The article examines the topicality, problems, theoretical and methodological approaches to improve the credit system in the production of competitive agricultural products and food in the EAEUcountries. The purpose of the study is to analyze the mechanism of lending and its impact on the development of agricultural production, as one of the priority areas in the context of integration of national economies. The agrarian policy of the EAEU states in the sphere of crediting is not yet sufficiently unified and differs in variety. In order to determine the role and place of agriculture in the economy of the EAEU member countries, a comparative analysis of the volume of state financial support is presented, the indicators of the gross added value of agriculture in GDP, labor productivity, and the share of credits in the economy of the country are analyzed. The article considers the mechanism of state management of agricultural production to provide financial resources in Kazakhstan, Russia, Belarus: lending, leasing services. Eurasian integration will reduce the costs of transportation, storage, sale of agricultural products and food, create new market institutions. The introduction of a unified mechanism of state management in the EAEUcountries, in theauthors opinion, will make it possible to equip agricultural producers in equal economic conditions, increase production efficiency and competitiveness in the world markets for agricultural raw materials and foodstuffs, as well as solve the problem of providing the population with food and other issues of economic development in the EAEU countries.

Introduction

Directions of economic development of the Eurasian Economic Union (hereinafter referred to as the EAEU)are the following: creation of conditions for business activity growth and investment attractiveness (removal of barriers, harmonization and unification); innovative development and modernization; ensuring the availability of financial resources and developing the financial sector; infrastructure development, including the implementation of transit potential; development of human resources; energy efficiency and resource saving; regional development; cross-border and international cooperation.

One of the priority areas of integration of our countries is the agro-industrial sector. Lending is one of the main elements of the current economic mechanism in the agriculture of the EAEU countries. The only way to stimulate the flow of financial capital into the agrarian sector is to subsidize interest rates on loans and borrowings. Short-term loans are more in demand than investment (long-term) loans due to the fact that they do not need a solid collateral base and investment of their own funds, as for investment loans, and the interest rateis attractivetaking into account the subsidy from the budget.

Analysis of the main socio-economic indicators made it possible to conclude that Kazakhstan and Russia are countries with a relatively more developed economy. Thus, the GDP per capita in 2015 in the Republic of Kazakhstan is 25,876.5 US dollars, which is 6 % higher than in Russia and 1.5 times more than in the Republic of Belarus. Analysis of the statistical data shows that the volume of loans extended to all spheres of the economy in the EAEU countries in 2015 decreased by 45.4 % in comparison with 2014 and amounted to 734.5 billion dollars, including Belarus — by 28.5 %, (25.4 billion dollars), Russia — by 46.8 % (661 billion dollars), Kazakhstan — by 28.7 % (42.2 billion dollars). In the structure of allocated loans for 2015, the share of Russia amounted to 90 %, Kazakhstan — 5.7 %, Belarus — 3.4 %. The share of credits in GDP by countries was 46.3 %, including Belarus — 47.5 %, Russia — 49.6 %, Kazakhstan — 22.9 %. The share of credits in the agro-industrial complex in the total volume of these loans amounted to 10.6 % in Belarus, 4.1 % in Russia, and 6.1 % in Kazakhstan.

The GDP was $ 1 for Belarus, $ 2.1, Russia $ 2.0, Kazakhstan $ 4.4, agricultural products: $ 3.1 for Belarus, and $ 3.1 for Russia, Kazakhstan - 4.8 dollars. According to Table 1, the budget is surplusin Kazakhstan and Belarus; there are not enough funds to meet state needsin Russia.

Table 1

Analysis of individual indicators of economic development of the EEU member countries for 2015

|

Indicator |

unit of measurement |

Belarus |

Russia |

Kazakhstan |

|

GDP per capita |

US $ |

US $ 17660~ |

US $ 24451~ |

US $ 25876~ľ5~ |

|

Surplus (deficit) of the consolidated budget as % of GDP % |

% |

1.8 |

-3.5 |

9.6 |

|

Growth rates of agricultural products 2015g. by 2014 |

% |

103.2 (97.2) |

104.2 (104.4) |

102.5 (104.3) |

|

Gross Domestic Product |

billion US $ |

53.5 |

1332.1 |

184.3 |

|

Gross agricultural production, including |

billion US $ |

8.4 |

83 |

12.4 |

|

plant growing |

billion US $ |

3.8 |

39.6 |

6.7 |

|

livestock |

billion US $ |

4.5 |

43.5 |

5.7 |

|

Loans to the economy total |

billion US $ |

25.4 |

661 |

42.2 |

|

Agribusiness loans billion |

billion US $ |

2.7 |

27.1 |

2.6 |

|

Share of gross agricultural production in GDP |

0/ |

15.7 |

6.2 |

6.7 |

|

The share of agribusiness loans in the total volume of loans |

0/ |

10.6 |

4.1 |

6.1 |

|

Share of loans in GDP |

0/ % |

47.5 |

49.6 |

22.9 |

|

Specific weight of agribusiness loans in gross output |

% |

32.0 |

32.6 |

20.8 |

|

Produced GDP for loans |

US $ |

2.1 |

2.0 |

4.4 |

|

Produced gross agricultural output for loans |

US $ |

3.1 |

3.1 |

4.8 |

|

Employed in agriculture million people. |

mln people |

0.4 |

4.5 |

1.6 |

|

Average monthly wages of agricultural workers |

US $ |

304 |

321 |

319 |

|

Productivity (gross output) per employee thousand dollars |

Thousand US $ |

21.0 |

18.4 |

8.0 |

Note. Compiled by the authors according to sources [1, 2].

In 2015, the growth rates of agricultural products in Russia have a relatively stable dynamics. In the Republic of Belarus, agricultural production grew by 6.2 %, which is due to significant measures of state support to farms (agricultural loans, special tax regimes). In the Republic of Kazakhstan, the growth rate decreased by 1.7 % and is 102.5. The highest refinancing rate for 2015 in Belarus is 25 %, which exceeded in Russia by 2.2 times. Weighted average interest rates for individuals (in national currency) for short-term loans were: for Belarus — 26.3 %. Kazakhstan — 18.0 %, Russia — 24.2 %, long-term loans for Belarus — 19.3 %, Kazakhstan — 17.2 %, Russia — 17.5 %.

The average weighted interest rates for legal entities (in national currency) for short-term loans in Belarus amounted to 32.8 %, Kazakhstan — 17.2 %, Russia — 13.8 %, long-term loans for Belarus — 23.2 %, Kazakhstan — 12 %, Russia — 13 % [3].

The agrarian mechanism of the EEU member countries in the field of lending is very diverse. Thus, lending in the Russian Federation is one of the main elements of the current economic mechanism in agriculture and the only way to stimulate the flow of financial capital into the agricultural sector is to subsidize interest rates on loans and borrowings. One of the shortcomings of the current mechanism for supporting lending in Russia is the linking of subsidies for the reimbursement of part of the cost of paying interest are tied to the refinancing rate of the Central Bank of Russia; the refinancing rate is 3 times lower than the weighted average loan rate. Thus, even subsidies for compensation of 100 % of the refinancing rate cover only a part of the costs incurred by agricultural producers. This led to a significant increase in the debt of agricultural producers on loans, which is 42 % of the annual GDP of the agricultural sector. The bulk of credit resources(78.2 %) was provided by Sberbank of Russia and Rosselkhozbank OJSC. For agricultural producers engaged in the production of milk and beef, subsidies at the rate of 80 % of the refinancing rate and at least 20 % at the expense of the regional budgets, for the development of crop production under investment loans at OJSC Rosselkhozbank - 38.2 %, Sberbank of Russia - 28.4 % of the total amount of loan funds. In 2015 the weighted average interest rate on loans was 20.9 % in JSC Rosselkhozbank, and 19.5 % in Sberbank of Russia. The size of the compensation rate for short-term loans is 17 %.

In the Republic of Belarus, loans to the agro-industrial complex are made with the participation of the state; preferential terms for the issuance of various types of loans are being developed. Priority areas of lending are the implementation of investment projects: the formation of the main flock, the purchase of machinery, the construction of production facilities, the construction of housing in the countryside for workers of agricultural organizations; credit support for repair, service organizations, harvesting and processing agricultural products of enterprises. The volume of financial state support for preferential lending under state programs to support the agro-industrial complex is set at 10 % of the gross value of agricultural products produced. To stimulate the attraction of financial resources, programs are implemented where the main measures are subsidizing interest rates on bank loans in the amount of 100 % of the refinancing rate, compensating the losses of banks when granting concessional loans to entities operating in the agro-industrial complex [4, 5].

In Kazakhstan, the share of loans in the agribusiness sector is 3.9 % in the total volume of the economy: the system of concessional lending to agricultural production is based on the allocation of state credit resources at regulated fixed interest rates and is completely state-administered. The main state body in the financial provision of agricultural production is the JSC «National Management Holding «KazAgro» (hereinafter referred to as JSC NMH «KazAgro»).

Financing of the Holding's activities is carried out at the expense of the republican budget, bonded loans, credit resources of commercial banks and other financial institutions. It includes: JSC NC «Food Cor- poration», «KazAgroFinance» JSC, «Agrarian Credit Corporation» JSC, «Fund for Financial Support» JSC, «KazAgroGarant» JSC, «Malindery Corporation» JSC, «KazAgroMarketing» JSC.

NC JSC «Food Corporation» allocates credit resources for the purchase of grain and other agricultural products from commodity producers at guaranteed prices; KazAgroFinanceJSC finances them on a leasing basis, Agrarian Credit Corporation JSC lends to rural credit partnerships through which resources are allocated to agricultural producers; «Fund for Financial Support» JSC makes payments for microcrediting and insurance payments for compulsory insurance in agriculture; «KazAgroMarketing» JSC provides effective protection of interests of agricultural producers (holders of grain and cotton receipts), informs and monitors the development of the agro-industrial complex; «Malinimderi corporation» JSC exports livestock products.

JSC NMH KazAgro is the largest creditor of Kazakhstan's agrarian sector: 44 % of loans are allocated; including 60 % are long-term and have a specific investment focus. During the last 5 years, more than 900 billion tenge was allocated to agrarian production: 25 % of budget funds, the main source of financing are own funds and borrowed loans.

The main goal of state management of agricultural production is to ensure its sustainable development, taking into account the increase in labor productivity, profitability and product competitiveness. For stable management of agricultural production, funds are needed to replenish current assets, which are attracted, mainly, from borrowed funds of financial institutions. However, due to the peculiarities of agricultural production, financial institutions issue short-term loans to commodity producers with high interest rates. The average interest rate of interest on loans for the period of 20142015 amounted to 12-16 % per annum, and in other sectors of the economy — 10-13 %. As a result, agricultural producers pay high remuneration for loans for replenishment of fixed and circulating assets, which leads to an increase in the cost of production of a unit of production and reduces its competitiveness. In order to reduce the financial burden of subsidies, interest rates on leasing and loans should not exceed 5 %.

The existing level of technical equipment hinders the effective development of the agro-industrial complex. As a result, the high cost of agricultural machinery, spare parts, equipment, high interest rates do not allow renewing fixed assets to the overwhelming majority of commodity producers and, first of all, to peasant farms. Taking into account the average interest rate of 12-16 %, the agricultural commodity producer pays almost two costs within 7-9 years. To this end, JSC NMHKazAgroshould reduce stepwise direct lending to the subjects of the agro-industrial complex and, on the basis of its own and attracted funds, will carry out funding for second-tier banks. This will allow commodity producers to obtain loans at an acceptable rate for longer periods, as well as a full sector of banking services.

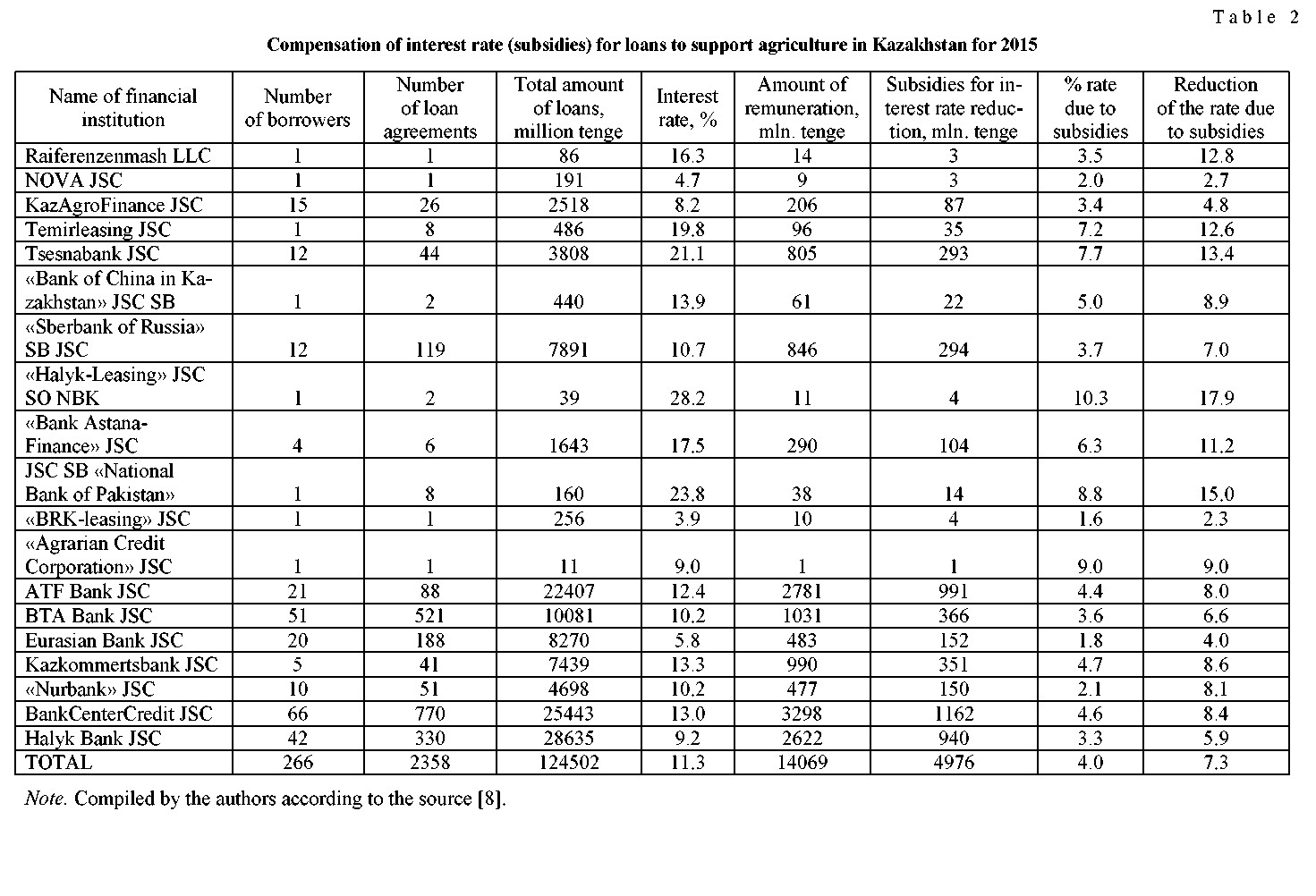

For the development of agricultural production, commodity producers are allocated subsidies for reimbursement of interest rates to credit institutions. So, in 2015 19 credit institutions, 266 borrowers were involvedin the allocation of short-term loans, 2358 loan agreements were concluded. Agricultural producers received 124.5 billion tenge of loans. In the structure of credit resources, the share of JSC «Narodny Bank» was 23 %, JSC Bank-CenterCredit — 20.4, JSC «ATF Bank» — 18, JSC «BTA Bank» - 8.1 %. The average interest rate for Kazakhstan is 11.3 %, including 9.23 for JSC Halyk Bank, 13.2 for Bank CenterCredit, 13.2 for JSC ATF Bank, and 10.2 % for JSC «Bank». Financial institutions received for the issuance of credit resources KZT14.1 bn compensated by subsidizing KZT5 bn. (Table 2).

Consequently, agricultural producers paid loans to credit institutions for loans received, taking into account the interest rate and its subsidy KZT133,595 m. The share of credit resources in 2015 in the total amount for Almaty city is 15.7 %, Kostanay region — 13.7, Pavlodar — 11.5 %. The volume of credit resources in the East Kazakhstan region is 16.1 %, South Kazakhstan — 14.2, Karaganda — 17.2, North- Kazakhstan — 11.5 billion tenge.Forecast calculations show that the average annual volume of loans provided by financial institutions through the system of insurance and loan guarantees for 20172021will be on av- erage232 billion tenge. The volume of subsidizing the interest rate is KZT15 bn, the average interest rate due to subsidies will be 6.5 % [6, 7].

A successful approach to the financing of agriculture and a stable financial position of the banking system should be carried out taking into account the following requirements when placing a loan: an assessment of the potential profitability of the operation, which allows to determine whether the expected income of the agricultural producer will cover interest on the loan, ensure its return and leave sufficient fundsfor the development of production. Calculations show that exceeding the collateral of the loan obligations should be at least 30-40 %.

In the EAEUcountries it is necessary to develop methodological approaches and special programs on agricultural credit, providing for a credit system with preferential loan terms. The credit mechanism should include concessional lending for the share of long-term loans, lower interest rates, lending directly from public sources through the mechanism of collateral transactions, the development of a mortgage loan in commercial banks, the establishment of lending institutions (agricultural credit bank, commercial banks, credit cooperatives, financial industrial groups and others).

The system of agricultural crediting should be improved in the following areas: the development of mechanisms for state regulation and supervision of credit activities, with the principle of the availability of credit to agricultural producers; use of public funds and the results of the agrarian lending and subsidy program; improvement of the normative and methodological framework, which contributes to the development of directions and objects of lending.For this purpose, it is recommended to create special state funds for preferential short-term and long-term loans, mortgage and leasing funds of commodity producers of agrarian products, which allow more efficient use of credit resources. It is also necessary to introduce a system of interest-free crediting by commercial structures for the development of production and processing of agricultural products for all technological costs.

To concentrate credit resources and, above all, resources (subsidies, loans, etc.) from budgetary funds, an agricultural bank should be established. Banking institutions should take part in the implementation of the program of financial support of the agro-industrial complex, servicing leasing companies, investing through direct lending, providing guarantees, and creating long-term resources through the issuance of bonds. For efficient use of financial resources in the EAEU countries, it is advisable to set standards for the formation of the banking system and the optimization of banks [8–10].

Financial recovery must be carried out on a contractual basis by agricultural producers, the creditor and the state. Creditors provide restructuring of financial obligations of agribusiness entities through reduced interest rates, prolongation of loan repayment terms, granting of a grace period for repayment of the principal debt, writing off penalties, interest, delayed remuneration, other measures, refinancing and financing of agribusiness entities to pay off arrears. Agricultural commodity producers ensure the non-distribution of profits before full performance of obligations to the creditor, fulfillment of planned indicators of financial recovery and other measures.

It is necessary to introduce subsidies from the budget of the main part of the interest rate on loans issued by banks to pay premiums for agricultural crop insurance, with repayment of these loans through insurance compensation.

There is a need to introduce short-term (for current costs) and long-term (for replenishment of fixed assets) loans. Acceptable payment for a short-term loan is a rate of 10-12 %, long-term: 3-5 % per annum. This will ensure the availability of credit resources to agricultural producers and increase their recoverability.

To create equal conditions for managing agricultural producers in the EAEU, it is necessary to unify loan rates for the use of resources. When buying or selling fixed assets and equipment, including agricultural machinery, it is necessary to abolish the value-added tax, land and real estate tax.

Leasing can become an important means of technical re-equipment in agriculture. The share of leasing in capital investments spent on the purchase of equipment in the total volume of deliveries to the US, Germany is 25-30 %, in Russia, Belarus and Kazakhstan 8-10 %.

For the successful use of leasing in agricultural production in Kazakhstan, along with other activities, it is necessary to improve the legal and organizational and methodological base including: revision of the procedure for using the leasing fund for the purchase of machinery and animals; to increase in the leasing period for equipment prior to physical wear and tear; to reduce the first payment to 8-10 %; to decrease in supply- and-marketing margins during leasing operations to a minimum size; to reduce customs duties and taxes on leasing operations for the leasing of property, including VAT; to release the lessor from payment of profit tax received under contracts for a period of at least 3 years; to provide for accelerated depreciationin leasing contracts, leased property not to be taxed. To enterprises and organizations that carry out leasing operations, the income tax rate for the first year (from the moment of registration) should be reduced by 90 %, over the next five years - by 50 %.

Based on international experience and the current economic situation in the country, further development of the domestic market for leasing services is expected to be carried out on the basis of stimulating investments in agroleasing with the involvement of domestic and foreign banks. At the same time, it is necessary that the state acts as a guarantor of rural commodity producers in leasing operations. This approach is one of the important instruments of market regulation and has significant opportunities in the new economic conditions [11, 12].

The reorientation of the use of budgetary funds from direct financing of agroleasing for the provision of state guarantees to lessors and their creditors will significantly reduce the risk of non-fulfillment of the terms of contracts, the share of interest rates of bank loans in the structure of lease payments, reduce the cost of transferred equipment, and increase the involvement of large financial resources in the agricultural sector of the economy. To achieve these goals, it is advisable to create a special fund for state guarantees on leasing transactions, which is replenished at the expense of part of the funds of budgets of different levels, currently directed to the technical re-equipment of agricultural enterprises.

The amount of guarantees provided to leasing companies can be established differentially, depending on the amount of the loan with the expectation that it covers at least 70-80 % of payments that have not been received from the lessees. To stimulate the attraction of loans, it is proposed to provide second-tier banks (on a competitive and licensing basis) tax benefits of up to 20 % of the amount of actual investment in financing leasing. A prerequisite for such benefits should be the establishment by banks of minimum interest rates for credit and the maintenance of preferential conditions for farms operating under state leasing. Banks receiving such privileges must provide loans to leasing companies at minimum interest rates, and the latter, in turn, provide leasing services under more loyal terms.

Thus, the analysis allows to draw a conclusion that when forming the economic mechanism in the EAEU in the sphere of crediting, one should take into account the experience of Belarus - in the sphere of financial state support for preferential lending within the framework of state programs to support the agroindustrial complex, Kazakhstan - on preferential lending to agricultural production based on the allocation state credit resources at regulated reduced fixed interest rates with a consistent transition to subsidizing these rates; Russia - in the sphere of stimulating the flow of financial capital into the agrarian sector through subsidizing interest rates on loans and borrowings.

References

- Statisticheskie dannye. Evraziiskaia ekonomicheskaia komissiia [Statistical tables. Eurasian Economic Commission. eurasiancommission.org. Retrieved from http://www.eurasiancommission.org.

- Sidorsky, S.S. (2014). Ahropromyshlennaia politika Evraziiskoho ekonomicheskoho soiuza [Agro-industrial policy of the Eurasian Economic Union]. Evraziiskaia ekonomicheskaia komissiia – The Eurasian Economic Commission, 23 [in Russian].

- Avtorskii kollektiv. Hosudarstvennaia podderzhka ahropromyshlennoho proizvodstva Kazakhstana v usloviiakh Evraziiskoho ekonomicheskoho soiuza. Ministerstvo obrazovaniia i nauki Respubliki Kazakhstan. Kazakhskii naucho-issledovatelskii institut ekonomiki selskoho khoziaistva i razvitiia selskikh raionov (2014) [The team of authors. State support of the agro-industrial production of Kazakhstan in the conditions of the Eurasian Economic Union. Ministry of Education and Science of the Republic of Kazakhstan. Kazakh Scientific Research Institute of Agricultural Economics and Rural Development]. Almaty [in Russian].

- Rossiia v tsifrakh [Russia in figures] (2015). Rosstat. Moscow [in Russian].

- Statisticheskii sbornik. Selskoe khoziaistvo Respubliki Belarus (2015) [Statistical compilation. Agriculture of the Republic of Belarus]. Minsk: Belstat [in Russian].

- Statisticheskii sbornik. Selskoe, lesnoe i rybnoe khoziaistvo v Respublike Kazakhstan (2015) [Statistical compilation. Agriculture, forestry and fisheries in the Republic of Kazakhstan]. Astana [in Russian].

- Sigarev, M.I. (2015). Subsidirovanie selskokhoziaistvennoho proizvodstva v Kazakhstane [Subsidizing agricultural production in Kazakhstan]. Almaty: Kazakhskii nauchno-issledovatelskii institut ekonomiki ahropromyshlennoho kompleksa i razvitiia selskikh territorii [in Russian].

- Ministerstvo selskoho khoziaistva Respubliki Kazakhstan [Ministry of Agriculture of the Republic of Kazakhstan]. mgov.kz. Retrieved from http://mgov.kz [in Russian].

- Tarr Davyd, G., &Tаrr Dаvid, G. (2012). Evraziiskii tamozhennyi soiuz Rossii, Belarusi i Kazakhstana: mozhet li on preuspet tam, hde eho predshestvennik poterpel neudachu? [The Eurаsiаn CustomsUnmn аmоng Russiа, Belаrusаnd Kаzаkhstаn: Cаn it su∞eed where its рredeсessоr fаiled?]. Tsentr ekonomicheskikh i Iinansovvkh issledovanii novoi ekonomicheskoi shkoly - Centre for ісоп()іпіс<іпі Finаnсiаl Resenrch аt New Eсоnоmiс Sсhооl, 37, 75 [in Russian].

- Maslova, V.V. (2015). Ekonomicheskie aspekty formirovaniia Evraziiskoho ekonomicheskoho soiuza v ahrarnoi sfere [Economic aspects of formation of the Eurasian Economic Union in the agrarian sphere]. Ekonomika selskoho khoziaistva Rossii – Economics of agriculture of Russia, 7, 89-95 [in Russian].

- Sigarev, M.I. (2011). Rol lizinha kak instrument modernizatsii i innovatsionnoho razvitiia ekonomiki [The role of leasing as an instrument of modernization and innovative development of the economy]. Ekspert RA Kazakhstan – Expert RA Kazakhstan, 1, 25-30 [in Russian].

- Alekseenkova, E.S., Glotova, I.S., Devyatkov, А.У., & etc. (2017). Perspektivy razvitiia proekta ЕЖ do 2025 hoda. — Rossiiskii Sovet po mezhduπarodπym delam (RSMD) [Prospects of development of the project of the ЕАЕÙ by 2025. - The Russian Council for International Affairs (INF)]. Moscow: NP INF [in Russian].