Trends in the development of the modern banking system in the context of the globalization of the financial market and the stagnation of the world economy require consideration in determining the prospects for the development of the credit institution. This article describes the main issues and theoretical aspects of stress testing in banking. The most commonly used method is the scenario analysis. Stress test scenarios containing synchronous changes in a number of risk factors (for example, ordinary share prices, exchange rates, interest rates) reflecting an event that may occur in the future are considered. The models and indicators of stress testing are considered in the course of the research based on the analysis. In particular, a conditional example analyzes the execution of the stress test model based on the factor associated with the growth of the currency exchange rate on the example of the us dollar. Stress testing for stability through the implementation of sensitivity analysis, which calculates the impact of adverse factors that affect commercial banks as much as possible, is carried out on the example of a conditional Bank. It is concluded that stress testing in modern conditions can be one of the perspective instruments of Bank risk management and prevent the emergence of problematic situations in the activities of second – tier banks, regulate the risk operations of banks.

Trends in the development of the modern banking system in the context of globalization of the financial market and the stagnation of the world economy need to be taken into account in determining the prospects for the development of the credit institution, not only the specifics of the situation in the national economy, but also global changes. Therefore, there is a need to constantly modify the tools for assessing and managing Bank risks. In recent years, stress testing has become the most effective tool for risk management in banks.

Stress testing is applied:

- to determine the potential exposure of the Bank to risks in various stressful conditions, which makes it possible to develop or select an appropriate strategy to overcome the risks;

- to identify and understand the Bank's opportunities and risk structure;

- as an analytical tool that assesses the ability of a credit institution to profit and its capital adequacy for stress resistance;

- to identify the amount of losses that banks are willing to incur in case of implementation of this or that scenario, and as a consequence — to set limits on risky operations.

The very first step in creating a stress test is to determine the likely «incoming» shock or a combination of them. For example, the assessment plenitelnogo default (default) all borrowers cannot [1].

It is impractical to carry out stress testing of all risks and potential threats and requires huge efforts due to the need to focus attention on the most important aspects of activity.

Today in the international banking practice the most used technique is scenario analysis (both on the basis of historical and hypothetical events). Another is the sensitivity analysis of the portfolio of financial assets of the Bank to the effect escabrosa factors, and then calculated the maximum loss. Scenario analysis is mainly aimed at long-term assessment of the prospects of the credit institution and allows analyzing the potential simultaneous impact of a number of risk factors on the activities of the credit institution in the event of an extreme, but at the same time likely event. In Russian banking practice, as well as in international practice, the scenarios mainly affect the financial sector: fluctuations in exchange rates, securities prices, interest rates. Also, in the form of expert assessments can take into account possible changes in the customer base: customer outflow, early withdrawal of deposits, etc.

Unlike scenario analysis, sensitivity analysis results are mostly short-term. The sensitivity analysis assesses the direct impact on the credit institution's portfolio of assets of changes in the specified risk factor (for example, growth/decline in the national currency exchange rate; growth/decline in interest rates). The calculation of maximum losses determines the combination of risk factors, their negative dynamics, potentially able to bring the maximum losses of the credit institution. In view of the individual risk profile of eachcredit institution, as well as the lack of uniform and generally accepted standards for stress testing, credit institutions should develop their own models of stress tests.

Currently, the level of capitalization of the banking sector is generally consistent with the standards of capital adequacy. However, faster asset growth, with inadequate capital growth, has led to increased potential risks for the banking sector. One of the new and promising tools of risk management in banking is a stress – testing.

There are a number of types of testing in stressful situations: sensitivity analysis (which qualifies the impact of changes under the influence of one factor), scenario analysis, which considers the impact of simultaneous changes in a variety of factors; maximum loss assessment and the theory of extreme values (or the worst-case theory), considering the characteristics of the «tail» of the distribution of functions. The most commonly used method is the scenario analysis.

Depending on the type of scenario on which the analysis is based, a distinction can be made between historical and hypothetical scenarios. One of the main questions of scenario analysis is to what extent these scenarios are suitable for the existing test conditions. First, historical examples are not necessarily accessible, and second, crises rarely repeat each other. It also raises serious problems when the lack of available time series, and in some cases the absence of observed historical crises, make the identification of the shocks particularly difficult [2].

Another drawback that is often mentioned is that these tests (except for the extreme value theory based on statistical models) do not determine the probability of potential losses.

Stress testing — a key point for identifying events and phenomena that can have a serious impact on banks-is an important aspect of assessing the Bank's equity.

Understanding and developing measures to counter the impact of potential market risks is one of the key tasks of the Board of Directors and managers. Bank stress testing scenarios should cover a range of factors that can create extraordinary losses or profits as a result of ongoing operations with the Bank's portfolio, or if controlling risk levels in these portfolios by conventional methods is very difficult.

The stress test scenario contains synchronous changes in a number of risk factors (for example, common stock prices, exchange rates, interest rates) that reflect an event that may occur in the foreseeable future. A stress test scenario can be based on a significant market event that occurred in the past (historical scenario), or on a probable market event that has not yet occurred (hypothetical scenario).

A key step in the stress testing process is to identify the main risk factors that should be subjected to stress testing. Banks should take into account the nature of their transactions, as well as the correlation between the risk factors to which their portfolios are exposed, in drawing up a list of risk factors.

The risks of financial assets and portfolios are assessed by the variability of their market stability. One of the most frequently applied risk criteria is the deviation to changes in market value or VAR (representing the maximum loss that will be incurred by the portfolio with a specified confidence within a specified period of ownership). The market value of the Bank's portfolio may change for several reasons [3].

The sensitivity stress test separates the impact on the value of a portfolio of one or more predefined changes in a particular market risk factor or a small number of closely related market risk factors. Sometimes it contains symmetrical disturbances (up and down), unlike the stress test scenario, which usually affects a given market risk factor, only in one direction (up or down). The most common stress sensitivity test is a parallel shift in the yield curve.

The concept of stress testing is based on the notion that the value of the Bank's portfolio depends on several market risk factors.

We can assume the risk factors affecting the portfolio as r1,r2,...,rn and function, determining the value of the portfolio (when all risk factors are known) as Р. Assessment of risk factors r1,r2,...,rn characterizes the market situation so, as far as possible in relation to the Bank's portfolio. Risk factors describing the market situation can be combined into one vector r = ( r1, r2,., rn). The market situation r the value of the portfolio will be P (r). Then the value (rMM) set for the vector representing the current value of risk factors, i.e. the current market situation (ММ). Therefore, the current value of the portfolio can be defined as P(rMM ).

Scenario analysis means, first of all, determining the value of these portfolios, provided that the risk factors, instead of their actual values rMM = (rMM1 , rMM 2 ,., rMMn ) , have a cost r=(r1,r2,.,rn), reflected in the scenario. If the portfolio is fully revalued, the valuation function is applied to the new value r risk factor.The value of the portfolio in the scenario will then be P (r). Linear dependence binds sensitivity δ k the value of the portfolio relative to individual risk factors [4].

Sensitivity-an indicator indicating for each certain risk factor the degree of change in the value of the entire portfolio, depending on the modernization of this risk factor. The higher the sensitivity, the more influence this factor has on the value of the portfolio. The sensitivity is determined as follows: «typical» changes are selected Δ1, Δ2,...,∆n, for all risk factors. Then the sensitivity is calculated for each risk factor: δ = p(Г ■■■Г -∙-rn)-p(r1---rι δ -∙-rn)

i Δ. ' º

i

Sensitivity δ k reflects th e m ean value of the function oscillations P on a distance Δ . . Such indicators

of sensitivity in the range Δ . selected if the function P nonlinear in the i-th risk factor. Depending on the sensitivity of each risk factor, the approximate value of the portfolio will be calculated according to the following formula:

r1,r2,.,rn)=

rMM 1 , rMM 2 , . ,rMMn

-rMM.

.=1

.

(2)

where P1~ linear approximation of the estimated function relative to the number rMM (1).

The choice of factors depends on the structure of the Bank's portfolio. Not all of the Bank's portfolio are influenced by the same factors. The number of risk factors should include all likely parameters that will be affected by the impact on the value of the portfolio. You can initially use a large number of factors that allow a user to later rebuild their portfolio without additional consideration for a large number of subsidiary risk factors. The procedure for selecting risk factors in foreign banking practice is not clearly defined.

The value of the portfolio can be represented as a function of several risk factors, where special attention is paid to the interest rate. For example, discount factors or interest rates can be a risk factor. Function P depends on the portfolio: a differentiated portfolio has a different evaluation function. This function P is not fully expressed as risk factors. In particular, the value of non-traditional, exotic portfolio items is usually determined in the evaluation process using the evaluation function. One of these methods can be evaluation of the portfolio or its separate positions by using a simulation method Monte-Carlo.

Using Monte Carlo simulation, so-called correlated testing can be performed in stressful situations. Random observations for risk factors are formed, taking into account the correlation existing between them, and then their simultaneous impact on the market value of Bank portfolios is calculated. By analyzing the remaining «tail» of the obtained probability density functions, it is possible to determine values similar to those obtained by using VaR models. Quantitative assessment of the impact of changes in interest rates is carried out using indicators of duration.

Another important difference between correlated and uncorrelated tests in stressful situations is that, while uncorrelated tests in stressful situations determine the amount of loss (change in value) caused by individual shocks, correlated tests give an assessment of exposure to risks (in the form of a VaR assessment). Stress testing answers the main question: what happens if the R market situation suddenly arises? the scenario in this case is the sudden appearance of the R situation on the market. Therefore, scenarios can be identified with market situations and presented as vector r .

The following approach, in our opinion, seems to be the most acceptable, namely: finding the key risk factors explaining the losses associated with the worst-case scenario. For example, an explanatory ability of 80 % means that we are looking for a set of risk factors that will be able to explain at least 80 % of the losses in the worst-case scenario.

This suggests that instead of the entire scenario rwc = (rwc1 , rwc2 ,.,rwcn ) , only the value of the set of risk factors w(r.1,r.2,.,r.w) taken into consideration, this accordingly simplifies the scenario:

R= ( r, mm1

,r,.,r,.,r,.,r) , wc.1 wc.2 wc.w mmn

(3)

where risk factors r.1,r.2,. ,r.w have the worst value rwc.1 ,. ,rwc.w and other risk factors have their real meaning.

A set of risk factors will explain 80 % of the losses incurred as a result of the worst case scenario if:

P(rmm)-P(R)I0,8(P(rmm)-P(rwc)).

(4)

In order to determine the minimum set of risk factors, it is necessary to carry out an analysis using the primary approach: first, we try to find the only risk factor that explains 80 % of the losses. If it is found-the task can be considered solved. If not, you will have to look for two risk factors that will reveal 80 % of losses. In the case where two risk factors, such a loss cannot be explained, we consider three factors [5].

Thus, a set of risk factors is drawn up, which in General gives an answer to the question: as a result of what risk factors the Bank receives 80 % of losses? In the selection of risk factors W, which explain 80 % of losses, it is difficult to go through all the options with W elements. For example, if we are looking for a minimum set of risk factors with a given ability to explain 80 % of losses in the scenario with the worst outcome, which consists of 500 of risk factors, the estimated function is determined by 2,6х1035 times. A more efficient method is to use the minimization algorithm to find a set of values {I1,...iw} for which P (rmm1,...rwci1,).. rwci2, ... rwciw,..., rmmn) has the minimum value [6].

Bank risks in the process of stress testing can repay the impact on each other, and may increase. Therefore, in order to obtain a more accurate picture of the impact of potential risks on the Bank's operations, it is necessary to consider the impact of several risks (market and credit). When considering the situation taking into account the influence of several risk factors, stress testing scenarios are used, while the analysis of individual risk factors is more clearly reflected in the use of stress sensitivity tests [7].

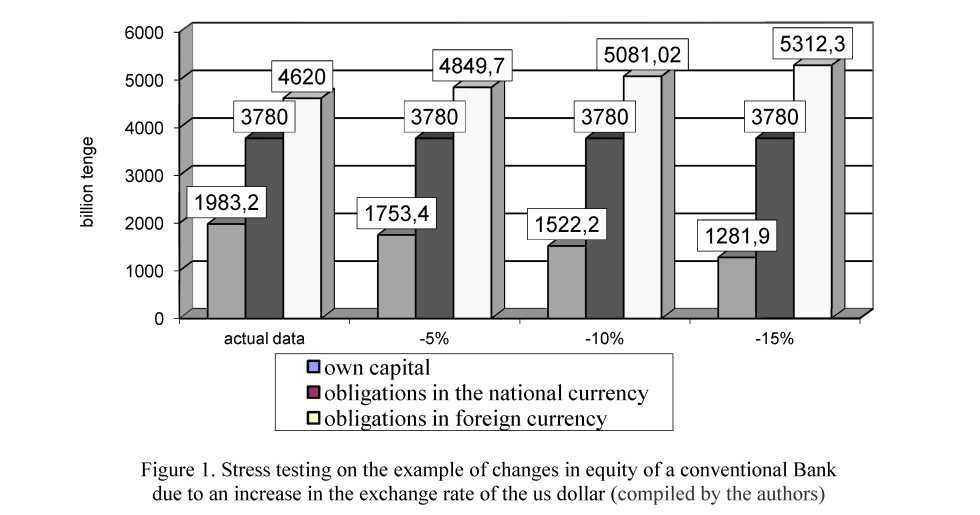

On the example of a conventional Bank, stress testing for stability is carried out through the implementation of sensitivity analysis, which calculates the impact of adverse factors that affect commercial banks as much as possible. We will consider 2 factors: the change in the exchange rate of foreign currency (us dollar) and deterioration in the quality of the loan portfolio on the example of a conditional Bank.

The scenario changes in the exchange rates of currencies. Let us assume that in the structure of claims and liabilities in foreign currency of the contingent Bank the largest share is occupied by claims and liabilities in us dollars. As of 1 January 2017, this figure was 55 %. In this regard, stress testing will be carried out on the basis of an open currency position on the us dollar.

Consider scenarios of increasing the tenge-us dollar exchange rate by 5 %, 10 % and 15 %. So, if on January 1, 2017 the rate of tenge to the us dollar amounted to 333.0, then the scenarios imply an increase to 335.8; 338.8; 3407.8. At the same time, due to changes in credit risk, provisions increased by 20 % of the difference between the actual and the resulting calculation of the amount of assets, which is reflected in Figures 1 and 2.

Hus, the results of stress testing it can be noted that the increase in the exchange rate of the US dollar by 5-15 %, the adequacy ratio of own capital to run the conventional Bank and the ratio of foreign currency net position to equity conditional Bank will remain at an acceptable level of 1.9 %.

Taking into account such a factor as the increase in the exchange rate of the us dollar, it ultimately leads to a decrease in the ratio of the Bank's equity capital, deterioration in the overall financial condition.

Currently, in the banking practice of developed countries, testing in stressful situations becomes an integral part of Bank risk management. The introduction of stress testing will allow early detection of the emergence of risks in the activities of banks and, accordingly, to develop measures to prevent or minimize losses that may occur in adverse situations. The main condition of effectiveness is that stress testing should be conducted regularly.

The frequency of stress testing should correspond to the dynamics of portfolio changes. Portfolios that are frequently changed and revised should be subjected to stress testing more often. The usual mode of stress testing in the practice of European countries implies quarterly research [8, 9].

Thus, stress testing in modern conditions can be one of the promising tools for regulating banking risks and preventing the emergence of problematic situations in the activities of second-tier banks, to regulate the risk operations of banks.

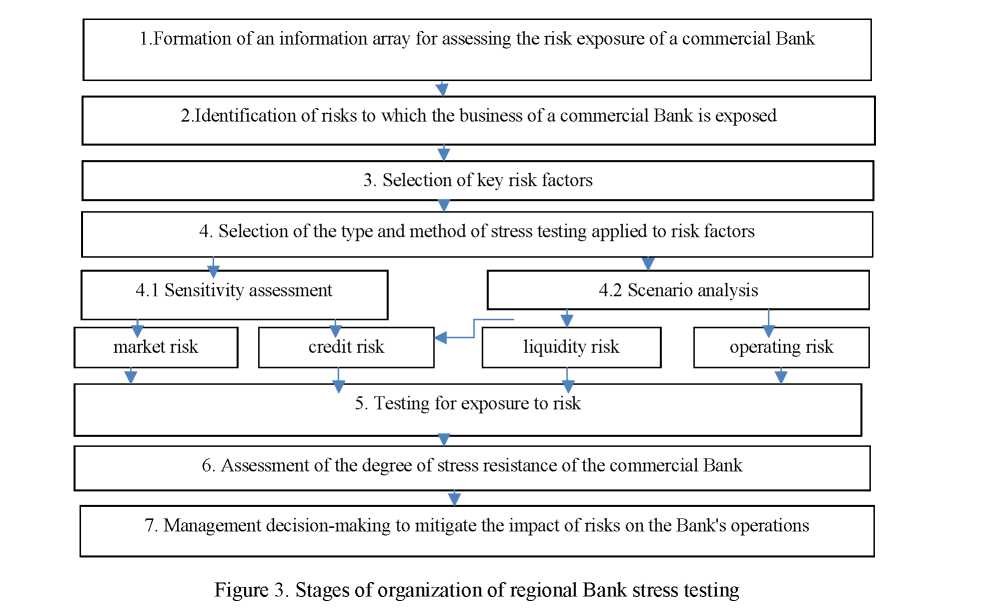

The main stages in the organization of stress testing include the following steps, presented in Figure 3.

The first step is to check the reliability, relevance and quality of information on the basis of which stress testing is carried out, including an assessment of consistency, continuity (continuous series of reporting data) and comparability (immutability of the methodology for calculating indicators) data. As part of the second stage, a detailed analysis of the loan and trading portfolios is carried out, identifying the risks to which the credit institution is most exposed. At the third stage, the analysis of the current dynamics of the key risk factors is carried out by determining the change in their values within a given time interval. The calculation can be carried out as the difference between the maximum and minimum value of the factor within a given time interval, and the difference between the values at the beginning and end of the study period. In the future, depending on the objectives of the analysis, either the average or the maximum value of the risk factor change is used in the calculations.

At the fourth stage, the choice of the type and method of stress testing is made. In our opinion, it is advisable to use sensitivity assessment when assessing portfolio risks, because of the high degree of variability of the initial information array. And when assessing liquidity risk and operational risks, a scenario analysis is a highly effective method that allows for taking into account sharp fluctuations in risk factors.

The fifth stage is the testing for exposure to risk. In the process of stress testing it is necessary to carry out a combination of criteria of extreme and probability of events. In contrast to the methods of VaR, stress tests do not answer the question about the likelihood of changes in risk factors. For this reason, when choosing scenarios, it is important to understand the probability of occurrence of certain events. It is not advisable to conduct stress tests based on incredible conditions.

Stress resistance is assessed at the sixth stage. Stress resistance of the Bank – is the ability of the Bank to withstand internal and external risks, which is influenced by indicators: availability of the resource base and its quality; quality of funding; profitability; liquidity; asset quality; capital adequacy; scale of activity; level of customer satisfaction, etc.for each of the risk factors is charged a certain point, forming the stress resistance of the Bank. On the basis of calculations the estimation of possible losses of credit institution as a result of realization of stressful conditions is formed.

In case of serious potential threats to the credit institution, the management of the credit institution makes appropriate management decisions, adjusts the risk management policy, and carries out additional risk mitigation measures. Regular updating (updating) of the stress test parameters is carried out as the market and General economic conditions, as well as the risk profile of the credit institution change [10].

Of course, the level of stress resistance to different risk groups is not a comprehensive assessment criterion and does not reflect all the differences between credit institutions. Nevertheless, in our opinion, it makes it possible to identify groups of credit institutions that can be considered sufficiently homogeneous in terms of ability to function steadily despite the high level of variability of the external and internal environment in the conduct of financial and economic research and monitoring of the functioning of the banking sector, as well as in the analysis of the consequences of actions and measures taken by the credit institution to achieve financial stability.

Thus, to date, stress testing has become a recognized and essential element of the risk management system, despite its, at first glance, a minor role. This situation is due to the probabilistic nature of the indicators used in risk assessment and analysis. The use of stress testing despite the relative subjectivity of the scenarios makes it possible to estimate the stress resistance of the credit institution with minimal costs, to determine the worst-case scenarios, to identify the most significant factors for the Bank, to develop a number of preventive measures.

References

- Bazovye printsipy effektivnoho nadzora za deiatelnostiu bankov: Konsultativnoe pismo Bazelskoho komiteta po bankovskomu rehulirovaniiu [Basic principles for effective Bank supervision: Advisory letter from the Basel Committee on banking regulation]. (1997, 2004, 2008, 2012). Basel.

- Pozdyshev, V. (2013). Basell significantly tightens the requirements. Banking review, 4, 28–30.

- Usoskin, V.M. (2010). Bazelskie standarty adekvatnosti bankovskoho kapitala: evoliutsiia podkhodov [Basel standards of Bank capital adequacy: evolution of approaches]. Denhi i kredit-Money and credit, 3, 39-51 [in Russian].

- Malykhin, D.V. (2012). Orhanizatsiia raboty vnutrennikh kontrollerov i auditorov po vypolneniiu novykh trebovanii k dostatochnosti kapitala «Bazel-3» [Organization of work of internal controllers and auditors to meet the new capital adequacy requirements «Basel-3»]. Banki Kazakhstana - Bank of Kazakhstan, No. 4, 41-44 [in Russian].

- Timofeeva, Z.A. (2002). Sistemy nadzora za deiatelnostiu kommercheskikh bankov [Systems of supervision of activity of commercial banks]. Denhi i kredit-Money and credit, 4, 53-58 [in Russian].

- Lisak, B.I. (2012). Bankovskie riski v Kazakhstane: v pohone za mirovymi standartami [Banking risks in Kazakhstan: in pursuit of international standards]. Banki Kazakhstana Hanks of Kazakhstan, 8, 13-20 [in Russian].

- Pashkovskaya, I.V. (2004). Stress-testirovanie kak metod obespecheniia ustoichivosti bankovskoi deiatelnosti [Stress testing as a method of ensuring the stability of banking activities]. Bankovskie usluhi - Banking service, 4, 4–26 [in Russian].

- Lisak, B.I., & Kim, A.B. (2012). [Otsenka veroiatnykh bankovskikh riskov metodom stress-testirovaniia [Assessment of probable Bank risks by stress testing method]. Banki Kazakhstana - Banks of Kazakhstan, 10, 48–55 [in Russian].

- Rachmetova, A., Kurmanalina, А., Gusmanova, J., & Erzhanova, S. (2017). Napravleniia stimulirovaniia bankov v Tmansirovanii innovatsionnoho sektora [Directions encouraging banks in financing innovation sector]. Vestnik Karahandinskoho universiteta. Seriia Ekonomika - Bulletin of Karaganda University. Economy Series, 4(88), 231-238 [in Russian].

- Iskakova, Z.D., Zenchenko, S.V., & Kurmanalina, A.K. (2016). Sovershenstvovanie protsedur stress-testirovaniia bankovskikh riskov v rehionalnykh bankakh [Improvement of procedures for stress testing of Bank risks in regional banks]. Proceedings from Development of the financial and credit system of the Republic of Kazakhstan in the conditions of the new global reality: Mezhdunarodnaia naucho-prakticheskaia konferentsiia, posviashchennaia 20-letiiu ENU imeni L.N. Humileva (15 aprelia 2016 hoda) - International scientific and practical conference, dedicated to the 20th anniversary of L.N. Gumiliyov ENU. (pp. 150-154). Astana [in Russian].