Purpose – Mobile banking, one of the popular financial service delivery media, has become very strong and widely accepted financial gateway to conduct financial transaction worldwide. The stakeholders of mobile banking services have significant roles to play to control and monitor the whole situation and to ensure further development in financial empowerment of its clients. This article indicates some challenges as well as analyzing and recommending some regulatory guidelines which help the mobile financial industry towards a glorious future.

Methodology – This research is conducted descriptive method. Data collected from secondary sources to analyze the expectations and challenges of this industry. Overall an empirical research to shape and expose the stakeholders’ expectations and challenges that will help private and government sector for guidelines to follow.

Originality/Value – The study is undoubtedly valuable not only in developing countries like Bangladesh but also for worldwide context as it will provide empirical facts to the current viability of mobile financial services. Stakeholders’ challenges and expectation for this industry will help the all the parties to understand and guide their vision towards this market driven sector.

Findings – This research focused on bringing out the hidden or discussed expectations of all the major parties of mobile financial service industry. The finding includes the challenge to face by this industry in coming years and to ways to meet those challenges.

1. Introduction.

Mobile financial services (MFS) are one of the largest growing financial sectors in Bangladesh. The rapid growth of mobile networks and wide spread adoptability bring this opportunity avail this horizon. Since the 2011, mobile financial services (MFS) had proved to be the finest integration of finance and technology in Bangladesh and it significantly contributed to rural-urban fund flow as efforts are being made to popularize mobile money as an important alternative to physical.

The tremendous growth of MFS agents crossing 543,000 agents which serving more than 25.87 million subscribers as reported in a survey conducted by USAID, 2015 demands a proper and effective panning and monitoring system in this sector.

The USAID report also showing that almost 68% of MFS transactions are originating from urban and semi-urban regions which indicate greater inclusion and penetration of financial services to mass market. Currently, almost all the portals accept mobile money as a preferred payment method. As of 2014, online shopping transactions accounted for BDT 200 crore and it has been growing at a rate of 30% every month (The Daily Star, 2014).

This rising and rapid innovation and transaction rate as well as massive mass population inclusion MFS clearly indicates that expectations and roles of stakeholders in mobile banking services of Bangladesh are getting higher and complicated which demands a systematic regulatory guidelines for further innovation and developments.

2. Stakeholders and their expectations in Mobile financial services.

The mobile financial services industry has been growing importance in every sector. The recent innovation in mobile technologies and awareness among mass population’s involvement become the reasons for many interested parties with it. Mobile financial services are fulfilling their immense potential by enabling transfers and gearing financial inclusion globally.

Stakeholders are as follows

- Consumers

- Merchants

- Mobile Network operators

- Mobile device manufacturers

- Financial institutions and banks

- Software and technology providers

- Government

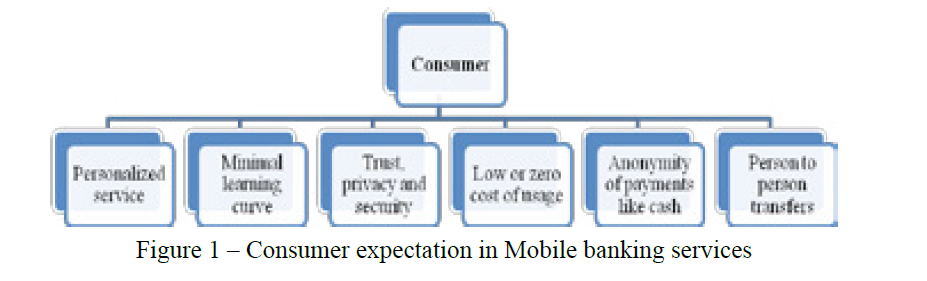

2.1 Consumers.

The reasons for providing Mobile Banking Service is that every individual is very busy at present world and so the clients of banks. For this reason banks are always eager to introduce such services which saves time and money of the clients, can reply immediately, can make customers happy or satisfied. These are the fundamental reasons which trigger the banks to introduce mobile financial serves. Following are the major expectation of customers of using and adopting mobile banking services:

Figure 1 – Consumer expectation in Mobile banking services

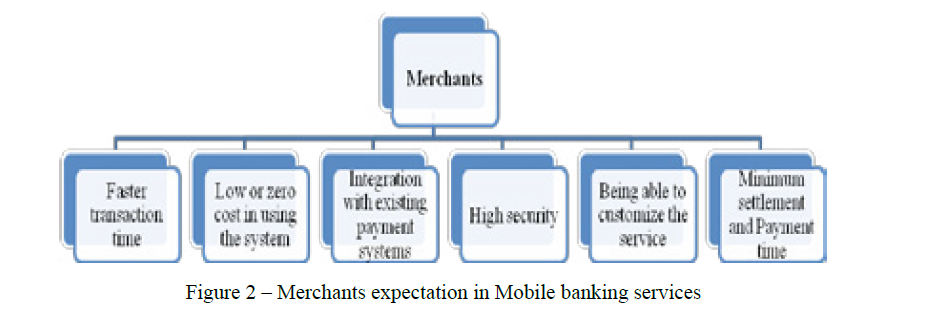

2.2 Merchants

Merchant being the party dealing with the customer interaction level play important role to widening the services. The more the merchants agreeing and promoting the mobile banking services the more the adoption and enrichment this sector can show. Merchants do have few expectations which include fast transaction time, low or zero cost in using and setting up the system, high security etc.

Figure 2 – Merchants expectation in Mobile banking services

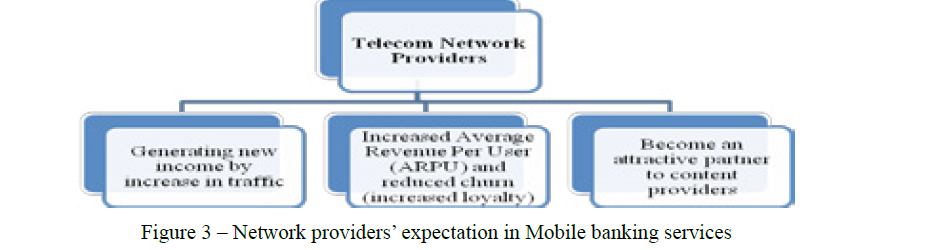

2.3 Telecom Network Providers

Telecom Network Providers are also has expectation form the industry, the main and for most expectation involve generating income and increase in traffic as well as partnering to the content providers which ensure sustainable income flow and customer loyalty.

Figure 3 – Network providers’ expectation in Mobile banking services

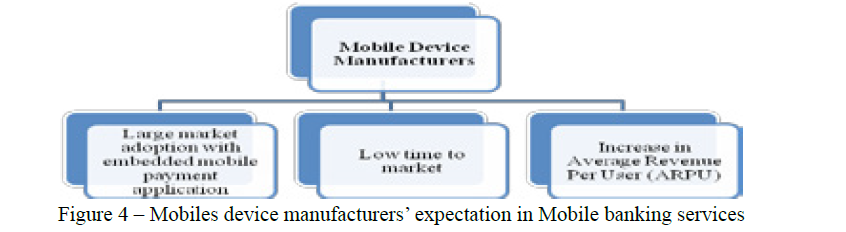

2.4 Mobile Device Manufacturers

Mobile communication technologies going through rapid changes starting from service through SMS to instant application responding. In the past, the customer’s usage of a mobile communication device was restricted by the device’s capabilities. Large market adoption with embedded mobile payment application is a vital expectation by manufacturer. Low time to adoption in market and increase in average revenue per user assures the manufacturer profitability and stability. Following are the major expectations of mobile device manufacturers from the mobile financial service sector:

Figure 4 – Mobiles device manufacturers’ expectation in Mobile banking services

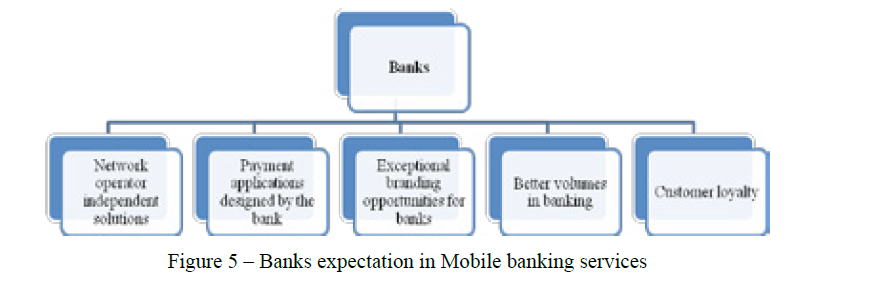

2.5 Banks

Each and every bank and customer wants to reduce his cost. Researchers have found that operating expense of the banks has been increased so they are taking extra fee to cover the cost but the fee structure is very much reasonable.83.33% banks are charging less than 1,000 taka per year. Only Trust Bank could not tell its fee because it depends on some factors. Simultaneously previous studies has found the customer number of the selected banks has been increased due to inauguration of mobile banking service although the service is very new in the market and they still cannot provide all types of services.

Figure 5 – Banks expectation in Mobile banking services

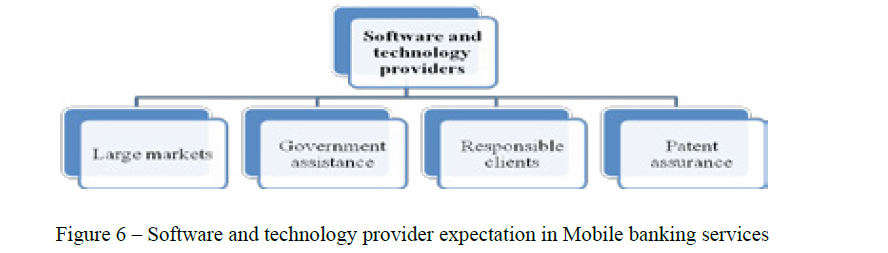

2.6 Software and technology providers

In most instances the mobile Software and technology providers (mobile banking vendor) has been the pioneer in shaping industry adoption and lobbying the other stakeholders on the value of extending the banking franchise to mobile. These initial visionaries have persisted in lobbying the banking industry over this time with little success, and where implemented, little consumer adoption yet in recent time it’s been the major influencer and security manager for banks as well as for consumers.

Figure 6 – Software and technology provider expectation in Mobile banking services

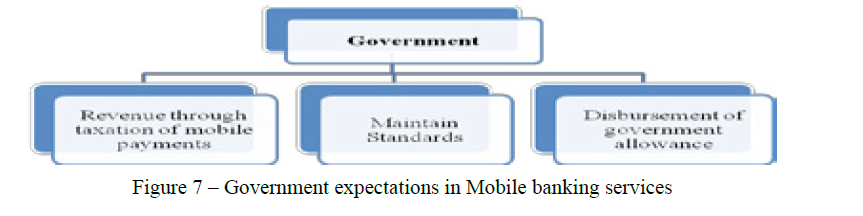

2.7 Government

Government being responsible in all aspect to monitor and maintain the guide line, it itself expect few important aspects from the mobile banking industry. Revenue through taxation of mobile payments, maintain Standards in mobile banking industry, disbursement of government allowance to rural and urban population are few of them.

Figure 7 – Government expectations in Mobile banking services

3. Growth and importance of Mobile Phone Network Operating Companies in Bangladesh

Mobile Phone Operator that can be used for Mobile Banking in Bangladesh are consist of six mobile phone operators, they are: Grameen Phone, Robi, Banglalink, Citycell, Airtel, Teletalk. Different banks use different operators but recent update showing most banks using multiple or most operator’s service simultaneously for providing instant and customer friendly services. Following table shows the significant growth in mobile phone subscribers and a potential customers growth in mobile financial services.

Table 1 – Mobile phone Subscribers in Bangladesh

|

OPERATOR |

SUBSCRIBER (IN MILLIONS) |

|

Grameen Phone Ltd. (GP) |

56.132 |

|

Banglalink Digital Communications Limited |

31.96 |

|

Robi Axiata Limited (Robi) |

27.553 |

|

Airtel Bangladesh Limited (Airtel) |

10.351 |

|

Pacific Bangladesh Telecom Limited (Citycell) |

0.833 |

|

Teletalk Bangladesh Ltd. (Teletalk) |

4.257 |

|

Total |

131.085 |

|

Note – BTCL, Mobile phone Subscribers in Bangladesh February, 2016 |

|

Table 2 – Mobile cellular subscriptions in Bangladesh

|

|

Mobile cellular subscriptions (per 100 people) |

Mobile cellular subscriptions |

|

1990 |

0 |

0 |

|

2000 |

0.210751714 |

279000 |

|

2006 |

13.20573922 |

19130983 |

|

2007 |

23.46762823 |

34370000 |

|

2008 |

30.16828408 |

44640000 |

|

2009 |

34.35334451 |

51359315 |

|

2010 |

44.94535882 |

67923887 |

|

2011 |

55.19256723 |

84368700 |

|

2012 |

62.82023906 |

97180000 |

|

2013 |

74.42964608 |

116553076 |

|

2014 |

80.03535051 |

126866091 |

|

Note – World Development Indicators [last update: 05/02/2016] |

||

Internet Subscribers in Bangladesh

The total number of Internet Subscribers has reached 58.317 million at the end of February, 2016.

Table 3 – Internet Subscribers in Bangladesh

|

Operator |

Subscriber (in millions) |

|

Mobile Internet |

55.512 |

|

WiMAX |

0.136 |

|

ISP + PSTN |

2.669 |

|

Total |

58.317 |

|

Note – Internet Subscribers in Bangladesh February, 2016 |

|

The above mentioned figure (table 3) represents the number of Active subscribers only. A subscriber/ connection using the internet during the last Ninety (90) days is considered to be an Active subscriber.

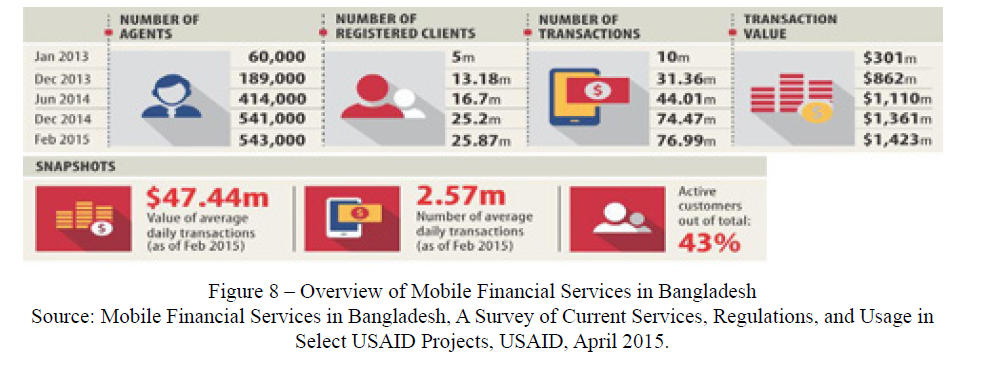

Economic impact of mobile financial services in Bangladesh is easily understood from the following figure:

Figure 8 – Overview of Mobile Financial Services in Bangladesh

Source: Mobile Financial Services in Bangladesh, A Survey of Current Services, Regulations, and Usage in Select USAID Projects, USAID, April 2015.

4. Positive impact of Mobile banking in Bangladesh

Banks, which invest in the mobile banking, can tap into a market that is colossal and to fit the model of m-commerce (Vats and Mohan). It will provide the banks to take services where the customers and their needs lie (Vats and Mohan). Many bank customers are willing to pay extra fee for the utilization of mobile banking.

- Prompt Transaction: Mobile banking has prompted the transactions of banks either national or international level for receiving or paying to customers. Because of the use of quick data transaction facility through electronic system it has reduced time and labour with

- Reducing the stress of customers: The introduction of mobile financing system has bridge the gap between customer and bank. Now it is not necessary to go to any branch of bank close to customer for withdrawing money from the ATM’s With the help of the interbank-switch which are linked with mobile financing systems which safes time energy and reduces stress of the customer. Customers can execute transaction from home with the use of mobile or other electronic devices enabled for financial transition.

- Less use of paper currency: The introductions of the mobile financial services have reduced the use of paper currency that dragging us towards cashless economy. The settlements of financial obligations are now done by the use of electronic gadgets such as computer, mobile, telex, instead of currency notes (Anyanwaokoro, 1997). The more use of these mobile financial transactions actually reduced use and transfer of paper currency as reported by central banks.

- Helping the law and order situation: The use of electronic payment system has reduced the rate of theft and hijacking in the Recent studies in Bangladesh shows similar improvement in road hijack and street robbery has less been reported compare to other crimes. That proves that virtual money transfer (online or mobile) can be one important reason for this improvement.

- Growth of Entrepreneurship and E-Commerce: The development of payment system through mobile and online banking channels made it easy for young and innovative entrepreneurs to set up online base small It not only make it affordable for the entrepreneurs but also wide reachable to most customer segments with the help of Facebook and Google Plus, two most widely used social media, that ensures stronger economic condition of the country as well as reduce the unemployment rates.

5. Challenges ahead

This system is not free from drawbacks. The followings are the current or future challenges ahead for mobile financial services:

5.1 Power Failure and Broken Communication Links

Constant power failure leads to deficiencies in infrastructures such as system computers and mobile networks which stops, slows down the rate of electronic transactions as well as failure links to main control systems and inter-banks getaways. Uninterrupted power system can solve this issue easily.

5.2 Lack of Computer Backup

Lack of computer data backup may result in significant loss of important information relating to customer and the bank which will cause serious misappropriation of customers account. Banks should use secured system to backup data and mobile banking service users are also ensured advanced encryption technology to prevent unauthorized access of information.

5.3 Lack of investment in information technology

Banks should invest to avail new and advanced information technologies to compete in the digital era. Updated technologies should be used to cope with international banking system. Advancement needed in transferring fund through mobile financial services of banks for providing the benefit of authorized fund transfer in home and aboard.

5.4 Capabilities of Clients

While introducing mobile banking services, having cell phones and access to networks is not enough only to start mobile banking. There is a greater challenge lay capabilities of the customer. Mobile financial service providers should train people to use the technology for banking purposes.

5.5 Lack of public confidence

Building customers trust in mobile banking is very much important now. Customers may adept technological aspects of operating a mobile device but in conducting financial transactions through the device they may not have enough trust as they are not doing physical transaction of money.

5.6 Lack of transaction charge

The charge for transaction imposed for mobile banking transaction is very high for general public. It may cause lack of interest in using mobile financial services. The mobile banking service provider should take care about charges of transferring fund and availing services.

5.7 Increase excessive Withdrawal

Mobile banking services has made it easy for customer to withdraw money, shop and transfer fund so the rate of withdrawals also increased which results less savings and lack of capital formation of the economy.

6. Conclusion

The growth and mass distribution of mobile phone adoption open up the horizon to implement some of the highly innovative tools for increasing the standard of living, mobile financial services is one of them. To control and monitor its distribution and effective use it is required to set up some useful guidelines that match the expectations and roles of its different stakeholders. Bangladesh been focusing its mobile financial services towards digitalization and widespread development (Yamin, A., 2017) its effectiveness and efficiency should be assured with proper setup and maintenance of guidelines.