In the article a comparative description of banking regulation, as well as the regulatory characteristic of regulatory and supervisory functions of the state in the sphere of banking activity are given. Methods and tools of banking regulation and supervision are considered. The classification model, interrelation of methods and monetary regulation tools in the author's edition are given. The role and importance of innovations in the development of the country's economy is studied. The features of the the state innovation policy in modern conditions, the main factors influencing it were studied. The characteristic of the main factors and types of innovation policy are given. Experience of innovative activity regulation on the example of the European Union, Japan and the USA is considered. The main characteristics of innovation policy on the example of developed countries with the identification of the main specific features and characteristics are studied. The comparative characteristic of the state bodies of supervision in the sphere of banking innovations, their distinctive features are given. The types of innovation policy and the role of the state in stimulating and regulating innovation are considered. The role of the state and state institutions in regulation and stimulation of innovations is revealed. Based on the analysis of the current state of banking supervision in the world economic space, certain conclusions were made and specific recommendations were proposed.

The current state of the banking sector and the ongoing changes in the economy make it clear what an important and direct impact the steadily developing financial and banking sector of Kazakhstan has on the economy as a whole. Being the «main arterial vessel», an indicator of the overall development of the country's economy, the financial and banking sector deserved and continues to deserve the most careful and careful study and analysis. Constant and continuous monitoring, analysis and forecasting of the development of financial and monetary relations in the country guarantees positive and dynamic development of the banking system. One of the most important tasks set on the way to achieving prosperity and wealth of both the banking sector and the economy as a whole, and, consequently, raising the living standards of the country's population, is the implementation of competent, consistent, and most importantly, constructive and long-term regulation of the banking system.

The importance of the banking sector is due to the role it plays in the formation and development of new elements of the market economy, taking into account completely different features of the state policy in the field of money, credit, finance, reflecting the dissimilarity and difference of our Republic from other States.

Considering the process of regulation and supervision from a microeconomic standpoint, i.e. from the point of view of individual effects on individual areas of financial activity from the body it can be defined as external (Central regulation) [1; 18].

External regulation is a system of special economic relations between the Central Bank of the country and the second — tier banks, as the banking system is a set of subjects of financial and credit relations. And «banks are the main link of control and regulation of the economy. Any uncoordinated actions can cause a chain reaction of bankruptcy and reduction of production efficiency across the country» [2; 168].

The main priority element of regulation is the system of supervision and control, without which it is impossible to use methods and tools of monetary policy. Regulation and supervision of banking activities is carried out through the mechanism of its implementation.

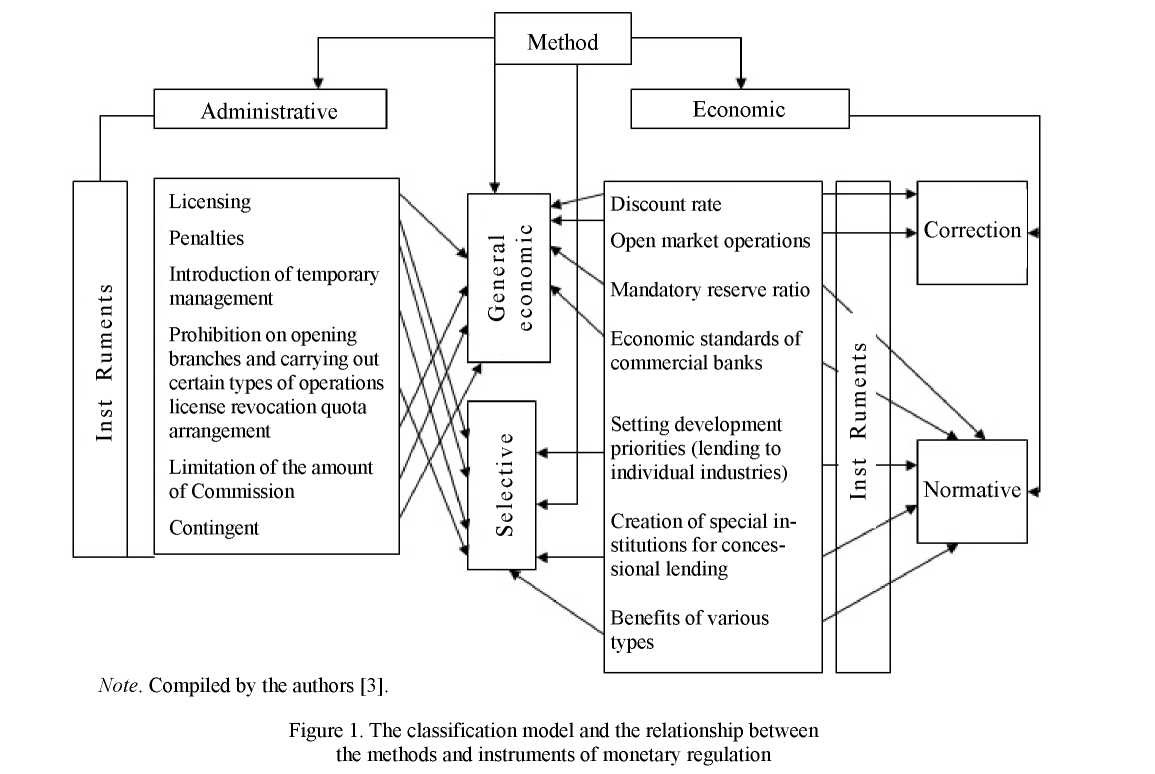

To streamline the use in theory and practice of banking, methods and instruments of regulation and supervision of banking activities, it is necessary to classify them, reflecting the relationship in accordance with different criteria by forms, nature of interaction and methods of use.

In all developed countries, banking is subject to enhanced control and supervision, more stringent than in relation to other aspects of the economic life of the state. The Bank's activities are more general than those of other entities involved in «money trading». Banks are responsible for the protection of customers: organizations, industrial and commercial enterprises and individuals and monitor the solvency of their borrowers. Borrowers who do not repay loans on time, may be at the initiative of the Bank to be deprived of the opportunity to manage their business.

Figure 1 presents a model of classification and interrelation of methods and instruments of banking regulation and supervision.

In recent years, one of the new directions of economic development has become innovation as an advanced engine of its development. All modern trends in the economy are accompanied by the rapid development of innovations and digital technologies. Industry and production is an inexhaustible source of innovation. However, the sphere of services and money circulation has also become an arena for the development of innovations in the field of information technology, the development of electronic money, the development of blockchain technology, etc.

In modern conditions in most developed countries, the innovative policy of the state should be systematic and due to the following factors:

- competition for human capital comes to the fore, which has become a new trend in global innovation development;

- development of mobility of highly qualified personnel, which contributes to the wide dissemination of knowledge and skills;

- the role of information technologies in the process of dissemination of knowledge and growth of innovative activity is increasing, as technologies and information have gone beyond the borders of individual countries long and are global in nature;

- due to globalization, many countries and enterprises are forced to compete at a high level, which entails at the same time specialization in certain innovations.

Consider the European model of state innovation policy. In such leading European countries as Germany, great Britain and France, the main role in the formation of scientific and technical potential of the economy, the development of innovation in the national economy is played by public authorities.

The main innovation policy document is the «plan for the development of international infrastructure for innovation and technology transfer», which was published in 1985. Its main engine was the acceleration and simplification of the processes of implementation of scientific projects in the finished production, the spread of innovation in the EU. Further, the following programs were adopted: «Velyu», ESRPIT (European strategic research program in the field of information systems technology); RACE (research of advanced methods of communication in Europe); EUREKA (program aimed at creating alliances between European groups of major industrial companies in the fields of optics, new materials, computers, lasers, particle acceleration, artificial intelligence) [3].

The main directions of the EU innovation policy include:

- – Stimulating knowledge-intensive small and medium-sized businesses;

- – Direct financing of innovations in the field of new technologies;

- – A single anti-monopoly legislation on the regulation of innovation;

- – Financial support of interaction between theoretical science (universities) and scientific organizations, institutes;

- – Extensive use of accelerated depreciation of equipment;

- – Preferential taxation of high-tech enterprises.

The main operators of the state policy in the field of innovation are the Central banks.

It should be noted that the main centers of scientific and technological thought were countries such as the United States, Japan and the European Union. Over the past 20–30 years, the US remains the undisputed leader in the market of high-tech products. Thus, the beginning of 2010 in the United States was concentrated up to 30 % of the world production of high-tech goods [4; 156–168].

At the present stage, the main role in the development of innovations still falls on the state bodies, which have a great opportunity to finance significant sectors of the economy, especially science-intensive and high-tech sectors.

It is possible to distinguish countries by types of innovation policy into 3 groups. The first group includes countries that focus on large-scale projects, including the full cycle from development to implementation. In such countries, a significant share of innovation falls on the military-industrial complex, the defense sector. These include the United States, England and France. The second group includes countries focused on the dissemination of innovation and the creation of an enabling environment for them, in General, to improve the economy, for example, Germany, Sweden and Switzerland. The third group includes countries in which innovation policy is aimed at stimulating innovation, coordinated work in all branches of science and technology. This is Japan and South Korea [5; 58–61].

Two directions of development of innovations are defined. The first is the organizational aspect, namely:

- creation of centers of scientific thought;

- launch of technological initiatives (platforms);

- the stimulation of fundamental science through the development of a competitive environment between research groups;

- creating conditions to prevent the outflow of personnel and attracting qualified foreign research;

- development of research infrastructure;

- coordination of national research programmes.

The second area is institutional change:

- integration of science and industry, development of innovations in the regional aspect;

- strengthening the role of government support for innovation;

- development of new forms of cooperation between universities, private business and the state;

- state support in commercialization of R & d results and expansion of demand for the results of activities of state research institutes;

- creation of a new scheme «science + education + innovative business». For this purpose, special funds and enterprises in the format of public-private partnership are created;

- strengthening the role of government regulation in innovation, especially in the field of intellectual property protection.

Thus, the innovation policy of the EU countries has become systematic and long-term with specific priorities [6].

The activities of the Bank of Japan are strictly regulated by state policy and controlled by the Ministry of Finance, which has the right to order certain activities. Monetary policy in Japan is implemented both through the Bank of Japan and through government financial institutions. In the 70-ies Japanese economists have repeatedly expressed their wishes to present the Bank of Japan wider independence. In the early 80-ies restrictions were adopted on direct financing of the economy by the state through government financial institutions and restrictions on the expansion of monetary flows directly controlled by the government [7].

In Japan, the main coordinator for innovation is the Ministry of foreign trade and industry, and the Department of science and technology is responsible for monitoring the implementation of specific areas of scientific and technical projects. In addition, the country has a Japanese Association of industrial technologies, which is engaged in the issuance and acceptance of licenses. As in the EU, the focus in the development of innovation is on large corporations [8].

Now public spending on R & d in Japan has increased to 3.5 % of GDP and is aimed at fundamental research and the search for fundamentally new ideas. If earlier Japan mainly bought licenses for innovative projects, now the policy is aimed at their export.

Japan's innovation policy in addition to the General methods of stimulating the development of innovation, indirect methods are used, namely:

- targeted financing at the expense of private investors-banks and their concentration in priority sectors of the economy;

- assistance in the purchase of advanced foreign technologies;

- control over scientific and technical exchange with foreign countries.

The main difference between the Japanese model of innovation policy is the construction of cities- technopolises as centers of R & d and science-intensive production. State regulation of innovations in Japan is characterized by planning, high import customs tariffs, tax and credit benefits, active state support for innovations [9].

Currently, Japan is at the stage of transition to a completely new model of innovative development, which is designed to provide scientific and technical leadership through the commercial implementation of national companies of scientific achievements and developments not previously used by competitors. Thus, in accordance with the new innovation strategy developed in 2009 — New Growth Strategy, the main objectives are: ensuring the leading position of the country in the creation of environmental technologies, bringing the annual volume of investment in R & d to 4 % of GDP, increasing the number of world-class research centers, ensuring full employment of young scientists, widespread introduction of innovations in the social sphere [10].

It should be noted that the USA remains the undisputed leader in the innovation market. In the US, it is officially recognized that investment in knowledge — intensive production is investment in the future of the country. One of the main strategic goals is the development of experimental development. The main feature of the American model of innovation policy is the close interaction of the state and private business. In America, there are many joint ventures financed by public and private funds.

In the US, each state has its own control body, but the general functions of control and regulation of banking activities are carried out by the federal reserve system. The act on the federal reserve system (1931) formulates one of the tasks of the fed as «creating more effective control over the banking business». Sharing this responsibility with other federal banking institutions, the fed combines monetary policy with a regulatory function. It is primarily responsible for the financial stability of the economy. Taking decisions within the framework of its control and regulation functions, the fed takes into account the resonance in other sectors of the economy caused by actions affecting monetary institutions.

The main tasks of the federal reserve in the field of control and regulation of deposit institutions in the United States include: control and regulation of the activities of state-registered banks — members of the federal reserve system, all corporations operating under the law of the edge, as well as all banking holding companies; control and regulation of activities in the United States of foreign banking organizations under the international banking Act 1978; regulation of the structure of the US commercial banking through the implementation of the Law on Bank holding companies of 1956 and later amendments, and through the implementation along with other federal departments, law on merger of banks, 1960, and the act for amendment of banking supervision, 1978; regulation of foreign activities of all American commercial bankingorganizations — members of the fed or organizations conducting their foreign economic activities through a corporation established on the basis of the edge law [11].

Three federal bodies are involved in the control: the federal reserve, the office of the comptroller of monetary circulation (CDO) and the federal deposit insurance corporation. These federal agencies work together with the supervisors of banking in fifty States. There is some duplication of responsibilities in this structure. For example, the comptroller of the currency shall register the national banks. It is given the primary responsibility. The federal reserve system has overall responsibility for monitoring and regulating the activities of all banks — members of the federal reserve system, which includes national banks, from which the legislation requires them to be members of the fed, the federal deposit insurance corporation has power over banks-members of the fed and over insured banks that are not members of the fed, the law requires mandatory federal deposit insurance. In practice, three Federal agencies and several state agencies reach agreements that reduce the impact of duplication. The Federal deposit insurance corporation acts as the main supervisory authority for insured commercial banks that are not members of the fed, as well as for insured savings banks registered at the state level. The BWC apparatus deals with national banks, and the federal reserve carries out supervisory functions in relation to the banks-members of the fed, registered at the state level, as well as in relation to all Bank holding companies.

The federal Council on the audits of financial institutions, which represent the inter-ministerial body, was established under the laws of 1978. Its mission is to develop uniform principles, standards and report forms for the federal audit in Bank deposit and savings and credit institutions. The Federal Council also promotes coordination in other areas of oversight, including coordination between state and federal supervisors. The federal reserve is responsible for control over domestic and international operations of all member banks of the federal reserve, corporations created on the basis of the law of edge, and US Bank holding companies, as well as activities on the territory of the United States of foreign banking organizations.

The federal reserve carries out special audits of member banks in certain areas of their activities, such as work with consumers, the activities of trust departments, the activities of agents for the transfer of shares and trade in municipal securities, the operation of electronic data processing systems.

At the federal level, the 1978 act distributes control over the activities of branches or agencies of foreign banks in the United States. Federal reserve system — the wide inspectorial powers of oversight over all branches and agencies of foreign banks operating in the United States, and which is licensed at the federal level and at the state level. The fed should analyze the impact and condition of foreign banks, activities of which are to go beyond one state. The fed is authorized to conduct field audits to determine the assets and liabilities of all branches and agencies. It is usually satisfied with the results of inspections and audits conducted by state and other federal banking authorities.

An important responsibility of the federal reserve system is the implementation of the proposed mergers of banks, result of which is in the formation of fed member banks, registered at the state level. According to the law, all proposed mergers and acquisitions of insured banks have received initial permission from the federal agency regulating banking activities under whose jurisdiction the absorbing Bank or the newly formed Bank will fall. In order for all three agencies to be guided by uniform criteria in the analysis of Bank mergers and acquisitions, the law requires the Agency involved to request reports from the other two agencies on possible competitive factors. A request is also made to the Ministry of justice. In accordance with the provisions of the law on banking holding companies, the merger of the two companies falls under the jurisdiction of the federal reserve system.

In the US a program of banking supervision reform has recently been carried out. A project was proposed to replace the federal banking commission with an independent organization with greater authority. However, it was rejected due to the fact that, according to most opinions, it (the federal banking commission) could lose its connection with the financial sector, become unable to respond quickly and efficiently to emerging crises in the banking sector [12].

As for the regulation of innovation, it can be noted that in the United States in the 70s a special program was created in the field of development of new technologies. To that end, a national centre for scientific and technical information and a consortium of federal laboratories had been established, comprising almost 300 state scientific departments. Under this program, a huge fund of scientific works and projects of more than 200 federal organizations was collected, most of which are almost 80 % of the ministries of defense, energy and NASA. In addition, the national center cooperates with industrial firms and organizations [13].

Economic policy of the United States for many years is based on the mechanism of commercialization of scientific and technical products, through the purchase of budgetary funds or private investment of new developments from scientific laboratories in industrial production.

The following organizations are government regulators of innovation in the United States: the American science foundation, which is responsible for basic research; the American science council — industry and universities; NASA; the national Bureau of standards; the Department of defense; the national center for industrial research; the national Academy of Sciences; the national technical Academy; and the American Association for the advancement of science. The last 4 organizations have mixed funding, the rest are financed from the Federal budget [14].

The main sources of R & d funding are private companies — 50 %, 46 % — the federal government, the remaining 4 % — educational institutions (universities, colleges) and non-governmental organizations [15].

In recent years, the main focus of investment in innovation in the US has become the defense industry, and their results are also for society. In recent years, the share of spending on the military industry has increased from 20 % to 50 % [16].

One of the important incentives for innovation development is the creation and support of venture funds and research centers. According to the US national fund, the most effective research centers and venture companies can be fully or partially financed from the federal budget for the first 5 years. Due to the high complexity, business risk and international competition, the state can fully finance the most effective and science-intensive research. Also in the United States there is a practice of issuing free licenses for commercial use of inventions obtained in the course of budget research and are owned by the state [17].

The competence of the state includes monitoring and forecasting of innovation processes, both at home and abroad. Also, the search for the most effective and profitable technologies for their implementation, state expertise of innovative projects [18].

Thus, we can say that the main directions of innovation policy in the United States are: forecasting standardization, optimization of management decisions, state examination of innovative projects, maintenance of innovation statistics, development of competition at the local and international level, well- established antitrust legislation, which has its history for more than 100 years.

Summing up, we can say that the main regulator in the innovation market is the state, which acts as a coordinator of innovation processes and directs the results of its activities to the development of priority sectors of the economy.

References

- Marshall, A. (1993). Printsipy ekonomicheskoi teorii [Principles of economic theory]. (Vol. 1, 451). Moscow: Prohress [in Russian].

- Kadyrov, R.F. (1991). Zapiski bankira [Notes of a banker]. Ufa: Prohress [in Russian].

- Tekenov, U.A. (2016). Zarubezhnyi opyt rehulirovaniia innovatsionnykh protsessov i eho adaptatsiia v usloviiakh kazakh- stan-skoi ekonomiki [Foreign experience of regulation of innovation processes and its adaptation in the conditions of Kazakhstan economy]. VestnikKazakhskoho natsionalnoho Universiteta - Bulletin of the Kazakh National University [in Russian].

- Ivanova, V.V. Natsionalnye innovatsionnye sistemy Rossii i ES [National innovation systems of Russia and the EU]. Moscow: Tsentr issledovanii problem razvitiia nauki RAN [in Russian].

- Lebedeva, T.P., & Mikhaylova, O.V. (2011). Hosudarstvennoe upravlenie v zarebuzhnykh stranakh: opyt administrativnykh reform [Public administration in foreign countries: experience of administrative reforms]. Moscow: Izdatelsvo Moskovskoho universiteta [in Russian].

- Dynkin, A.A. (2004). Innovatsionnye perspektivy SShA, ES, Iaponii [Prospects for Innovation, US, EU, and Japan]. Moscow: IMEMO [in Russian].

- Klimova N. V. & Larina N.V. (2014). Zarubezhnyi opyt stimulirovaniia innovatsionnoi deiatelnosti v promyshlennom sektore [Fundamentalnye issledovaniia Foreign experience in stimulating innovation in the industrial sector]. Fundamentalnye issledovaniia -Fundamental research, No. 6, 1442–1446 [in Russian].

- Blackhurst, K. (1985). Chto skryvaetsia pod bankovskim nadzorom v Velikobritanii? [What is hidden under banking supervision in the UK?]. Mezhdunarodnyi obzor Jinansovogo Zakonodatelstva - International financial law review, February, No. 2, 4–10 [in Russian].

- Avdokushin, E. (2010). Natsionalnaia innovatsionnaia sistema Iaponii [The national innovation system of Japan]. Voprosy novoi ekonomiki - Questions of the new economy, 4, 39–53 [in Russian].

- Davydenko, E.V. (2014). Problemy modernizatsii i perekhoda k innovatsionnoi politike [Problems of modernization and transition to innovation policy]. Problemy sovremennoi ekonomiki - Problems of modern economy, 2, 23–26 [in Russian].

- OECD Science, technology and Industry Outlook 2012. OECD. (2012). oecd.org. Retrieved from www.oecd.org/sti/oecdsciencetechnologyandindustryoutlook.htm (Organisation for economic cooperation and development) (accessed: 11.03.2014)].

- Kosov, G. (1997). Nalohooblozhenie filialov mezhdunarodnykh bankov i nadzor za ikh deiatelnostiu v Germanii [Taxation of branches of international banks and supervision of their activities in Germany]. Biznes i banki – Business and banks, 24, June, 25–29 [in Russian].

- Gonchar, K. (2009). Innovatsionnoe povedenie promyshlennosti: razrabatyvat, nelzia zaimstvovat [Innovative behavior of the industry: it is impossible to develop to borrow]. Voprosy ekonomiki - Questions of economy, No. 12, 125–141 [in Russian].

- Emelyanov, S.V. (2002). Stratehiia razvitiia nauki i tekhnolohii v SShA v 21 veke. Menedzhment v Rossii i za rubezhom [Strategy of development of science and technology in the USA in the 21st century. Management in Russia and abroad]. Moscow: INFO [in Russian].

- Gusmanova, F.A. (2009). Sovershenstvovanie mekhanizma rehulirovaniia bankovskoi deiatelnosti (na materialakh Respubliki Kazakhstan) [Improving the mechanism of banking regulation (on materials of the Republic of Kazakhstan)]. Karaganda: TOO «Hlasir» [in Russian].

- Iskakova, Z.D., Konakbayev, A.G. Gusmanova, Zh.A., Kurmanalina, A.K., & Rakhmetova, A.M. (2012). Rol hosudarstva v razvitii i modernizatsii bankovskoho sektora v postkrizisnyi period [The role of the state in the development and modernization of the banking sector in the post-crisis period]. Moscow: Izdatelskii dom «Ekonomicheskaia hzeta» [in Russian].

- Kalkabaeva, G.M., Kurmanalina, A.K., & Gusmanova, Zh.A. (2017). Current State and Forecasting of the Development of Bank Crediting in Kazakhstan. Journal of Advanced Research in Law and Economics. Quarterly Volume VIII Issue 4 (26) Summer 1161–1167 p. Impact — factor 1.25.

- Rakhmetova, A.M., Gusmanova, Zh.A., Kurmanalina, A.K., & Erzhanova, S.K. (2017). Directions encouraging banks in financing innovation sector. Bulletin of Karaganda University, Karaganda, 4, 231–239 [in Russian].