Purpose – This paper directed to consider the objective reasons that underpin the necessity to introduce new approaches towards the regulation of financial and banking sector in the Republic of Kazakhstan.

Methodology – The study employs such scientific research methods as analysis, observation, comparison, abstraction techniques, as well as induction and deduction methods.

Originality / value – The study shows that based on the experience of foreign countries and compare the degree of monetization and capital base with the indicators in Kazakhstan, it is possible to infer that there is a strong necessity to develop new mechanisms to saturate the national economy with financial resources and to develop the corresponding directions to regulate the financial and banking sector.

Findings – The study presents the indicators of the monetization of the economy of Kazakhstan based on the analysis of M2 and M3 monetary aggregates growth rates and inlfation. The results are indicative of the absence of any relationship between money supply and inflationary processes for the period between 2006 and 2015. Further, the necessity to create new mechanisms of regulation of the financial and banking sector is justified.

Introduction. In recent years, due to the economic crisis the issue of financial regulation has become a subject of strong debates. Different alternative points of view with respect to the existing practice have emerged, and there are arguments in favour of each of them. One of the perspectives states that there is a necessity to develop the mechanism of national money, and hence to revise the existing approaches towards financial regulation in the country. The coefficient of an economy’s monetization (the degree of monetization) is measured as the ratio of broad money to GDP. The term "broad money" comprises M2 monetary aggregate and central (national) banks’ foreign exchange deposits denominated in hard currency. In some cases, the coefficient of an economy’s monetization is estimated – using a simplified method – as a ratio of M2 to GDP. This indicator shows the volume of real monetary supply in a country for a given year. The degree of monetization determines the ability of a country to borrow funds in internal financial market, as well as to implement the social support programs and to solve the tasks associated with economy and development.

Main part. The term "degree of monetization" is not commonly used by Western economists, and the research on the impact of a ratio of money supply to GDP on economic development is limited as well. The reason is that the majority of Western economic classics agree on the following: the coefficient V should be constant in the following equation:

MV = PQ (1)

where M – is money supply,

V – is the velocity of money circulation in economy, P – is the set of current prices on goods and services,

Q – is the quantity of assets, goods and services produced during the year [1, 2].

Many famous scholars precede with this assumption, in particular Keynes, Marshall, and Locke [3, 4].

However, the fact that the velocity of money circulation indeed changes due to current circumstances is quite obvious. Economy is not based solely on mathematics; it is affected by human behavior as well. One can observe it even at household level; when the economy is prosperous, people are more willing to spend their money, whereas in crisis periods people are less confident in the future and tend to consider carefully their expenses. If it is true with respect to households, it is fair for business as well [5, 6].

In addition, it is important to note that non-cash money is issued not only by central banks. First of all, it is issued by commercial banks and other financial organizations. Regulators try to control the growth of money multiplier using various measures. However, it is still high. Moreover, the more developed the financial system in a country, the more loans are provided; the more derivative instruments are used, the larger the money supply. And if lending collapses for whatever reason, it leads to quite rapid contraction of money supply as old loans are repaid and in particular bad debts are written off. Further, the lack of money leads to the situation when counterparties fail to fulfill their obligations on payment for delivered goods and services. The counterparties who have not received the payment in turn cannot pay to the supplier, employees, and etc. [7, 8]. Eventually, the velocity of money decreases. And state authorities have to control this.

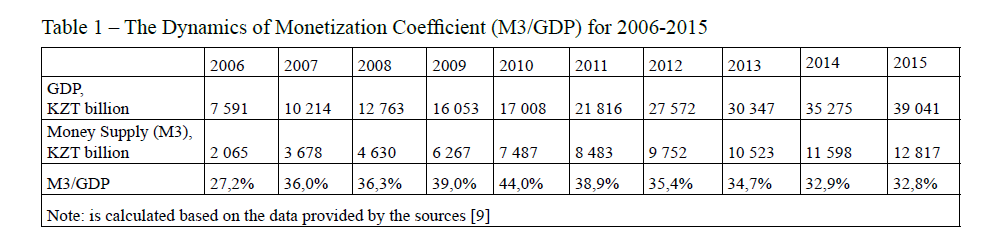

Table 1 – The Dynamics of Monetization Coefficient (M3/GDP) for 2006-2015

The coefficient of monetization of Kazakhstan economy in 2007-2008 was 37-39%, however as a result of devaluation conducted in February 2009, the coefficient increased to 44%. The growth is associated with the fact that the share of foreign currency component in money supply is large (M3 monetary aggregate is used in calculations); hence after the devaluation the national value of the foreign currency component has increased significantly. Starting from 2010, one can observe a downward tendency in the dynamics of the coefficient. In particular, for the last five years the degree of monetization has decreased from 44% in 2009 to 32.8% by the end of 2014.

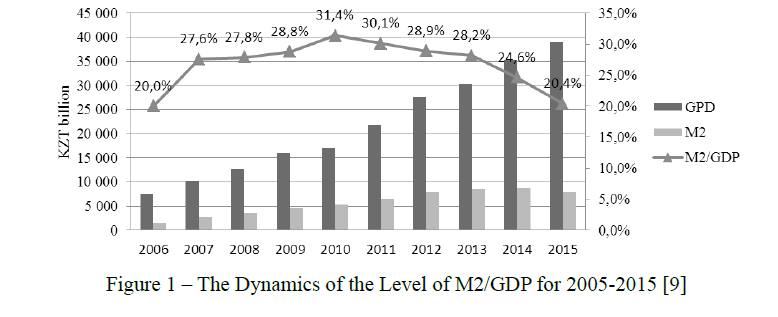

Figure 1 – The Dynamics of the Level of M2/GDP for 2005-2015 [9]

The situation is complicated due to the use of M3 monetary aggregate for calculating the coefficient of monetization. However, it is more appropriate to apply M2, since everything excluded from M2 is included in M3 – it is currency, to be more specific deposits of individuals and legal entities in USD, EUR and etc. Figure 1 represents the dynamics of the level of M2/GDP for 2005-2015, thus the coefficient of KZT monetization is even lower and is about 20%.

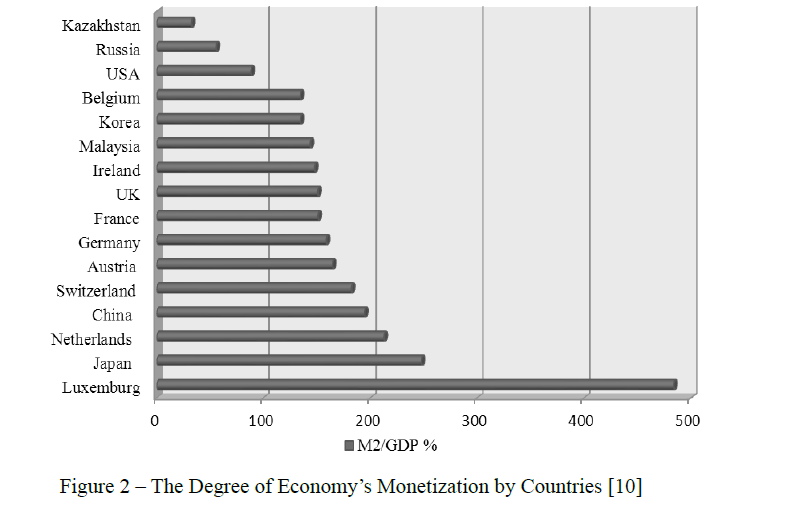

Figure 2 – The Degree of Economy’s Monetization by Countries [10]

To understand whether the indicator in Kazakhstan is high or low, one should compare it with the indicators in other countries, in particular those that serve as an example for us to borrow the experience, economic models and reforms. In this way, the coefficient of monetization in the countries of Eastern Europe constitutes about 60-80%, in Western Europe and USA it ranges between 120-140%, while in China and Japan it amounts 250-300% (Figure 2). It means that Kazakhstan is seriously lagging behind other countries.

In particular, the level of inflation in the USA is less than 2% under the largest currency issuance. It appears that one of the reasons for that is safekeeping of the US banks’ excess reserves in the Federal Reserve. At the end of 2007, the Fed’s reserves constitute about $4.8 billion. By May 2013, the reserves have grown almost 400 times and reach $1.9 trillion (Figure 3, 4). At the same time, the monetary base increases by 3.6 times only – from $846 billion to $3.1 trillion) [12, 13].

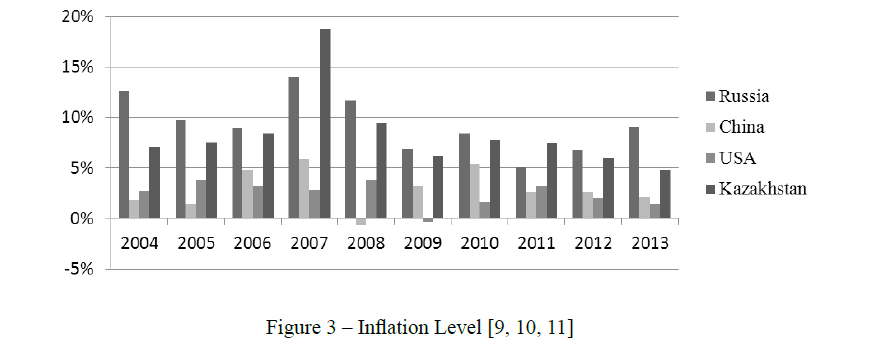

Figure 3 – Inflation Level [9, 10, 11]

In other words, there has been a large-scale "self-sterilization" of financial resources by the US banks. The policy of the leading US banks on the formation of large cash reserves also contributes to this. The above mentioned actions prevent the flow of newly-issued dollars in the economy and slow down the multiplier effect that convert the monetary base into the corresponding monetary aggregate (in October 2008 the Federal Reserve set the payment on the banks’ reserve requirements placed with it – currently the rate amounts 0.25%).

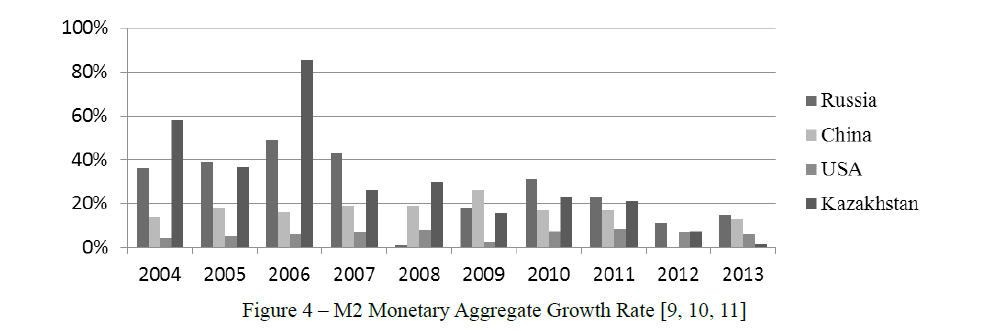

Figure 4 – M2 Monetary Aggregate Growth Rate [9, 10, 11]

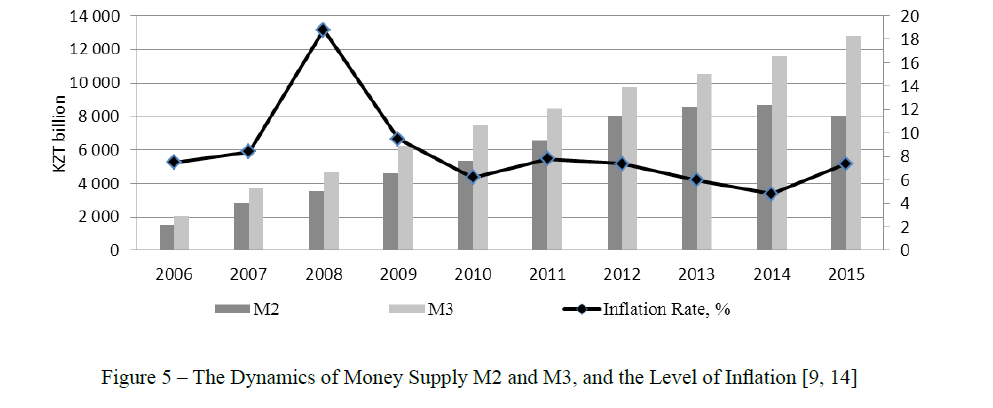

Over the last ten years, one can observe a stable trend, under which the increase of money in the economy does not lead to a similar rise in the inflation rate (Figure 5).

Figure 5 – The Dynamics of Money Supply M2 and M3, and the Level of Inflation [9, 14]

It seems that the additional liquidity growth should cause the prices to go up as well. However, it does not happen in our case, and it does not happen for a long period of time. The highest annual inflation rate in Kazakhstan of 18.8% is observed in 2007. The sharp increase in inflation, however, is accompanied by a moderate growth of money supply. The growth of money supply in 2007 amounts 26.6% (in 2006 – 85.6%). The monetary base for 2007 shrinks by 2.5% (for 2006 – increases by 126.5%). The main factors that determine the dynamics of inflation in 2007 include the external factor that has a character of shock, the growth of aggregate demand, low labor productivity, rise in prices in real economy.

As a result of such "monetary shock", non-payments, barter, money substitutes and other quasi-money emerge in the economy to compensate for arising distortions. Obviously, inflationary consequences of money growth are limited in such conditions. "Monetary contraction" ultimately leads to the reduction of banks’ capitalization and monetization of the economy as a whole. Though, the indicators have increased in recent years, they are still quite low and might significantly restrict the economic growth opportunities.

The depth of decline of the real value of M2 in Kazakhstan highlights the presence of another dimension of the studied issue, which is a geopolitical dimension. If we assume, for instance, that the main channels of liquidity replenishment in our country are some foreign sources, it might signal serious risks: foreign resources will constitute the critical share in money supply, and the owners of these resources ultimately define the priorities and the character of the economic development of the country.

Conclusions. It is important to emphasize that the low capital base of the economy does not allow solving efficiently the tasks related to its development. In addition, under post-crisis conditions, when there is a migration of capital that looks for the sphere where it can be applied, the low degree of monetization of Kazakhstan economy does not allow to neutralize effectively the destabilizing effect of hot money inflow. As a result, this risk becomes more prominent. Under the conditions of excessive global liquidity, even IMF despite its conventional liberal approaches in the sphere of capital movement has been forced to admit that the introduction of measures on capital movement management might appear to be useful in order to protect the stability of financial system. Long before the crisis, a famous economist and IMF functionary M. Mussa argue that high degree of openness to international capital movements, in particular to those that are short-term, might be dangerous for undercapitalized and inadequately regulated financial systems [15].

Taking into consideration the emerging risks, a number of developing countries (in particular, Brazil and South Korea) are introducing the measures that offset the negative impact of speculative inflow of short money. Many countries considerably increase the monetization and capital base, since the more the degree of national economy monetization, the less the degree of its sensitivity to destabilizing effect of hot money. At the same time, the undesired outflow of resources is regulated by the established standards and other measures that make the operations with national currency more attractive.

The issues discussed earlier are extremely important for Kazakhstan economy, since it is concerned with the challenges of sustainable development and minimization of external risks. To meet such challenges, adequate supply of financial resources in the economy is necessary. However, the financial resources should be formed primarily based on the internal sources of monetization rather than external ones under the leading role performed by the national monetary authorities, as it is conducted in mature financial systems. Further, the supply of resources should be targeted, i.e. should response to the economic priorities of the development. At the same time, the inflationary risk should be constrained with low degree of monetization, whereas the capacity of economic growth formed as a result should serve as a base for its development in a long-term perspective. The negative impact of the external environment due to the inflow and outflow of financial resources can be minimized if needed using the measures that regulate the capital movement, tax levers and other special control mechanisms (currency positions, and etc.). Given such a multilevel regulation, it is possible to create the conditions for more effective formation of financial resources necessary to ensure the sustainable growth and development of Kazakhstan economy.

References

- Маршал А. Основы экономической науки. – Пер. с англ. – М.: Эксмо, Антология экономической мысли, 2007. – 832 с.

- Лопатников Л. И. Экономико-математический словарь: Словарь современной экономической науки. – 5-е издание, переработанное и дополненное. – М.: Дело, 2003. – 520 с.

- Ядгаров Я. С. История экономических учений: учебник. – 4-е изд., перераб. и доп. – М.: ИНФРА-М, – 480 с.

- Кейнс Д. М. Общая теория занятости, процента и денег. – М.: Гелиос, АРВ, 1999. – 352 с.

- Самуэльсон П., Барнетт У. О чем думают экономисты: Беседы с нобелевскими лауреатами. – Пер. с англ. – М.: Альпина Бизнес Букс, – 490 с.

- Абдуразаков Т. К. Исследование взаимосвязи темпов роста денежных агрегатов и объема ВВП// Финансы и кредит. – 2009. – № 5 (341). – С. 46-64.

- Малкина М. Ю. Уровень монетизации, структура денежной массы и качество денег в экономике (сравнительный анализ положения в России и зарубежных странах) // Финансы и кредит. – 2010. – № 30 (414). – С. 2-10.

- Садков В. Г. О целевых ориентирах уровней монетизации экономики и инфляции с позиции конечных результатов развития общества // Общество и экономика. – 2008. – № 5. – С. 3-22.

- Официальный сайт Национального банка Республики Казахстан [Электрон. ресурс]. – URL: http://nationalbank.kz (дата обращения: 01.2016)

- The World Indicator [Электрон. ресурс]. – URL: http://data.world (дата обращения: 20.01.2016)

- «Региональный Центр Инновационных Технологий». Сравнительная статистика денежной массы (М0, М2) и ВВП в России и Китае [Электрон. ресурс]. – URL: http://www.rcit.su/inform-dm.html (дата обращения: 01.2016)

- Ершов М. Пять лет после масштабной фазы кризиса: насколько стабильна ситуация? // Вопросы экономики. – 2013. – № 12. – С. 29-47.

- Сандоян Э. М. Неинфляционная монетизация экономики как фактор экономического развития // Вестник Нижегородского университета им. Н. И. Лобачевского. – 2008. – № 5. – С. 178-181.

- Официальный сайт Комитета по статистике Республики Казахстан [Электрон. ресурс]. – URL: http://www.stat.gov.kz (дата обращения: 09.2015)

- The liberalization and management of capital flows: an institutional IMF. – 2012. – November, 14. – p. 18.