This article summarizes the theoretical concepts of controlling. As practice shows, strategically oriented management requires comprehensive information, analytical, organizational and methodological support, which cannot be fully ensured in the framework of management accounting and control. Controlling must satisfy this need, which represents an effective form of support for management functions. The emergence and evolution of controlling as a tool for managing a company are due to the development and complication of the structure of market relations that change the internal and external environment, so controlling became the result of the formation of a new concept of business management. The content of the definition of controlling foreign and domestic economists is disclosed. Two types of controlling, operational and strategic, are described, and the main objectives, functions and tasks of controlling are substantiated. Controlling as a system in the management of an enterprise was considered and its main subsystems were identified. The basic concepts of controlling and their essence and tasks are shown. The content of modern methods of controlling is disclosed. The role of controlling in the Republic of Kazakhstan on the example of a large company is considered. It is concluded that the controlling system creates certain advantages for enterprises and affects the socio-economic development of the country as a whole

An important feature of the modern world economy is the activity of its economic agents in the conditions of fierce competition, due to the struggle for markets, information saturation and communication. The modern stage of Kazakhstan's economy pays special attention to the real sector of the economy, the main elements of which are manufacturing enterprises, various trade and intermediary organizations. For the dynamic development of industrial enterprises and organizations, good management is needed. In connection with the transnationalization of the world economy, there arises the problem of interpenetration of competitive, financially-owned firms from developed countries to new markets, which domestic enterprises can not withstand due to a lack of financial and intellectual resources, and also due to the lack of quality management. It should be noted inadequate management in national pension and insurance organizations, as a result of which they become unprofitable, incur losses and, in connection with this, are closed. The need to develop and apply modern approaches and tools in the management and organization of their effective functioning is determined by the orientation of the modern management system to strategic development and the creation of potentials for long-term growth of the enterprise.

Currently, one of the main directions of the enterprise management system development is the development and application of the controlling concept. The concept of controlling is the core around which the basic elements of the organization and management of the enterprise should be combined.

The word «controlling» comes from the English «to control» - to control, which, in turn, comes from the french word meaning the register, the checklist [1]. The term controlling is more commonly used in Germany than in English-speaking countries, where it moved to the CIS countries, and in German the writing of «Controlling», reflecting the English-speaking origin of the concept of controlling, is preserved. Its origin is associated with a change in the organizational management strategy, designed to respond to changing conditions.

Controlling, widely spread in recent years in Russia, Kazakhstan and other CIS countries, represents a separate area of economic work at the enterprise, associated with the adoption of operational and strategic management decisions by top management [1].

In the foreign economic literature, the concept of controlling is quite broad and diverse. Do not confuse «control» and «controlling», as control is one of the functions of controlling. M.Meckon and F.Hedouri understand control as a process that ensures that the organization achieves its goals. According to E. Meier, controlling is the guiding concept of effective enterprise management and ensuring its long existence. R. Gersne and P. Hovart define the concept as a function in support of management, management [2]. The most common definitions of controlling in the domestic literature, which are widely used in the world theory of controlling:

- Controlling - a set of methods for operational and strategic management, accounting, planning, analysis and control at a qualitatively new stage of market development, an unified system of direction for achieving strategic goals of the company [1].

- Controlling - the concept of enterprise management and the way managers think, based on the desire to ensure the long-term existence of the enterprise. It performs the functions of accounting, planning, monitoring and verification, reporting and consultation [3].

- Controlling - a system to ensure the survival of the company in the short term, aimed to optimize profits, in the long-term - to maintain a harmonious relationship with the environment [3].

- Controlling - a system for monitoring and studying the economic mechanism of a particular enterprise and developing ways to achieve the goals it sets itself [4].

Author's interpretation implies under controlling the modern concept of effective management of an economic entity to increase profits and ensure its long-term existence.

Summarizing the above definitions, we can conclude that controlling is a system of profit management of the enterprise.

The main objective of controlling is the orientation of the management process towards the achievement of all the objectives of the organization [4].

Controlling is a new phenomenon in the theory and practice of modern management, which arose at the junction of economic analysis, planning, management accounting and management. An important property of modern controlling is its ability to create prerequisites for a successful operation of the enterprise in the long term based on:

- adaptation of strategic goals to global trends in the development of the external environment;

- coordination of current plans with the strategic plan of enterprise development on the basis of the priority of the strategic plan;

- coordination of current plans for different business processes;

- creation of a system for monitoring the implementation of plans;

- adjustments in the content and timing of the implementation of strategic plans.

In modern theory and practice, various types of controlling are applied, which differ depending on certain parameters and tasks of controlling (Table 1).

Table 1

Classification of controlling types [5]

|

Options |

Types of controlling |

Tasks of controlling |

|

1 |

2 |

3 |

|

By date and purpose |

strategic |

|

|

operational |

|

|

|

optional |

- regulation of plan execution |

|

|

By activity |

controlling production |

|

|

banking controlling |

|

|

|

controlling in small and medium business |

|

|

|

controlling in services |

|

|

|

controlling in agriculture |

|

|

|

in the range of issues under consideration |

risk controlling |

risk management to reduce risk |

|

marketing controlling |

sales policy |

|

|

finance-controlling |

financial policy |

End of Table 1

|

1 |

2 |

3 |

|

ecological controlling |

determining the impact of production on the environment and reducing eco-risks |

|

|

business controlling |

|

|

|

technological controlling |

controlling in the useof technology |

Controlling in the enterprise management system is based on the basic principles that are [4]:

- the primacy of profitability (the efficiency of the enterprise as a whole and its subdivisions)

- measures to ensure profitability growth should not increase the permissible risk levels

- the growth of business volumes of the enterprise is justified only if the previous level or efficiency is maintained

Controlling transfers the management of the enterprise to a qualitatively new level, integrating, coordinating and directing the activities of various services to achieve operational and strategic goals, while dividing the company's objectives into two groups: operational (short-term) and strategic (long-term) [5].

The purpose of operational controlling is the creation of a management system for the achievement of the company's current objectives, as well as making timely decisions to optimize the cost-profit ratio [4].

The purpose of strategic controlling is to ensure the survival of the enterprise and to «track» the movement of the enterprise towards the planned strategic development goals [6]. The establishment of strategic development goals begins with the analysis of information on external and internal factors of impact on enterprises. Before you exercise control over the attainment of any goal, you need to establish whether the goal is justifiably chosen and how realistic it is to achieve it.

Strategic and operational controlling should not be strictly divided, as there is a close relationship between them. They can differ in different models used, but the goals are the same - improving the quality of decisions made. Thus, operational planning strongly depends on the strategic, and, in turn, gives impulses for changing the strategic direction of the enterprise, which in turn forms a direct interaction between the two areas.

According to the existing theory and practice, controlling performs the following functions:

- Informative, which is manifested in the development of controlling information for management, by means of transformation, entering the department of controlling.

- Accounting and control, which is used when:

- comparison of planned and actual values for measuring and assessing the degree of achievement of the goal;

- establishing the permissible limits of deviations from the specified parameters;

- interpretation of the causes of deviations and development of proposals for their reduction.

- Analytical, the essence of which is manifested in the development of the main controlled indicators, allowing to assess the efficiency of the enterprise [4].

The main function of controlling is the quantitative and qualitative preparation and support of the operational and strategic objectives of the company's management.

The tasks of controlling are:

- optimization of organizational structure management;

- organization of an effective system for recording transactions and results;

- implementation of planning, control and analysis systems;

- providing staff motivation to improve the efficiency of the company;

- automation of accounting and management systems [4].

Summarizing the above, we can say that the main taskof controlling in the management of an enterprise is to inform the decision-making process and adjust the work of all divisions to achieve the goals [7].

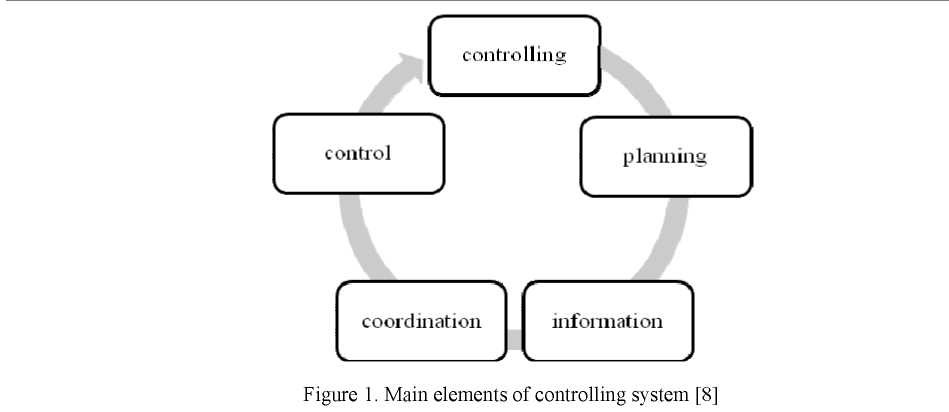

It seems more appropriate to begin the process of controlling from the collection of information, after which the analysis of the data is carried out, after which the activities of the enterprise are planned, then the process of implementing the plan is coordinated and control of the execution of management decisions. In general, the entire process can be depicted in Figure 1. In the German interpretation, the definition of controlling has the designation IPKK, which includes Infromation, Planierung, Koordination, Kontrolle.

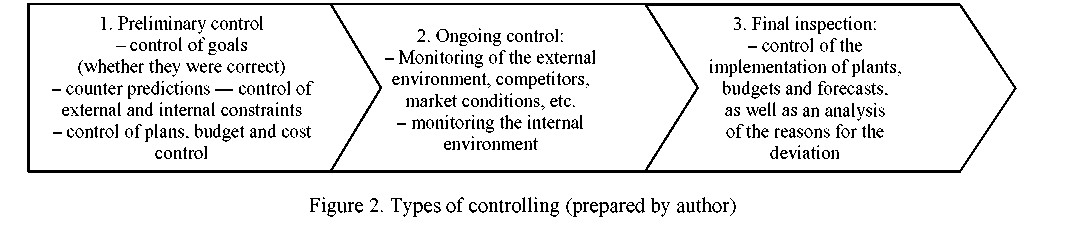

Control, as the most significant stage of the business process is divided into:

- Internal control - detection of negative trends and shortcomings in the activities of the enterprise for taking measures to eliminate them;

- Accounting system and internal audit;

- External control - examination - external auditors

Control as the initial and final stage of controlling is expressed in the assessment of forecasts and the results of the work done. Types of controlling can be grouped as follows in Figure 2:

Controlling as a system includes three subsystems:

- management information system

- budgeting system

- management system by objectives

Each of these subsystems does not reflect, in general, the total volume of problems and achievements of the company, so it is important to analyze and compare the performance of all three subsystems as a whole.

If we talk about the management system by purpose, then every enterprise, ideally, should have a piece of paper, which summarizes the main goals and indicators for assessing the extent of their achievements. One of the most popular methodologies for practical implementation of the concept of management by objectives is the Balanced Scorecard methodology, which presupposes the setting of goals in the projections «Finances», «Clients», «Business Processes», «Infrastructure / Personnel» [8].

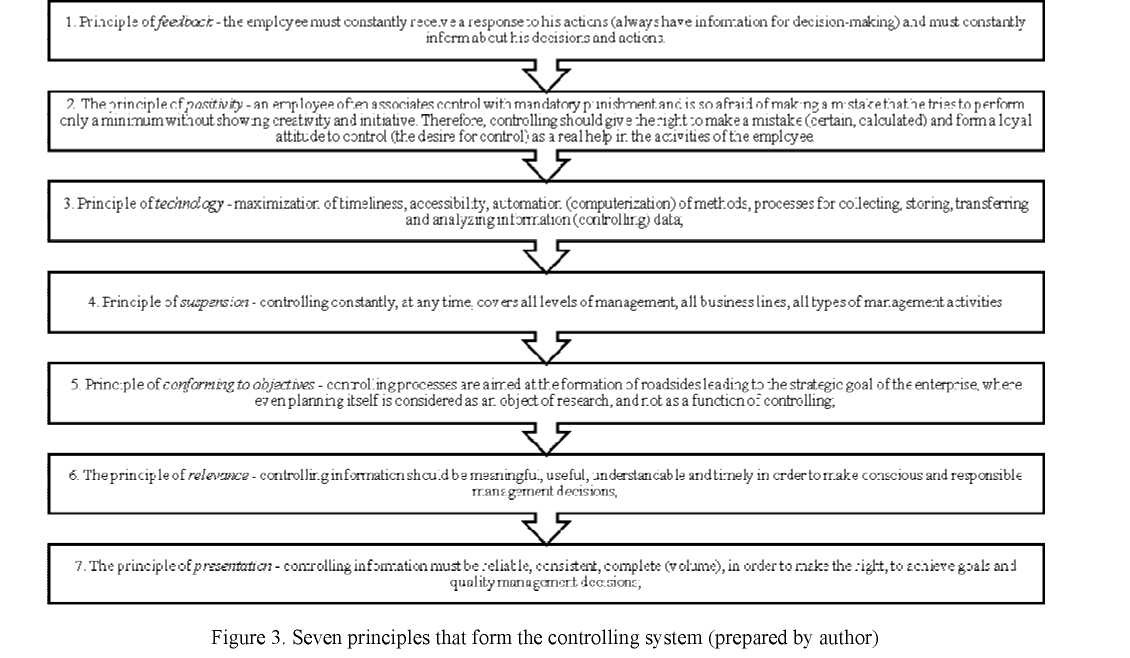

There are seven principles that form the controlling system which are presented in Figure 3.

In general, the controlling system is aimed at:

- achievingthegoal;

- future;

- identification and elimination of bottlenecks;

- processoptimization;

- market;

- client.

For various enterprises, such as production, agricultural, trading, the controlling system may have specific features [6]. In general, these specific features can be divided as follows:

- General industrial controlling: investment and financial controlling, technological controlling, division management, organizational and strategic planning, general management of counterparties, development of enterprises of various types;

- Personnel Controlling: personnel planning and performance measurement through Scanning, «Quali- fied Controlling», engineering work with personnel training in innovation;

- Assortment control: assortment planning, assortment management, assortment control;

- Controlling the use of areas: managing the use of areas based on the scanning of analytical data on the efficiency of the use of areas, the management system of the use of areas;

- Inventory control: the ordering system, the logistics system, the receipt and storage of raw materials and raw materials, the coordination of the work of the warehouse, the shipment of finished products, and so on.

Depending on the scope and direction of the enterprise, the controlling system may become more complicated. Thus, the possibility of applying the controlling system to a particular enterprise requires the advice of specialists in this field of economic science and practice.

The concept of controlling is understood to mean the integration of the institutional level, functional delineation, technologies and instrumental methods in the context of the organization's objectives relevant to controlling, as well as the objectives of implementing the controlling system resulting from the objectives of the organization [7].

The basic concepts of controlling differ in essence and the main control tasks, which are given in Table 2.

Table 2

Basic concepts of controlling [1]

|

Orientationofconcept |

The essence and main tasks of controlling |

|

On the accounting system (was developed in the 1930s). |

The reorientation of the accounting system from the past to the future, the creation on the basis of the accounting information of the information system support for management decisions related to the planning and control of the enterprise. Modeminterpretation - budgeting, orientedtoresult. |

|

On the management information system (was developed in 1970-1980). |

Creation of general information management system. Development of the concept of a unified information system, its implementation, coordination of the functioning of the information system, optimization of information flows |

|

On the management system (was developed in 1990-200- ies) |

Planning and control of the activities of the structural units of the enterprise. Coordination of the enterprise management system |

The set asks and controlling functions are applied bothm to the enterprise as a whole and toitsproduct, functional and regional divisions, as wellas product and service groups, program activities and projects at alllevels of management.

The primary information tool in controlling is the accounting system, which includes accounting, financial, statistical and management accounting. In its unity, these types of accounting provide controlling internal information about resources, their sources, directions and efficiency of use. The accounting system also generates data on the processes and results of activity in the sphere of production and circulation used by controlling companies: a system of target indicators that unambiguously characterize the content of management decisions.

Controlling measures are carried out within the scope of controlling - the actual values of the indicators are compared with the planned tasks. The controlling service forms and submits proposals to the company's management on the expediency of introducing corrective measures based on the analysis of identified deviations.

On the basis of the controlling methodology is the refinement and adjustment of the system of basic indicators characterizing the state of the enterprise as an economic system and the processes of its functioning. The effectiveness of the implementation of management decisions and the company's strategy depends on a properly formed system of analytical indicators that assess the activities of the enterprise. This system of indicators is formed on the basis of current indicators of the functioning of the organization, on information obtained during the analysis of bottlenecks of production [9].

The concept, focused on the management system is directly related to the development of project management, the emergence of matrix organizational structures.

Matrix organizational structure is the type of organizational structure in which for each project implemented at the enterprise a special temporary working group is created, headed by the project manager. Members of this group are subordinated to both the leader and the heads of those functional departments in which they work. When the project is completed, the group disbanded and its members return to their departments. The matrix organizational structure is widely used in the aviation industry, automotive industry, etc. [7].

Controlling provides the development of indicators and techniques used in the analysis of competition. Competitive environment of the organization is constantly changing, which requires monitoring of the external environment. Changes in the market situation include shifts in the ratio of supply and demand, changes in the average market price, changes in consumer requirements for the quality of goods, etc. To form and plan your own competitive strategy, you need information about the state of the market. With this information, the company can identify its own strengths, on the basis of which new strategies will be developed. Within the framework of this strategy, the weaknesses of the enterprise.

An important methodical technique used in controlling is portfolio analysis, which is used to improve strategic planning in the enterprise. The key to the success of the firm is the availability and implementation of portfolio strategies. The company's portfolio is the relative market share, product portfolio, customer portfolio, portfolio of activities. Portfolio analysis also allows to identify the stages of the life cycle and the profitability of individual product groups, as well as to forecast the need to develop new products and determine the financial resources required for this [9].

A well-known method of SWOT analysis is used in controlling. This is an analysis of the capabilities of the enterprise, based on identifying the strengths and weaknesses of the firm (internal analysis), as well as the opportunities and dangers posed by the market (analysis of the external environment). The main opportunities and threats for the enterprise are determined by such conditions as the economic situation in the country, the region; market conditions; technology changes; changes in the demographic situation; the level of political stability. Strengths and weaknesses of the organization include key success factors that have the greatest impact on the performance of the company and determine the situation at the enterprise in comparison with competitors [10].

There are many other effective methods and tools that are used in controlling: STEP analysis covering the social, technological, economical and political aspects of the organization, the method od developing future scenarios, ABC analysis for optimizing the value of inventory, marginal analysis and others. The listed methods and tools are well known, but the specificity of controlling is that it integrates already existing methods intro a single system and thus provides a new quality of information and analytical activity that consists in complex analysis and the possibility of cross-checking the results obtained by different methods.

In Kazakhstan, for the time being, only the foundations for widespread introduction of controlling are being formed. The most active development of controlling is observed in large business and financial centers, such as Astana, Almaty, Atyrau, representing South, Central and Western Kazakhstan, which embodies the principle of regional development in the country's development. As noted in individual works, Kazakhstani developers use the theory and practical experience of American, European and East Asian states in terms of management accounting. Despite significant theoretical work in the field of controlling or management accounting in the United States, as in many countries, the organization of analytical work at enterprises is not systemic, which is primarily due to the individual approach of management of individual firms. Large oil and oil transportation companies use a controlling system, represented by computer programs developed in developed countries. In accordance with these programs, accounting, analysis and planning of the enterprise activity in the current and forecast modes are carried out. Controlling tools are also used by the Kazakhstan Electricity Grid Operating Company (KEGOC). The electric power industry is an indicator of the social and economic development of the Republic of Kazakhstan, as the growth or decline in consumption and, accordingly, electricity production characterizes the overall rate of economic development of the country, and the cost of electricity for a large part of enterprises is a determining cost item in the structure of the cost of production [11].

Based on the analysis, we can conclude that controlling is an important place in the management of any enterprise, and in particular affects the socio-economic development of the country. The studied control theory helped to reveal that controlling creates certain advantages in the management of an enterprise: the high level of transparency of activity achieved through controlling allows to detect weaknesses; realizing the planning function, controlling ensures the management of the enterprise, oriented to the future; the search for solutions becomes more justified and quick; improvement of communication, which leads to a clearer understanding by employees of the interrelations in the economy of the enterprise; through controlling the improvement of personnel management is achieved. All these advantages show the importance of controlling in the management system of an economic entity.

In Kazakhstan, for the time being, only the foundations for widespread introduction of controlling are being formed. Nevertheless, its in-depth study and implementation is necessary today, because it allows using the most modern management methods much earlier than competitors, contributes to the introduction of innovations. The organization of training of professional specialists in Kazakhstan has not yet been widely disseminated and understood, therefore, in this matter, it is necessary to unite with specialists from other countries having a sufficient level of specialization and institutional structure in the field of training and advanced training of controllers.

References

- Tashenova, S. (2011). Kontrollinh [Controlling]. (2d ed.). Almaty: Izdatelstvo MAB [in Russian].

- Abatova, S. (2006). Kontrollinh kak effektivnyi instrument upravleniia [Controlling as an effective management tool]. Tribuna molodoho uchenoho – Tribune of a young scientist, 2, 77-80 [in Russian].

- Falko, S. (2007). Kontrollinh dlia rukovoditeleii i spetsialistov [Controlling for managers and specialists]. Moscow: Finansy i statistika [in Russian].

- Tashenova, S. (2013). Kontrollinh v teorii i praktike: mirovoi i kazakhstanskii opyt [Controlling in theory and practice: foreign and Kazakhstani experience]. Almaty [in Russian].

- Hilmar, I. (2001). Instrumenty kontrollinha ot A do Ya [Controlling tools from A to Z]. Moscow: Finansy i statistika [in Russian]

- Tashenova, S. (2006). Sistema kontrollinha: teoriia i metodolohiia formirovaniia i model razvitiia [Controlling system: theory and methodology of formation and development model]. Almaty: Kazak universiteti [in Russian].

- Petrenko, S. (2008). Kontrollinh [Controlling]. Kiev: Nika-Tsentr; Elha [in Russian].

- Tolkach, V. (2006). Kontrollinh [Controlling]. Biudzhetirovanie. Analiz i uchet na predpriiatii – Budgeting. Analysis and accounting in the enterprise, 2, 27 [in Russian].

- Mezhdunarodnye standarty finansovoi otchetnosti [International Financial Reporting Standards]. (2012). Moscow: Askeri ASSA [in Russian].

- Dauzova, A.M., & Shtiller, M.V. (2015). Kontseptsiia kontrollinha v sisteme upravleniia predpriiatiem [Controlling concept in the enterprise management system]. Vestnik Kazakhskoho natsionalnoho universiteta – Bulletin Kazakh National University, 5, 88–89 [in Russian].

- Tashenova, S. (2010). Rehionalnyi aspekt razvitiia kontrollinha v Respublike Kazahstan [Regional aspect of the development of controlling in the Republic of Kazakhstan]. Vestnik Kazakhskoho natsionalnoho universiteta – Bulletin Kazakh National University, 6, 17-22 [in Russian].