The article is devoted to the problem of reforming the tax systems of Kazakhstan and Russia in a market economy; the main key steps and the quality of their realizations are described. Of particular relevance is the analysis of the impact of tax regulators on the country's economic growth. In the context of integration into the world economy. it is necessary to find the most appropriate scientific approaches to reforming tax systems by improving the analysis. planning and forecasting the trends of its development. taking into account the influence of various factors. As the analysis of the works of foreign scientists in forecasting the development of complex financial systems in the conditions of a modern market economy shows. it is the methodology of alternative forecast scenarios that reflects the needs of strategic foresight in the context of a complex intertwining of contradictory trends in the development of the world economy. It is generally recognized that in the context of rapid and ambiguous changes. it is no longer possible to use planning methods based solely on extrapolating existing trends in technical. technological. economic and social development. Therefore. it is important to compare the state of tax systems to date and assess their level of competitiveness. Regarding Kazakhstan and Russia. the results of the regression model should be taken into account when carrying out reforms. The model of the tax system is an aggregate indicator. the so-called tax policy. so only a systemic transformation will help to qualitatively influence the economic growth of the country.

Tax systems are one of the main mechanisms for influencing the country's macroeconomic policy. After the collapse of the USSR. Kazakhstan and Russia faced the problem of adapting economic systems to the conditions of new challenges of a market economy. Reforming tax systems was a priority in the transformation process [1].

Kazakhstan's tax system of the transition period was subject to dependence on the Russian economy due to the attachment of budget policy to the Russian ruble and relied on its experience in the development of regulatory and legal documents. So. essentially the legislative document «On the tax system in the Republic of Kazakhstan». adopted on December 24. 1991. It is almost the same as the version of the Russian legislation. It should be noted that borrowing foreign experience is a very controversial issue. direct copying often does not lead to an effective result. it is important to take into account the peculiarities characteristic of the country in question. Therefore. the rush in the adoption of the tax policy in Kazakhstan led to the choice of the Russian three-tier model of the tax system. characteristic for countries with a federal arrangement [2].

The tax system of Russia of that period was characterized by excessive tax burden. So. according to the estimates of the specialists of the Central Economics and Mathematics Institute of the Russian Academy of Sciences E. Yegorova and Y. Petrov. the tax burden borne by enterprises in 1992-1994 was 58.9 %. which is 15 points higher than the critical point and practically completely excluded the investment process in Russia but in such a disappointing situation. the state's activities were limited only to the introduction and modification of individual presidential decrees [3]. Rigid tax policy of Kazakhstan and Russia led to a significant reduction in the amount of profits after tax deduction. which automatically triggered the process of evading entrepreneurs from taxation and the prosperity of illegal production. tax revenues in the budgets of countries were reduced.

Russia. The plan of measures to improve the tax system was outlined by the Government Program of the Russian Federation for 1995-1997. where special transformations were not made. Since the beginning of 1999. a new round of improving the system of taxes and fees in the Russian Federation has begun. This stage of the reform was marked by the entry into force on January 1. 1999 of the first (common) part of the Tax Code. which established the principles of taxation in their modern form. Since January 1. 2002. the next new chapters of the second part of the Tax Code of the Russian Federation have entered into force.

Kazakhstan. The abundance of inefficient taxes created an unmanageable and completely inefficient tax system. In order to improve it. in 1994. the concept of tax reform was developed in Kazakhstan. in which

two stages emerged, 1994-1995 the development of the Tax Code, 1996-1998. completion of the formation of the tax system. According to the tax laws, 11 types of taxes began to function instead of 45 taxes, and instead of a three-tier system, 11 types of taxes were grouped in accordance with the unitary structure of the state into two groups: national and local taxes and fees.

Tax legislation in Kazakhstan in 1995, at first gave progressive changes, but by 1997 the tax system was again unstable. Proclamation of 11 taxes was only declarative in nature, in fact, the number of fees and payments began to increase to 17.

In the wake of Russia, on July 1, 2001, the Kazakhstan Tax Code entered into force.

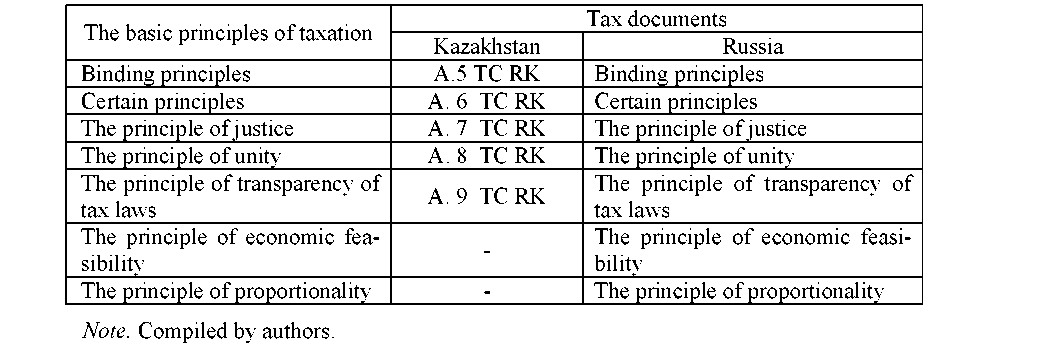

It is not surprising that in comparing the basic principles on which the construction of the tax systems of Kazakhstan and Russia is based, no significant differentiation was found (Table 1). At the same time, the Kazakh TC does not describe private legal principles, which include the principle of economic validity and the principle of proportionality. According to them, taxes and fees should have an economic justification, and cannot be arbitrary, nor should they be excessively onerous for taxpayers [4].

Table 1 Principles of Taxation in Kazakhstan and Russia

The next significant stage of changes in the tax systems of Kazakhstan and Russia falls on the pre-crisis period 2007-2008.

Kazakhstan adopted a new course of economic development, which also affected the fiscal policy. According to the message of the President of the Republic of Kazakhstan in 2008: «There is a need to bring the tax system in line with the tasks of the new stage of development of Kazakhstan. The current Tax Code has played a positive role in economic growth, but at present its potential is almost exhausted. The Code includes over 170 types of benefits and preferences, which constantly and unsystematically grow. The government should develop a new Tax Code». It should promote modernization and diversification of the economy, the emergence of business from the «shadow». So in accordance with the new Tax Code in the Republic of Kazakhstan, which entered into force in 2008, there are 13 types of taxes, 5 fees, 10 fees [5].

The share of tax revenues in the GDP of the Republic of Kazakhstan has doubled in comparison with 1994 in 2008, but after a decrease occurred, with the introduction of amendments in 2009. In the Tax Code, the rates of the main system-forming taxes were reduced, the scope of tax incentives was expanded, and the rate of tax revenue growth was reduced (Table 2).

Table 2

The share of tax revenues to the gross national product of the Republic of Kazakhstan in 2008-2010

Note. Compiled by the authors.

|

Indicators |

2008 |

2009 |

2010 |

|

Tax revenues, million tenge |

2819510 |

2228682 |

2934081 |

|

Gross domestic product, million tenge |

16052919 |

17007647 |

21513473 |

|

The share of tax revenues in GDP, % |

17,56 |

13,10 |

13,64 |

Серия «Экономика». № 1(89)/2018

247

During this period, in 2007, the Russian Federation first developed a document for a three-year planning of the tax policy. Subsequently, such documents are compiled annually, which is very important for the transparency of the tax system and the ability to forecast its activities for taxpayers.

During this period, in 2007 the Russian Federation was the first to develop a document on a three-year plan of tax policy. In the following year, it is prepared such documents, which is very important for the transparency of the tax system and the ability to project their activities for taxpayers [6].

With the formation of integration association - the Eurasian Union has become an important aspect of the development of cooperation in the field of taxation. Therefore important to compare the state of the tax systems of today and to assess their level of competitiveness [7].

The most successful embodiment of the tax preferences in Russia and Kazakhstan is the mechanism of tax incentives. Since it really stimulates investment potential, at the same time it is relatively convenient for avoiding the creation of administrative barriers. The mechanism of accelerated amortization of the author's opinion does not contain a strong investment component. To validate arguments N. Vishnevskaya «Acceler- ated depreciation cannot replace investment incentives, as its mechanism does not stimulate the modernization, expansion of production and R&D, because it may be subject to accelerated depreciation and purchased the old equipment».

Establishment of the Eurasian Economic Union presents new challenges for tax systems of Kazakhstan and the Russian Federation in the process of unification of the foreign economic policy difficult issue becomes a harmonization of tax systems, which contains the problems of formation of legal documents, the introduction of various control methods of unfair tax competition between EU countries, etc. In addition, there are some long-standing problems: unlike most Western countries, in Russia and in Kazakhstan, a large percentage of tax exemptions account for indirect taxes, the uneven distribution of the tax burden on the various sectors of the economy, weak fiscal discipline and tax administration. Solving these problems is a priority and urgent, both for the countries themselves and for their mutually beneficial relations.

In the ranking, compiled by the agency in 2015 PricewarehouseCoopers Kazakhstan in terms of userfriendly tax systems in the world in an impressive position among 189 countries in the rating of Russia has made a significant leap with 102 seats in 2012 to 49 in 2015, despite significant progress, the backlog of Kazakhstan significantly, however the sub-indicator «time for registration tax» Russia Kazakhstan surpassed in 2015 by reducing the time from 209 hours to 168 hours per year (Table 3).

Table 3

The tax system of Kazakhstan and Russia in 2015

|

Indicators |

Kazakhstan |

Russia |

|

Place in rating PwC |

17 |

49 |

|

The number of tax payments per year |

6 |

7 |

|

Time for registration and payment of taxes (hours per year) |

188 |

168 |

Note. Compiled by the authors based on PricewarehouseCoopers.

High places in the ranking are quite dubious achievement, because for the ranking compiled official information about the completion of the formal procedures, without taking into account the corruption component, the proportion of which is significant in developing countries, what are the Kazakhstan and Russia. Moreover, in carrying out reforms often rely on the published ratings and even set goals and objectives to improve the country's position in it. The degree of dependence of these indicators with the index economic growth of the country is interesting from the point of view of the analysis. Which fiscal instruments and how can affect the growth of the national economy.

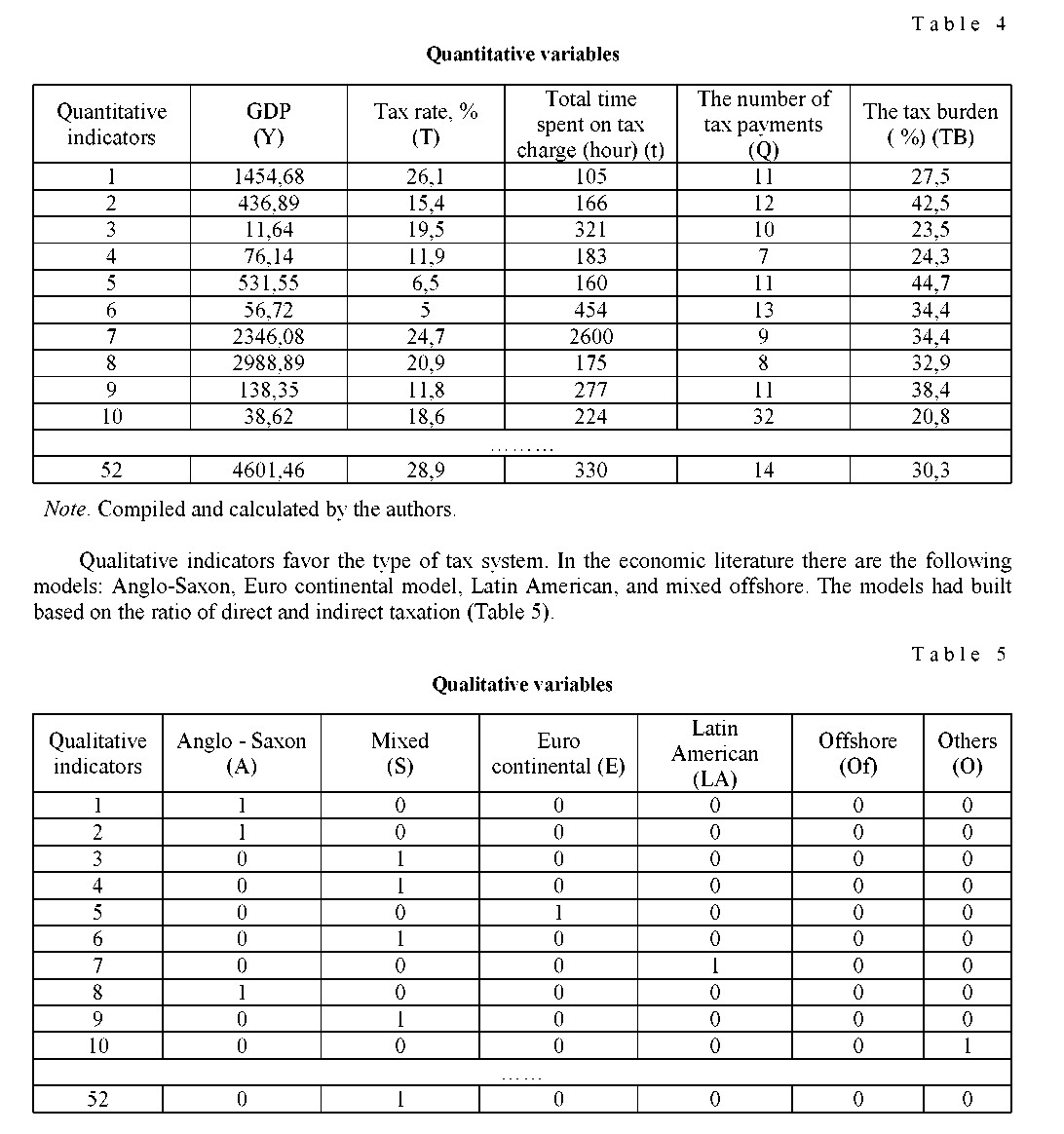

For this study, a representative sample is selected for 52 countries of the world. Set of variable gross domestic product, which characterizes the country's economic growth. As the explanatory variables are the fiscal indicators on which set the rating countries in terms of availability of tax systems PWC- income tax rate, number of payments per year and the total amount of time spent on the payment of taxes, the following quantitative traits selected indicator of the tax burden based on data OECD (Table 4).

Foreign practice shows that in conditions of unstable economic systems, characterized by a high level of inflationary processes and their strong influence on the behaviour of economic agents, the levers of direct incentives from the state (subsidies from the budget, subventions) should recede into the background. The decisive role here belongs to the levers of indirect stimulation [8].

Among indirect methods of stimulation it is necessary to allocate active application of tax instruments. The increase in the proportion of benefits providing a favourable innovative climate is a general trend.

After studying a lot of foreign sources, we identified the most common types of support and stimulation of innovation in practice in different countries:

– direct financing of costs for the creation of new products and technologies, accounting for up to 50 % of its total amount — USA, France;

– granting to innovators of interest-free loans — Sweden;

- – tax incentives in the form of lowering tax rates, establishing a simplified taxation regime, granting tax credits;

- – creation of innovation innovation funds to reduce risks — Germany, Switzerland, France, the Netherlands;

- – Granting of gratuitous loans, providing up to 50 % of the costs of implementing new projects — Germany;

- – reduction of state duties for individual inventors, deferment of payment of duties, if the invention is related to energy saving - Austria, Germany, USA;

- – free services of patent attorneys and office services for individual inventors — Germany, the Netherlands;

- – various grants, loan guarantees, competitive support programs, tax credit programs used in many countries.

Despite a large number of forms and methods of financial stimulation of innovation activity, for today, there are many problems hampering the development of innovation activities, both in Kazakhstan and in other EEU countries.

In the field of taxation of the innovation sector in the Republic of Kazakhstan, a number of problems have been identified:

- – despite the existence of preferential tax regimes in the Republic of Kazakhstan, most innovative enterprises pay taxes on the traditional taxation system;

- – Innovative products have a large added value, and in the total tax burden of these organizations, the share of value added tax (VAT) is high;

- – high level of aggregate tax burden (especially taking into account corporate income tax, corporate property tax and land tax). To change the current situation, it is necessary to use the full range of financial instruments, primarily tax incentives.

Analysis of the development of SEZ and their role in the development of Kazakhstan's innovative potential has shown the incompleteness of the formation of the SEZ infrastructure, which is a consequence of the lack of sufficient funding. Also, the insufficient development of the transport, logistics, energy and other infrastructure of the country is a barrier to the development of industrial sectors [9].

Unequivocally, we must admit that there are no departments in Kazakhstan that re-integrate accumulated knowledge and technologies into side effects. Some innovative technologies are not protected by copyright and, therefore, their use does not require a license, and this, in turn, negatively affects the amount of investment from other innovators. The volume of investment is very meagre, in some SEZs they do not exist at all (Taraz Chemical Park).

Taking into account the above, we believe that it is necessary to conduct a simulation of the financial and socio-economic development of the special economic zone in the regions, taking into account the entire breadth of the interacting factors of the financial and socio-economic base, and to express the «integrity ef- fect» of this system, it is necessary to combine the SEZ indicators In separate sets or information blocks.

In the model we propose, there is a general trend in the development of a special economic zone and innovative activity in the region of the country (for the example of the Karaganda region), for the period analyzed, expressed by indicators of financial and socio-economic development in their unity and interrelationships, as well as trend calculation of the revenue projection from entities Innovative activities that will apply the proposed new special (simplified) taxation regime.

Each block of indicators will reflect the dynamics of one of the components of the development of SEZ.

The model of each block describes the set of factors of the economic state and innovative development of the Karaganda region, which will express a separate direction of the analysis of the region's economic development.

To achieve innovative development in Kazakhstan, it is necessary to consider the possibility of introducing a change in the taxation system of the innovation sector, in particular, it is necessary: to provide an investment tax credit for 3-5 years, or for the entire period of the innovation project implementation; To exempt from imported value added tax and import customs duties imported equipment, raw materials, licenses, know-how necessary for the implementation of the investment project and are not competitors to domestic producers for projects on breakthrough priorities, or to lower taxes and duties by 50-75 % On socially- oriented priorities; Remove restrictions on accelerated depreciation of scientific and technological equipment, proceed with the determination of the depreciation life from moral rather than physical wear and tear; When calculating the property tax, do not include in the taxable base of industrial enterprises the cost of machines, equipment, prototypes, mock-ups and other products transferred for testing and experiments of a scientific organization in the process of fulfilling an order for the creation of scientific and technical products in accordance with the terms of the contract [10].

But at the same time, all incentives for innovative activities should be provided «conditionally», in the case of not implementing an innovative project, taxes should be paid with a penalty for late payment of tax, and soft loans - returned with payment of increased interest.

Among other measures of tax incentives, it is necessary to allocate such a form as a special (simplified) tax regime for the innovation sector, which is recommended to introduce taxation of subjects of innovation activity into Kazakhstan practice. Within the framework of this special tax regime, it is proposed to free scientific and innovative organizations from paying income tax from organizations, social tax, VAT, corporate property tax and land tax. Thus, the main result of the introduction of a new special tax regime could be, first of all, the reduction of the general tax burden on the organization of the innovation sphere.

The first step in the study is based correlation matrix, reflecting the interdependence of variables. According to the matrix, you can draw the following conclusions:

- On the value of GDP in most influence: the tax rate and type of tax system, with a correlation coefficient equal to 0.3801 and 0, 3154, respectively.

- Positive relationship has Latin American type of tax system and the total amount of time spent on the payment of taxes. (According to the statistical data is a pattern indeed traced Countries with tax systems of the Latin American type of spend n-number of hours per year for the payment of taxes in excess of the average value in the context of 52 countries For example, in Brazil a year spent 2600 hours on payment of taxes, Mexico -334 hours per year, as compared with Denmark -130 hours per year (Anglo-Saxon model), Luxembourg - 55 hours per year (offshore model) [11].

- Euro continental type of tax systems has a positive relationship with the tax burden. This statement is also confirmed by the data from the original table, Belgium - 44.7 %, Germany 36.5 %, Italy 43.9 %, etc.

- High negative relationship is the tax burden and the number of payments per year.

In Kazakhstan and Russia, the results of the regression model should be taken into account in carrying out reforms. Model of the tax system is an aggregate indicator, so-called fiscal policy, so that only a systemic transformation will qualitatively affect the country's economic growth.

References

- Alisenov, A.S. (2004). Problemy ekonomicheskoi bezopasnosti v protsesse intehratsii nalohovykh sistem Rossii i Kazakhstana [Problems of economic security in the process of integration of the tax systems of Russia and Kazakhstan]. Candidate's thesis. Moscow, 4-6 [in Russian].

- Armstrong, D. (2006). Long-term Forecasting: Principles and Techniques. London: Weily.

- Egorov, E.N., Petrov, Y. (1997). Sravnitelnyi analiz nalohooblozheniia zarabotnoi platy v Rossii i zarubezhnykh stranakh [Comparative analysis of the taxation of wages in Russia and foreign countries]. Moscow: TsEMI RAN [in Russian].

- Gaidar Forum. nalogforum.ru. Retrieved from (2014). http://nalogforum.ru/?p=299.

- Kenzheguzin, M.B. (2007). Krupnye ekonomicheskie struktury pri perekhode Kazakhstana k rynochnoi ekonomike (orhanizatsiia i upravlenie) [Large economic structures under Kazakhstan transition towards market economy (organization and management)]. Almaty: Hylym [in Russian].

- Morozova, T.G., & Pikulkina, V.V. (2000). Planirovanie i prohnozirovanie rynochnykh uslovii [Forecasting and planning under market conditions]. Moscow: INITI-DANA [in Russian].

- Nakipova, G. (2006). Conceptual basics for managing modern production and economic systems. Eurasian Community, 4(56), 18-26.

- Nazarov. V.S. (2008). Nalohovaia sistema Rossii v 1991–2008 hodakh [The tax system in Russia in 1991-2008 years]. ru-90.ru. Retrieved from http://www.ru-90.ru/node/1170[in Russian].

- Organization for Economic Cooperation and Development (2012). oecd.org. Retrieved from http://www.oecd.org/.

- Paying Taxes (2012). The global picture. PricewarehouseCoopers.

- Steinbruner. R. (2006). Forecasting: Judgment under Uncertainty. Bloomington: Indiana University Press.