This article examines the content of the system of bank lending. In the process of analyzing the current state of bank crediting the special attention is paid to the central problems faced by banks and borrowers, including the high credit risks, lack of long-term credit resources, low availability of the credits for enterprises of the real sector of economy, etc. Limiting the credit risk is considered as the main condition for ensuring credit repayment. Calculation of the credit limit is based on determining the borrower's credit rating using a system of quantitative and qualitative indicators of its activities, taking into account industry and regional characteristics. The proposed method of calculating the credit limit consists of three consecutive stages: evaluation of the creditworthiness of the borrower - is realized by calculation of values of financial indicators by the commercial bank using the data of financial statements of the borrower, comparison of them with normative values and assigning the creditworthiness class to the borrower according to values calculated; definition of credit rating on the basis of estimation of qualitative characteristics of the borrower; calculation of the credit limit with the use of discount rates.

Currently, the banking sector is one of the most developed and significant segments of the financial market of the Republic of Kazakhstan in terms of the volumes, the spectrum and the quality of rendered services. Its leading role in financial support of economic development of Kazakhstan is caused, first of all, by availability of resource potential. At the same time, one of the main factors to raise the competitiveness of the domestic economy is the large-scale increase in loans and investments in the real sector, which requires a comprehensive reorientation of the credit resources of the banking system to the solution of the tasks of sustainable and long-term economic growth of Kazakhstan.

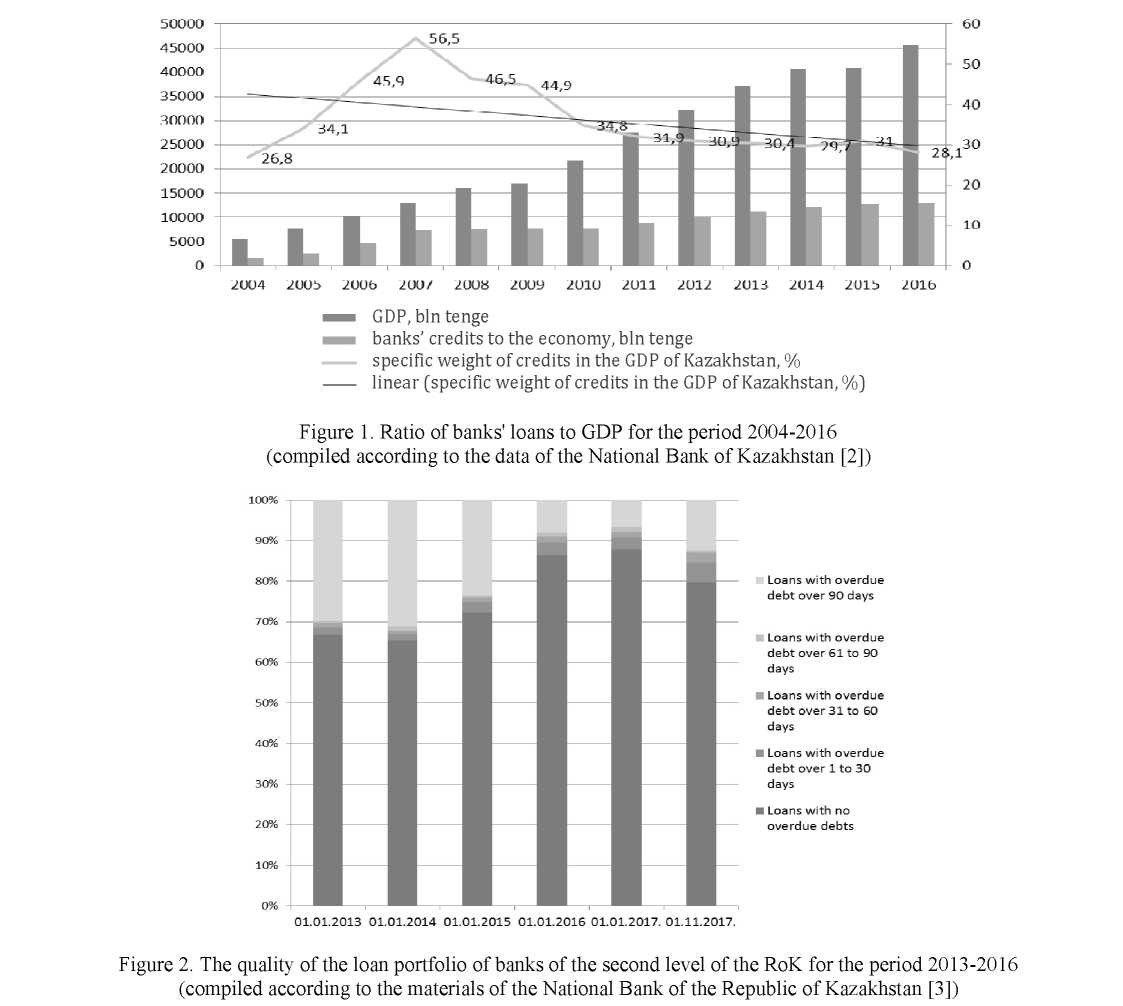

However, the credit relations between the banks of the second level in Kazakhstan and economic entities are characterized by insufficient use of credit opportunities. Thus, the ratio of bank loans to GDP at the end of 2016 was less than 30 % (Fig. 1).

The tendency to decrease the share of bank loans in GDP has been observed since 2008. This situation has been influenced by certain factors and causes, both micro and macroeconomic. The growth of the credit risks and reduction of banks' capacity to minimize them led to the reduction of the loan offer.

At the same time, the investment opportunities of Kazakhstan's banks are rather modest. In the structure of the bank loans, the share of long-term loans granted for the acquisition of fixed assets was 1180.5 bln tenge at the end of 2016 (or 9.2 % of the total amount of bank loans). The share of bank loans in financing of the investments in the fixed assets in 2016 was only 5.8 % [1].

In turn, the dynamics of lending to the economy was adversely affected by the high level of nonperforming loans in the banking sector. The presence of problematic loans in the loan portfolio reduces the credit potential of banks, forcing banks to divert significant funds for the formation of provisions and tighten

the terms of lending. The share of loans with overdue payments over 90 days was more than 13 % of the loan portfolio of Kazakhstan's banks at the beginning of 2015 (Fig. 2). At the same time, the share of three branches (construction, trade, non-productive sphere) accounted for more than 70 % of the corporate sector's non-performing loans. More than 60 % of the entire portfolio of non-performing loans was loans in foreign currency.

As a result of the joint work of banks of the second level and the National Bank of the Republic of Kazakhstan there was a reduction of problematic loans in the loan portfolio to 6.7 % in 2016.

In comparison with the developed countries, where the specified share is 20-30 %, it is possible to conclude that in Kazakhstan the participation of the banking sector in financing of investments is very insignificant. On average, the share of bank crediting for the period 2008-2016 accounted for 4-5 % of the total investment in the fixed assets. The possibility of financing the investments is limited by the scarcity of longterm resources of banks.

In accordance with the Forecast of the socio-economic development of the Republic of Kazakhstan for 2017-2021, the volume of the bank crediting by the year 2021 should grow up to 16397 bln tenge, while the average annual growth rate of crediting by banks of the second level in the period 2017-2021 should make 4.7 % [4].

It should be noted that during the last 8 years the maximum growth rate of bank loans was achieved in 2011 (16.1 %). According to the results of 2016, the growth decreased by 1.5 %.

In order to increase the rate of bank crediting to the economy, a number of state programs are implemented, providing various tools for supporting and stimulating financial support for enterprises of the real sector of the economy through banks of the second level of the RoK. The desire of the state to ensure the availability of credit has become realized through the state guarantees, subsidized interest rates, allocation of funds for the provision of targeted loans for small and medium-sized businesses and other tools.

For its part, the National Bank of the Republic of Kazakhstan intends to use certain measures to accelerate the credit activity of the banking sector. One of the priority directions of the monetary policy for 2017 is «... recovery of crediting of the economy through creation of appropriate macroeconomic conditions, stabilization of long-term expectations on inflation and growth of business activity» [5].

In this regard, the National Bank, in order to provide banks with credit resources, is working on the formation of a risk-free yield curve. This measure is aimed at the development of long-term tenge funding at the expense of the institutional investors. At the same time, measures are being developed to stimulate longterm investments and deposits through the regulation of their value, the process of issuing bonds by banks to the domestic market, the mechanism of security of the assets, etc.

With the purpose of formation of the long-term assets in the banking system the system of instruments of the National Bank of Kazakhstan is improved through introduction into the practice of the mechanism of provision of conditional funding (liquidity in exchange for the bank's obligation to reduce the volume of the problem assets, lending to the priority sectors) [6].

Thus, the revival of the real sector of the economy is now connected with the development of the bank crediting. Banks, as major financial intermediaries, mobilize and redistribute financial resources between sectors of the economy. The participation of banks in the turnover of the financial resources contributes to its more efficient functioning, accelerating the process of reviving the economy at a new level. However, the quality of the economy of Kazakhstan as a whole does not meet the criteria under which the processes of investment and credit become sustainable. Moreover, the investment opportunities of the banks of the second level do not meet the needs of the real sector. In this regard, increasing the role of bank crediting is a strategic objective in financial substantiation of Kazakhstan's economic development.

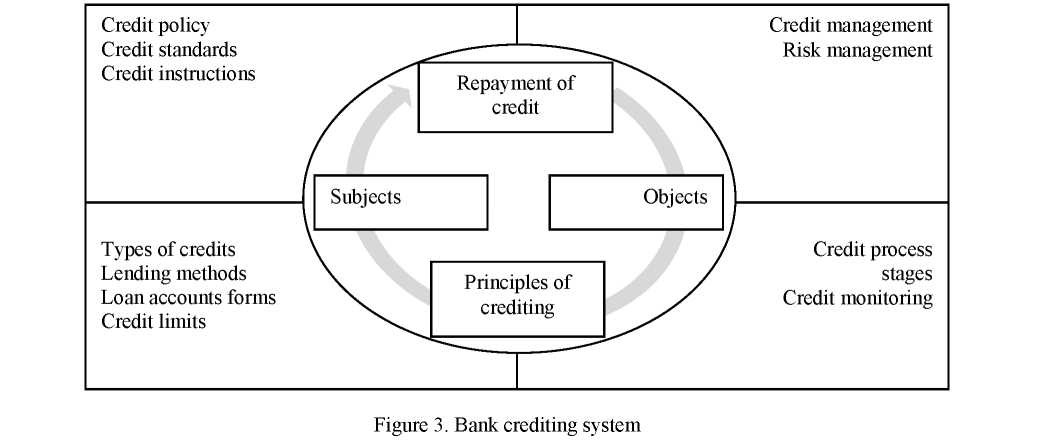

For deeper study of the theoretical aspects of bank crediting it is expedient to consider its content as a system with many interrelated elements.

According to Prof. O.I. Lavrushin, understanding and implementation of the crediting process as a system contributes to increasing the role of bank credit in stimulating the real sector of the economy and improving the credit process management system in order to minimize the credit risks [7; 9].

Indeed, bank crediting as a system covers the entire process of granting and repayment of loans, including the regulation of credit relations.

Bank crediting affects not only the relationship between the lender and the borrower over the transfer of loaned value, but also credit relations on a wide scale. Lending is an important factor in improving the socioeconomic situation and well-being of society by contributing to the improvement of proportions in the economy, creating favorable conditions for the creation of the new enterprises and firms, for the development of various forms of entrepreneurial activity and increasing on this basis the number of jobs.

Regulation of the credit relations lays in their regimentation by legislative and normative acts of the state, the credit policy, and the rules of crediting. Since a credit transaction is accompanied by the development of the economic relations arising from the production process, the legal norms are of special effect: a loan agreement is signed, according to which the creditor and the borrower become the subjects of crediting with obtaining the certain rights and obligations. That is, a special legal relationship is established between the creditor and the borrower, which starts from the moment of credit application submission by the borrower and its approval by the creditor and ends with a full refund of loaned funds. The creditor and the borrower interact with each other as participants of the credit agreement, and the creditor is a subject with free resources and voluntarily lending them to the borrower under certain conditions.

Consequently, there is a certain degree of confidence in credit relations, when the lender trusts, and the borrower takes the obligation to repay the loan in the future. As noted by Prof. O.I. Lavrushin, «... the moral and economic beginnings of trust remain the fundamental basis that is always present in the organization of the credit process. Trust in a credit transaction does not arise under duress, it is a consequence of existence of long-term stable relations between economic agents, and the correct fulfillment of mutual obligations» [8; 50].

The composition of all elements forming the bank crediting system is presented in Figure 3.

The bank crediting system is based on the subjects and objects of credit relations. Subjects are interested in the development of credit relations: a creditor – in receiving the income (reward) from the credit transaction, the borrower – in receiving the profit from the use of the bank loan in its activity. At present, the borrower is given a great opportunity to choose the bank, whose credit services he would like to use. Thus, for the crediting process to occur in the whole variety of conflicting interests of partners, it is necessary to find such a solution that the transaction is advantageous for both parties.

The objects of the bank credit may be the current needs of enterprises in current capital, some of which may be seasonal, and capital costs associated with the acquisition, expansion and renewal of basic production funds, introduction of innovations and modernization of production and technologies, etc. In determining the objects of crediting banks take into account their statutory requirements, the range of customers being served, the goals of their strategic development, the economic situation in the country and other factors.

As can be seen from Figure 3, the principles of crediting are an integral part of the bank crediting system. They should be reflected in the credit policy and have a direct impact on the lending mechanism.

Repayment, as the basic essential characteristic of a credit, distinguishes and allocates it as an economic category. It acts as an essential foundation that combines the principles of crediting. This approach to the study of the importance of crediting principles in the development of credit relations involves understanding of these principles from the position of mandatory repayment of loans issued. In this aspect the maturity and the security act in the new quality of return date and security as a guarantee of credit repayment. In combination all the principles of crediting provide the necessary conditions for the return movement of loaned value.

The credit policy regulates the organization of the bank crediting process. In essence, the credit policy establishes the equilibrium that exists between the level of the credit risk and the perceived income from the credit activity, because on the one hand, the interests of credit policy are influenced by the interest of depositors and shareholders of the bank, and on the other hand, by the need to meet the demand of the clients for monetary resources.

In combination, the credit policy, the credit standards and the credit regulations form an integrated crediting policy.

In turn, the lending mechanism, acting as one of the elements of the crediting system, expresses the technical procedure of the crediting process, beginning with the choice of the type of bank lending, opening of the loan account and a credit line and setting the schedule of the repayment of the loan debt, ending with the procedure of credit monitoring and repayment of the credit with the payment of remuneration.

From the practice of the credit business it is known that the crediting mechanism has many manifestations which can be considered in various aspects. The choice of a credit mechanism is interconnected with the choice of the type of bank lending and depends on the needs and specifics of the borrower's functioning and credit capabilities of a bank as a creditor.

The most important condition of timely and full repayment of credit is the correct organization of credit process by the bank. Availability of guidance and methodological documents regulating credit operations of a bank, development of a clear procedure for consideration and approval of a loan, determination of the requirements for credit documentation, creation of a system of effective control over the validity of the loan and the reality of the sources of its repayment, a good organization of the analytical work in the bank, a high level of information about the clients - all this greatly reduces the likelihood of non-return of bank loans.

Provision of a credit repayment is a complex purposeful activity of the bank, which includes the system of organizational, economic and legal measures, constituting to a special mechanism, determining the ways of providing loans, sources, terms and ways of their redemption, documentation that provides for the repayment of loans.

It should be noted that in order to ensure stability of the second level banks, an effective system of credit repayment management is necessary.

The credit recovery management system includes the principles of crediting, credit policy and credit standards, credit monitoring, mechanisms for reducing problematic loans.

In unity all elements are directed on development of the process of crediting, provision of repayment of all amount of credits, forecasting, overcoming and compensation of losses from non-repayment of credit. In turn, each of these elements as a subsystem, contains a corresponding set of components that specify its contents. Their use in credit activity of the bank depends on the ability of credit specialists to react to the possible negative consequences of credit risk in the bank's activity and to take complex decisions on its minimization.

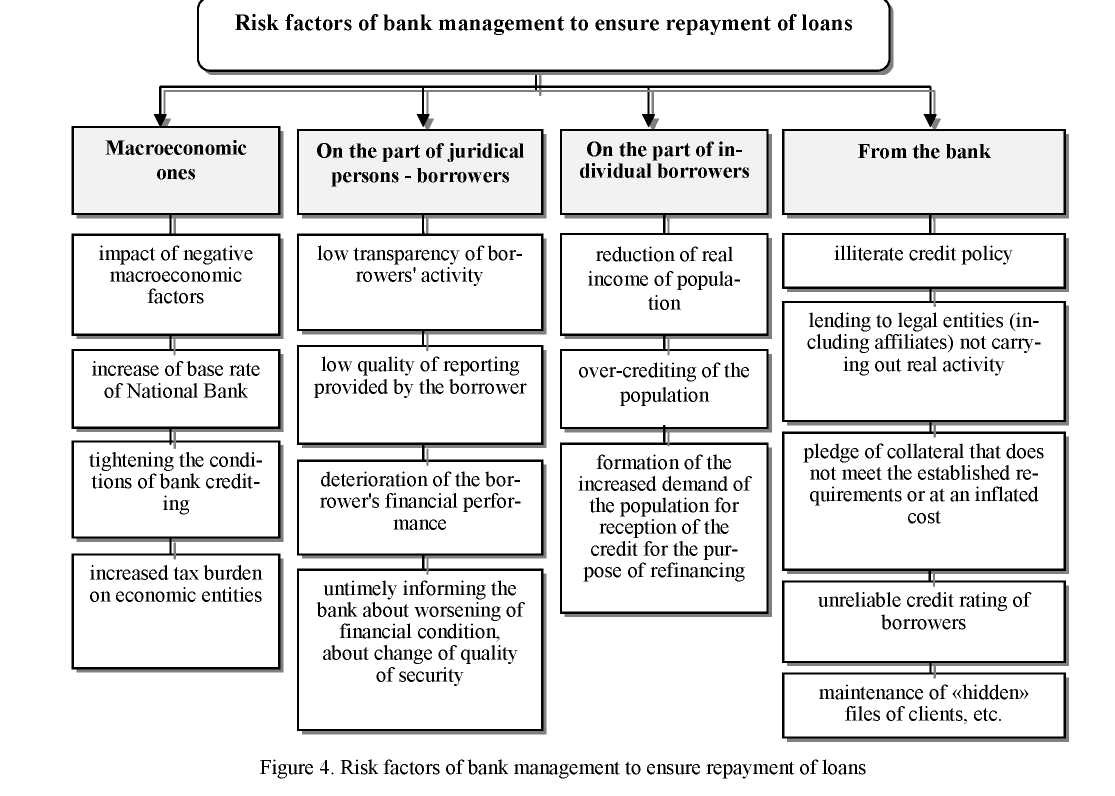

Structural reforms, especially in the area of risk management and management in banks, are needed to reduce the level of overdue loans and improve the quality of the loan portfolio. When issuing loans to their customers, banks need to consider and assess the future risks of the bank related to the financial condition of the client and its business plan in order to minimize the non-return of credits later. A comprehensive risk analysis of credit should take into account the main risks presented in Figure 4.

In the process of forming the optimal structure of the credit portfolio of the bank it is necessary to assess the risks not only of the borrower. but also to include a wider range of assessed factors. for example. assessment of economic situation in the industry. assessment of competitiveness and others.

The interaction of the banking sector and economic actors can be strengthened by a special complex scientific approach to the problem. In this regard. a scientifically-based methodology was developed for calculating the limit of bank crediting based on the borrower's credit rating. and using the system of quantitative and qualitative indicators of its activity.

The proposed method of calculating the credit limit consists of three consecutive stages: Stage I - evaluation of the creditworthiness of the borrower - is realized by calculation of values of financial indicators by the commercial bank using the data of financial statements of the borrower. comparison of them with normative values and assigning the creditworthiness class to the borrower according to values calculated; II stage – definition of credit rating on the basis of estimation of qualitative characteristics of the borrower; Stage III – calculation of the credit limit with the use of discount rates.

For realization of the first stage and for the purpose of more meaningful analysis of clients' ability to repay bank credit the financial analysis coefficients. available in the practice of domestic and foreign credit business were studied.

As a result of conducted researches in the field of methods of analysis of financial condition of the borrower the expediency of use of the system of 8 financial indices. grouped in factors of liquidity. repayment capacity. profitability. business activity is revealed (Table 1).

For the purpose of definition of credit limit of the system of the selected coefficients meets two basic criteria:

– firstly. it reflects the borrower's ability to repay the loan within the specified terms and pay the remuneration;

– secondly. the coefficients calculated on the basis of indicators determine the considerable (significant) peculiarities of the company's activity and duplicate each other to the minimum extent.

In addition. this system of financial indicators is characterized by a relatively simple collection of data necessary for the calculation. which are mainly reflected in the balance sheet and the profit and loss statement of each borrowing company and are included in the list of documents required for the formation of credit documentation.

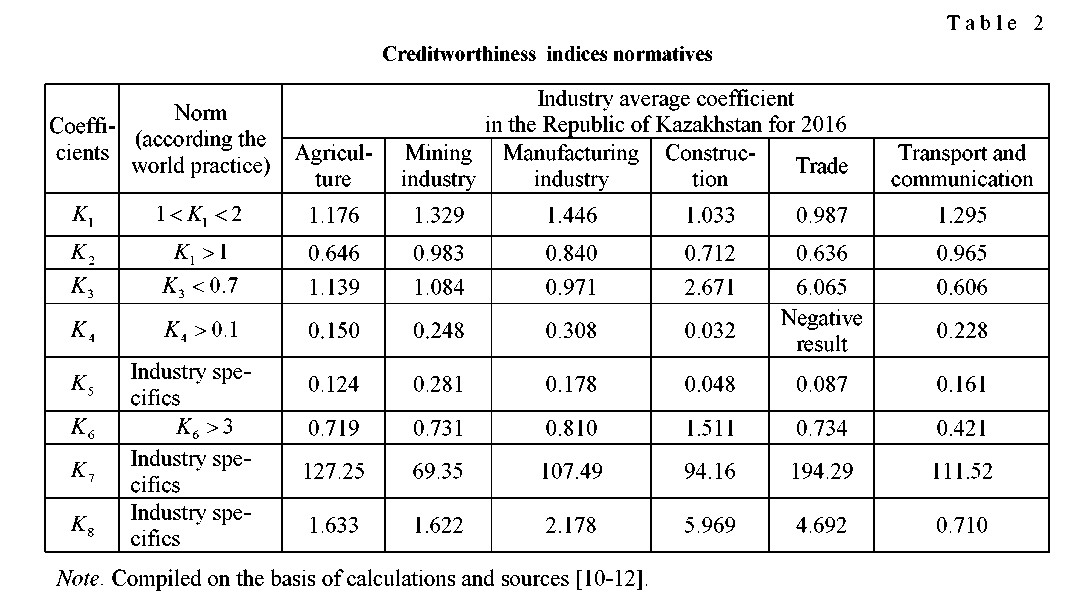

After calculating the credit ratios according to the data of the borrower, the obtained values are compared to the values of the industry average coefficients (Table 2). This approach is determined by the significant influence of specific industry peculiarities on the process of bank lending. In addition, the values of indicators established on the basis of study of economic literature according to the world practice of credit business were used as the recommended values.

When comparing the values of credit ratios calculated according to the borrower's financial statements with the values of the industry average coefficients for each indicator a certain number of points is assigned: the values of coefficients equal to industry average ones are assigned 10 points; above industry average - 15 points; below industry average - 5 points. If the amount of the scores exceeds 105 points, the borrower can be attributed to the 1st class of creditworthiness. If the amount of scores is less than 105 points, but more than 65 points, the borrower can be attributed to the 2nd class of creditworthiness. If the amount of the scores is less than 65 points, the borrower should be attributed to the 3rd class of creditworthiness.

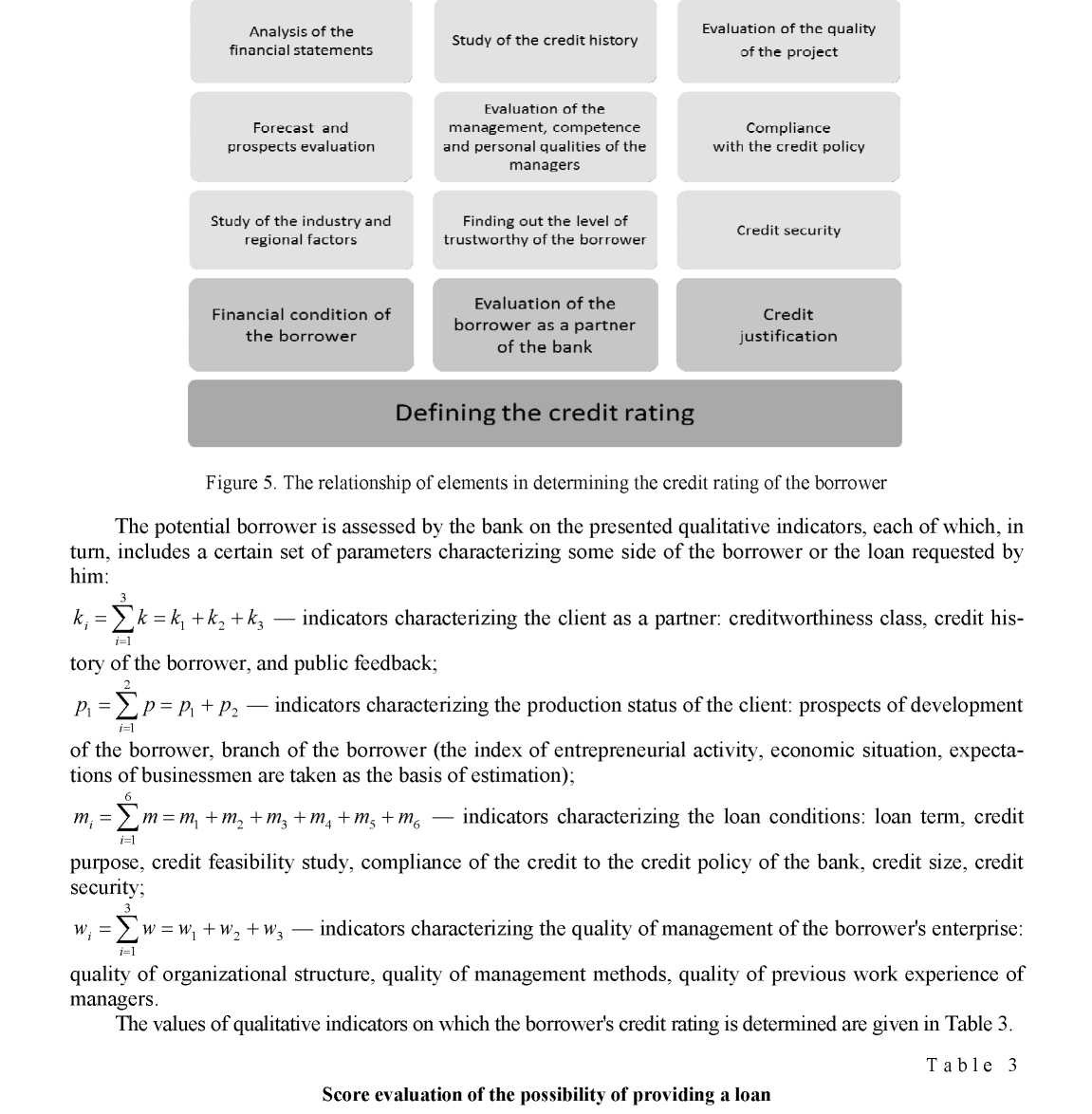

Stage II - Definition of the credit rating. In economic literature credit rating is defined as credit risk assessment and probability of default [13; 155]. In the considered methodology the credit rating is based on the analysis of the quality characteristics of the borrower, that is, it is a measure of the bank's «degree of trust» to the borrower. The credit rating is defined according to the scheme presented in Figure 5.

In Figure 5 the final result is the definition of credit rating of the borrower on the basis of the analysis of qualitative characteristics in three blocks. The first block contains the creditworthiness evaluation of the borrower, where the basic element is the calculated class of creditworthiness. The second block reflects the assessment of the borrower from the standpoint of its reliability and responsibility for fulfilling its obligations. The third block is aimed at studying the acceptability of credit transaction conditions to the bank and compliance with the credit policy provisions.

The calculation of the consolidated credit rating is made by the following formula:

|

Indicator |

Parameter |

Feature |

Number of points |

|

1 |

2 |

3 |

4 |

|

Class of borrower's credit- |

the 1st |

9 |

|

|

worthiness |

the 2nd |

5 |

|

|

the 3rd |

1 |

||

|

k |

Borrower's credit history |

excellent |

6 |

|

good |

5 |

||

|

satisfactory |

4 |

||

|

doesn't exist |

2 |

||

|

bad |

0 |

Note. Compiled according to the source [14; 46].

|

1 |

2 |

3 |

4 |

|

Feed-backs about the bor- |

excellent |

5 |

|

|

rower |

good |

4 |

|

|

are absent |

1 |

||

|

bad |

0 |

||

|

Enterprise development pro- |

dynamically developing |

9 |

|

|

spects |

stable functioning |

5 |

|

|

decline in business activity |

0 |

||

|

p |

Borrower's industry |

industry |

9 |

|

trade |

6 |

||

|

construction |

3 |

||

|

agriculture and other |

2 |

||

|

Loan term |

short |

8 |

|

|

medium |

2 |

||

|

long |

0 |

||

|

Purpose of the loan |

production |

3 |

|

|

non-production |

0 |

||

|

Credit Feasibility Study |

justified |

9 |

|

|

m |

unjustified |

0 |

|

|

Compliance with the bank's |

full |

9 |

|

|

credit policy |

partial |

5 |

|

|

no compliance |

0 |

||

|

Credit size |

acceptable |

3 |

|

|

unacceptable |

0 |

||

|

Credit Security |

secured |

7 |

|

|

unsecured |

0 |

||

|

w |

Company management |

competent |

5 |

|

incompetent |

0 |

||

|

Total |

Inclusion of discount rates in the formula of calculation of the credit limit is explained by the necessity of the real estimation of the existing assets of the enterprise by the bank.

When determining the credit limit as one of the important stages of the bank lending process, it should be borne in mind that the obtained credit limit values are conditional and are of recommendatory nature. They serve as initial information in the provision of credit, allow to accurately calculate the optimal amount of credit, which the borrower can actually return with payment of remuneration, reduce the costs of the procedure for determining the amount of credit, take into account the credit rating of the borrower in determining the volume of credit, and to ensure timely return of bank loans.

References

- Finansovo-khoziaistvennaia deiatelnost predpriiatii v Respublike Kazakhstan za 2016 hod [Financial and economic activity of the enterprises in the Republic of Kazakhstan for 2016]. stat.gov.kz. Retrieved from http://www.stat.gov.kz/ [in Russian].

- Statisticheskie biulleteni Natsionalnoho Banka Respubliki Kazakhstan [Statistical bulletins of the National Bank of the Republic of Kazakhstan]. nationalbank.kz. Retrieved from http://www.nationalbank.kz/cont/Binder12.pdf [in Russian].

- Tekushchee sostoianiie bankovskoho sektora na 01.01.2017 h. [Current status of the banking sector at 01.01.2017]. Retrieved from http://nationalbank.kz/?docid=1065&switch=russian [in Russian].

- Prohnoz sotsialno-ekonomicheskoho razvitiia Respubliki Kazakhstan na 2017-2021 hh., odobrennyi na zasedanii Pravitelstva Respubliki Kazakhstan [Forecast of the social and economic development of the Republic of Kazakhstan for 2017-2021, approved at the meeting of the Government of the Republic of Kazakhstan]. economy.gov.kz. Retrieved from http://economy.gov.kz/sites/default /files/pages/izmeneniya_v_pser_17-21_rus.pdf [in Russian].

- Osnovnye napravleniia denezhno-kreditnoi politiki Natsionalnoho Banka Respubliki Kazakhstan na 2017 hod, odobrennye Postanovleniem Pravleniia NBRK №271 ot 28 noiabria 2016 hoda [The main directions of monetary policy of the National Bank of the Republic of Kazakhstan for 2017, approved by the decision of the board of NBRK № 271 of November 28, 2016]. nationalbank.kz. Retrieved from http://www.nationalbank.kz. [in Russian].

- Kontseptsiia razvitiia finansovoho sektora Respubliki Kazakhstan do 2030 hoda, utverzhdennaia Postanovleniem Pra- vitelstva RK ot 27.08.2014 hoda. № 954 [Concept of the development of financial sector of the Republic of Kazakhstan till 2030, approved by the decision of the Government of the RoK of 27.08.2014. № 954]. nationalbank.kz. Retrieved from http://www.nationalbank.kz/?docid=382&switch=russian. [in Russian].

- Lavrushin, O.I., & Afanasyeva, O.N. (2013). Bankovskoe delo: sovremennaia sistema kreditovaniia [Banking: the modern crediting system]. (7d ed.). Moscow: KNORUS [in Russian].

- Lavrushin, O.I. (2015). O doverii v kreditnykh otnosheniiakh [About trust in credit relations]. Dengi i kredit – Money and credit, 9, 46–51 [in Russian].

- Matyash, I.V. (2010). Pokazateli sistemnoi effektivnosti v otsenke kreditosposobnosti i ustoichivosti predpriiatii v usloviiakh krizisa [Indicators of systemic efficiency in the assessment of creditworthiness and sustainability of enterprises in crisis conditions]. Ekonomicheskii analiz – Economic Analysis, 3, 2–9 [in Russian].

- Kapylova, A.S., Barannikova, O.E., & Ivanova, Yu.A. (2017). Metodicheskie osnovy otsenki kreditosposobnosti predpriiatii v zarubezhnykh bankakh [Methodical basis of estimation of creditworthiness of enterprises in foreign banks]. Teoriia i praktika aktualnykh nauchnykh issledovanii – Theory and practice of actual scientific researches, 66–68 [in Russian].

- Dadashev, B.A. (2013). Analiz osobennostei i sovershenstvovanie mekhanizma otsenki kreditosposobnosti predpriiatii ah- rarnoho sektora ekonomiki [Analysis of peculiarities and improvement of the mechanism of credit rating of enterprises of the agrarian sector of economy]. Nauchnye trudy Yuzhnoho filiala Natsionalnoho universiteta bioresursov i prirodopolzovaniia Ukrainy. SeriaEkonomicheskie nauki – Scientific works of the Southern branch of the National University of Bioresources and Nature Management of Ukraine. Series: Economic sciences, 152, 37–48 [in Russian].

- Galtsova, V.A. (2014). Vliianie otraslevykh osobennostei na otsenku kreditosposobnosti predpriiatii mashinostroitelnoho kompleksa [Influence of the industry peculiarities on the credit rating of the enterprises of engineering complex]. Uchet, analiz i audit: problemy teorii i praktiki – Accounting, analysis and audit: problems of theory and practice, 13, 41–44 [in Russian].

- Chernyshova, O.N., Fedorova, A.E., Cherkashnev, R.Yu., & Pakhomov N.N. (2015). Sovershenstvovanie metodov otsenki kachestva potentsialnykh zaemshchikov kreditnymi orhanizatsiiami [Improvement of methods for assessing the quality of potential borrowers by credit institutions]. Sotsialno-ekonomicheskie yavleniia i protsessy – Socio-economic phenomena and processes, No. 8, 152–161 [in Russian].

- Tipenko, N.G., Solovyov, Yu.P., & Panich, V.B. (2010). Otsenka limitov riska pri kreditovanii korporativnykh klientov [Estimation of risk limits at crediting of corporate clients]. Bankovskoe delo – Banking, 10, 44–52 [in Russian].