The article analyzes the influence of the main economic indicators of the real estate market in Kazakhstan, and a forecast of real estate prices. Since the real estate market refers to the resource market, then it affects all of the same factors that are characteristic of the resource market. It is not only the demand, supply, competition, the level of socially necessary labor, the industry average level of profitability, the state of the financial sector, the state level of intervention in terms of the functioning of the market, specific to the existence of market-based pricing mechanism. In accordance with its definition of the market value of the property depends on the factors that determine the average or more likely the price of its sale on the market in normal conditions of the transaction. Multivariate correlation and regression analysis for the period from 2007 to 2017 was conducted to assess the impact of the real estate market the main factors of development and forecast average annual data. As a result of the analysis obtained pairwise correlation coefficients, determining closeness of the relationship between variables. Along with the dynamics of the dollar for the analysis were chosen the most significant factors affecting the real estate market, such as the rate of the dollar to the tenge, the volume of mortgage lending; world oil prices, the nominal income residents. Determined closeness of the relationship between the studied factors. It revealed a level of correlation between the factors of the real estate market and selected the most relevant macroeconomic factors affecting the real estate market.

One of the main indicators of the development of normal market relations in the country is the state of real estate market in general and its individual sectors in particular. The real estate market is an essential component of any national economy, because real estate is the most important part of national wealth, which accounts for more than 50 % of the world's wealth. Without a real estate market, there can be no market at all.

The importance of the domestic real estate market as an economy sector is confirmed by its high share in the gross national product, high level of budget revenues from primary sale, rental of public and private real estate, high level of tax collection from real estate taxes and transactions with it.

Often, real estate is the only component of the availability of owners' capital and the most significant sign of its existence and development in the form of assets and management entities. Therefore, real estate can be acquired, transferred, improved, changed and destroyed. All these processes require valuation of real estate objects based on availability of functional, financial and physical components. Time-lagged estimates of this kind may vary significantly, because they depend largelyon methods used in making valuations, market fluctuations, location, purpose, modes of operation, and many other factors that affect the level of real estate value. Therefore, methods and processes of real estate valuations need to be studied, because this process has many specific features that distinguish it from the way other products, goods, works or services are evaluated that act as a result of human activity.

Often, methods of assessing the real estate and the results are beyond the direct ownership and management of it, because they are affected by political, social, general economic changes, emerging risks and taxation system, which requires real estate appraisers to globally look at many current and future processes, see their interrelation and mutual influence, as well as the ability to determine strategic directions and prospects for the development of this type of market.

Since the real estate market belongs to the resource market, it is affected by all the same factors that are typical for the resource market. This is not only demand, supply, competition, level of socially necessary labor inputs, average industry profitability level, state of the financial sphere, and level of government intervention in conditions of this market's functioning that are typical for the existence of a market mechanism for pricing.

In accordance with its definition, the market value of a property object depends on those factors that determine the average or more probable price of its sale on the market under normal transaction conditions.

On the first level of classification, they can be subdivided into objective and subjective factors.

In determining the market value, objective factors are considered. As for subjective factors, they are related to the behavior of a particular buyer, seller or intermediary when concluding a transaction in part not directly determined by its economic conditions (awareness, honesty, patience, gullibility, personal likes and dislikes, etc.). Objective factors are mainly economic, and ultimately, the average level of prices of specific transactions.

Economic factors can be subdivided into macroeconomic and microeconomic factors. The first include factors related to the overall market situation: the initial level of supply of real estate need in the region; volumes and structure of new construction and reconstruction; migration factors; legal and economic conditions of transactions; level and dynamics of inflation; dollar rate and its dynamics. In our conditions, the following long-term factors may also be included in the group of economic factors:

- differences in dynamics of prices for goods and services, as well as terms of payment that affect the scale of cash accumulation and amount of deferred demand;

- pace and scale of the formation of a new social stratum that has the potential to invest in real estate;

- development of the mortgage system;

- development of the system of foreign missions in the region [1].

Microeconomic factors characterize the objective parameters of specific transactions. Of these, those, which describe the object of transaction (apartment), are especially important. Significant are also the factors that are related to the nature of the transaction and the terms of payments. The main procedures of registration of transactions and their payment have been workedthrough. Therefore, for mass valuation of the market value of apartments one may and should focus on typical (medium) nature of the transaction, consider this factor constant and not consider it when assessing the market value of apartments. Then the market value (average price) of an apartment estimated at a fixed date is conditioned by its parameters (characteristics) as a use value.

To assess the impact of the main factors in the real estate market and develop a forecast based on average annual data, a correlation-regression analysis was conducted for the period from 2007 to 2015 and paired correlation coefficients were obtained. They determine the tightness of a relationship between the variables. Along with the dynamics of dollar for analysis, the most significant macroeconomic factors affecting the real estate market were selected: х1 — the dollar to tenge rate; х2 — volumes of mortgage crediting; x3 — world oil prices; x4 — nominal income of residents (Tables 1, 2) [2].

Table 1

Main factors affecting the real estate market

|

Factor name |

2007 |

2008 |

2009 |

2010 |

2011 |

2012 |

2013 |

2014 |

2015 |

|

Average supply price, tenge/sq.m |

259152 |

220870 |

197745 |

192168 |

230597 |

262701 |

304498 |

369180 |

358310 |

|

Dollar to tenge rate |

120,82 |

119,994 |

150,34 |

146,713 |

146,99 |

150,41 |

152,921 |

183,507 |

221,73 |

|

Volumes of mortgage crediting, billion tenge |

111,3 |

100,9 |

97,7 |

102,6 |

115,4 |

129,9 |

153,62 |

175,43 |

177,6 |

|

Oil price, dollar / barrel |

72,7 |

97,7 |

61,9 |

76,6 |

111 |

121,4 |

108,8 |

98,9 |

55 |

|

Level of nominal income, tenge |

48669 |

65 590 |

70 705 |

83 787 |

80495 |

90409 |

98665 |

116249 |

128035 |

To perform the correlation analysis, we use the «Data Analysis» package of the MS Excel application. Let's calculate the matrix of pair correlation coefficients.

Table 2

Level of correlation between factors in the real estate market

|

у |

Х1 |

Х2 |

Х3 |

Х4 |

|

|

у |

1 |

||||

|

Х1 |

0,737778 |

1 |

|||

|

Х2 |

0,974044 |

0,825635 |

1 |

||

|

Х3 |

-0,00928 |

-0,35126 |

0,008996 |

1 |

|

|

Х4 |

0,774979 |

0,924091 |

0,887561 |

-0,03044 |

1 |

The analysis has shown that property prices are the most sensitive to mortgages and incomes. Their dependence is 97 % and 77 % respectively.

Experience shows that during the crisis, the growth rate of mortgage lending volumes falls from a level of +1 % to -7 % per year. Given the continued positive dynamics of mortgage lending, to calculate the forecast we will use a more optimistic indicator of 1 % of mortgage growth per year. It should also be considered that, as the retrospective analysis shows, during the crisis, nominal incomes of the population do not grow, but in real terms, they fall by an average of 2.5 % per year. The average price of oil in 2015 was $ 55 per barrel. We use these parameters as a basis for calculating the forecast, at the same time we assume different versions of the dollar exchange rate [3].

- An example of the crisis 2007—2009 shows that a decline in the parameters of economic growth inevitably leads to a decline in housing prices. At the time, the tenge price had been declining for about 3 years in a row and lost a total of 30.5 %. The dollar price also showed an impressive decline of about 50 %. Other conditions being equal (a slowdown in mortgage growth to 1 % per year, a decrease in real household incomes and an average annual price of oil at $ 55-60 per barrel), the decline in tenge prices in the housing market before the end of 2017 will be 15-20 %.

- One-time devaluation by 25 %. As the situation is aggravated by other factors compared to 2009 (a longer and deeper fall in oil prices, economic sanctions), many experts predict a further 25 % devaluation, or up to 385 tenge per dollar. In this situation, due to the growth of the tenge price of housing, the average annual rate of growth in prices in tenge will end by the end of 2017, and the subsequent correction will stretch to 2018 and amount to another 15-20 %. The dollar price under this scenario will reduce by another 30 % within a year and a half [4].

Table 3

Forecast of indicators and rates of change in prices in the housing market until the end of 2017 for different values of the tenge to dollar exchange rate

|

Values and average annual increase, % |

||||

|

Dollar rate |

Mortgage lending Volumes |

Nominal income |

Oil price |

Rate of price growth in housing market |

|

221,73 tenge per dollar |

+1 % peryear |

0-0,3 % per year |

$55-60 per barrel |

minus 14-15 % intenge |

|

385 tenge per dollar |

+1 % peryear |

0-0,3 % peryear |

$55-60 per barrel |

minus 2,5 % -plus 1,9 % intengein 2017 and minus 15-20 % in 2018 |

As the analysis shows, investments in foreign currency and pegging of real estate prices to dollar, despite good benefits in the short term, have a negative effect in the long term. Strong dependence on dollar leads to a number of problems, one of which is the impoverishment of the bulk of the population receiving income in tenge. Only those win on the market who profit in time by selling their property at the peak of prices (and this peak has already passed). Basing on the new market reality,it is possible to recommend to citizens to focus, first, on dynamics of tenge prices and on announcements denominated in tenge. One can also get a stable income from renting an apartment. Thus, even in «bad» times, provided

long-term investment, the profitability of housing will be approximately at the level of yield of tenge deposits and will be insured against inflation.

Let us analyze the prices of the real estate market in Kazakhstan in 2017.

2017, as well as 2016, proved to be difficult for the Kazakhstan's real estate market. First, the transition to a floating exchange rate, and then the ban on the nomination of prices in dollars caused many difficulties in terms of pricing for all market participants. It would seem that against the backdrop of rising inflation and a decrease in people's incomes, house prices should fall, but against the backdrop of currency shocks, the tenge price tags were only able to regain the difference in rates [5].

The outgoing year turned out to be tense and eventful for the Kazakhstan's real estate market. In the first half of the year, de-dollarization was declared, in the second half of the year, a new state program «Nurly Jer» was announced. And all this against the background of an unstable exchange rate. For these reasons, the expectations for the next year are very different for sellers and buyers.

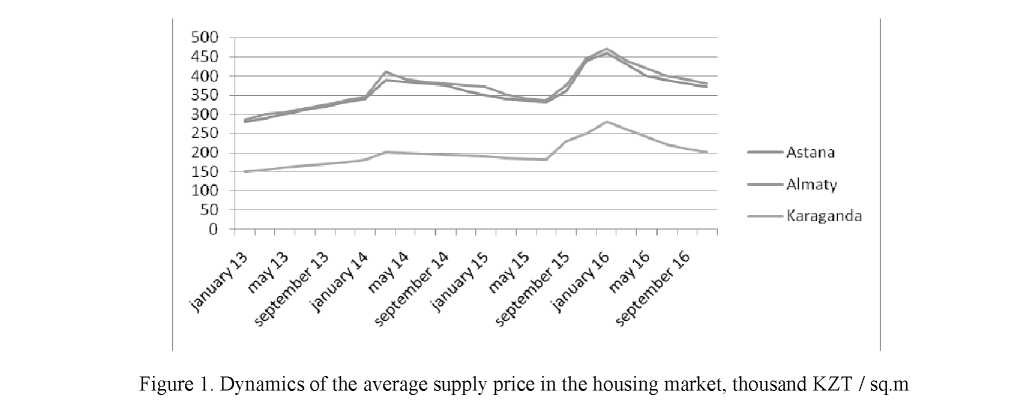

In 2017, prices for apartments have declined significantly. Despite the ban on the nomination of real estate prices in foreign currency, pricing in the secondary market is still tied to the dollar equivalent. For this reason, the dynamics of tenge prices in 2016—2017 was mainly due to fluctuations in exchange rates, which is clearly seen in Figure 1.

By now, in fact, the tenge price has retreated to the level of the beginning of 2014, that is, by the time of the first devaluation, which indicates the stagnation of housing prices in the last 3 years.

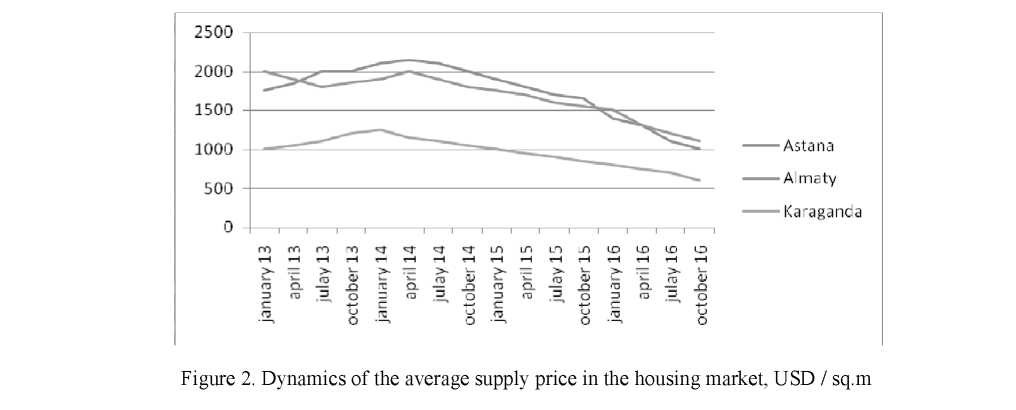

Of course, the same cannot be said about the dollar price. The dynamics of the indicator in dollar equivalent shows that since the beginning of 2014, it has fallen by an average of more than 50 %, including 21 % in 2016 (Fig. 2).

In 2016, against the background of the general crisis, the domestic real estate market continued to develop under the auspices of EXPO-2017 and the continuation of public housing programs implementation. In 2017, peaking volumes of new housing were introduced in the country, the bulk of which fell on Astana.

The volume of commissioning of new housing in the capital in 2017 exceeded 2 million sq.m, whereas before the announcement of EXPO, the average annual input did not exceed 1.3 million sq.m.

Along with this, during 2017, the domestic housing market continued to have negative trends expressed in a decrease in the mortgage lending volume. The growth of the dollar rate by more than 80 % over the past year has led to an increase in the cost of currency savings of the population, which share in the total volume was about 70 %. The growth in the value of currency deposits on the background of price lowering in the secondary market has led to an increased demand in regions with high incomes [6].

Dynamics of registered transactions for the sale of apartments in some regions over the past two years showed significant growth. For example, in Astana this year the volume of transactions on the market has increased by 61 %, in Almaty by 48 %, in Aktau by 42 %, in Shymkent by 18 %. In Karaganda, the growth was not so significant and amounted to 4.7 %.

In regions with low and medium incomes during the year, demand fell or remained at the same level (Fig. 3).

By the end of 2016, average housing prices fell by 18-28 %, depending on the city. As can be seen from Table 4, prices dropped the most in Shymkent - 28 %, the least in Karaganda - 18 %. In Aktau, the rate of decline was 25 %.

Table 4

Average prices for housing in cities of Kazakhstan

|

City |

Average price, KZT /sq.m |

Deviation by November |

DeviationbyNovember |

|

(November 2016) |

2015, KZT/sq.m |

2015, % |

|

|

Astana |

354 255 ~ |

-105 741 |

-23 % |

|

Almaty |

377 924 |

-104 194 |

-22 % |

|

Aktau |

290 000 |

-98 840 |

-25 % |

|

Karaganda |

207 774 |

-46 738 |

-18 % |

|

Shymkent |

198 340 |

-77 000 |

-28 % |

Property prices will decrease in 2018. Despite the beginning of a weak increase in commodity prices since the beginning of 2017, the analysts' consensus forecasts for the oil market for the coming years remain rather low-key. Leading international investment banks predict an average price for oil not higher than 50 KZT / barrel in the current year and an average of 56 KZT / barrel in 2018.

According to Bloomberg, the consensus forecast for Brent crude oil prices from 25 leading financial and consulting companies for 2018 will be 52.9 KZT / barrel. The International Monetary Fund (IMF) in its World Economic Outlook report has reduced the forecast for the growth of the economy of Kazakhstan in 2017 to 0.1 percent. At the same time, the inflation forecast for the following year was 9.3 percent.

Among the reasons, the IMF names a deep recession in Brazil, Russia and a weak economic growth in Latin America and the Middle East.

In the absence of long-term funding, banks note a low interest in issuing mortgage-housing loans in the medium term. Along with this, demand is also affected by negative factors: high interest rates on loans and uncertainty in projections for the cost of housing.

The main operator providing preferential mortgage lending is Zhilstroysberbank. However, in conditions of uncertainty and liquidity decrease, it also reduces the volume of issuance. Inadequate supply of credit resources from banks leads to the fact that customers who want to buy housing, go directly to the owners, bypassing financial institutions, and find new acceptable conditions for payment settlements (installments, barter and other types of settlements).

An additional test for the capital's real estate market in 2017 was its oversaturation after the end of the EXPO exhibition. In 2016, developers have created a two-year stock of real estate, which is to be sold in the coming years. Against the backdrop of high supply volumes, decreasing revenues and difficulties with mortgages, prices will have to decline.

Thus, it is expected that prices in the housing market in 2018 will tend to decline.

What does the theory of cycles in the economy predict?

The fact that prices in 2018 have yet to fallis also stated by the theory of cycles in the economy. The French economist, Clement Juglar, has studied 7-11 year long investment cycles. In each cycle, Juglar has singled out two main phases: the phase of recovery and the phase of recession. In Juglar's cycles often, but not always sub-phases are distinguished:

- phase of recovery (subphasesof start and acceleration);

- phase of expansion or prosperity (sub-phases of growth and overheating, or boom);

- phaseof recession (sub-phases of collapse / acute crisis and recession);

- phase of depression or crisis (sub-phasesof stabilization and shear).

As the research of the analytical service kn.kz shows, in the dynamics of prices in the real estate market, one can already single out two medium-term cycles, the first of which lasted 9 years.

The period of the first cycle lasted from 2000 to 2009. The phase of recovery and expansion began in 2000 and ended in the summer of 2007. The phase of recession, crisis, recession and stagnation began in August 2007 and ended in the fall of 2009. The total duration of the first cycle was 9 years, of which 6.5 years took the recovery phase and the recession phase lasted for 2 years. The period of the second cycle began in the autumn of 2009 and continues to the present. The phase of expansion and recovery of the second cycle began in the autumn of 2009 and ended in February 2014.

The phase of recession, crisis, decrease and stagnation began in February-March 2014 and continues to the present. In the second cycle, the recovery phase lasted 4.3 years, in 2014, we entered the recession phase, which has been going on for 3 years. However, as seen on the chart in 2015—2016, we were in a phase of slowdown and stagnation, which is to be followed by a real decline. Considering such fundamental factors as falling of the populationincomes, volumes of mortgage crediting and restrained forecasts of economic growth, in the coming year we will see a continuation of negative price dynamics. How long can this last? Assuming that the second cycle will be the same in duration (9 years), then the economy and real estate market will begin to recover only in 2018.

Under current conditions, the depth of the fall in prices in 2018 may be 10-15 % with an average drop rate of 0.8 % -1.25 % per month. But it is worth noting that the dramatically changing situation on the world market sometimes forces theadjusting of positions and revising of forecasts. In addition, next year the government and international experts forecast an economic growth of 2-2.5 %. This will support the real estate market as well, but it will have a deferred impact on the market and is unlikely to lead to an increase in prices [7].

So, let's summarize. The study showed that many different factors affect the prices of the real estate market. The most significant factors are the dollar to tenge rate, mortgage lending volumes, world oil prices, nominal incomes of the population. Correlation-regression analysis showed that property prices are the most sensitive to mortgages and incomes.

The main driver of the market was the state housing program «Nurly Zher». The updated program, launched at the beginning of the year, affected all areas of the primary housing market and returned second- tier banks to the mortgage market. The activity of the state has led to a doubling of the mortgage loans volume for ten months. The activity of the program «Nurly Zher» increased the demand for new buildings and increased the flow of customers to the primary market. On the one hand, it supported prices for new squaremeters, on the other - increased the downward trend in the secondary market. Today there is an active construction. There are a lot of social programs and social projects. The only thing would like to see is some more good soft loans related to mortgages.

References

- Kasyanenko, T.G., Makhovikova, G.A., Yesipov, V.E., & Mirzazhanov, S.K. (2015). Otsenka nedvizhimosti [Property valuation]. Moscow: KNORUS [in Russian].

- Utkin,V.B. (2015). Ekonometrika [Econometrics]. Moscow: Dashkov and K°[in Russian].

- Nivorozhkina, L.I., & Arzhenovskiy, S.V. (2009). Mnohomernye Statisticheskie metody v ekonomike [Multidimensional statistical methods in Economics]. Moscow: Dashkov and K [in Russian].

- Sait nedvizhimosti v Kazakhstane [Real estate website in Kazakhstan]. tengrinews.kz. Retrieved from https://tengrinews.kz/ [in Russian].

- Ofitsialnyi internet-resurs Komiteta po statistike RK [Official Internet resource of the Committee on Statistics of the Republic of Kazakhstan]. stat.gov.kz. Retrieved from stat.gov.kz [in Russian].

- Natsionalnyi analiticheskii sait [National analytical website]. kn.kz. Retrieved from kn.kz. [in Russian].

- ocenka-uko.kz. Retrieved from www. ocenka-uko.kz

- fin-izdat.ru. Retrieved from www.fin-izdat.ru/journal/analiz.