figure 2 – Tendency of Taffler’s Z-Score Model for Commercial Banks for 2011-2015 [16, 17]

Conclusions

The results of investigation verify the hypothesis that was stated earlier:

H3: Little predictive ability of Taffler's Z-score model to forecasting financial situation of Kazakhstan banks.

For the purpose of investigation, the author collects the data for the sample of 23 commercial banks that are different in terms of size, public participation and presence of foreign capital. These banks tend to demonstrate relatively good financial performance, and none of them default during the period of the analysis (2011-2015). One of the most significant issues related to the model presented in this study is the fact that it is applied only with respect to the banks whose shares are traded in stock exchange. It is possible, to substitute the market value of shares with some estimation of assets value. For instance, one can estimate the value of banks using the discounted cash flow method or employ net asset value reflected in the balance sheet. The accuracy in this case directly depends on initial information when model is developed.

The application of foreign models when analyzing the domestic financial system has serious limitations, since the implementation of economic patterns in the financial relations of Kazakhstan banks is quite specific. In this context, there is a need to develop Kazakhstan bankruptcy prediction models taking into consideration the peculiarities and conditions of the financial system of Kazakhstan [18, 19].

In domestic practice, the quantitative assessment models are at the stage of their development and becoming, and therefore are not applied for the purpose of implementation of state supervisory function over the financial state of commercial banks.

Today, various programs are elaborated by the authorized bodies in order to support the country's financial system. In the framework of implementation of the instruction of the head of state to reduce the level of nonperforming loans to 15% in 2015 and up to 10% by January 1, 2016, the National Bank, in collaboration with the Government, has put significant efforts to decrease the amount of overdue loans and take measures to prevent further growth in their volume. To ensure monitoring and coordination of measures to reduce the level of non-performing loans, the Commission for evaluation and control of the activity aimed at the reduction of overdue loans has been established. To further improve the quality of loan portfolios, the regulator has planned to introduce a prudential norm for banks on the maximum limit of non-performing loans at the level of 10% from January 1, 2016. However, taking into consideration the length of time that is necessary for banks to bring in line their loan portfolios, a decision has been made to postpone the deadlines until January 1, 2018 [5].

In summary, it is important to note that the banking sector plays an important role in the economic development of Kazakhstan. This role is determined by its ability to ensure a channel for the uninterrupted transfer of temporarily available funds to the real economy that requires substantial capital investment for modernization purposes, as well as to overcome the crisis phenomena and enter the path of sustainable economic growth.

References

- Morttinen, L. Analyzing Banking Sector Conditions: How to Use Macroprudential Indicators // DNB Working Paper. – 2010. – № 9. – pp. 24-30.

- Altman, E. Financial ratios, discriminant analysis and the prediction of corporate bankruptcy [Electronic source] // Journal of Finance. – 1968. – № 4. – URL: www.jstor.org/stable/2978933?seq=1#page_scan_ tab_contents (accessed: 08.01.2017)

- Wang, , Campbell, M. Business failure prediction for publicly listed companies in China // Journal of Business and Management. – 2010. – № 16 (1). – pp. 75-88.

- Wang, , Campbell, M. Do Bankruptcy Models Really Have Predictive Ability? Evidence using China Publicly Listed Companies // International Management Review. – 2010. – № 6 (2).

- The National Bank of the Republic of Kazakhstan: Financial Stability Report of Kazakhstan [Electronic source]. – 2014. – URL: www.nationalbank.kz/?docid=954&switch=english (accessed: 02.2017)

- TheReportoftheNationalBankoftheRepublicofKazakhstanAssessmentofRisksintheFinancialSystem of Kazakhstan [Electronic source]. – – URL: ww.nationalbank.kz/cont/%D0%93%D0%9E_2015_%20 %D1%80%D1%83%D1%81%D1%81%D0%BA_.pdf (accessed: 16.04.2017)

- Altman, E. An Emerging Market Credit Scoring System for Corporate Bonds [Electronic source] // Emerging Markets Review. – 2005. – № 6. – URL: www.iiiglobal.org/sites/default/files/29creditscoringsystem0. pdf (accessed: 08.01.2017)

- Neumaierová, I, Neumaier, I. INFA Performance Indicator Diagnostic System // Central European Business – 2014. – № 3. – pp. 35-41.

- Лаврушин О. И. Устойчивость банковской системы и развитие банковской политики. – М.: КНОРУС, 2014. – 72 с.

- Vineet, , Richard J. T. Twenty-Five Years of the Taffler Z-Score Model: Does It Really Have Predictive Ability? [Electronic source] // Accounting and Business Research. – 2007. – № 37. – URL: www.tandfonline.com/doi/abs/10.1080/00014788.2007.9663313 (accessed: 12.02.2017)

- Tafa er J., Tisshaw, H. Going, going, gone – four factors which predict // Accountancy. – 1977. – № 88. – pp. 50-54.

- Altman, E. , Danovi, A., Falini, A. Z-Score Models' Application to Italian Companies Subject to Extraordinary Administration // Journal of Applied Finance. – 2013. – № 23 (1). – pp. 128-137.

- Pavlovic, , Muminovic S., Janko M. C. Adequacy of Taffler's model for bankruptcy prediction of Serbian companies [Electronic source] // Industrija. – 2011. – № 4. – URL: www.scindeks-clanci.ceon.rs/data/ pdf/0350-0373/2011/0350-03731104057P.pdf (accessed: 08.01.2017)

- Machek, O. Long-Term Predicticve Ability of Bankruptcy Models in The Czech Republic: Evidence from 2007-2012 [Electronic source] // Central European Business Review. – 2014. – № 3 (2). – URL: cebr.vse.cz/index.php/cebr/article/viewFile/120/94 (accessed: 16.03.2017)

- Muminović, Revaluation and Altman`s Z-score –the Case of the Serbian Capital Market [Electronic source] // International Journal of Finance and Accounting. – 2013. – № 2. – URL: www.article.sapub.org/ pdf/10.5923.j.ijfa.20130201.02.pdf (accessed: 25.03.2017)

- Consolidated Financial Statements of Commercial Banks of the Republic of Kazakhstan [Electronic source]. – 2017. – URL: www.kase.kz/ru/emitters (accessed: 04.2017)

- Current State of the Banking Sector of Kazakhstan [Electronic source]. –2016. – URL: nationalbank.kz/cont/%D0%A2%D0%B5%D0%BA%D1%83%D1%89%D0%B5%D0%B5%20 %D0%91%D0%92%D0%A3_eng_01.12.pdf (accessed: 25.02.2017)

- The IMF Country Report No. 14/258. The Republic of Kazakhstan. – 2014. – [Electronic source]: https://www.imf.org/external/pubs/ft/scr/2014/cr14258.pdf (accessed: 02.2017)

- The IMF Country Report No. 15/241 The Republic of Kazakhstan [Electronic source]. – 2015. – URL: http://www.imf.org/external/pubs/cat/longres. aspx?sk=43232.0 (accessed: 01.2017)