In work on the basis of the synthesis of the SERVQUAL methodology with calculations of integral indices of the correspondence of the quality content to customer requests, a generalized indicator of the quality of banking services, tools of correlation and regression analysis methods, a multi-channel queuing system, a comprehensive methodology for assessing the quality of banking services was developed. As the economy of Kazakhstan develops, the relevance of problems related to the quality of service in banks in a competitive environment is growing.The organization of the Bank's activities raises the issue of developing a system of measures to assess and manage the quality of banking services, which will allow the bank to flexibly maneuver with available information, material and financial resources in solving strategic and tactical tasks. Quality is now quite new from a scientific point of view, the object of management. Together with this, the modern representation of the concept of quality, its parameters does not meet the requirements of the market. This necessitates the scientific comprehension and practical development of new effective forms and methods, the formation of methodological approaches in assessing the quality of banking services through an appropriate quantitative toolkit. The search for forms and methods of effective functioning of domestic banks is an urgent problem in which quality issues occupy one of the leading positions. These facts make it possible to relate the given problem to the number of the most relevant in modern science.

The complexity and multidimensional nature of problems of assessing the quality of banking services is due to a wide range of issues related to the insufficient development of organizational and methodological instruments in commercial banks.

To cover at length the research topic, much attention is paid to the scientific approaches developed by E. Deming [1], Ch. Gronroos [2], Y. Lee [3], G.H.G. McDougall [4].

The necessary quality measuring indicator of banking services is the desired, necessary, and possible level of service quality taking into account the specific waitings and requirements of customers.

The quality management of banking services is a type of activity aimed at meeting the requirements and expectations of consumers set for the quality of banking services. It depends on the degree of interaction and optimality of internal relations [5]. Therefore, it will be true that in the case of determining the opinions of customers on the quality of the services provided by a bank, it is possible to adjust internal communications in the best possible way. Then the main task of setting up the management system and internal interaction is to build its quantitative assessment, adequately reflecting the assessment of the quality of banking services in a dynamic external environment.

When considering the parameters of the quality of banking services, it should be considered that they are not exclusively additive by nature. Factors determining quality can be independently additive, but also represent a multiplicative effect on other criteria or their parameters, enhancing or weakening their positive or negative impact.

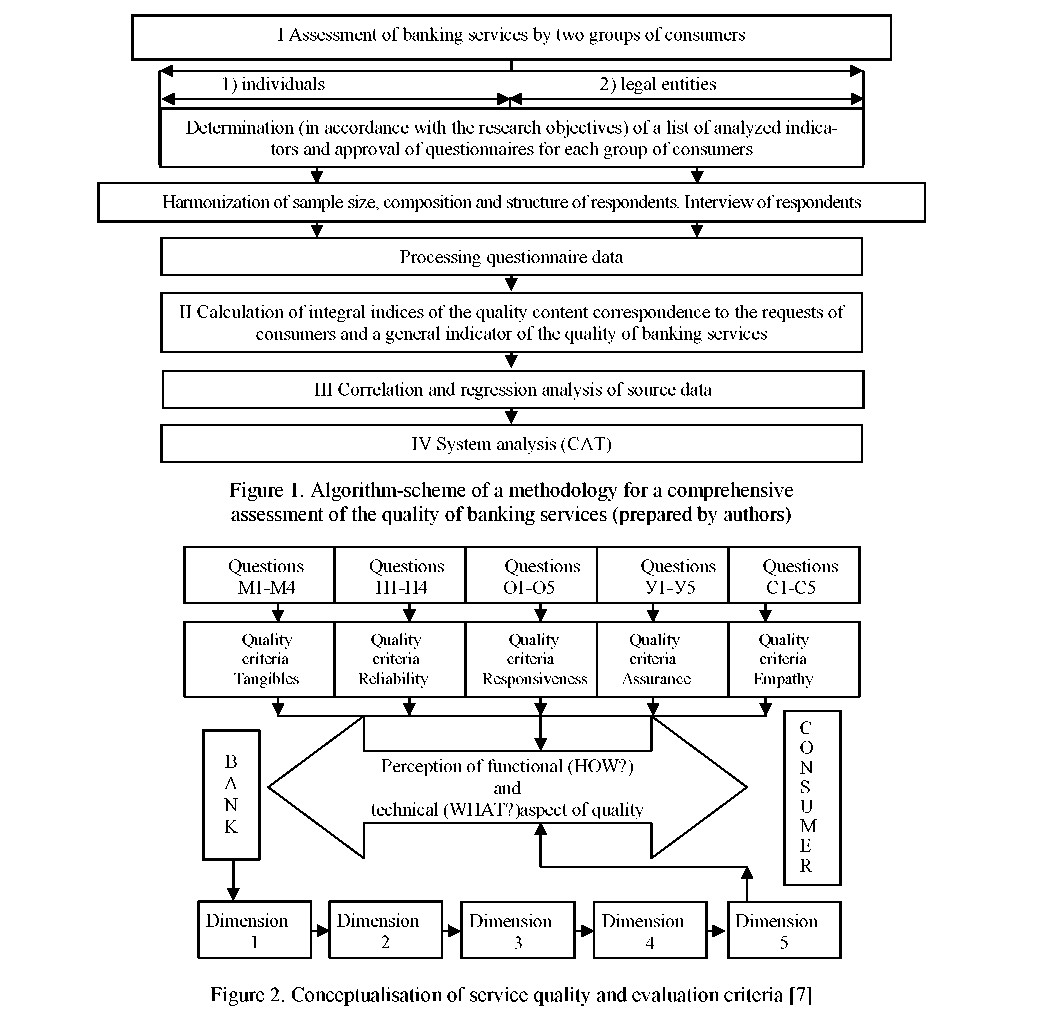

To access the quality of banking services, it seems advisable to use a system of indicators or a comprehensive assessment of the quality of banking services, which is based on the principle of quantitative assessment, which gives a fair presentation of the quality level of the management object. The algorithm of its implementation can be presented in scheme (Fig. 1).

The primary information for assessing the quality of banking services to the needs of consumers according to the methodology includes the survey interview data on two consumer groups: legal entities and individuals serviced in the bank under investigation. Questionnaires are compiled in accordance with the principles of the SERVQUAL methodology (Fig. 2).

Based on the proposed five-dimension model, according to the SERVQUAL methodology, it turns out that: the first dimension is the gap between the consumer's expectation about the quality of the banking service and the reaction of the bank's management to these expectations; the second dimension is the gap between the management's understanding of the customer's expectations and the process of implementing the quality system in its bank; the third dimension - the gap between the quality system introduced by the bank's management and the unpreparedness of the bank's personnel to follow established standards; the fourth dimension is the gap between the existing quality system in the bank and the inflated advertising of this quality system in the media; and. finally. the fifth. the most important. dimension is the gap between the expectations of consumers of the banking service and the process by which the bank provides this service.

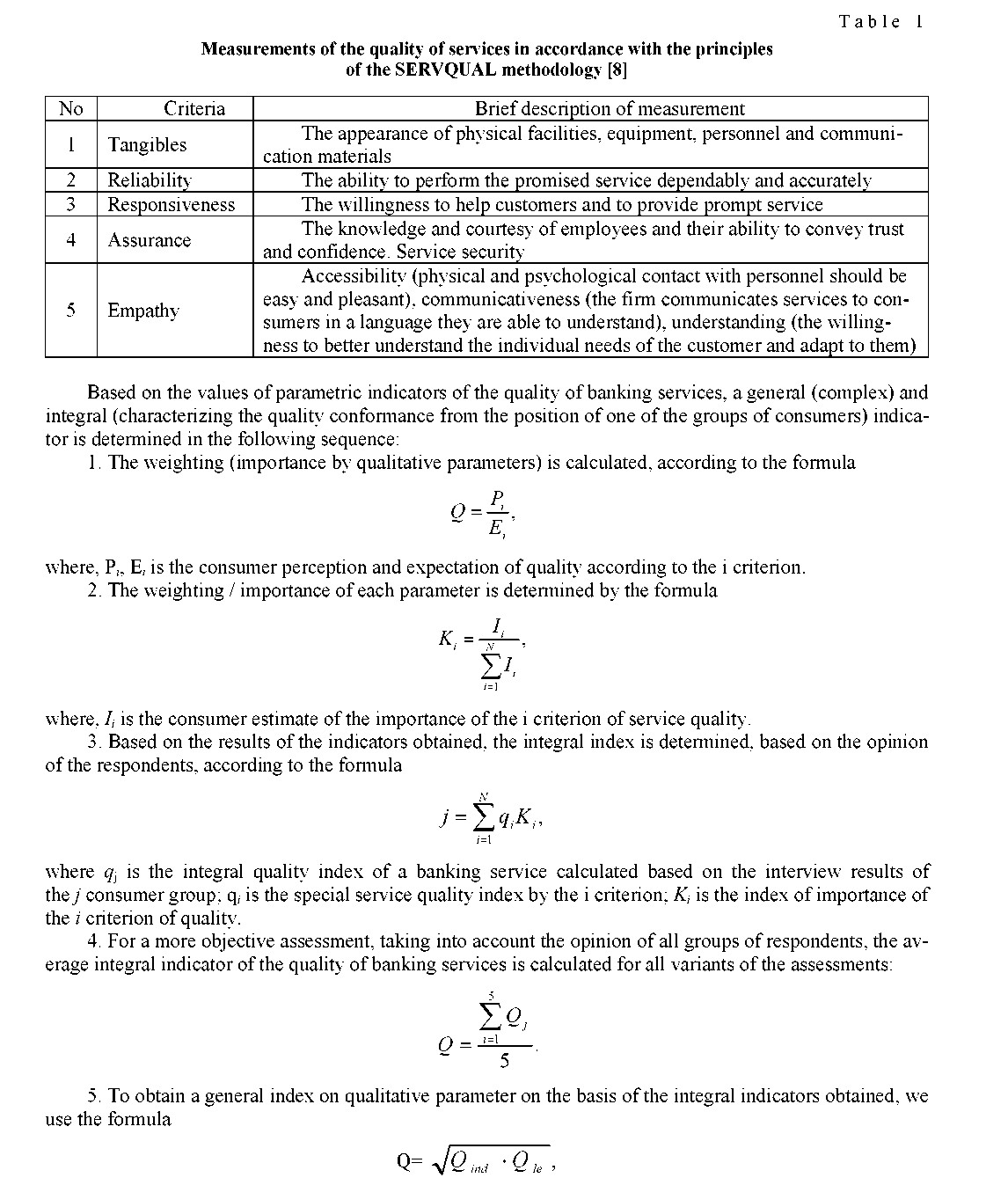

The conducted research of the consumer behaviour of the banking industry showed that clients mainly assess the functional and technical aspects of the quality of banking services in accordance with the five main criteria specified in Table 1.

The processing of the questionnaire data consists in calculating the indicator (score) of expectation. perception and importance. as well as the quality factor as a difference in perceptions and expectations for each indicator [6].

Evaluation of the SERVQUAL methodology applied to the sphere of banking services within the framework of research has proved its effectiveness by revealing the most bottlenecks in the bank's activity. Based on the results obtained. the relative picture of quality in the bank under investigation and the most problematic quality characteristics are determined. Therefore. for a more in-depth analysis of problem areas. it seems necessary to conduct a comprehensive assessment of the quality of banking services.

where, Q is the general index of the conformity of the content and quality of banking services; Qind., Ql.e. are the integral indices of the conformity of the content and quality of banking services, respectively, calculated by the results of individuals and legal entities interview.

The calculated values of the integral and general index, determine the level of satisfaction of the bank's customers, and the possibility of applying the indicator to develop recommendations for improving the quality of banking services.

Further, on the basis of the results of the questionnaire on the two groups of respondents, the values of the general and integral indicators of the quality of services are determined.

By reason of its general sense the quality indicator reflects the difference between the expected service and delivered service per unit of perception from the result of the consumption of banking services on quality parameters. Accordingly, the level of respondents' satisfaction with the five quality criteria is estimated according to Table 2.

Table 2 Evaluation of the quality of banking services compliance with the requirements of consumers [9]

|

Quality Index Range |

Grades of assessing the quality of banking services |

|

From 0,80 to 1,00 |

Normal |

|

From 0,60 to 0,79 |

Satisfactory |

|

Less than 0,59 |

Critical |

The result of further research is a detailed assessment of each of the factors (parameters) impact of the five main criteria for the quality of banking services on the level of the performance indicator. In this connection, the probability theory methods and mathematical statistics are used, which allow us to discover regularities hidden among randomness. Data processing has been performed using the «Correlation and Regression Analysis» standard program.

«Modelling on the basis of regression equations can be reduced either to the construction of one equation with the inclusion of a large number of factor characteristics, or to the construction of a system of equations. In the latter case, a system of statistically unrelated equations is obtained; however, the entire system is connected by a single chain of cause-effect relationships» [10].

In the research, a general question can be used as an outcome, for example: «How, in general, do you evaluate the quality of service?» Factor characteristics are twenty-two indicators within the five quality crite- ria/dimensions in the framework of the SERVQUAL methodology.

After selecting the effective and factor attributes, the preconditions for the multicollinearity phenomenon occurrence are checked. This phenomenon often represents a perceptible threat to the correct identification and effective evaluation of interrelations [10].

For this, it is advisable to use a method based on the analysis of paired correlation coefficients, which indicate estimates of the constraint equations accuracy (reliability) and the validity of their application.

The analysis of the obtained correlation coefficients calculated for factor indices within the framework of five quality criteria indicates the presence or absence of collinear factor indices.

It is believed that the two indicators are collinear if the pair correlation coefficient is not less than 0.8 [11].

After selecting and determining the most influential factors for the effective indicator of service quality, their communication form, the analysis of the initial statistical information, it is necessary to proceed to multi-step regression analysis based on the elimination of nonessential factors according to the Student's t-test (t-statistics). By this criterion, the hypothesis is tested whether the regression coefficient αj is significantly different from zero for some given level of significance ₤, which shows the probability of rejecting the correct hypothesis.

The result of multi-step regression analysis in the construction of a model for assessing the quality of banking services is the elimination of statistically insignificant factor indicators of the multiple regression equation.

The coefficients of the linear multiple regression equation (bi ) show the degree of influence of the factor Xi on the analyzed indicator Y (with the fixed at a constant level influence of other factors included in the model and the average level of influence of unaccounted factors). The regression coefficient, interpreted in this way, is used in economic statistical analysis as an average estimate of the effectiveness of the i factorargument on the function.

A direct comparison of the regression coefficients in the multiple regression equation shows the degree of influence of the factor characteristics on the performance indicator only when they are expressed in the same units and have approximately the same variability. For this purpose, it is proposed to use a whole system of indicators: average frequency coefficients of elasticity, beta coefficients and delta coefficients [10; 87].

The research has used the average partial coefficient of elasticity (Ei ), which allows the measurement in percentage terms of changed effective indicator with an increase in each factor by the same relative value - by 1 %. This interpretation is very convenient and understandable for every economist.

Thus, it is possible to identify the main exposures affecting the effectiveness of quality management of banking services in the bank under investigation. They should be focused on first.

It should be noted that the model makes it possible to establish only the level of the phenomena under study corresponding to the chosen factors. But since it is practically difficult to allocate all the factors that affect the quality of banking services, the deviations of the actual values of the analyzed indicators from the calculated ones can be explained by the action of unaccounted factors. Including more factors in the model significantly increases its adequacy.

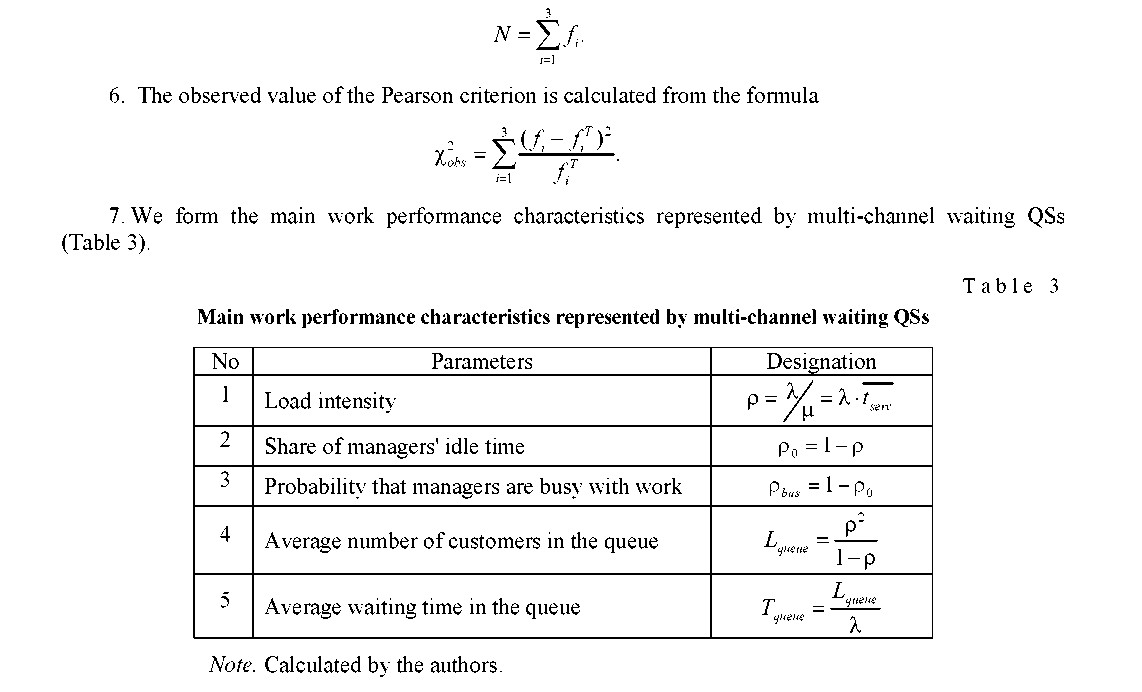

The system, as an economic entity, is predominantly of productive function to make profit. Proceeding from this, let's consider the efficiency of credit departments on servicing the bank's individuals and legal entities, whose purpose is to conclude the maximum possible number of loan agreements.

Economic and mathematical models should be used to determine the servicing process, the optimal allocation of working hours in the bank's credit management. Unsatisfactory assessments of some quality parameters identified on the basis of the survey, allow proceeding to a quantitative assessment of the system analysis.

The bank is a system, since it is a collection of elements (subsystems) that are in relationships and connections with each other and form a certain integrity (unity). Under these conditions, the elements (for example, the bank's credit department) themselves can be considered as systems, and the system under study - as an element of a more complex system - the bank.

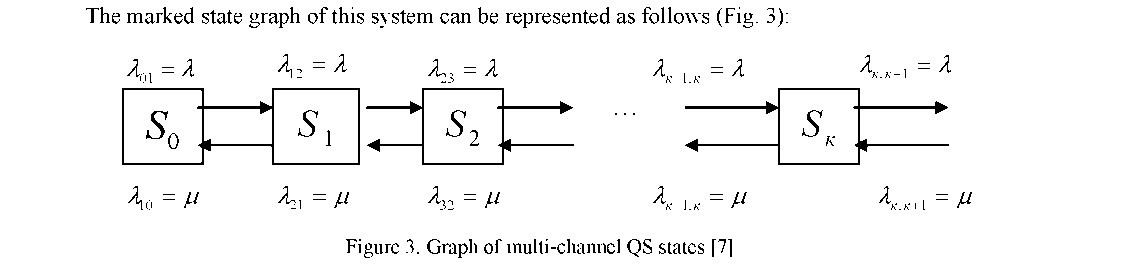

The system of credit departments is intended for a reusable use when solving similar tasks with arising service processes, and this means that this system is queuing system (QS) [7].

To classify the QS, the service discipline is important that determines the order of selecting applications from among those received and the order of distributing them among free channels. On this basis the application can be serviced under the «first came - first served» principle.

The queueing process described by this model is characterized by the intensity of the incoming flow λ , and at the same time no more than n customers (applications) can be served. The average service time of one application equals 1. The incoming and outgoing flows are Poisson. The operation mode of a given service μ

channel does not affect the operation mode of other service channels of the system, and the service procedure duration for each of the channels is a random variable subject to the exponential distribution law.

The purpose of the mathematical description of the bank's credit departments as a queuing system is to construct a mathematical model linking the given working conditions of the QS (the capacity of the service canal, the nature of the applications flow, etc.) to the operating performance indicators of the QS describing its ability to cope with the flow of applications.

The multichannel QS, describing credit departments of the bank, can be in one of an infinite number of states:

- — the channel is free (therefore, there is no queue);

- — the channel is busy and there is no queue, i.e. (one application is serviced in the QS);

- — the channel is busy, one application is in the queue;

Sk — the channel is busy, k-1 application is in the queue.

p and τ there is the following relationship:

where a = np is the average number of events falling on a time interval that can be determined through the intensity of the event flows λ as follows:

The dimension of the flow intensity λ is the average number of events per unit time. Between n and λ ,

The incoming flow of applications and the application service flow - the simplest flows that have the properties of ordinariness (the occurring probability for an elementary (small) time interval Δt of more than one event is negligible compared to the occurring probability during this interval of one event); absence of consequences (events in the flow appear at successive time instants independently of each other); stationarity (probabilistic characteristics do not depend on time).

If the flow simultaneously has the properties of stationarity, ordinariness and absence of consequences, then such a flow is called the simplest (or Poisson) flow of events. The mathematical description of the effect of such a flow on systems is the simplest. Therefore, in particular, the simplest flow plays a special role among other existing flows.

The QS transitions from state to state from left to right arrows (the receipt from the customers of speed servicing requirements) occur under the influence of the same incoming flow of applications with intensity λ. Therefore, the density of transition probabilities:

The QS transitions from state to states from left to right arrows (applicationas are serviced by the managers of the bank's credit departments) are awaited by the flow of services with the intensity μ.

to right arrows (applicationas are serviced by the managers of the bank's credit departments) are awaited by the flow of services with the intensity μ.

Fulfilling the inequality λ ≥ μ (the intensity of receipt from customers of the speed servicing requirements ≥ of the intensity of application serviced by managers of bank's credit departments) means that the intensity λ equal to the average number of applications received in the system per unit time is not less than the intensityμ equal to the average number of applications serviced for the same time with continuously operating channel, it is obvious that the queue is growing.

Where λ < μ, i.e. when loading on the system p = (λ∕μ) < 1 means that the limiting mode of customer service and the limiting probabilities of states exist.

Considering a certain time interval τ , the probability of a random event occurring in this interval p, and the total number of possible events n, with the ordinariness property of event flow, the probability p will be a sufficiently small value, and n is a sufficiently large number, since mass phenomena are considered. Under these conditions, to calculate the occurring probability of a certain number of events m on a time interval τ , the Poisson formula can be used.

п

Серия «Экономика». № 1(89)/2018

259

260

Вестник Карагандинского университета

Based on the above, we can draw the following conclusions:

Based on the SERVQUAL methodology synthesis calculating integral indices of the correspondence of the quality content with customer requests, a generalized indicator of the banking services quality, tools of correlation and regression analysis methods, a multi-channel queuing system, a comprehensive methodology for assessing the banking services quality has been developed.

Thus, the methodology for a comprehensive assessment of the banking services quality can be applied during computational experiments, in studies whose purpose is to elucidate a possible picture of future development and predict the values of some variables depending on changes in others. Consequently, the research tool is practically meaningful, in its factor structure, and hence universal, in various sectors of the services market, including banking.

The Source of financing: The Grant of the Ministry of Education and Science ofRepublic of Kazakhstan «The Best teacher - 2016» (Mussina A.A.).

Referances

- Deming. E. (1994). Vykhod iz krizisa [Exit from the crisis]. Tver: Izdatelskaia firma «Alba» [in Russian].

- Gronroos. Ch. (1982). Strategic management and marketing in the service sector (Research reports / Swedish School of Economics and Business Administration). amazon.com. Retrieved from https://www.amazon.com/.

- Lee, H., Lee, Y., & Yoo, D. (2000). The determinants of perceived service quality and its relationship with satisfaction. Journal of Services Marketing, l4 (3), 250. doi.org/10.1108/08876040010327220.

- McDougall, G.H.G., & Levesque, T. (2000). Analyzing customer satisfaction with service quality in life insurance services. Journal of Targeting, Measurement and Analysis for Marketing, 18(3-4), 401. Retrieved from https://link.springer.com/article/10.1057/jt.2010.17.

- Chernyshev, B. (2004). Menedzhment v servisnoi ekonomike: sushchnost i soderzhanie [Management in service economy: essence and content]. Problemy teorii i praktiki upravleniia - Problems of management theory and practice, 1, 111 [in Russian].

- Novatorov, E.V. (2001). KAChOBRUS: marketinhovyi instrument dlia izmereniia kachestva obrazovatelnykh usluh [KACHOBRUS: a marketing tool for measuring the quality of educational services]. Marketing. – Marketing, 6, 54–67 [in Russian].

- Andreyev, I. (1998). Kriterii konkurentosposobnosti odnorodnykh bankovskikh usluh [Criteria of competitiveness of homogeneous banking services]. Marketinh – Marketing, 1, 38–40 [in Russian].

- Fomin, G.P. (2005). Matematicheskie metody i modeli v kommercheskoi deiatelnosti [Mathematical methods and models in commercial activity]. Moscow: Finansy i statistika [in Russian].

- Otdel marketinhovykh issledovanii vuza — sviazuiushchee zveno. Konkursnaia rabota [Marketing research Department of the University. Competitive work]. ram.ru. Retrieved from http: // www. ram.ru /activity /comp /bp 2003 /files /std16.pdf [in Russian].

- Korolev, Yu.G., Rabinovich, P.M., & Shmoilova, R.A. (1985). Statisticheskoe modelirovanie i prohnozirovanie [Statistical modeling and forecasting]. Moscow: MESI [in Russian].

- Frenkel, A.A. (1989). Prohnozirovanie proizvoditelnosti truda [Prediction of labor productivity]. Moscow: Ekonomika [in Russian].