The article considers modern trends of long-term bank crediting of enterprises of the real sector of Kazakhstan's economy. The main reasons for the low activity of second-tier banks in investment lending have been identified. The factors that had a negative impact on long-term loans of Kazakhstan banks provided to the real sector of the economy are justified. A comparative analysis of the proportion of long-term loans in GDP. The methods and tools of state regulation of the activities of second-tier banks on long-term lending to subjects of the real sector of the economy are systematized. One of the directions of the public economic policy is the regulation of investment activities of commercial banks, which is aimed, on the one hand, to contribute to the socio-economic development of the country, and on the other hand, to ensure the financial stability of the banking system as a whole and an appropriate level of protection of the interests of banking services' consumers. The economic-mathematical model for forecasting the volume of long-term bank lending and the impact on them of macroeconomic regulation instruments in the Republic of Kazakhstan is presented. Measures to create conditions for the development of long-term bank lending are outlined.

One of the directions of the public economic policy is the regulation of investment activities of commercial banks, which is aimed, on the one hand, to contribute to the socio-economic development of the country, and on the other hand, to ensure the financial stability of the banking system as a whole and an appropriate level of protection of the interests of banking services' consumers.

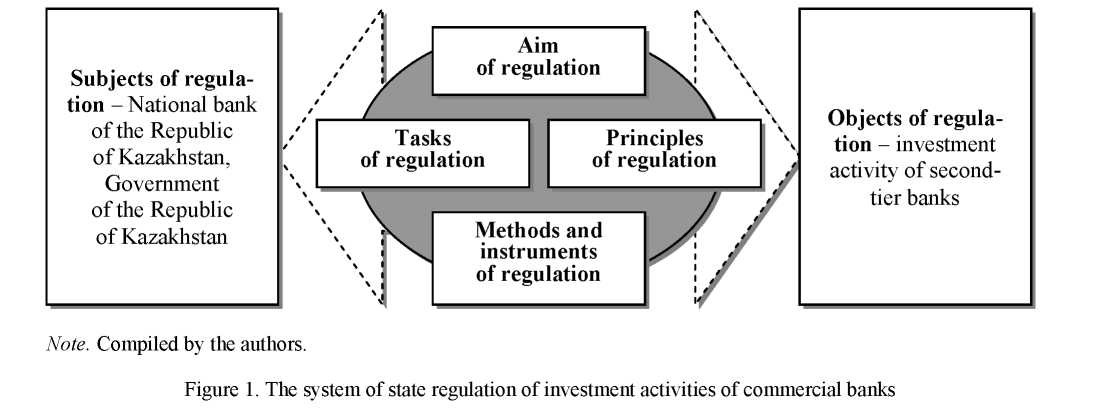

The object of regulation in this case is the investment activity of banks, which in frames of the macroeconomic aspect can be understood as an activity which is aimed at meeting the investment needs of the economy. It is known that the main criterion for classifying a certain type of banking activity as an investment is the productive orientation of the bank's investments. Industrial investments, acting as a form of the bank's participation in capital expenditures of economic entities, are carried out by providing investment loans and various ways of participating in financing investment projects.

It should be noted that there are three types of commercial bank activities in investment process: servicing the movement of funds owned by investor-clients and intended for investment purposes; cooperation in accumulating money holdings and savings for investment purposes through the securities market; investments in investment projects of own financial resources and borrowings. Issues of the theory of investments and investment activity have been studied in the scientific papers of many scientists and economists. Studying the activities of Kazakhstani commercial banks in the field of investments, it can be noted that in the vast majority of cases it is limited to banking services for the movement of investment capital of investor-clients, and only 8-10 % of the credit resources of second-tier banks are allocated for the acquisition of fixed assets. In order to enhance the participation of commercial banks in the investment process, effective state measures are needed that will allow to secure investment priority for a long term and ensure most favored nation treatment.

The peculiarity of regulation of the investment activity of commercial banks is defined by the final results — achievement of the efficiency of the investment activity of commercial banks through the matching of the volumes and directions of this activity with the needs of the country's socio-economic development.

Confirming the existence of specific principles of state regulation of banking investment activities, these include: efficient use of resources and regulatory tools, transparency of banks activities, ensuring financial stability of the banking sector; stimulation of investment operations in a certain quantitative scale by banks.

In this regard, we have the opportunity to show in combination the composition of all the elements that form the system of state regulation of investment activities of commercial banks, in accordance with Figure 1.

The impact of the state on the investment activities of commercial banks is carried out through:

- Instruments of prudential regulation, monetary policy, tax regulation, the establishment of rules and requirements for commercial banks;

- the allocation of financial resources of the state (lending, corporatization) and banking activities by administrative methods (permits, direct quantitative restrictions, prohibitions);

- establishment of special institutions whose operations have an impact on the volumes and directions of investment banking, as well as through the creation and development of industries, business activity objects interacting with the banking sector.

The legislative basis for the regulation of banking activities in the Republic of Kazakhstan is represented by the Laws of the Republic of Kazakhstan «On Banks and Banking Activities in the Republic of Ka- zakhstan», «On the National Bank of the Republic of Kazakhstan», regulatory legal acts, as well as special laws, ensuring the functioning and development of the banking business infrastructure. The legislative impact is aimed to ensure, first of all, the financial stability of the banking sector, to force commercial banks to take certain actions or to limit them, in order to protect the interests of market participants, minimize the risks of their activities, effective economic development, which is defined by achieving the required macroeconomic parameters.

Excessive concentration of ownership of non-financial enterprises in banks is associated with an increase in banking risks, a decrease in the reliability and stability of the banking system. In this regard, the existing laws and regulations contain a number of restrictions on the participation of banks in economic activity. Among them, it should be noted, first of all:

- a legislative ban on engaging in productive activities;

- limiting the participation of banks in the capital of other enterprises and organizations;

- limitation of investments in the acquisition of shares (stocks) of one legal entity;

- various credit risk restrictions;

- other restrictions (antitrust rules, regulations governing participation in financial and industrial groups).

According to banking legislation, the authorized bodies establish regulatory restrictions on the banks activities by approving prudential standards and other mandatory norms and limits for banks, provisions against doubtful and hopeless assets, minimum reserve requirements, and the procedure for switching to international standards.

Considering the theoretical content of prudential standards, it should be noted that they include the limit values of risks accepted by credit organizations established by the regulatory body, the norms for creating reserves to ensure their liquidity, requirements whose non-fulfillment can negatively affect the financial situation of credit organizations. In turn, prudential standards in the Republic of Kazakhstan include the minimum size of the bank's authorized capital requirements, capital adequacy ratio, the maximum size of the risk for one borrower, liquidity ratios, restrictions on capital structure and maximum size of the banks' investments in fixed assets.

Except prudential standards, the authorized body can affect directly the investment activities of banks through the establishment of requirements for the placement of a part of funds in certain types of assets.

The policy of prudential regulation of investment activities of commercial banks is complemented by monetary policy measures. This is due, first of all, to the fact that the supply of money supply in a market economy mainly consists of bank liabilities. It is obvious that the wider the money supply, the wider the resource potential of banks for investment activities. Monetary policy can be characterized as a part of the integrated public macroeconomic policy in the field of monetary relations aimed at improving the stability of economic processes, controlling inflation, improving the investment climate, creating prerequisites for economic growth and equalizing the balance of payments.

Comprehensively studying the instruments of monetary policy, it can be noted that most of them relate to indirect measures of influence. In Kazakhstani practice, such measures include interest rate policy, establishment of reserve requirements, operations on the open market.

In this case, interest rate policy, being an integral part of monetary policy of the central bank, aimed at regulating the interest rates on the money market in the country to achieve its goals. It has a significant impact on the inflationary expectations of economic agents and forms the conditions for the functioning of the national economy.

By adjusting the interest rates on the instruments, the central bank seeks to address some tasks of monetary policy, such as the formation of return; preventing the influx of significant volumes of speculative capital and the formation of profitability in the market, which cannot be provided by the national economy and the banking system on a sustainable basis; the formation of market expectations that this practice of setting rates will continue in the medium term.

At the same time, the use of this tool shows that the results of monetary policy are poorly predictable. In the short term, a decrease in the refinancing rate is a «broad» measure, in the long term it can be as a restraining measure respectively.

Changing the official discount rate as an instrument of monetary regulation is widely used by central banks of developed countries, while in developing countries, direct interest rates on loans and deposits of commercial banks are mainly preferred.

In the Republic of Kazakhstan, within the framework of the interest rate policy, the National Bank has an official base rate, interest rates on reverse repurchase transactions in order to influence market interest rates on the financial market as part of the current monetary policy. According to the legislation of the country, the official base rate is set depending on the general condition of the money market, supply and demand for loans, inflation and inflation expectations. The official base rate is a benchmark for interest rates for basic monetary policy operations [1].

The most important task of the National Bank of Kazakhstan (NBK) is to improve the refinancing system of banks. The NBK, responsible for the stability of the banking system, should create an effective mechanism for providing banks with cash resources. He does this by providing loans to financially stable banks secured by reliable securities for a short period (1,7, 30 days).

The minimum reserve requirements play a special role in the monetary regulation system of Kazakhstan. Mandatory reserves represent the percentage of cash from liabilities of a commercial bank, which is held in accordance with the legislation with the central bank as reserves. Traditionally called the dual purpose of the system of reserve requirements: the current regulation of bank liquidity; current regulation of the loan market and the issue of credit money by commercial banks.

As practice has shown, a frequent revision of the mandatory reserve requirements, which is an instrument for tight regulation of the issue of credit money and liquidity of the banking system, does not give the desired effect. To regulate the money supply, central bank operations in the open market are becoming increasingly important. To guarantee the solvency of banks, a deposit insurance system has been introduced in many countries. In addition, a frequent change in standards can and in some cases led to a backlash. Many banks either stocked up excess reserves, or sought in different ways to circumvent reserve rules.

In the Republic of Kazakhstan, the mechanism of minimum reserve requirements has been amended in terms of determining the minimum reserve requirements themselves, as well as the structure of bank liabilities accepted for calculating the minimum reserve requirements and the structure of reserve assets. So, cash desk and correspondent accounts in foreign currency were excluded from the structure of reserve assets. The formation of reserve assets of banks only at the expense of assets in tenge will allow the National Bank of the Republic of Kazakhstan to adequately assess the level of free tenge liquidity in the money market, more clearly respond to changes in demand for the national currency and, accordingly, increase the efficiency of liquidity regulation operations [2].

In the future, taking into account the result of the analysis of the current standards of minimum reserve requirements and international experience in order to increase the transmission function of reserve assets, we will consider the issue of limiting the use of cash in tenge when meeting the minimum reserve requirements, since from the point of view of monetary policy this component is poorly regulated.

In the system of monetary regulation of the economy of Kazakhstan, an open market policy is becoming increasingly important. The main condition for the functioning of the open market policy is the availability of a securities market in the state.

The central banks of many countries use open market operations to reduce or increase the excess reserves of commercial banks, thereby affecting their credit potential. The use of this tool affects the level of interest rates and, accordingly, the foreign exchange and capital markets [3].

Open market policy, in our opinion, is the most effective monetary policy tool in the presence of a developed securities market. Unlike other economic instruments, it has a quick corrective effect on the liquidity level of commercial banks and the dynamics of the money supply in the country, which is especially important during short-term market fluctuations. The independence of the central bank in the application of this instrument makes its regulatory influence quite significant, accurate and effective in the presence of a developed securities market and the use of reliable forecast models. In addition, the consequences of conducting operations on the open market can be adjusted by performing the reverse operation.

The ability to conduct operations on the open market immediately after a decision is made and in arbitrary volumes makes this method of monetary regulation convenient for absorbing small amounts of excess money supply. It is this use of open market operations that prevails in a number of countries, including Germany. In other countries (for example, in the UK) open market operations are carried out mainly to stabilize long-term government obligations. This strategy to a greater extent corresponds not to direct transactions with securities, but to regulation of the conditions under which the Central Bank agrees to conduct these operations.

At the same time, open market operations are not used on the same scale by central banks of different countries. The main obstacles to their intensive use are, firstly, the underdevelopment of the secondary securities market, and secondly, the insufficient funds for conducting operations on the necessary scale.

When analyzing the effectiveness of monetary policy in the Republic of Kazakhstan, it should be noted that at present, the National Bank of Kazakhstan has a fairly limited list of instruments. Liquidity can be withdrawn by the National Bank of the Republic of Kazakhstan by issuing short-term notes and attracting deposits, and liquidity can be withdrawn by means of refinancing loans and repos. Open market operations are still not in high demand [4].

The main reason for the impossibility of using open market operations to sterilize the money supply is the underdevelopment of the national financial market. Moreover, in modern conditions, government securities continue to be an insufficiently attractive investment tool for commercial banks.

Based on the foregoing, it can be argued that monetary control instruments aimed at combating inflation can put significant pressure on the investment activities of commercial banks. The ability of the inflationary component of bank investments to influence the economy as a whole and the inflation rate in particular requires a comprehensive and balanced approach to its study, measurement and evaluation, the selection of those indicators that are most closely related to the goals of economic development. Otherwise, in an effort to achieve a secondary goal (slowing inflation), you can simply cross out the solution to the objectively main task — to maintain a stable positive rate of economic growth.

Permissible government intervention in market mechanisms can be varied. For example, in Japan this is carried out in accordance with the concept of «life cycles» of industrial production. Its meaning is that state intervention should follow the line of change in the «life cycle». In some industries, large-scale government intervention is observed at the initial stage of the «life cycle». After the full development of the industry, it drops sharply. If the industry is faced with hard-to-solve problems, then it intensifies again [5].

Of course, the industrial policy of the state should contribute to the development of the competitiveness of the domestic economy in the world market, its growth, efficiency and follow national interests. As international experience shows, the state influences the investment process by regulating interest rates and cash flows.

Strict regulation of interest rates was applied in France, in the USA, post-war Japan. This method has been successfully used in a number of countries in Southeast Asia, China, India, and the countries of the Near and Middle East, providing a high level of capital accumulation and economic growth rates.

The development of the production sector is also achieved through targeted regulation of cash flows and the transformation of domestic savings into production investments through commercial banks. The steady growth of investment activity in post-war Japan was largely determined by state control over the use of population savings. They accumulated in savings banks and pension funds. They were provided as liabilities to the Japan Development Bank and other investment institutions [6].

In France, the mechanism for transforming savings into investments relied on postal savings institutions that attracted deposits, and on specialized credit institutions created to provide targeted loans to housing, agriculture, the hotel complex and various industries.

In India and China, the main cash flows were directed by state banks responsible for investing accumulated savings and attracted credit resources in the development of production — investment was carried out in accordance with centrally determined priorities for socio-economic development and at adjustable interest rates.

The direct impact on the investment activities of commercial banks, in addition to the measures of prudential and monetary regulation may have the use of tax policy instruments. The principle of comprehensiveness should be based on the system of tax stimulation of investment activity of banks: the corresponding potential of the taxation system should be used by the state along with other levers to stimulate investment activity — monetary policy by forming an effective financial market infrastructure, an active industrial and structural policy.

Another major principle of tax incentives for investment activities of banks is systematic: to reorient financial flows from banking to the real sector of the economy, tax incentives are needed for both investment operations of banks and investment demand and supply. Moreover, the high riskiness of investment operations of banks and the need to divert significant resources over the long term require stable and clear tax legislation, as well as effective judicial protection of the rights and interests of taxpayers and the state. The tax regulation policy should aim to create an institutional and legal economic environment that promotes investment in the real sector of the economy.

The next important element in the mechanism of state regulation are direct impact methods. In modern conditions, the possibilities of directive disposal are significantly limited and can extend only to those types of activities and operations that, in the opinion of regulatory authorities, can carry serious risks and threats for both the banking sector and the country's economy as a whole. Measures of a prohibition and authorization are reflected in the relevant legislative acts.

One of the ways the state directly affects the investment activities of commercial banks is participation in the capital of financial institutions through the mechanisms of corporatization and lending to banks. World experience shows that the preservation of a significant share of the state in the banking system of such countries as Germany, South Korea, Japan, and China made it possible not only to ensure increased investment activity, but also to maintain the stability of the banking sector during the crisis [7].

In economic science, the opposite of opinions about the presence of the state in the banking sector remains. In our opinion, the financial participation of the state in the capital of the banking sector is permissible and justified in the following cases:

- lack of domestic private funding sources for banks. So, under pressure from a liquidity shortage in October 2008, the leadership of France, Germany, Great Britain, the United States decided to directly fund financial institutions and increase their capital;

- the short-term nature of bank liabilities in comparison with the needs of the subjects of the economy;

- achieving the multiplicative effect of government investment in the banking sector, which would provoke banks to invest additionally own funds in the economy;

- suspension of investment activities of banks in industries whose development is of paramount importance for the country's economy;

- accumulation of significant reserves of budget funds;

- participation of commercial banks in the implementation of large-scale investment projects for the construction, modernization of production.

In all other cases, public authorities should be focused on using other methods of influencing the investment activity of banks, for example, through the creation and development of the banking business infrastructure.

One of the key problems restraining the quality development of banks' investment activities remains the extremely high risks of investments in the real sector of the economy. There is a shortage of operational, reliable and complete information about the real state of borrowers, about the structure of their property, etc. The situation with control over the targeted use of borrowed bank loans by borrowers is slowly improving.

To some extent, the solution to this problem can be found in the creation of special institutions whose activities contribute to reducing the risks of investing in economic entities. International experience testifies to the positive impact on the activities of banks of cooperation with institutes for insuring banking risks, exchanging data from credit histories of borrowers, repurchasing troubled assets of banks, and institutes for refinancing bank loans. The state, in the person of authorized bodies, initiates the creation of such institutions, forms the necessary legislative base, and in some cases, acts as their founder or co-founder.

The impact of the state on the investment activities of commercial banks is possible through the implementation of separate development programs, when a certain industry or production receives a new development impulse, which is then enhanced through interaction with the banking sector. That is, creating new viable industries, the state, therefore, forms potential borrowers for the banking sector, creates conditions for private investors to work with them.

So, as part of the implementation of the Industrial and Innovative Development Strategy in Kazakhstan, it is planned to create new industries and develop existing ones with the aim of ensuring the country's sustainable development on the basis of diversification and modernization of the economy [8]. State-funded investment projects significantly increase the liquidity of enterprises, as Development Institutions develop the appropriate growth strategy with the client. As a rule, this strategy provides for corporatization of the enterprise, regular external audits, the company's transition to international financial reporting standards, and the introduction of an international production and management quality system. The requirement for corporatization of enterprises provides for increased transparency and liquidity of potential borrowers of commercial banks.

Significant potential of the state's regulatory impact on the investment activity of commercial banks contains measures of indirect impact. The objects in this case are not investment entities, but investment recipients, that is, those business entities whose activities contribute to the achievement of the country's socioeconomic development goals.

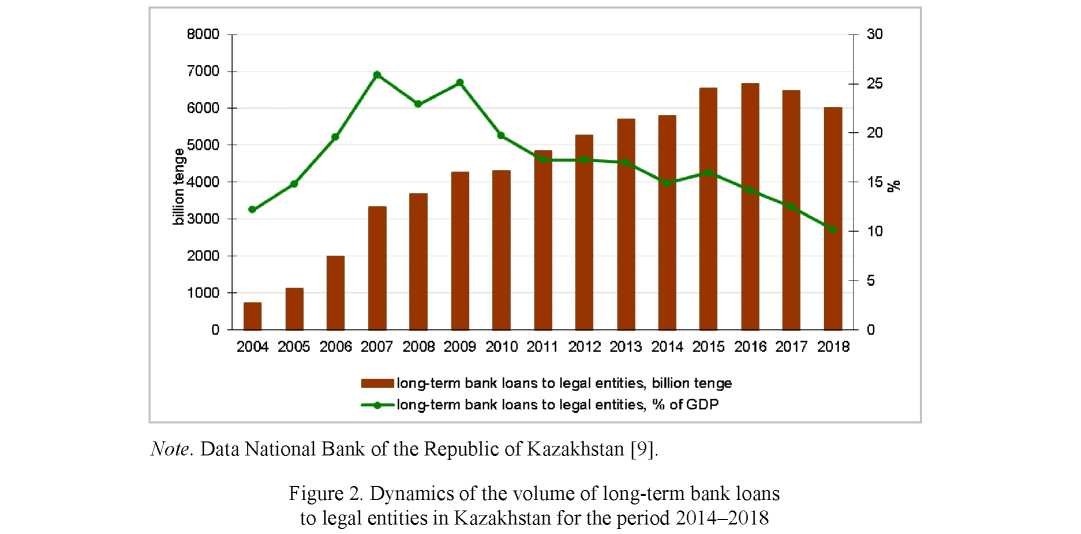

Figure 2 shows the dynamics of the volume of long-term bank loans to legal entities in Kazakhstan for the period 2014-2018.

In this work we have attempted to analyze the effect of the volume of long-term bank credit to legal entities on the gross domestic product of the Republic of Kazakhstan. To do this, we construct the equation of simple linear regression.

The analysis of the obtained regression coefficients shows that:

- - with an increase in the base rate of the National Bank of the Republic of Kazakhstan by 1 %, the volume of long-term bank credit to legal entities will decrease by 686,941 billion tenge;

- - with an increase in the minimum reserve requirements by 1 %, the volume of long-term bank credit to legal entities will decrease by 2391,046 billion tenge.

In order to stimulate and maintain the investment orientation of the banking system, the government needs to ensure the profitability of long-term banking operations. The following government measures can serve to achieve this goal:

- continue to implement monetary policy aimed at stimulating economic growth by lowering the refinancing rate;

- profits from long-term operations of banks partially or fully exempt from taxation;

- provide state guarantees for long-term loans (depending on the degree of priority of the facility being credited);

- provide banks with preferential long-term loans exceeding the state-determined percentage in the bank's portfolio with a preferential refinancing regime with the NBK;

- subsidization by the state of interest on long-term loans granted to finance priority investment projects;

- in order to reduce the risk of long-term operations of banks, introduce joint shared financing of priority investment projects, etc.

The centralized government measures listed above, which ensure the profitability of long-term operations of banks, will increase the interest of commercial banks in long-term lending to business entities and the investment focus of the banking system as a whole.

References

- Decision on the base rate of the National Bank of Kazakhstan. nationalbank.kz. Retrieved from www.nationalbank.kz

- Resolution of the Board of the National Bank of the Republic of Kazakhstan of March 20, 2015 № 38 «On approval of the rules on minimum reserve requirements, including the structure of obligations of banks accepted for calculation, the conditions of performance of the minimum reserve requirements, reservation order». nationalbank.kz. Retrieved from www.nationalbank.kz

- The main directions of monetary policy of the National Bank of the Republic of Kazakhstan for 2019. nationalbank.kz. Retrieved from http://www.nationalbank.kz/

- Concept of the development of financial sector of the Republic of Kazakhstan till 2030, approved by the decision of the Government of the RoK of 27.08.2014. № 954.

- Rudko-Silivanov, V.V., & Zubrilova, N.V. (2013). Formation and development of the banking system of Japan. Money and credit, 2, 31-41.

- Nozdryev, N.S. (2012). Structural crisis of the financial sector of the economy of Japan. The world economy and international relations, No. 1, 54-58.

- Gavrilova, N.M. (2014). Modern experience of innovative development in Germany and possibility of its use in Russia. Proceedings of Financial University, No. 6, 13-20.

- State Program of Industrial and Innovative Development of the Republic of Kazakhstan for 2015-2019, approved by the Decree of the President of the RoK of 01.08.2014. № 874.

- Statistical bulletins of the National Bank of the Republic of Kazakhstan. nationalbank.kz. Retrieved from http://www.nationalbank.kz/cont/Binder12.pdf