In the article the importance of the development of the Institute of tax administration in the fundamental transformation of the tax system is considered. Sufficient development of the tax administration system and the optimization of the work of the tax authorities are the necessary conditions for ensuring the financial security of Kazakhstan. In the article, tax administration is a complex socio-economic and political phenomenon, reflecting the degree of development of market infrastructure, public administration mechanisms and principles of civil society. The activity of the Ministry of Finance of the Republic of Kazakhstan is the main source of information for determining the policy and direction of the country. In the article the indicators used to monitor progress in achieving the country's goals are discussed and the changes after the reduction and simplification of administrative barriers in the Republic of Kazakhstan is analyzed. The article discusses the forms and methods of tax administration. In conclusion, the authors propose several principles of building a tax system for finding the optimal way of developing and improving tax administration in Kazakhstan.

One of the components essential for the fundamental transformations of the tax system is the formation and development of the institution of tax administration. Sufficient development of the tax administration system and the optimization of the work of the tax authorities are the necessary conditions for ensuring the financial security of Kazakhstan. Tax administration is a complex socio-economic and political phenomenon, reflecting the degree of development of market infrastructure, mechanisms of government and principles of civil society.

The significant source of a government's budget is taxes. Their full and uninterrupted receipt is impossible without the creation of an effective tax structure in the country. The tax structure of the Republic of Kazakhstan includes both tax authorities and customs authorities. The important part of the tax structure is the tax authorities, which are responsible for the collection of taxes and other obligatory payments to the budgets of all levels based on tax legislation [1].

Kazakhstan's strategic goal is to become one of the 30 most developed countries in the world. Therefore, the government revenue agencies of the Republic of Kazakhstan, as part of the public administration system, are obliged to take coordinated and coordinating measures to achieve this goal. The main task in implementing the measures taken is to ensure trust and partnership with the business community.

Indicators of achieving the goals are the positive dynamics in the international business competitiveness indices of the World Bank (VIC, «Doing Business», LPI) and indicators of customer satisfaction of government revenue agencies (survey results).

The «Doing Business» rating is an objective external assessment of the Government's actions to improve the business climate of the country and is conducted annually by the World Bank in most countries of the world using 11 indicators.

According to the results of the Doing Business-2018 report, Kazakhstan took the 36th place out of 190 countries. Improving the position of Kazakhstan in the World Bank's «Doing Business» rating is a priority for the country. The following indicators are in the competence of the State Revenue Committee of the Ministry of Finance of the Republic of Kazakhstan:

- Taxation;

- Resolution of insolvency;

- International trade [2].

According to the «taxation» indicator, Kazakhstan ranked 50th (from 190 countries). It has improved its performance by 10 positions.

These indicators have improved due to the reduction and simplification of administrative barriers:

- In the process of reforming the tax audit in 2017, the procedure for the appointment and conduct of audits was revised. As a result, for the 12 months of 2017, the number of tax and customs inspections hasbeen halved. In 2016, 77860 inspections were conducted. While, 42873 inspections were conducted in 2017, which is less by 45 % compared to the previous year. At the same time, the efficiency of tax audits was increased. The budget collected 94.8 billion tenge. The result increased by 1.5 times compared to 2016;

- From July 1, 2017, the procedure of the consideration of taxpayers' complaints about the results of tax control was changed. Now, appeal procedures are being held at the level of the Ministry of Finance. The Appeals Commission, including representatives of interested government agencies and from NPA Atameken, reviews complaints about notifications on the results of inspections. During the period from July 2017 to May 2018, a total of 300 complaints were received for a total amount of 96417.2 million tenge. 244 (94596.9 million tenge) of them were tax issues, and 56 (1820.3 million tenge) were custom issues. Only 154 complaints (22761.4 million tenge) were considered, of which 120 were tax (22014.1 million tenge) and 34 (747.3 million tenge) were custom. A decision was made in favor of the applicant in only 62 issues (4937.8 million tenge), 47 (4 540.6 million tenge) of the them were tax and 15 (397.2 million tenge) were custom issues;

- The new tax code provides for the return of the debit balance on value-added tax. That is, from January 1, 2019, any taxpayer who will use the VAT control account will be able to return the full amount of the VAT excess [3].

The first Code codified the norms, the second reduced the tax burden, and the task of the third Code is to change the ideology and simplification.

Ideology aims to protect the bona fide taxpayer. The administration has been simplified and will motivate self-pay taxes. In addition, a paradigm shift allows the use of new customer-oriented models: firstly, it is planning revenues with the business based on the new Driver Model; secondly, the reduction of inspections and economic investigations; thirdly, this is assistance from the government to the business through the reduction of tax reporting forms, the expansion of tax advice and the improvement of the infrastructure of government revenue agencies.

In response, the business will provide informational openness in terms of the information required for tax administration, which will allow combining the efforts of public control and the government revenue risk management system.

The rate of returning excess VAT for all categories of taxpayers is suspended until January 1, 2019 [3].

As planned measures to improve the position of Kazakhstan on the «Taxation» indicator, the followings are planned:

- Extract of electronic invoices by all VAT payers, as well as the introduction of a special VAT account;

- Return of the debit balance on the VAT in the presence of the control account.

Statistics on the number of registered VAT payers:

In order to reduce administrative barriers, the procedure for registering on value-added tax has been revised and simplified. Thus, in accordance with legislative changes, from May 1, 2017, taxpayers are entitled to register as a payer of VAT in the following ways:

- by filing a tax application for registration of the value-added tax on paper in ad-hoc order or in electronic form;

- at the government registration of a resident legal entity in the National Register of Business Identification Numbers.

That is, the mandatory procedure of a visit to the tax authority for registration has been abolished; at present, it is enough to fill out an electronic application on the «Taxpayer's Cabinet» web portal or mark the corresponding box when registering a legal entity through the e-government portal e.gov.

For 2017, the number of registered VAT payers in electronic form was 12713. For the first half of 2018 registered VAT payers in electronic form amounted to 15672. According to the International Trade indicator, Kazakhstan ranked 123rd (119 last year), dropping 4 positions. The reason for the decrease in this indicator is an excessive amount of time and financial costs of export.

The export of goods in the «International Trade» indicator does not mean only the customs procedure for exporting goods. This indicator includes all costs (time and cash costs for permits from other government agencies, broker processing of customs documentation, loading, transporting and unloading goods, etc.) related to the export and import of goods. Thus, according to the interdepartmental research (MOF, MID, MNE), the share of expenses for customs operations in this indicator is not significant and amounts to an average of $ 70 (out of $ 894) for financial costs and an average of 7 hours (out of 261 hours).

In order to simplify and speed up customs operations, to increase the effectiveness of the fight against corruption, work is currently underway to introduce electronic goods declaration with respect for the E-window principle.

On October 1, 2017, the Transit module of Astana 1 was implemented. Taking into account the fact that the new Code provides for the electronic declaration, on January 1, 2018, the Export 10 module was launched in the Astana-1 information system on the Asycuda platform. From April 1, the module «Import» and other customs procedures in which 100 % electronic declaration is provided (Table 1).

Table 1 Electronic declaration of goods

09.08.2018

|

Indicators |

Issued (p.) |

Green channel (p.) |

Red channel (p.) |

Yellow channel (p.) |

|

Transit |

317 465 |

295 693 |

2 379 |

19 393 |

|

Export |

46 314 |

43 714 |

256 |

2116 |

|

Import |

117710 |

74 436 |

5 830 |

32 377 |

|

Other procedures |

10 293 |

8 268 |

9 |

171 |

In general, this initiative of the Ministry of Finance was accepted positively by participants of foreign economic activity. This is explained by the fact that this information system is free for use by traders. Data updating is carried out by QGD forces without outsourcing.

The government revenue authority is a customer-oriented service with a highly efficient management system that ensures the economic security of the Republic, creating conditions for free international trade and the voluntary payment of taxes and payments.

In the Strategy for the future development of the government revenue agencies of the Republic of Kazakhstan, the main values are:

- Patriotism: ensuring the protection of the economic interests of the Republic, well-being, security, and prosperity of the citizens of Kazakhstan.

- Professionalism: improving professional skills in work, striving for new knowledge, application of modern information technologies and highly efficient working methods.

- Honesty: expression of the true attitude to work, objective opinion about its improvement, integrity and impeccable performance of their duties.

- Impartiality: ensuring a comprehensive, objective and unbiased approach to decision-making, the provision of public services to each client at a high level.

- Politeness: compliance with business ethics, display of courtesy in behavior, reflecting respect and attentiveness to each client.

The main objectives are:

- Stimulating trade by reducing barriers, improving foreign trade administration and ensuring the security of the customs border;

- Ensuring the completeness of the receipt of taxes, fees, and other obligatory payments;

- The adoption of effective measures to minimize the «shadow» economy;

- Increasing public satisfaction with the activities of government revenue agencies.

The main tasks include:

- Ensuring a balance between unhindered foreign trade activities and the necessary level of economic security at the customs border;

- Liberalization and optimization of tax, customs and other legislation aimed at reducing the administrative burden on business;

- Modernization of information systems with the prospect of transformation into a single technological platform for electronic interaction of customers with government revenue agencies;

- Ensuring effective work to counter the «shadow» economy, including by preventing the involvement of legal entrepreneurs in the «shadow» business;

- Improving the provision of public services to facilitate the implementation of voluntary fulfillment of obligations by customers through the creation of legal and technical conditions;

- Creating a system of motivation and control, providing anti-corruption, improving the culture of staff with the further development of personal capabilities and providing a high level of service to society;

- Improving the structure of the government apparatus and decision-making procedures that protect the rights and legitimate interests of individuals and legal entities;

- Ensuring active participation in international cooperation institutions and regional economic associations, information interaction with the business community [4].

The tax system of Kazakhstan is based on the principles of stimulating scientific and technical progress, bringing domestic producers to the world market for high-tech products, stimulating entrepreneurial production activities and investment activity, the equivalence and proportionality of tax collection from both legal entities and individuals, preventing tax discrimination, social justice, economic efficiency and other important principles.

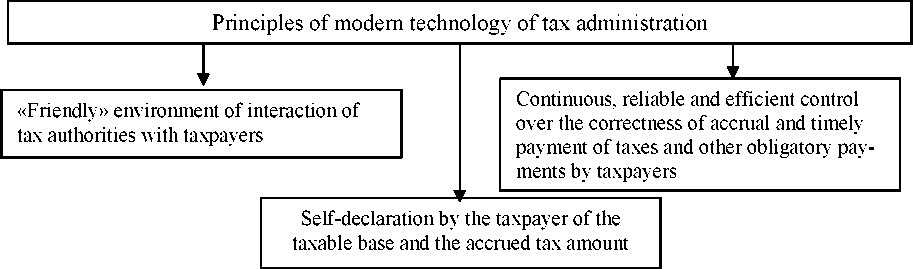

Tax administration ensures the implementation of the government tax policy. Tax administration is the most socially expressed sphere in which the government interacts with the population and business. Certain flaws or shortcomings, which can lead to a decrease in tax revenues and other mandatory payments to the budget, increase the likelihood of tax offenses, ultimately having a negative effect on our country's economy. In this regard, the modern technology of tax administration is determined by the following principles (Figure) [5].

Figure. Principles of modern technology of tax administration

The tax burden of the regional economy is estimated using the GDP indicator. Currently, the movement of financial flows is concentrated mainly in large cities, such as Almaty and Astana, as well as in the oilproducing regions of the country, which is related to the corporate interests of large taxpayers, which predetermined the concentration of cash in the financial centers of Kazakhstan, and the insufficient development of the banking sector in the regions, therefore, the task of tax administration is the relative leveling of the tax burden for the subjects of the Republic of Kazakhstan.

The complexity and rigid centralization of the organization of tax administration have different effects on economic entities — taxpayers; stimulate their economic development with the help of a complex of different methods.

Tax administration is a dynamically developing tax relationship management system that coordinates the activities of tax authorities in a market economy.

The economic situation in Kazakhstan requires the tax system to solve problems of timely replenishment of the Government budget, its balance in income and expenditure, reduce the deficit and external debt, and provide funding for regional needs. Ensuring the growth of tax revenues and increasing the level of tax payment collection remains a priority task for Kazakhstan tax authorities [6].

On another hand, the need to improve production efficiency at all its stages, eliminate the imbalances that arise during the restructuring of industries, as well as the task of raising the real standard of living of the majority of the population require reducing the tax burden. Favorable conditions are necessary for increasing the working capital of enterprises and organizations and stimulating their investment activities.

The tax potential of any region should be considered in terms of an evolving system. For this, it is necessary: first, to substantiate the content of informational links of the tax potential, focusing on the organizational and management structure of the tax system; secondly, to determine the functional tasks and content of tax monitoring, without which it is impossible to achieve high efficiency of tax administration at the regional level. The Government Revenue Department of the Ministry of Finance of the Republic of Kazakhstan is a unified system of agencies that monitor compliance with tax legislation. It implements its functions in relation to government and local taxes, which follows from the principle of the unity of government tax policy.

In accordance with the laws and regulations of the Republic of Kazakhstan, regulating the organization of the tax system, its main task is to control:

- execution of tax legislation;

- correctness of the calculation of taxes;

- completeness of tax calculation;

- timeliness of making taxes and other payments [7].

Tax administration is carried out on the basis of the following forms and methods:

Table 2 Tax administration forms and methods

|

Tax Administration Methods |

Tax Administration Forms |

|

Tax planning |

1. Tactical |

|

- assessment of the tax potential of the region |

|

|

- approval of the budget for taxes |

|

|

- development of control tasks |

|

|

- determination of share distribution of rates and benefits |

|

|

2. Strategic |

|

|

Tax regulation |

3. Tax incentive systems |

|

3.1. Change in tax due date |

|

|

- tax rate optimization |

|

|

- system of tax benefits |

|

|

- cancellation of advance payments |

|

|

- reduction of tax liabilities |

|

|

- reduction of the tax rate |

|

|

3.2. Granting tax and investment tax credit |

|

|

3.3. Deferral or installment payment |

|

|

4. Sanctions system |

|

|

- financial |

|

|

- administrative |

|

|

- criminal |

|

|

Tax control |

- registration and accounting of payers |

|

- receiving and processing reports |

|

|

- accounting of taxes and accrued amounts |

|

|

- control over timely receipt of payments |

|

|

- tax audits |

|

|

- implementation of verification materials |

|

|

- control over the implementation of materials verification and payment of accrued sanctions |

The management of tax processes involves not only specialized agencies. It involves all legislative and executive agencies, the Constitutional Court of the Republic of Kazakhstan, research teams of branches of institutes, universities, and public organizations, such as, for example, the Public Association for the Protection of Taxpayers' Rights. The tax relations of the payers and the government are also influenced by law enforcement agencies, auditing, advocacy and consulting and legal services. Their activities are also part of the tax relationship management process [8].

There is a need to change the structures and functions of tax administrations, aimed tax policy and methodological foundations of tax production, which causes the adoption of drastic measures, up to the next stage of tax reform.

For the optimal way of development and improvement of tax administration, it is necessary to designate the principles of the tax system. Modern principles of the tax system and the organization of tax policy are divided into three groups:

- Organizational, reflecting the administrative management of the taxation process (universality, uniformity, flexibility);

- Economic, determining the impact of taxes on the economy (efficiency, economy and tension);

- Legal, reflecting legislative certainty of tax relations (unity, stability, certainty).

References

- Kozhakhmetova, M.K. (2009). Nalohovoe administrirovanie [Tax administration]. Almaty [in Russian].

- Indikatory DoingBusiness, otnosiashchiesia k kompetentsii Ministerstva finansov Respubliki Kazahstan [Doing Business indicators within the competence of the Ministry of Finance of the Republic of Kazakhstan]. doingbusiness.gov.kz. Retrieved from http://doingbusiness.gov.kz [in Russian].

- Model perspektivnoho razvitiia orkhanov hosudarstvennykh dokhodov Respubliki Kazakhstan na 2015–2017 hody [Model of perspective development of government revenue agencies of the Republic of Kazakhstan for 2015–2017]. online.zakon.kz. Retrieved from http://online.zakon.kz. [in Russian].

- Goncharenko, L.I., & Anashkin, A.K. (2018). Nalohovoe administrirovanie: luchshe byt, chem kazatsia [Tax administration: it is better to be than to pretend]. Vash nalohovyi advokat – Your tax lawyer, 5 [in Russian].

- Izmailov, A.T. (2017). Nalohovoe administrirovanie i eho znachenie v povyshenii sobiraemosti nalohov [Tax administration and its importance in increasing tax collection]. [in Russian].

- Ospanov, M.T. (2007). Nalohovaia reforma i harmonizatsiia nalohovykh otnoshenii [Tax reform and harmonization of tax relations]. Saint Petersburg: UEF [in Russian].

- Ponomarev, A.I. (2015). Nalohovoe administrirovanie: sushhnost i formy [Tax administration: the essence and forms]. Nalohi i nalohooblozhenie – Taxes and taxation [in Russian].

- Pushkareva, L.V. (2017). Formirovanie sotsialno orientirovannoi sistemy nalohooblozheniia [Formation of socially oriented system of taxation]. Nalogi – Taxes, 1 [in Russian].