Searching of the effective organization and management accounting development are becoming increasingly important in modern conditions of Kazakhstan, and all around the world. That is why, the development and improvement methods of planning, analysis and costs control and benefits issues are the main in the system of management accounting.

It is began to use operation management or cost management with the help of the management of individual transactions or individual activities in recent times by major companies of costs and profits control. The operations, which make up the individual activities, are performing intermediate object of calculation and overhead costs are the main object of accounting and analysis. Then, the AB-costing system has been introduced as the result of it.

The AB-costing system (Activity-based costing) is one of the modern systems of cost accounting and total cost calculation, which meets the conditions of modern organizations with a highly developed industrial production and wide assortment of products and high level of indirect costs. The system has been developed in the 80 years of the 20th century in R.Kuper and R.Kaplan writings who spoke critically of the traditional allocation of overhead costs, significantly distorting the real cost of organizations products. The AB-costing system allocates indirect overhead costs more accurately [1].

« The АВ-costing» process-oriented cost management is a useful concept that can be used in order to correct deficiencies overly generalized cost accounting systems of the past time. In «The АВ-costing» calculation system is based on another approach to the formation of the cost production in companies with a high relative share of indirect costs.

AB-costing – is a progressive concept that can overcome the limitations of traditional cost accounting system and to set cause – and – effect link between the products and costs to produce it. It follows, that the ABC is a cost accounting system, which consists of costs objects determining, cost classification and method of the objects distribution.

The AB-costing main areas of use:

- -in confirmation of the cost calculation of cost objects and according to this, prices establishment;

- -in costs budgeting and monitoring by activity, departments, divisions, units, etc.;

- -the information base for benchmarking activities and reengineering of business processes on the basis of its results;

- -the information base for outsourcing decision-making (one of the engineering types), and other decisions.

The purpose of the AB-costing method – is to achieve the accuracy of the results of product cost calculation and cost management.

Application areas of the system – any enterprise. However, diversified enterprises and economic complex systems, with a high proportion of indirect costs in the cost structure would have the most effective use of the АВ-costing method.

According to the relationship of activity types with a behavior of costs, the AB-costing system can distinguish:

- Activities defined by the number of units of production (unit-level activities), in other words, direct variable costs of companies: the direct costs of materials and direct labor

- Activities, determined by the manufactured products number of batches (batch-level activities). Generally, such activities are serving departments of companies: installation of equipment, material transport, quality control,

- Activities, defined by the concrete manufactured products (product-level activities). It can be design development, marketing research, promotions and

- Activities, defined by the number of production facilities (facility-level activities). This activity is related to the company generally: security, utilities, depreciation of fixed assets, etc. The majority of these costs is related to fixed or quasi-fixed costs and is not related to specific products [2].

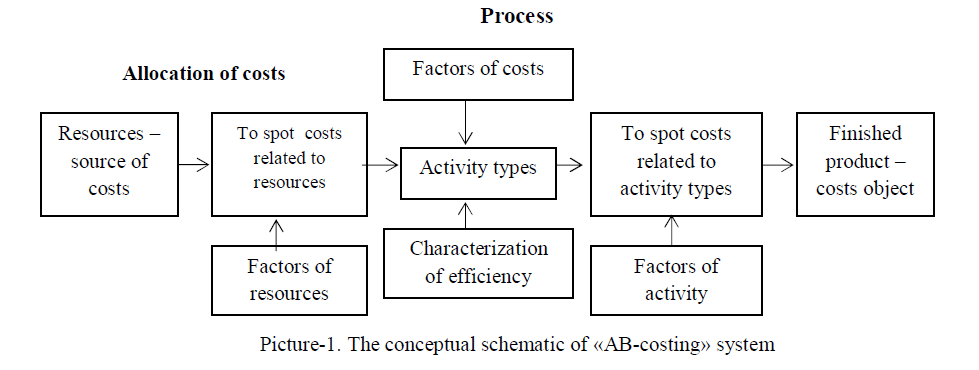

The AB-costing system use can be distinguished for the following steps (1-picture):

- Grouping and distribution of overhead costs by its activity – centers, in enterprises, of functional

- Isolation of factors causing overhead costs using and its assignment being the costs carriers.

- Calculation of overhead cost rates distribution to the cost

- Inclusion (absorption) of overhead costs into the cost of products by the distribution of calculated

Picture-1. The conceptual schematic of «АВ-costing» system tasks:

AB-costing method of the product or service cost calculating is meant for the following

-The cost price of the product on the different stages of product life rhythm, which is meant

for the calculation and analysis of the unit cost from the time of its development until the phase-out.

- -The costs of the value degrees, which is meant to analyze the cost of the product, not only inside but also outside the company, including to the general structure of the suppliers, dealers and consumers costs.

- -Functionally-cost analysis. It includes analysis of the product design elements.

- -Costs for the design, which help to answer the question: how does the design influence on the life rhythm and value degrees of product manufacturing? What is the impact of changes of product consumer properties to its cost?

- -Operation analysis of costs. It includes calculation of costs for the implementation of individual technological operations.

- -Cost accounting according to the activity reveals drivers of indirect production, marketing and administrative costs. Its main aim – to assess the need in certain activities for the production and marketing of the product, the assessment of the resources, which are need to carry activities out [3].

Advantages of this system are different from other calculating systems of the product (works, services) such as:

- -Precise determination of operating costs, the ability to eliminate the overhead costs;

- -An effective management mechanism for cost and profit, as it can determine the "contribution" of each product, each customer, and each area to the total financial result;

- -Control of the costs volume, but also the reasons for its occurrence;

- -The establishment of cause – and – effect relationship between costs and products;

- -Strengthening of the administrative control over all activities of the company;

- -Ability to use AB-costing information for long-term management decision making.

- -Possibility to use effective pricing and marketing policies as the tool of development.

Also, this list may be added by the significantly cutting costs of AB-costing system implementing in recent years, which allows to use it not only by major but also medium-sized enterprises having a high share of indirect costs.

However, the AB-costing using, there are disadvantages are related to its implementation and application: labor intensity, complexity, and a limited number of companies. Therefore, it is recommended to use this system only for companies with a high share of indirect costs.

Therefore, after analyzing the features and characteristics of the AB-costing system, it has been found that it is a powerful management mechanism, which has become to overcome the inefficiencies of traditional ways of accounting and cost management.

It should be noted, that the problems increasing of indirect cost sharing and need in a reliable indicators of production costs for the strategic management decisions led to a leap in the development of management accounting – information for business management based on the cost of operations. «The АВ-costing» method, primary developed to improve the methodology of the traditional calculation, turned into a unique calculation system, that provides a wide range of management solutions of the product.

The AB-costing method provides:

- -Refined calculation of the actual (or planned) costs of the product unit;

- -Generation of the information about non-traditional objects cost, as a consequence, is used to justify various strategic management decisions, makes a different way of costs analysis and helps to identify ways to reduce them;

- -Using to evaluate and improve its activity;

- -Improvement of products, technological processes;

- -Business process reengineering.

The cost accounting system can be applied in major industrial companies that meet the following criteria:

- -A complete range of products;

- -A high relative share of overhead costs;

- -A significant diversity of overhead costs;

- -The complexity of the processes of production;

- -The lack of a direct relationship between the level of overheads and the volume of company activity;

- -A number of branches.

Prospects of «The АВ-costing» system development associated with its using for the responsibility centers evaluation, as well as an information basis for the products and processes development. Moreover, the possibilities of modern information systems make it possible to account more effectively.

Thus, the AB-costing system helps not only to determine the costs of products, processes and types of operations, but also provides financial and non-financial information needed to identify opportunities to reduce costs and improve functioning. This system – one of the most important way, to succeed and grow of any company.

Literature:

- Аverchev I.V. Management accounting and recording. Realization and baptism. -М.: Vanity press «Vershina», 2006. -

- Blatkov N.A. Basics of industrial accounting and calculation.-М.:Finance, 2007.-198p.

- Kiselyev A. Perspectives of baptism ABC system in russian companies.// Management accounting. 2007. № 5. - 18-24p.