Abstract

Object: The purpose of the research work is to justify the application of a model that allows assessing the probability of a borrower's default and to propose including in the work plan and internal audit program an assessment of the probability of a borrower's default to reduce credit risk.

Methods: The article uses quantitative data, statistical model (Logit model).

Findings: As a result, during the audit of the banks' debt portfolio, the Logit model was used to assess the probability of a borrower's default. The ROC curve of this Logit model allows you to predict the default situation of the borrower for risk management purposes. Therefore, it is proposed to include an assessment of the probability of default of the borrower based on the model in the work plan and internal audit program. In conclusion, a risk-based internal audit system will help ensure the financial stability.

Conclusions: In conclusion, a risk-based internal audit system will help ensure the financial stability. Since we evaluated the debt portfolio and found that the Logit model, which was used to predict the probability of default of borrowers, can prevent risks. This is evidenced by the ROC curve of the Logit model for predicting the probability of default.

Introduction

Currently, measures that can alleviate the consequences of external impact on the country's economy are being actively searched. Monetary policy plays a big role here. It is significant to keep in mind that debt allows supporting continuity of industrial processes in the conditions of sharp fluctuations in cash flows, a decline in productivity of organizations at certain stages of the economic cycle. Phantom debts are debts that cannot be recovered by the Bank due to the poor financial condition of the borrowers. Further reduction in the volume of credit investments in the economy can cause irreparable harm to economic entities.

Restricting credit support for organizations with large and predictable sustainable credit loans can lead to disruption and aggravate the situation in the economy. In our opinion, one of the solutions to credit issues in the context of increasing credit risks is to improve the quality of credit risk management in banks. First of all, it is necessary to take into account the financial condition of the borrower, its creditworthiness, and the specifics of the financial sector (Lambekova, Syzdykova, Kuzgibekova, Kalymbetov, Amirbekuly, 2018). It also referred to the need to improve the evaluation system, including the development of a mechanism for assessing the probability of default To ensure the implementation of the new credit policy related to the adoption of IFRS 9 “Financial instruments”, it is necessary to strengthen the role of internal audit. In addition, it is necessary to increase its importance as an element of the corporate governance and risk management system. The Bank expects the formation of a new methodology for assessing credit risks, so the internal audit service is assigned certain tasks. Let's look at how to include these services in the credit risk audit program. Decisions of management bodies within the framework of lending in the Bank can be reflected in the Bank's internal regulatory documents. In particular, credit policies, restrictive policies, and risk management policies (Yang 2018).

Hypothesis. Using the Logit model for assessing the probability of default of the borrower, aimed at identifying credit risk, their reduction will allow you to assess the probability of default.

Literature Review

During the audit, the internal auditor should pay attention to the Bank's approved system of credit risk indicators and the relevance and regularity of reviewing the target values of indicators (Canakoglu, Muter I, Adanur O, 2018).

The function of every single aspect adds up to make effective corporate management of the Bank. The document “Basic effective principles of Bank supervision” issued by the Basel Committee assumes that this management is based on risk (Basel Committee on Banking Supervision, 2019).

The study aims not only to assess losses that can be investigated by determining credit risk factors in the research process, but also to prevent negative impacts, both external and internal aspects, and to develop an action plan to preserve the financial stability of the banking sector.

The study is not required only for assessing losses that can be investigated by determining credit risk factors in the research process. It is also necessary to prevent negative impacts, both external and internal, and to develop an action plan to preserve the financial stability of the banking sector. As a comprehensive indicator covering credit losses due to market and credit risks, many kinds of literature have the VaR-Value-at-Risk indicator, which was discovered in the work of M. Sorzha.

In addition, M. Sorzha noted the feasibility of using an integrated approach with financial systems that have active trade-in credit assets (for example, corporate bonds).

Moreover, the “mark-to-market” principle is applied, which provides for the revaluation of assets following current market prices. However, the financial systems of many transition economies are characterized by insufficient development of the financial asset market and absence of price fluctuations. A selective approach with the choice of a specific credit risk indicator is acceptable for assessing the stability of banks with a low level of correlation between market and credit risks. Additionally, due to the ease of implementation, the low level of need for statistical data and computational loads, the partial approach is widely considered by researchers.

The partial analysis is conducted under econometric models to assess the relationship between financial stability indicators, macro indicators, and specific indicators of financial institutions. Besides, the estimation is performed using models for time series and panel data. Banks are given the right to form stricter criteria for determining default and the significance of credit obligations. This allows the Bank to treat certain categories of borrowers more differentially. In recent crisis years, research has focused on ways, methods, and models for assessing credit risks. M. Sorzha noted that the advantage of panel data is the ability to study the impact of the qualitative characteristics of countries or individual banks on the quality of loans (Vaquero, Diaz, Ramirez,2019).

One of the works using panel data is the work of j. Pasolini. The author studies the impact of macroeconomic indicators on problem loans in Scandinavian and other European countries using data from 1980 to 2002 (Pesola, 2011).

As a result, the main source of credit losses for banks in these countries was high customer debt income volatility, and the real interest rate, which is measured as the ratio of debts to GDP.

S. Pestova and T. Solntseva conducted a study of problem debts using annual data from 1997–2009 for 38 countries (Yavuz, 2002). In this regard, the authors identified the factors of formation of non-refundable problem debt. This has a negative impact on the same direction of the business and credit cycles, the weakening of the nominal exchange rate and the reduction of the real interest rate on credit risks.

In General, the internal audit service is the main risk management tool in all operating organizations [Sourour, 2019]. In addition to assessing credit risks, the panel data method is used in commercial Bank research.

Methods

Banks are given the right to form stricter criteria for determining default and the significance of credit obligations. This will allow the Bank to treat certain categories of borrowers more differentially. During the last 2008 crisis, research focused on methods, approaches, and models for assessing credit risks. At the same time, schemes based on probability estimation were used only in a limited way, since the regulator did not perceive such models (Ozten S., Kargin S., 2012).

Currently, it is necessary to improve the accuracy, efficiency and reliability of credit risk assessment in relation to various groups of borrowers and credit requirements. This requires further processing of the models. To explore the possibility of assessing the probability of a borrower's default based on the published financial statements of organizations we have created an appropriate model that has acceptable estimated capabilities. Indicators for assessing the financial condition of the borrower based on their understanding of their significance were selected (Lambekova, Nurgalieva, 2017).

The organization information for the two groups is chosen randomly according to publicly available information. Data on the financial position were obtained from the financial statements of organizations in the KASE database (KASE, 2018).

Information is received for the period from 2016 to 2018. This forecast allows predicting the probability of default of the borrower for one or two years. The regression analysis was performed in the statistical econometric package R.

Data based on the model formed in accordance with Basel recommendations must be reliable. In this case, the reliability is confirmed, first of all, by the mandatory audit report and audit of the tax authorities. The majority of organizations in industrial spheres have service of life is more than ten years.

The next stage of the study is data analysis. To study the relationship between indicators, a correlation matrix was created.

According to the hypothesis of the research work, financial stability affects the assessment of the probability of default of borrowers of the estimated coefficients.

The objective of the research work is to determine the impact of financial stability assessment coefficients on the assessment of the probability of default.

According to the relevance of the study, banks are not based on the fact that the expected credit costs were not incurred, but on its prevention.

Now let's move on to the research methodology. Procedures that ensure that research goals are considered. In particular:

- study design;

- data collection tools;

- data analysis and data collection procedures.

Study design. The model for estimating the probability of a borrower's default should be based on statistical data collected by the bank over a number of years or over several economic cycles. In most cases, this information is unavailable to external users during the course of the study. Therefore, the data was obtained from the Kazakhstan stock exchange (Naceur,2018).

Data collection. In the course of the study, data was collected from calculating coefficients of the financial statements of the list of companies in Kazakhstan stock exchange.

Data analysis, results, and discussion. To confirm hypothesis above, a Logit model was created in the Logit model R statistical package program.

Thus, the Logit model is an econometric model that is not used in simple regression analysis methods. Unlike the other models, it can only accept a limited number of dependent variable values, such as 0 or 1.

To put it another way, the most common model for assessing the probability of bankruptcy can be overviewed. These models allow you to determine an accurate assessment of possible bankruptcy risks. The model for estimating the probability of bankruptcy is the logistic inverse equation. This is why it is called the logistic backflow model (L-M) L-M (Logit model).

According to A. Gruzdev, the statistical package program R is widely used as statistical software for data analysis and is practically a standard for statistical programs (Gruzdev, 2018).

The binary variable probability of default of the borrower's PD is obtained, which takes one of two possible values for building the model as a dependent variable:

-PD = 0 if any borrower organization has a good financial position at a certain stage;

-PD = 1 if any borrower organization is in default at a certain stage.

To build a model of the probability of a creditor's default, 33 debt recipients in various industries were selected and divided into two groups. Of these, 25 are good and 8 are in case of default. Enterprise data for the two groups is selected randomly according to publicly available information. Data on the financial position is obtained from the financial statements from the KASE database. Information obtained in the period from 2016 to 2018. This forecast allows you to predict the probability of default of the borrower for one or two years.

The regression analysis was carried out in the statistical econometric package R. We selected a number of parameters that determine the level of financial stability of borrowers.

Financial stability is evaluated by indicators of liquidity, profitability, business activity presented in Table 1.

Table 1. Indicators selected for building a default assessment model

|

Indicator |

Name |

Economic content |

|

K pokr |

Current ratio |

ability to repay short term liabilities at the expense of current assets |

|

K avt |

Autonomy coefficient/Equity ratio |

independence from external sources of funding |

|

K ob cc |

Equity to non-current assets ratio |

availability of the company's own working capital |

|

K dtoe |

Debt-to-equity ratio |

describes the ratio of borrowed funds to equity |

|

K ap oc |

Equity capitalization |

describes the share of fixed assets financed from equity sources |

|

K_obor_ta |

Current asset turnover ratio |

reflects the amount of turnover of the company's current assets for the current period |

|

K ct plat o |

The degree of solvency |

characterizes the overall solvency of the enterprise |

|

Note — compiled by the author based on the literature (Aleskerov F. T., Andrievskaja I.K., Penikas G.I., Solodkov V.M.) |

||

Today, mathematical assessment of Bank risks is widely used in foreign countries. Such assessments not only contribute to the prevention of risks at the time of their occurrence, but also make predictions. For example, F.T. Aleskerov presented mathematical models of Basel II risk assessment in Russian banks (Krylov, 2016).

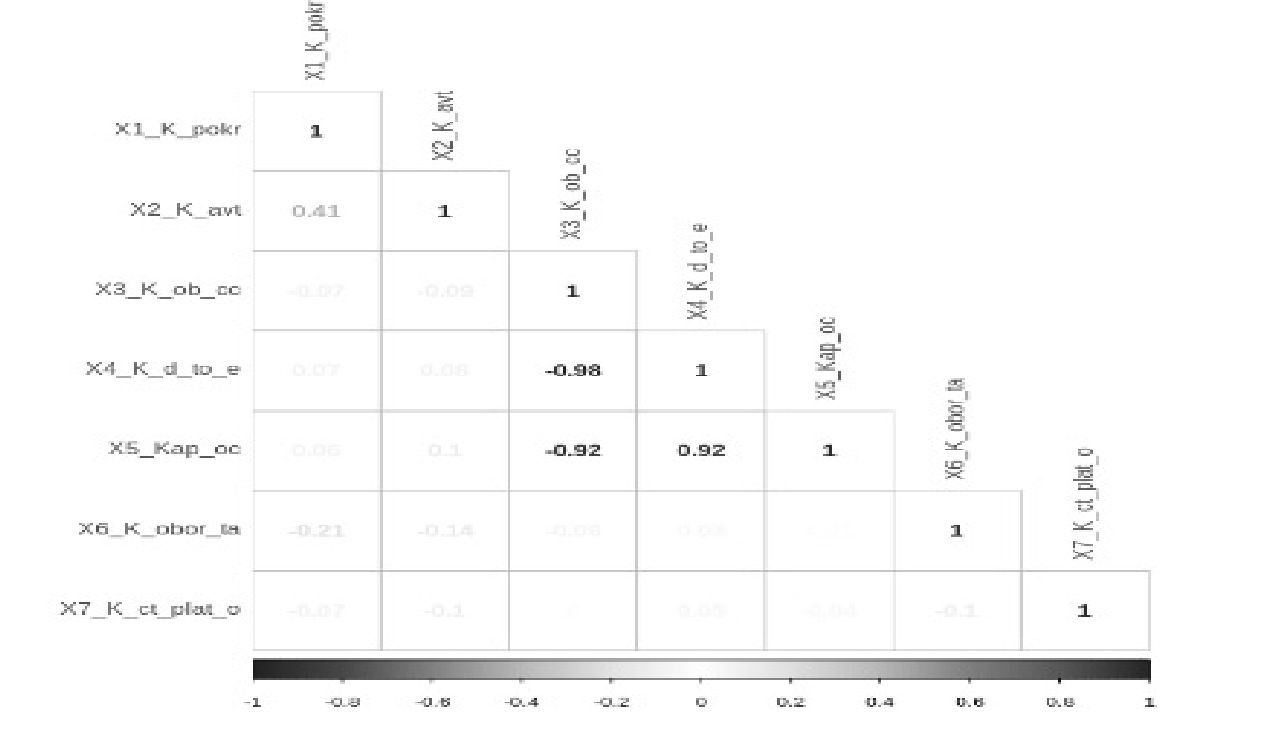

The next stage of the study is data analysis. At the same time, organizations belong to industrial sectors, the service life of the majority is more than ten years. All necessary data is provided in Appendix D. to create a model, a set of codes is specified in Appendix E. To study the relationship between indicators, a correlation matrix was created (Figure 1).

Figure 1. correlation between the factors

Note — complied by the author in the statistical batch program R on the basis of warning-calculated data

As can be seen from the correlation picture, factors X4 and X5 are multicollinear. So we remove these factors from the model. The concept of multicollinearity is fulfilled under the condition that a linear relationship between the explained variable leads to a non-confidence regression. Correlation between multicollinear factors leads to unreliable, unstable, and meaningless price dependence of multicollinear parameters. It cannot make a correct decision about parameters.

Data obtained in accordance with Basel recommendations must be reliable. In this case, the reliability is confirmed, first of all, by a mandatory audit report and an audit of the tax authorities. If all the conditions are fulfilled, the sample variances of variables with control digits are large, and the variances of random variables are small, then a good estimate can be obtained as a result.

Consideration of this issue affects the effective evaluation of regression. If the obvious indicator of two or more independent variables is a time trend, then they are in close contact and this leads to multicollinearity.

To understand the effect of the mechanism on parameters, consider the following statement. There is a linear dependence between the first and second factors (Rahmetova, 2016).

There are several ways to prevent multicollinearity:

– Removal method.

– Regression step.

In our case, we use the first method. Correlation connection without multicollinear factors is shown below (Figure 2)

As can be seen from the figure, for risk management purposes, we observe that the coefficient of autonomy in case of default of the borrower organization is high. Other factors also have an impact, but they are weak.

Results

As a result of the above-mentioned analyses, during the audit of the banks' loan portfolio, the Logit model was used to assess the probability of a borrower's default. Now let's build a Logit model based on this correlation (Table 2)

|

Deviance Residuals: |

||||

|

Min |

1Q |

Median |

3Q |

Max |

|

-1.76205 |

-0.52145 |

-0.23519 |

-0.02412 |

2.38113 |

|

Coefficients: |

||||

|

Estimate |

Std |

Error z |

value Pr(>∣z∣) |

|

|

(Intercept) |

1.12290 |

1.06782 |

1.052 |

0.2930 |

|

X1K pokr |

-0.47052 |

0.47701 |

-0.986 |

0.3239 |

|

X2 K avt |

4.40686 |

1.41149 |

3.122 |

0.0018 ** |

|

X5 K ap oc а |

0.60240 |

0.34719 |

1.735 |

0.0827. |

|

X6 K obor ta |

-0.56717 |

0.31491 |

-1.801 |

0.0717. |

|

X7 K ct plat o |

-0.09600 |

0.05556 |

-1.728 |

0.0840. |

|

Signif. codes: 0 ‘***' 0.001 ‘**' 0.01 ‘*' 0.05 ‘.' 0.1.,1. ‘ ' |

||||

|

Note — complied by the author in the statistical batch program R on the basis of warning-calculated data |

||||

Table 2. Criteria for evaluating the significance of the model

As it is illustrated in the table, variables of X2_K_avt show the most statistical significance at defining default of organization. Statistical significance of variables X5_Kap_oc, X6_K_obor_ta, and X7_K_ct_plat_o has a probability of 10 % which is explained by possibility of randomness of data. Understanding the causes of default is important, but it is also important to anticipate it based on available data.

In other words, to what extent can the Logit model assume a default situation for the borrower? To answer this question, we assume the probability of default of debt-receiving organizations based on data that we have not previously seen in the model (based on 4 organizations).

Then the forecast results will be compared with the results of the test model. However, the Logit model does not give a solution as 0 (no default) or 1 (default); it gives probability of organization to be in default

We must decide the type of probability limit to be used as a boundary between 0 and 1. Selecting an upper limit reduces the number of false positives (the model assumes that the organization is defaulting, and the organization is not defaulting). It also reduces the number of real positive results (the model assumes the case of default for organizations that have been defaulted).

In each logit model, the probability of default is calculated using the General formula of the logistics function:

Lowering the limit works in the opposite direction, increasing the number of false starts as well as the real positive number. To determine the accuracy of the forecast, it is important to set an average limit value. It is defined by the ROC curve. In other words, through a curve. In social science, the ROC curve is used to express an opinion about the quality of probability models.

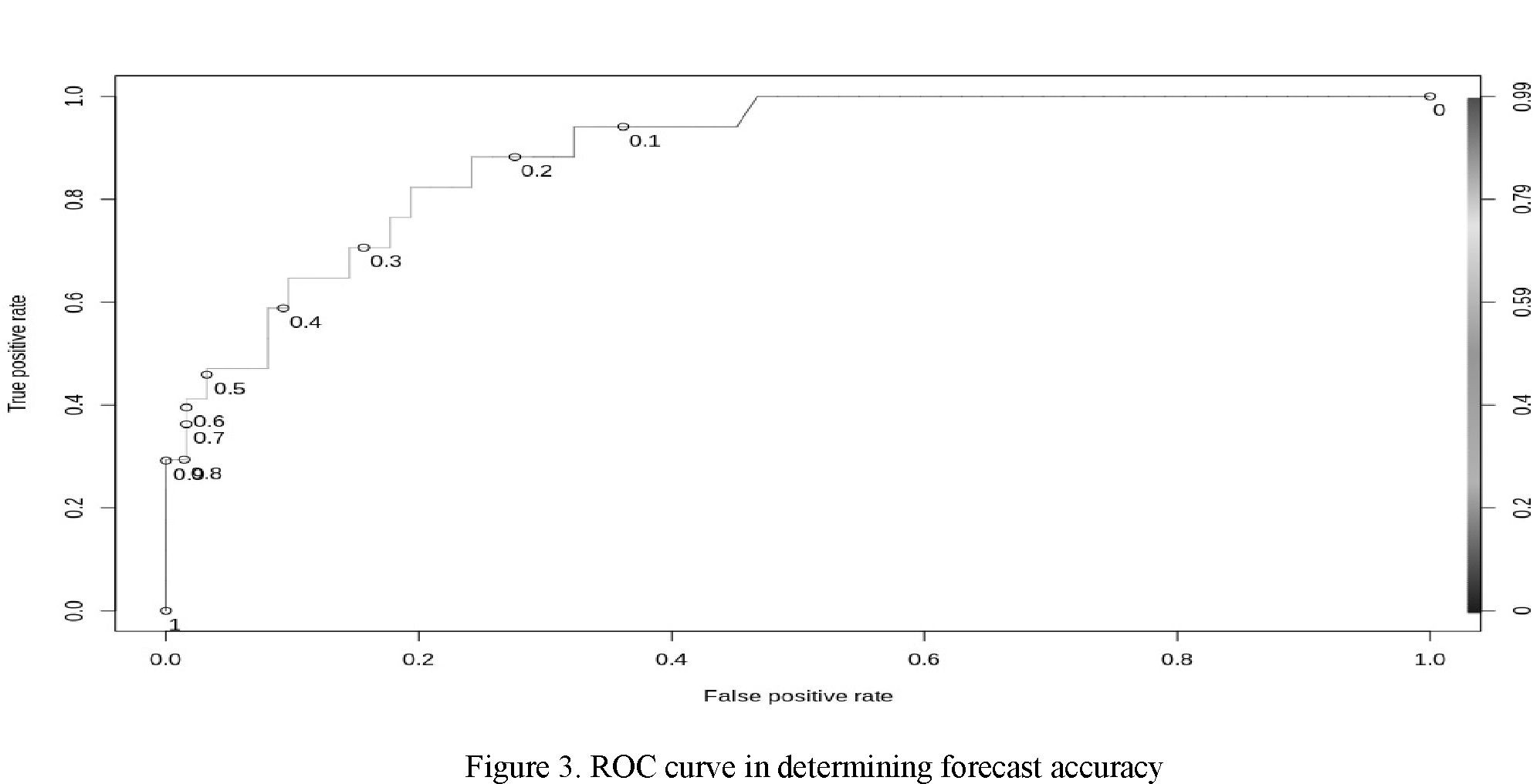

We will test based on the other four companies as a test to determine the accuracy of the model. The indicators of the coefficients calculated for testing are shown in Appendix J. In Addition, the curves were used in product quality management and credit scoring. This is shown in the curve line on the figure (Figure 3).

Note — complied by the author in the statistical batch program R on the basis of warning-calculated data

The Logit model curve above shows that the borrower is well qualified to determine the default status for risk management purposes. It is in the range of 0.3, it has reached almost 70 % of the real positive indicators. In the table below, we present a matching matrix that allows calculating the accuracy of the model (table 3)

|

Indicators |

Forecast = 0 |

Forecast = 1 |

|

Fact = 0 |

3 |

3 |

|

Fact = 1 |

3 |

2 |

|

Note — complied by the author based on calculated data |

||

Table 3. A matching matrix that allows you to calculate the accuracy of the model

As can be seen from the results in the table, this fact coincides with the forecast that the financial condition of the borrower company is satisfactory. The case of default of the borrower does not correspond with unit of fact 1. This means that the specific financial position of the borrower company, expected in case of default, is stable. Overall, the forecast accuracy is 83 %. This means that the results of calculating the probability of default show that the proposed model can be used in practice.

Discussions

In our opinion, today the application of IFRS 9 “Financial instruments” in banks has set new challenges for internal auditors. For example, according to the implemented standard, lending or effective and high-quality methodological advice to risk management departments on risk prevention, etc.

It is very important to consider the credit risks of borrowers based on the Bank's internal ratings in accordance with the model of assessing the probability of bankruptcy. This, of course, raises the internal auditor to a new, high-quality level of credit risk management in banks.

Using models to assess the probability of a borrower's default and the amount of costs associated with a default allows banks to lend only to trusted clients, take acceptable risks, and create sufficient reserves to compensate for potential losses.

Conclusions

The role of internal audit was defined to verify the correctness of credit policy implementation in connection with the implementation of IFRS 9 “Financial instruments”. At the same time, corporate governance has grown in importance as a key tool of the risk management system. Currently, it is expected that banks will be given effective advice on developing acceptable and effective methods for assessing this credit risk with the internal audit system. The Bank may provide various procedures for assessing the credit risk of the application and analyzing the creditworthiness of the borrower. Assessment of the probability of a creditor's default in banks is not yet sufficiently conducted. In this regard, we used the Logit model, aimed at preventing the expected damage in order to reduce or prevent credit risk on the debt portfolio of banks. The model is based on the financial indicators of 33 borrower organizations. And the ROC curve of the Logit model allowed us to determine the default state of the borrower company. The model has been tested, so it can be offered in banks in order to reduce credit risk.

In conclusion, a risk-based internal audit system will help ensure the financial stability of the second-tier banks, because the debt portfolio was evaluated and found that the Logit model, which was used to predict the probability of default of borrowers, is able to prevent risks. This is evidenced by the ROC curve of the Logit model for predicting the probability of default. This model, developed by internal auditors to prevent risks, is taken into account in the internal audit process.

Summing up, internal auditors contribute to the formation of a highly effective internal audit system to ensure the bank's financial stability and the way of meeting modern requirements.

References

- Yang, B.H. (2017). Point-in-time PD term structure models for multi-period scenario loss projection: methodologies and implementations for IFRS 9 ECL and CCAR stress testing. Journal of Risk Model Validation, 11(3), 76–97.

- Lambekova, A.N., Syzdykova, E., Kuzgibekova, S., Kalymbetov, U., Amirbekuly, Y. (2018). The Increasing Role of Internal Audit in the Banking System in the Context of Expanding the Range of Financial Services. Journal of Applied Economic Sciences. — Romania: «ASERS», 6(60), 1758–1766.

- Lambekova, A.N., Nurgalieva, A.M. (2017). «Halyq Bank» Akcionerlik qogamynyn qarjylyq turaqtylygyn taldau ishki audit juiesinin tiimdiligin arttyru quraly retinde [Analysis of financial stability of Halyk Bank joint-stock company as a tool for improving the effectiveness of the internal audit system]. Vestnik Karagandinskogo Universiteta. Serija Ekonomika — Bulletin of the Karaganda University. Economy Series, 2(86), 236–242.

- Canakoglu, E., Muter I., Adanur, O. (2018). Audit Scheduling in Banking Sector. Operations Research Proceedings, Springer, 5, 499–505. https://doi.org/10.1007/978-3-319-55702-1_66

- Basel Committee on Banking Supervision. Core Principles for Effective Banking Supervision September. www.bis.org

- Ben Naceur, Katherin Marton, Caroline Roulet (2018). Basel III and bank-lending, Journal of Financial Stability, 39, 1– 27.

- Pesola, J. (2001). The Role of Macroeconomic Shocks in Banking Crises. Bank of Finland Discussion papers. Retrieved from www.core.ac.uk.

- Yavuz, S.T. (2002). Components of Internal Control Function — Internal Control Center Is a Different Mechanism From Internal Audit (Internal Audit). Bankers Magazine, 42, 39–56.

- Sourour Hazami-Ammar (2019). Internal auditors' perceptions of the function's ability to investigate fraud. Journal of Applied Accounting Research. - Emerald Publishing Limited, 20(2), 134–153.

- Ozten, S., Kargin, S. (2012). Credit Control and Accounting Process Within the Scope of Internal Control Activities in Banking. Afyon Kocatepe University Publishing, 14(2), 119–136.

- KASE database (2018). Retrieved from www.kase.kz.

- Gruzdev, A.V. (2018). Prognoznoe modelirovanie v IBM SPSS Statistics, R, Python: metod derevev reshenιι ı sluchaιnyι les[Predictive modeling in IBM SPSS Statistics, R, and Python: decision tree method and random forest]. Moscow: DMK Press.

- Aleskerov, F.T., Andrievskaia, I.K., Penikas, G.I., Solodkov, V.M. (2013). Analiz matematicheskih modelei Bazel II [Analysis of mathematical models Basel II]. (Izd. 2-e, ispr.), Moscow: Fizmatlit.

- Krylov, S.I. (2016). Finansovyi analiz [Financial analysis]. Ekaterinburg: Ural. Universitet.

- Rahmetova, R.O. (2016). Ekonometrika [Econometrics]. Almaty: Ekonomika.