In the article the features of the development of light industry sector in the consideration of the emergence in global market are discussed. The features of light industry are the insignificant need for capital investments, constant growth, rapid capital turnover. Therefore, this industry has become the starting point in the economics of developed countries, and in developing countries it is considered with high priority. This paper presents the experience of the development of light industry in China, Turkey and Kyrgyzstan, where there is a constant increase due to the steady increase in demand for products. Through the implementation of a wellthought-out strategy covering the macro, industry and micro level, the success of light industry development has been achieved in most countries. Light industry as an industry is a set of enterprises, producing goods that compete with each other and meet similar needs. The demand for light industry products is constantly growing. Buyers increasingly prefer high-quality goods, although in the recent yeas price was the determining factor when choosing a product. Light industry is a powerful diversified complex, both in the production of consumer and industrial goods, and carries out both the primary processing of raw materials and the production of finished products.

Considerable attention is paid to the development of light industry in many countries of the world, since this industry has considerable socio-economic importance, ensuring high employment of the able-bodied population, particularly women's population, reducing social tensions and improving the standard of living of the population. One of the main advantages of this industry is that in terms of consumption it occupies the second position after the food products consumption.

The share of light industry in total industrial production in developed countries (Germany, USA, Italy, France) is 6-12 %. In Korea and Japan, this industry positioning at the second place in terms of marketable products after the automotive industry. Therefore, up to 20 % of the budget of these countries is formed due to the sewing and textile enterprises. The production of ready-made clothes, fabrics, knitwear, shoes for 75-85 % satisfies domestic demand. Significant government support for light industry in developing countries (China, Turkey, India, Mexico) led to rapid growth in the industry. Over the past two decades, the production center (especially in the textile industry) has shifted to Asia and South America, gradually replacing the United States and Western Europe. This traces another feature of light industry — countries with low labor costs lead in it.

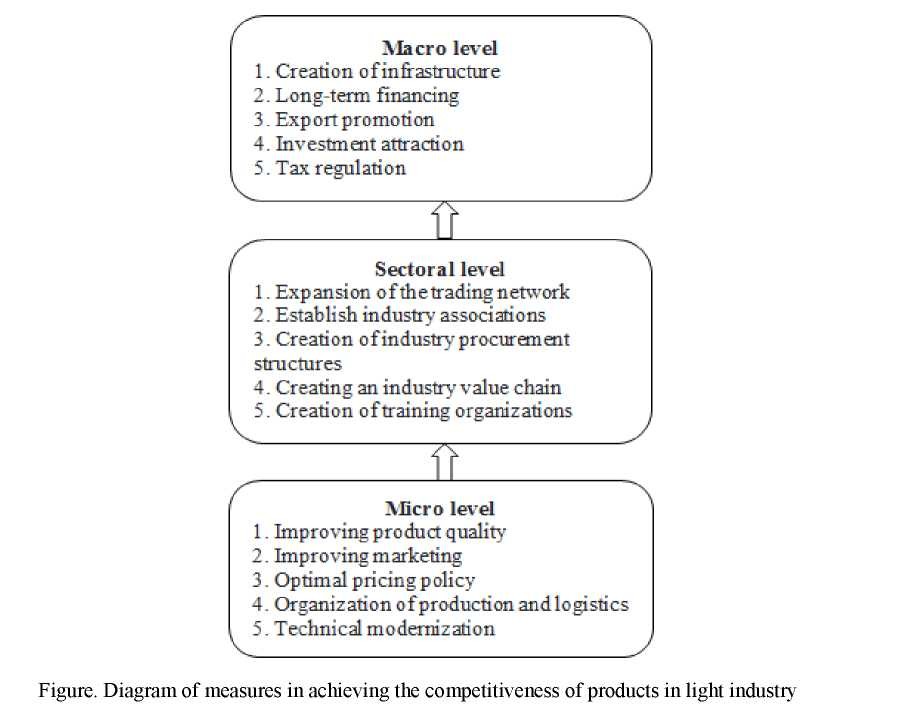

International experience shows that achieving competitiveness in the light industry is the result of well thought-out development strategy pursued at three levels: macro, sectoral and micro levels. Figure shows a diagram of the major events held at every level.

China's economy is a prime example that the development of light industry can be an effective basis for the construction of an industrial society. Light industry is traditional for this country. Nowadays, light industry leads China in industrial production and accounts for 21 % of total production (currently there are more than 360 industries in the country) [1].

Chinese textiles, clothing, leather goods, shoes are exported to almost all countries of the world. Today, China dominates the world trade in consumer goods accounting its share of 20 %. In competition, China gradually ousted its most important rivals — Turkey and Mexico, being the most important supplier of textile products in the United States.

The key factor in achieving the competitive advantages of Chinese products is their low cost. Annually, exports of Chinese textile products increase by an average of 6 %. Only in 2008, due to the global financial crisis, exports of Chinese textiles decreased by 9 % (in other countries this decrease reached 16 %). With the recovery of the economic situation, the growth of Chinese textile exports amounted to 23.6 %, and that of garments — 21 %.

A sharp rise in China's light industry occurred in the 1980s, when this industry became a key link in the economy. The growth of the industry was promoted by the application of the experience of developed countries and the introduction of five-year development programs into practice by the government [2]. The textile industry developed most rapidly, and today it is predominant among other industries.

The success of the Chinese light industry contributed to a combination of factors, the main of which is the presence of a large number of cheap labor. Another very important aspect is the availability of its own raw materials, which fully meets the needs of the industry (China is the world leader in the production of flax, cotton, wool, etc.).

A major role in the growth of the industry was the creation of an industrial infrastructure. This was facilitated by the feature of concentration of industries in cities and provinces that specialize in the production of certain types of products. For instance, the textile industry is concentrated in small towns of the provinces of Guangdong, Zhejiang, Changshu, Liaoning. Some cities specialize in the production of certain products (for example, Shengzhou — the production of ties, Yuhan — the production of fabrics, Jimo — knitwear). Small towns and villages have a narrow specialization (for example, Datan specializes in the production of socks, Fengqiao — in the manufacture of men's shirts) [1].

At present, the state's economic policy is oriented in industry (including light) export. One of the major goals of the government is to increase the export of high value-added goods and reduce the export of commodities. For this purpose, incentive measures are applied — the provision of concessional targeted loans to produce finished products with high added value, intended for sale abroad.

Thanks to the achieved competitive advantages, China's light industry will lead the world market for many years. However, there are certain risks that the Chinese clothing and textile industry faces today.

Firstly, it is the increase in material costs. In the past 10 years, the cost of cotton has more than doubled and the trend is growing. The cost of synthetic fibers increases, which may cause the loss of cheap goods.

Secondly, the cost of labor increases, which relates to the introduction of new labor legislation since 2008.

Thirdly, the lack of qualified personnel. Low qualification of the staff does not allow to produce high- quality products. Today, buyers seek to choose good quality clothing and textiles at an affordable price.

Last, but not the least, the growth of the exchange rate of the Chinese yuan against the dollar leads to higher prices of exports.

Overview of light industry in Turkey

Due to a combination of different strategies, light industry in Turkey is actively developing.

Nowadays, this country is the largest supplier of textiles and clothing in the world market, and among exporters to EU countries, Turkey occupies the second position, second only to China. Turkish light industry accounts for 10 % of GDP and provides 40 % of budget revenues (in the country's economy, this sector is ahead of tourism only). The export of the country is also dominated by light industry products (ready-to- wear, textiles, products made of yarn, carpets, synthetic and textile fabrics, wool and articles thereof) — 40 % [3].

Since 1933, the Turkish government has fully taken the patronage of the industry. The textile industry has been declared a priority. Light industry was raised through lending, the use of own budget funds and foreign investment, the modernization of equipment and production, and the training of personnel abroad.

For purpose of lending to the light industry in 1933, the government of Turkey established the state holding Sumerbank, which functioned for several decades (Sumerbank was privatized in the early 1990s). As a result, over a short period, the volume of production of light industry increased by 60 %, including cotton fabrics — by 65 %, woolen clothes and fabrics — by 45 %, leather goods — by 36 %. The number of textile, shoe, and garment enterprises has increased significantly.

Until the 60s of XX century, the main goal of supporting the development of light industry in Turkey was to meet domestic demand, import substitution and market saturation with domestic goods. This goal was successfully implemented, and by 1970, Turkey almost completely abandoned clothing imports.

Since the early 1980s, the Turkish government has adopted a new strategy for the development of light industry, according to which the industry has become actively reoriented towards exports. The need for such an economic policy was caused by the acute need of the country for the inflow of foreign currency.

To implement the new strategy, a set of incentive measures was implemented:

- provision of preferential loans to exporters;

- state insurance of export operations;

- reimbursement of expenses for research and development;

- partial or full refund of taxes included in the cost of export goods;

- increase import duties on imported products.

The result of this policy was a sharp jump in exports of the Republic of Turkey (over ten years, the export of Turkish clothing and textiles increased almost 22 times). There was a significant increase in the number of enterprises operating in the light industry.

Due to the stable state of the industry and export growth, Turkey remained a relatively stable state before the global financial crises.

The next stage in the development of light industry in Turkey was the need to improve the quality and competitiveness of products. There was a demand for a new quality that meets European standards and a new image that would enhance the prestige of the goods. To achieve this goal, since the beginning of the 1990s, a massive technical and technological modernization of the industry has begun. This entailed significant investments and, as a result, light industry products lost their cheapness — the main factor in the competition. It was inevitable in the early stages of introducing new equipment. However, a new trump card was acquired — now the products meet European quality standards and meet modern fashion trends. In addition to the modernization of equipment and technologies, measures such as the introduction of modern principles of production and management, and staff development were taken.

Currently, the light industry of Turkey occupies one of the leading positions in the world. The leading role in this belongs to the textile industry, which competes with recognized world leaders — Germany and Italy. The textile industry in Turkey is rightfully considered the «face» of the republic's economy. Even the presence of many domestic raw materials is not able to meet the needs of the industry. Therefore, the country is forced to import raw cotton and cotton threads from Italy, India, Pakistan and Egypt.

In addition to textile production, Turkey has been successfully engaged in the apparel industry, synthetic fibers, wool and leather products, carpets, yarn and fabrics.

By equipment with technological equipment, Turkey occupies one of the leading places in the world. The use of high-quality raw materials allows to produce competitive products.

The success of the establishment and development of light industry in Turkey has contributed to:

- implementation of well-thought-out government strategies, timely and accurate implementation of state programs for the development of the industry;

- active interaction of business and government;

- attracting foreign direct investment;

- the presence of favorable climatic conditions for the cultivation of cotton crops and sheep (for wool);

- the timely creation of a well-established industry infrastructure, which was greatly facilitated by the presence of traditional ancestral and family ties;

- the creation of a closed industry cycle from the receipt of raw materials to the creation of finished products with high added value, established links between the links of the industry chain, business cooperation;

- active promotion of products to the market by manufacturers (in particular, holding of specialized exhibitions);

- orientation of the industry to the changing needs of the market.

Iowever, Turkish light industry is not without its weaknesses:

- the complication of the supply of raw cotton (due to the increased demand for raw materials) to the country due to Turkey's accession to the EU Customs Union and the increase in customs tariffs on goods of supplying countries;

- low qualification of staff compared with EU countries, poor knowledge of foreign languages, which impedes international entrepreneurship;

- insufficiently adjusted management, which entails lower labor productivity than in competing countries;

- weak marketing, in particular, marketing communications.

The following measures are planned to support and grow Turkey's light industry [4]:

- the involvement in the agricultural circulation of arid lands through the construction of dams, which will contribute to the growth of agricultural crops, diversification of the production of raw cotton;

- professional development of production personnel, training of new generation specialists;

- improving the organization of production and management;

- further work on improving product quality.

Overview of light industry in Kyrgyzstan

The point of interest lays in the experience of development of light industry in Kyrgyzstan.

Over the past decade there was a sharp rise in the industry. The light industry of Kyrgyzstan forms more than 10 % of GDP, its share in total industrial production exceeds 16 %, it employs 30 % of the working-age population (about 150 thousand people). The garment industry is developing most successfully (other subsectors — textile, leather, footwear — are currently lagging in the development of the garment industry). Ready-made garments of Kyrgyzstan production are successfully sold in the CIS countries, especially in Russia and Kazakhstan, they are able to compete with similar products of Chinese and Turkish production due to acceptable quality at a low price [5].

The main target segment for Kyrgyz clothing manufacturers is the Russian market. Produced collections are intended mainly for the middle class. In general, products are sold in clothing markets. Models are developed by the owners of enterprises, considering the tastes of consumers. Information about fashion trends is obtained from fashion magazines, thus, professional fashion designers are usually not hired. Buyers' preferences are determined without marketing research, but by direct contact.

In recent years, the technical equipment of enterprises has significantly improved. Iowever, the age of the equipment used at different enterprises varies: from Soviet technology, which is 50 years old, to the newest machines, equipment for design and cutting, as well as computer programs for modeling and design. Mainly technological equipment comes from China.

The emergence of Kyrgyz industry, including light, began even before the October Revolution. It was represented by workshops with a handicraft production method. From 1928 to 1940, the light industry of Kyrgyzstan began to develop intensively. Fifteen large factories were commissioned, including those for the production of garments, fabrics, wool processing, a shoe factory, two tanneries and a silk spinning mill. During the Great Patriotic War, light industry enterprises were evacuated to the territory of Kyrgyzstan, and on their basis knitwear and garment factories were established in the republic. During this period, the number of light industry enterprises doubled.

In the 1960s, there was a significant growth in the industry. The enterprises were reconstructed, the technological process was automated. In a relatively small area, all new enterprises were created. Thus, by the time independence was gained in Kyrgyzstan, light industry had become the most developed sector in the country's economy. Especially the textile industry was developed (knitwear, wool, cotton enterprises). The largest sewing enterprises are concentrated in the cities of Bishkek, Osh, Talas. The largest silk spinning mill functioned in the city of Osh. Wool sub-industry produced 90 % of all wool fabrics produced in Central Asia [5].

Since 1994, due to the economic crisis, there has been a decline in all industries, including the light one. The share of the industry in the total volume of industrial production gradually decreased and amounted to 8.5 % in 2000 (in 1994 this figure was 30.4 %). The decline was observed in almost all sectors of the light industry, only the garment industry was stable and growing.

Since 2000, the government of Kyrgyzstan began to take decisive measures for the rehabilitation of light industry. The main government measure was the provision of tax incentives to manufacturers. The situation began to improve in a short time.

However, related industries of light industry began to develop unevenly and independently from each other, a closed industry chain ceased to exist. Cotton production declined as farmers moved to grow more profitable crops. Wool production was also insufficient, as farmers switched to raising more profitable sheep meat breeds. As a result, the previously leading textile industry was in a critical condition. Silk production has almost stopped.

The exception was the production of ready-made clothes. This is due to the creation of competitive advantages. Today, the garment industry of Kyrgyzstan produces high-quality and low-cost products that can compete both in the domestic and foreign markets. This industry proved to be resistant to the global financial crisis of 2008 and difficulties in the country's energy sector. However, the garment industry of Kyrgyzstan is dependent on imported raw materials. Local manufacturers of textiles are not able to provide them with raw materials and materials either in quantity nor quality. In addition, local textiles are not able to compete with imported textile at a price. Therefore, 90 % of the raw materials used for the clothing industry are imported into the republic. Sewing accessories and accessories are also imported.

To resolve the situation, the Government of Kyrgyzstan adopted the «Strategy for the Development of the Textile and Clothing Industry of the Kyrgyz Republic for 2010-2011». This program was compiled within the framework of the overall development strategy of the country to improve the efficiency and competitiveness of industries based on funding and a clear business plan [5]. One of the most important planned measures is the restoration of the national value chain and a focus on the output of final products. The strategy provides for organizational and economic measures that are carried out at three levels: the macro level, the industry level and the micro level.

At the same time, the state pays attention to the garment sector as the most developed and strong, which makes it auspicious. The revitalization of the textile sector is considered possible with fundamental changes, including the rehabilitation of state enterprises operating in the industry, and the creation of favorable conditions for investors.

Thus, the features that give advantages to the Kyrgyz light industry are as follows:

- low cost of labor, which allows to win in price competition;

- favorable conditions for the import of products, especially to the Russian markets;

- favorable financial conditions for the implementation of activities;

- availability of state support in the tax direction;

- the ability to produce good quality products at low cost. Weaknesses include:

- the absence (or lack) of local raw materials, fabrics, accessories, as well as dependence on foreign suppliers;

- high staff turnover (due to harsh working conditions);

- low staff qualifications;

- low level of marketing, insufficient knowledge of sales markets;

- poor level of business relations with suppliers of raw materials as well as relations with consumers.

The danger for the light industry of Kyrgyzstan can be represented by the producers of Southeast Asia, whose products lead in sales in the world. Russia's accession to the WTO complicates the situation, as opportunities for imports of Chinese garments and textiles increase.

In such circumstances, the strategic directions of development of light industry should be based on the following principles:

- careful study of demand, improvement of the range;

- strengthening competitive advantages;

- system regulation of the industry value chain;

- creating a favorable investment climate and the development of public private partnership in light industry.

References

- Doklad o razvitii malykh i srednikh predpriiatii Kitaia v 2005 hodu [China SME Development Report 2005] (2006). Moscow [in Russian].

- Politika v oblasti razvitiia maloho i sredneho predprinimatelstva v KNR [Development policy for small and medium-sized businesses in the People's Republic of China] (2010). Moscow [in Russian].

- Simay K.H., & Deniz N. (2013) Comparative advantage of textiles and clothing: evidence for Bangladesh, China, Germany and Turkey. Fibres and Text. East. Eur., Vol. 21, No. 1, 14–17.

- Yepanchintseva, S.E. (2016). Mirovaia lekhkaia promyshlennost: sovremennye osobennosti i tendentsii [World light industry: modern features and trends]. Vestnik Kazakhskoho natsionalnoho universiteta. Seriia ekonomiicheskaia – Bulletin of Kazakh National University, No. 4, 23–29. Almaty [in Russian].

- Stratehiia razvitiia tekstilnoi i shveinoi promyshlennosti Kyrhyzskoi Respubliki na 2010–2011 hody [The development strategy of the textile and clothing industry of the Kyrgyz Republic for 2010–2011] (2011). Bishkek [in Russian].