Information on costs in the system of information on the activities of construction organizations plays a significant role in making managerial decisions, since the main indicators characterizing the activities of the organization are the volume of costs and the cost of production calculated on the basis of data on costs. The relevance of this article lies in the fact that the technology of construction production has a number of specific features that affect the organization of analytical and synthetic accounting of business entities. High competition, the search for reserves to reduce the cost of construction products and increase profitability require information on the real level of costs, rationality of use various resources. In the management system of a construction enterprise, an important place should be given to management of construction costs. The article also considers analytical tools and recommends a combined system for calculating the cost of construction products in the organization of management accounting, ensuring the adoption of effective management decisions of the construction company. When writing the article, general scientific methods of cognition (statistical, normative analysis, synthesis, analogy, generalization), empirical-theoretical (collecting, studying and comparing data), as well as methods of scientific cognition (historical and legal, systemic) were used. When processing and systematizing data, grouping and classification methods were used. The information-statistical base of the study was made up of data from official periodicals and information- analytical publications of the Republic of Kazakhstan.

Features of cost accounting and calculation in construction organizations is a separate branch of the economy, characterized by certain relationships between its subjects. At the same time, questions of the economic content of production costs are important, since economists often put different contents in the same concept of costs, which leads to a misinterpretation of economic processes.

In domestic scientific publications there are many classifications of the method of accounting for production costs and calculating the cost of production.

Analyzing the studies conducted in this area, we can conclude that one group of researchers considers methods of cost accounting and costing, which supplies only the information created at the stages of accounting for production costs. However, we adhere to this point of view, since the component of management accounting is production accounting, which is understood as accounting for production costs, calculation and cost analysis. Based on information on production costs, management decisions are made.

The main task of accounting for the cost of construction works is the reflection of costs: timely, reliable and as complete as possible. These costs are associated with the production of construction work, the delivery of construction work to the customer, the determination of possible deviations from accepted standards and planned costs, proper control over the use of production resources [1].

Analyzing the studies conducted in this field, we can conclude that one group of researchers considers methods of cost accounting and costing, which provides only information created at the stages of accounting for production costs.

The development of market mechanisms highlights the need to measure production costs and profits, their balance relative to each other, which is the basis for sustainable development of the enterprise. In these conditions, to develop effective management decisions, it is necessary to create a cost management system that ensures a constant focus on the final results of production.

Construction has its own characteristics, which leave their mark on the organization of management accounting, including costing and budgeting. A feature of construction work is the duration of the production cycle [2]. As a rule, the execution of contractual agreements takes more than one month. The time and cost of material resources for the construction of a residential building or household facility cannot be compared with the production of food and non-food products. During this time, prices may change, the economic situation in the country, which means that it is necessary to achieve constant cost reduction in construction by improving equipment, technology and construction management. Therefore, the most important task of cost accounting and calculation in this industry is to minimize the cost of construction production [3].

As T.N. Shevchenko notes in his publications on cost accounting and costing in various industries, construction has its own characteristics:

- In construction, there is always work in progress, which complicates cost control.

- Construction objects cannot be transported, that is, a strict accounting of supply and demand is necessary.

- The depreciation period is longer than that of machinery and equipment, it is necessary to carry out reconstruction and modernization, which saves time and money in comparison with new construction, and all this must be taken into account when establishing depreciation rates.

- The assessment of the construction site is very complex and requires:

- firstly, the calculation of numerous qualitative indicators;

- secondly, highly professional specialists, etc.

Thus, the goals and objectives of calculation and budgeting in construction are different from the goals and objectives in industry. For proper cost accounting in construction, it is necessary to keep records separately for each contract. To calculate the costs corresponding to the income received during the reporting period, you must have information about the actual costs, the reimbursement of which is provided for by the contract.

Analytical accounting of the costs of the main production is carried out for each type of work in the statement of type of cost, where the actual cost of each completed and commissioned object (type of work) is generated. In analytical accounting, a separate analytical account is opened for each calculation object of construction and installation works.

In the management accounting system, the procedure for generating cost is not so regulated. This cost is not formed for tax purposes, but to ensure that the manager has a complete picture of the costs. Therefore, in the system of this accounting, various methods for calculating the cost can be used (depending on which managerial task is being solved).

According to IFRS 11 «Accounting for construction contracts», the costs arising in the course of the implementation of the construction contract can be grouped into three main elements (International Financial Reporting Standard (IAS) 11 «Construction Contracts»).

The calculation method of accounting for production costs, used in domestic accounting practice, involves the formation of overhead costs separately, by industry or even by the enterprise as a whole, and is subject to write-off at the end of the reporting period by ownership with their simultaneous distribution between calculation objects, in the context of which an analytical accounting in proportion to the distribution base adopted in the industry. Most often, overhead costs are distributed in proportion to the direct costs or salaries of the main production personnel, after which the process of calculating the total cost of production is carried out [4].

Overhead costs with the same characteristics are distributed between the objects in a calculated way based on the normal (optimal, normative) level of construction activity. Overhead costs of construction may also include borrowing costs if the contractor uses an alternative accounting method in accordance with IAS 23 «Borrowing Costs».

Grouping by cost element is the basis of the estimated cost of production — a planning document that reflects all the costs of the enterprise due to the release of a certain volume of industrial products for both its own divisions and third-party customers.

Recognition of costs under construction contracts is carried out by the following entries:

Dt1340 — «Construction in progress»;

CT — accrued wages to workers:

- accumulated depreciation of fixed assets used during construction;

- the cost of renting machinery and equipment;

- the costs of design and engineering support in the implementation of work on a specific object, etc.

The distribution (allocation) of costs is necessary in order to obtain data intended for:

- calculation of the cost of the product;

- assessment of the quality of management and control;

- making informed and timely management decisions.

The procedure for the distribution of overhead costs by accounting objects (contracts; projects; construction objects, types of work, etc.) is determined by the business entity itself and reflected in the accounting policy.

Overhead costs can be allocated to accounting objects:

- in proportion to direct costs;

- in proportion to the contractual (estimated) cost of construction and installation works;

- in proportion to the cost of paying workers in the main production;

- in proportion to the number of spent machine shifts (for the costs of operating construction equipment and in structural units of mechanization);

- other methods.

To determine the cost of construction at various stages of the investment process, one should use a system of norms of overhead costs, which according to their functional purpose and scale of application are divided into the following types:

- aggregated standards for the main types of construction;

- standards for the types of construction work;

- individual standards for a specific construction organization;

- marginal norms of overhead costs for construction work, designed to determine the cost of work at a basic price level.

Information base for control and analysis are:

- business plan of a construction organization — statistical reporting;

- work schedules;

- acts and certificates of admission of complexes (stages) and volumes of work;

- report on the costs of production and sales of products f-5-z;

- report on the costs of basic building materials;

- data of synthetic and analytical accounting [5].

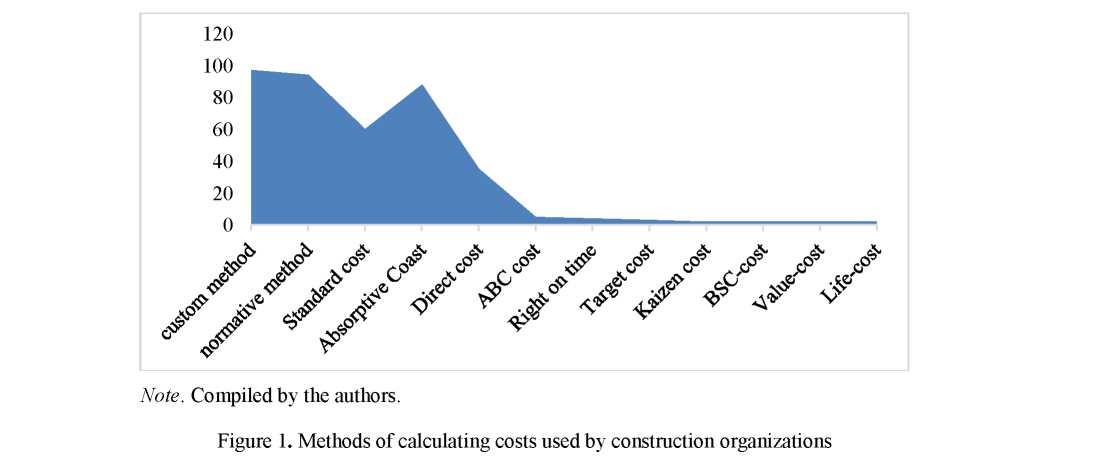

As in industry, the most important task of management accounting in construction is cost control. Modern construction organizations in their activities apply different methods of calculating costs, using traditional means and new developments. Nevertheless, many operating enterprises continue to fully use the traditional methods of calculation [6].

Methods of calculating costs used by construction organizations are presented in Figure 1.

According to Figure 1, when performing work, some large companies successfully use the entire list of tools listed, however, not all companies can afford to use such tools, which indicates the complexity of the work and in the large volumes of tasks solved by the management accounting system.

In his research, Davison J. confirms and proves that in order to choose one or another calculation method, the company management must present the specifics of each of them and the result that can be obtained by their application, and which will affect the financial result of the entire company.

A.Sh. Margulis in his work «Costing in industry» also considers the cost accounting method and the costing method as a single process of studying the costs of certain types of enterprises for the production and

sale of products from the standpoint of measuring, controlling, determining the cost of products and works; he notes that «the artificial separation of calculation methods from cost accounting methods leads to the technicalization of processes for calculating the cost of production and does not follow from the economic nature of cost accounting methods» [7].

Thus, based on the analysis of the study of the methods of calculating costs used by construction organizations, it is advisable to distinguish the classification of methods of cost accounting and costing the cost of production of construction organizations [8].

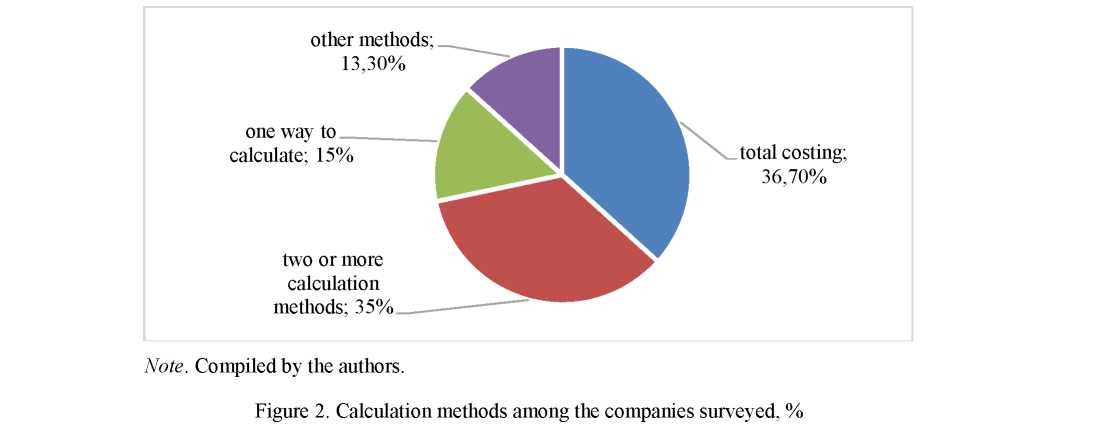

Classification of methods for cost accounting and costing of production costs of construction organizations is presented in Figure 2.

In the process of analyzing and studying the different opinions of academic accountants, economists and financiers, we came to the conclusion that the process of organizing accounting, managerial accounting and cost management allows us to identify approaches to classification:

- - management accounting methods (traditional methods of cost accounting);

- - cost control methods (budgeting, cost accounting for deviations);

- - methods of strategic management accounting (which are used before the start of construction activities).

Based on this classification of cost accounting methods that are used in construction organizations and stages of construction, it is necessary to correctly allocate costs in relation to the created product, as well as in the context of each of the activities and divisions. In addition, the level of expenses should be controlled, since the result of the work will depend on this.

According to L.N. Gerasimova and D.N. Silka needs to use the model of toolkit formation for cost management taking into account the life cycle of construction products and construction stages, which will make it possible to effectively manage all economic indicators during the adoption of diverse managerial decisions [9].

A questionnaire survey of construction companies conducted in the USA back in 2017 showed that more than 30 % of the 394 companies participating in the study use two or more calculation methods. Of the companies surveyed, 36.7 % use full costing [9].

In the scientific literature on the accounting of costs in construction, two classical methods are distinguished: the custom-made method of accumulating costs over a certain period of time by type of work and cost center [10]. In this case, various methods of calculating the cost of work performed and evaluating construction in progress [11].

Some economists use unconventional approaches to classifying cost accounting methods that can be adapted to the construction industry. So, in the work of I. Kuleshov methods of cost accounting are classified depending on the stage of the circuit of the nominal and real property of the enterprise [12]. O.V. Kaurova and O.S. Yumanova noted the need to take into account the practice of cost accounting and distinguish methods such as custom, alternate, process, part-price, part-time, depersonalized («boiler»), normative [13].

I. Tkachenko in his scientific articles notes that the most common method of accounting for costs of construction works is the custom method, when the accounting object is a separate order opened for each construction object (type of work) in accordance with the contract concluded with the customer for the performance of works, according to which cost accounting is kept on an accrual basis until the completion of work on the order. In this case, the cost of the order is determined by the sum of all production costs from the date of its opening to the day of completion and closing. Reporting costing with a custom accounting method is made after the work on the order is fully completed, which is a significant drawback of this method [14].

V. Fovanov claims that the specifics of the management and organization of accounting for construction products, construction is determined by the characteristics of the construction industry. The costs of the contractor in the performance of contract construction work relate to the costs of ordinary activities and are the sum of all actually incurred costs associated with the production of contract construction work performed them according to the construction contract, namely: from the cost of the materials used in the construction process 'an and labor, the depreciation of fixed assets and amortization expenses, as well as other types of costs [15].

The costs of contracting construction work are recognized in the accounting records subject to the following conditions:

- the expense is made in accordance with a specific contract, the requirements of legislative and regulatory acts, and business customs;

- the amount of consumption can be determined;

- there is confidence that as a result of a particular operation there will be a decrease in the economic benefits of the organization.

When forming the cost of construction products, there is an assumption of temporary certainty of the facts of economic activity, that is, the cost of construction work is included in the cost of the work of the calendar period to which they relate, regardless of the time of their occurrence and regardless of the time of payment — preliminary or subsequent [16].

In order to increase the significance of the information generated in the accounting of construction organizations for making effective management decisions, it seems to us that it would be appropriate to use a combined system for calculating the cost of construction products using the ABC method (Activity Based Costing). In this case, ABC-calculation should be considered as an additional method in relation to the traditional custom-made calculation method in construction.

We would also like to note the fact that for each stage and each stage of construction activity, we can distinguish characteristic methods and models of managerial accounting, and the combination and application of certain methods can lead to the creation of a mechanism for consistent, targeted management of the costs of building an object (Table 1) [17].

Table 1

The effectiveness of the application of cost management tools during the construction phase

|

Indicator |

Kaizen costing |

Standard Costing / Regulatory Accounting |

The method of forming the full cost |

Direct costing |

Custom method |

Cost accounting at the place of their occurrence |

|

Customer |

- |

- |

- |

- |

- |

- |

|

General contractor |

+ |

- |

+ |

+ |

+ |

+ |

|

Subcontractor |

- |

+ |

+ |

+ |

+ |

+ |

|

Mixed type of contract |

+ |

+ |

+ |

+ |

+ |

+ |

Note. Compiled by the authors.

There are a sufficient number of methods by which you can calculate the cost of production. To choose one or another calculation method, the company management should be well aware of the specifics of each of them and the result that can be obtained by applying them, and which will affect the financial result of the entire company [18].

Enterprises, using one or another calculation method in construction with cost accounting, are looking for ways to reduce production costs (Table 2).

Table 2 Cost reduction measures

|

No. |

Factors |

Actions |

|

1 |

Factors independent of the activities of the construction organization |

Changing the structure of work in the planning period |

|

Introduction of new tariff networks and rates |

||

|

Change in selling prices for materials and components |

||

|

Change in freight rates |

||

|

Change in estimated standards in the documentation (installation, equipment) |

||

|

2 |

Intrinsic factors |

Resource Consumption |

|

Decrease in shift losses (working hours, downtime) |

||

|

Choosing the best suppliers |

||

|

Cost reduction (transport, storage) |

||

|

Mechanization and automation of work |

||

|

Application of constructive solutions |

||

|

Rational organization of work:

|

Note. Compiled by the authors.

Thus, no matter what methods of calculating the cost of production in the construction industry will be used by enterprises, the main task is to reduce the cost of construction and installation works, as well as saving all types of resources — labor and material.

The lack of control over the expenditure of building materials artificially inflates the cost of construction of the company, therefore, the cost of construction and installation works is the most important indicator reflecting the activities of the construction organization, which determines the financial results, financial situation, and competitiveness of the construction organization. Therefore, constant monitoring of the formation of the cost of construction products and the search for ways to reduce it are necessary. The difference between the actual and the possible volume of construction and installation work, calculated on the basis of the largest average monthly (average quarterly) volume of work, shows the missed opportunities of the construction organization to increase construction volumes due to irregular work. The largest share in the cost of construction products is material costs, the size of which depends on:

- - on the volume and structure of construction and installation works;

- - norms of material consumption per unit of work performed;

- - the cost of material resources;

- - a change in the quality of building materials;

- - qualifications of employees;

- - volume of rejected products;

- - the level of organization of control over the safety and efficiency of use of material resources.

In order to realize the most important function of management accounting in construction organizations — «management by deviations», it is necessary to periodically calculate deviations between the actual and possible (planned) volumes of work for each responsibility center, which are objects, sites, etc. For this, management reports for each responsibility center.

The analysis showed that for each stage of construction activity, the most characteristic methods and models of managerial accounting can be distinguished, and a reasonable and consistent combination, and in some cases the complex application of the described methods, will lead to the creation of a mechanism for consistent, targeted management of construction costs.

References

- Saperova, E.I. (2018). Osobennosti ucheta sebestoimosti v stroitelstve [Features of cost accounting in construction]. Molodoi uchenyi — Young scientist, No. 18, 362-364 [in Russian].

- Shevchenko, T.N. (2016). Uchet zatrat i kalkulirovaniie sebestoimosti v razlichnykh otraslyakh proizvodstva [Cost accounting and costing in various industries: Training manual]. Bishkek: KRSU [in Russian].

- Mezhdunarodnyi standart finansovoi otchetnosti (IAS) 11 «Dohovory na stroitelstvo» online.zakon.kz. Retrieved from https://online.zakon.kz [in Russian].

- Avrova, I.A. (2006). Orhanizatsiia ucheta v stroitelstve [Organization of accounting in construction]. Moscow: Berator [in Russian].

- Nazarova, V.L. (2009). Kak vesti bukhhalterskii uchet v stroitelstve [How to keep accounting in construction]. Almaty: Bukhhalter [in Russian].

- Davison, J. (2015). Visualising accounting an interdisciplinary review and synthesis. Accounting and Business Research, Vol. 45, Issue 2, 121-165.

- Margulis, A.Sh. (1980). Kalkuliatsiia sebestoimosti v promyshlennosti [Industrial Costing]. Moscow: Finansy i statistika [in Russian].

- Zimakova, L.A., Tsyguleva, S.N., & Serebrennikova, I.V. (2014). Primenenie metodov i modelei upravlencheskoho ucheta na raznykh stadiiakh stroitelnoi deiatelnosti [Application of methods and models of management accounting at different stages of construction activity]. Mezhdunarodnyi bukhhalterskii uchet, No. 42 (336), 5-10 [in Russian].

- Gerasimova, L.N., & Silka, D.N. (2019). Innovatsionnye metody upravlencheskoho ucheta v stroitelnoi orhanizatsii [Innovative methods of management accounting in a construction organization]. VestnikMHSU, Vol. 1,1, 60-71 [in Russian].

- Budasova, V.A., & Yegorova, S.Ye. (2017). Sravnitelnyi analiz osnovnykh kalkuliatsionnykh priemov v upravlencheskom uchete [Comparative analysis of the main calculation methods in management accounting]. pskgu.ru. Retrieved from http://pskgu.ru/projects/ pgu/storage/wt/wt13/wt13_39.pdf. 11 Druri K. Vvedeniye v upravlencheskiy i proizvodstvennyy uchet. Moscow: YUNITI [in Russian].

- Drury, K. (2017). Introduction to management and production accounting. Moscow: UNITY [in Russian].

- Kuleshova, I.B. (2013). Teoreticheskie osnovy upravlencheskoho ucheta proizvodstvennykh zatrat [Theoretical foundations of management accounting of production costs]. Upravlencheskii uchet, No. 7, 7-9 [in Russian].

- Kaurova, O.V., & Yumanova, O.S. (2013). Sistema ucheta zatrat hostinits i analohichnykh sredstv razmeshcheniia: mezhdunarodnaia i otechestvennaia praktika [Cost accounting system for hotels and similar accommodation facilities: international and domestic practice]. Upravlencheskii uchet, No. 7, 7-9, 60-65 [in Russian].

- Tkachenko, I.Yu. (2017). Osobennosti ucheta zatrat na proizvodstvo stroitelnykh rabot [Features of cost accounting for construction works]. Moscow: UNITY [in Russian].

- Fovanov, V.A. (2008). Uchet zatrat i kalkulirovanie sebestoimosti produktsii razlichnykh otraslei [Cost accounting and costing ofproducts of various industries]. Moscow [in Russian].

- Semenova, F.Z., & Adzhieva, A.Sh. (2017). Otdelnye aspekty ucheta zatrat v Stroitelnykh Orhanizatsiiakh [Some aspects of cost accounting in construction organizations]. Vestniknauki i obrazovaniia, Vol. 1, No. 5 (29), 30–35 [in Russian].

- Adamov, N.A., & Chernyshev, V.E. Orhanizatsiia Upravlencheskoho ucheta v stroitelstve [Organization of management accounting in construction]. Seriia Bukhhalteru i auditoru, 192. Saint Petersburg: Piter [in Russian].

- novapdf.com. Retrieved from http://www.novapdf.com