Abstract

Object: The scientific paper focuses on issues of inefficient intersectoral interaction through the prism of an institutional methodological approach. In particular, the authors aim to investigate and identify problems that limit the harmonious and mutually beneficial interaction of subjects of the financial and credit and innovation sectors in the modern conditions of the Kazakhstani economy.

Methods: Based on the use of comparative, statistical and expert analysis, the authors conclude that it is necessary to level the existing problem nodes by improving the existing institutional environment in terms of developing financial, real and regulatory innovations, further developing the institutional infrastructure, and an optimal combination of formal and informal institutions.

Findings: It is recommended to change the current paradigm of regulatory institutions implementation in the direction of preventive and stimulating regulation of subjects in both sectors at the same time in order to reduce the existing asymmetry.

Conclusions: The article considers the sources of financial and credit support for the innovation sector, identifies problems in financing investment and innovation projects in Kazakhstan based on a comprehensive analysis of the costs of research and development, bank lending, foreign investment, investment potential of the pension and insurance sectors, and development institutions.

Introduction

In modern conditions of global changes, market fluctuations, influence of integration processes on economic development, the relevance of sustainable development of the national economy on the basis of a deeper, diversified and active use of innovations in real sector of economy is increasing. For Kazakhstan, as a country with emerging markets, these issues are especially important in frames of consistently low economic growth rates and excessive dependence of the economy's state on the income of the extractive sector. Thus, in accordance with the priorities of the President's Messages “Kazakhstan-2050” and “the Third modernization of Kazakhstan: global competitiveness”, the goals and objectives in the field of innovative development of Kazakhstan, aimed at overcoming existing structural imbalances, are outlined. However, the relevance of this issue is evidenced by the fact that, against the background of the long-term implementation of the state program of industrial and innovative development, Kazakhstan's rating position in the global innovation index has decreased from 74 to 79 place, and in the composite index of achieved results, Kazakhstan ranks only 92 out of possible 100.

We believe that state efforts alone are not enough to activate the subjects of the innovation sector, since best international practice indicates that the greatest success in the field of innovation performance is achieved by those countries that have managed to combine the efforts of the state and private entities primarily the financial and credit sector effectively, leaving the state authorities only the right of indirect preventive participation in regulation aimed at supporting and stimulating the latter in a market model of the economy (Rakhmetova et al., 2019, 115).

At the same time, the multidirectional vector of goals and interests that guide the subjects of the financial and credit and innovation sectors of the economy, entering into the process of interaction, despite the asymmetric nature, can be adjusted in one direction through the institutions that form the basis of the mechanism of effective intersectoral interaction.

In this regard, the purpose of this study is, based on an analysis of the theoretical and methodological foundations of the interaction of entities of the financial and innovation sectors of the economy, to identify existing restrictive barriers, and to offer appropriate recommendations for their elimination, primarily by improving the institutional infrastructure that ensures efficiency intersectoral interaction at the micro, meso and macro levels of the economy.

Institutions, according to the institutional-evolutionary concept, form the basis of any society, contributing to its sustainable and effective development. In particular, the founder of this scientific theory, D. North (North, 1997), noted in his works that “the way the economy functions is determined by a set of rules, informal laws and mechanisms that fix them, while if laws and rules can be changed overnight, then informal norms are formed and changed over a long time”.

Appealing to the basics of institutional-evolutionary concepts in the context of this study is not accidental, because the complex of formal and informal institutions, in our opinion, is able not only to maintain the stability and resilience of complex systemic process of interaction of subjects of the financial and innovative sectors of the economy, but also allows to adjust the trajectory of its development in the right direction against the background of influence of many various factors.

The consequences of the so-called great recession (the financial crisis of 2007–2008) revealed the most pronounced dependence of intersectoral interaction between the financial and real (including innovative) sectors of the economy on the institutional infrastructure. So, the rapid development of the market of fictitious capital and derivatives market led to the fact that they began to use real assets that eventually led to the establishment of their reserves gradually began to define the fluctuations and manipulation of prices of these assets rather than the real needs of actors in real and innovation sector of the economy. In addition, due to increasing globalization, there was an increase in financial technologies, the development of international financial centers and offshore companies, whose activities generated super-profits outside the sphere of industrial production. The expansion of international financial institutions has led to the dependence of national economic systems on unified norms that do not always take into account the national true interests of national economies.

In our view, ongoing and periodically exacerbated contradictions in the relations of subjects of financial- credit and real (including innovative) sectors of the economy taking its roots in the conflict between the existing formal institutions, regulation and sustainable informal institutions, which are used to guide economic agents, which significantly reduces the efficiency of their interactions at both the micro and macro economy.

In particular, a preliminary analysis of the problems that limit the high efficiency of interaction between financial and credit organizations and enterprises of the innovative sector in domestic practice has shown that they can be grouped into so-called barriers or problem nodes, which are tied to many other smaller problems related to each other by cause and effect: 1) the first group of problems is associated with high risks (financial and industry), which do not allow financial and credit organizations to interact more actively with innovative enterprises; 2) the second group of problems is related to the adequacy of the conditions for providing the innovation process with financial resources; 3) the third group of problems comes from the imperfection of the regulatory practice, its single-vector nature and inflexibility.

Literature Review

Understanding that the role of the innovation sector in the development of a high-tech economy is currently increasing is a key to the stability and well-being of the state. Financial support for the effective functioning of the innovation sector is an object of active research in connection with the need to improve it. Various aspects of the problem were considered in the works of domestic and foreign scientists, which will be the scientific and methodological basis for developing the topic and achieving the research goal.

The impact of the degree of development of stock and credit markets on the high-tech sector in advanced economies is investigated in the work of Brown Jr., Martinsson, G., and Petersen B.C. (Brown et al., 2017). In turn, the work of Xiao S., Zhao S. (Xiao – Zhao, 2012) analyze how financial development affects the innovative activities of companies, including the functioning of the stock market and the banking sector in countries with different levels of state ownership of banks. Problems of availability of financial and credit resources for innovative firms in the conditions of insufficiently developed financial sector of countries with transition economies are investigated in scientific works of Botric V., Bozic L. (Botric – Bozic, 2017). The scientific paper of Hudson J., Orviska M. (Hudson – Orviska, 2014) examines the role of the EU financial sector in providing firms with financial and credit resources to promote potentially successful R&D on the world market. The study of the effectiveness of EU programs for financial support of innovative small and medium-sized businesses, availability of financial resources and satisfaction with cooperation with public institutions is presented in the work of Viskovic J., Udovicic M. (Viskovic – Udovicic, 2017). A detailed study of the possibilities of providing financial support to the innovative sector through the use of various government tools was conducted in the works of Kryskova L., Strzelczyk W. (Kryskova – Strzelczyk,2013), Nikolov M. (Nicolov, 2013). Problems of sustainability management in companies based on the introduction of business innovations are studied by Fogarassy C., Horvath B., Magda R. (Fogarassy et al., 2017).

According to L.I. Yuzvovich (Yuzvovich, 2012), the financial and credit mechanism can be considered from the position of attracting real investments as a “tool for influencing the process of financing real investments within the framework of a single investment system”. This mechanism makes it possible for financial and investment institutions to have a targeted impact on investment relations and creates the necessary prerequisites for redistributing financial flows across various segments of the financial market.

In the economic literature, there is a need for a more in-depth study of the problems of evaluating the effectiveness of the system of financial and credit support for the innovative sector.

Methods

Theoretical and methodological base of research were represented by the works of Kazakhstani and foreign scientists-economists in the field of financial-credit support of innovative sector, normative-legal acts of the Republic of Kazakhstan in the sphere of development of innovation and financial system, the State program of industrial-innovative development of Kazakhstan for 2015–2019. In the process of research, general scientific methods were used: the method of comparative and dynamic analysis, system-structural and cause-and- effect analysis, SWOT analysis of the system of state financial and credit support for innovation, as well as analysis and forecasting based on a multi-factor correlation and regression model.

The study was made with the help of Committee on statistics of Ministry of national economics of the Republic of Kazakhstan, the National Bank of Kazakhstan for the years 2011–2019, analytical reports and studies, annual reports of development institutions and second-tier banks in the Republic of Kazakhstan.

A multi-factor correlation and regression model was developed to determine the degree of influence of various sources of financing for the innovation sector on the volume of production of Kazakhstan's manufacturing industry. Program Stata 13 was used as a modeling tool, and a graphical illustration of dependencies was performed in Excel. In the framework of modeling the selected indicators of dependence (the impact of financial assets on the growth of the innovation sector), an attempt was made to determine the degree of the greatest impact of various sources of innovation financing on the growth of the innovation sector. The sources of statistical data for this group of dependencies were statistical indicators from the database of the World Bank and the National Bank of the Republic of Kazakhstan for the period from 1995 to 2018.

Results

The risk node barrier in the context of interaction between financial and credit organizations and enterprises in the innovation sector is of paramount importance and includes a number of interrelated problems such as: asymmetry of goals of sector entities, asymmetry of information exchanged between them, regulatory requirements in terms of risk assessment, internal risk management systems, low quality of financial assets, high cost of financial services, state and potential of subjects and industries, specifics of their activities, etc. The risk nature of innovation undoubtedly affects not only the entire process of interaction between the financial and credit and innovation processes, but also the results of such interaction. Today, high financial and industry risks constrain all independence and initiative of financial and credit organizations in relation to the subjects of the innovative sector.

The next key barrier that restricts the active interaction of the financial and credit and innovation sectors of the economy is the resource sector. Total growing volatility in financial and commodity markets and the instability of the macroeconomic indicators today reduces the confidence of potential investors long-term resources temporarily available to financial institutions in the country, which leads to more hoarding and transfer of available funds primarily on the real estate market, currency, investments in other real assets and accounts of foreign banks, whose activities have proved reliable for centuries. Unfortunately, all these trends are due to the lack of clear, effective and time-tested mechanisms for saving and investing temporarily available resources. The problem is not even that these resources are not available, on the contrary, the country has serious savings from mining, and there are long-term savings in insurance and pension funds and in the hands of the population and business entities. All this suggest that this nodal barrier is closely related to the first “risk”, because even if resources are available (including when the state sends trillions of funds to the banking sector in order to Finance the needs of the real sector under different programs), these funds are “stuck” in the financial and credit system due to high risks. The relationship between the first two problem nodes is shown by the incommensurability of the duration of the innovation process and the terms within which financial and credit institutions have the right and opportunity to place the attracted resources. As practice shows, the innovative developed countries that occupy the top 5 in the global innovation index have an average innovation cycle duration of 7–10 years (Sweden, Denmark, the Netherlands), while the term of placement on Bank deposits of domestic banks does not exceed 3–5 years. In addition to banks, the financial sector also has insurance and

pension organizations that have longer-term resources on their accounts, but these organizations, following the “letter” of the law and regulatory requirements, are also limited in risky investments. The significance of the resource node barrier is determined by the need to organize an optimal allocation mechanism that can provide sufficient and uninterrupted inter-subject, inter-territorial and inter-industry capital transfer within the country and obtain positive effects at all levels of the national economy.

The third key barrier that constrains the harmonious interaction between the subjects of the financial and credit and innovation sectors of the economy is the costs of the regulatory system. Of course, self-regulation cannot be a problem or a barrier, but the nature, direction and limits of the current regulatory system in relation to subjects of intersectoral interaction. In particular, it is a combination of such problems as: low competitiveness of domestic enterprises, under development of innovative sector entities, regional and sectoral imbalances in development, corruption at all levels, disparity of target indicators and vectors of development of the main directions of the implemented economic policy (monetary, industrial, innovative, antitrust, financial, banking, etc.)

It should be emphasized that this particular node barrier directly affects the previous two. At the same time, the cyclical nature of the development of economic systems dictates a periodic change in the regulatory vector depending on the current economic situation. Depending on the stage of the economic cycle, regulatory measures can either smooth out or exacerbate contradictions in the interaction of financial and credit organizations and enterprises in the innovation sector. So the significance of regulatory issues for the progress and results of intersectoral interaction between subjects of two strategically important sectors of Kazakhstan's economy necessitates adjustments to current regulatory practices from hard-sided restriction measures that target short-term effect towards a balanced and preventive regulation, which are of a stimulating nature and is designed, primarily, long-term multiplier effects.

We believe that such a difficult task in the current conditions of development of the Kazakhstani economy is unsolvable without a proper institutional infrastructure and environment that would support the trajectory of intersectoral interaction in the right direction, not only inter-subject relations, but also general economic development. In other words, the existing institutional infrastructure does not fully cope with its main function, which allows us to conclude that institutional reforms should not be aimed at maintaining individual sectors and their subjects, protecting their interests, but at maintaining mutually beneficial intersectoral interaction in order to achieve cumulative macroeconomic effects.

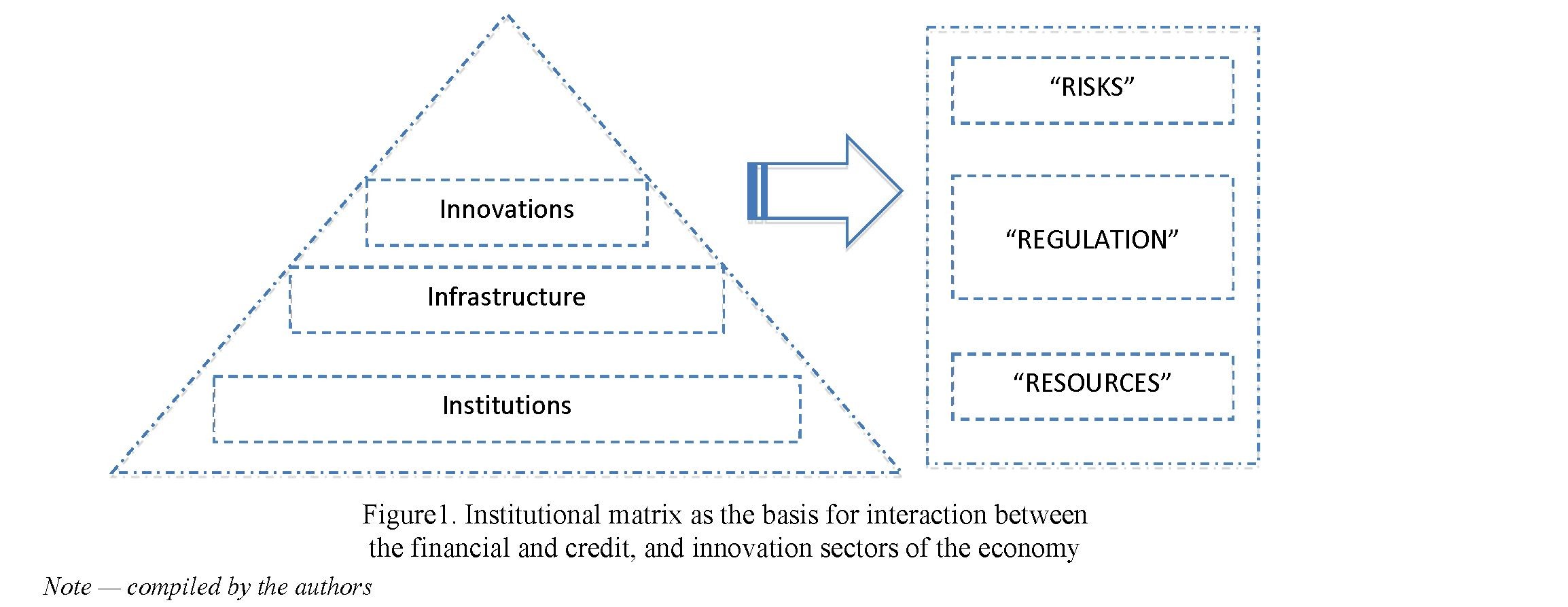

The essence of the institutional framework for interaction between the financial and credit and innovation sectors can be presented in the form of an institutional matrix, which is understood as a three-unit association consisting of a set of elements that are interconnected, representing the key areas of development (Figure 1). For the first time in their works, representatives of the institutional theory of North D. and Polanyi K. mentioned institutional matrices as a system of institutions represented as specific ways of development of a particular society.

The matrix is based on institutions that modern science associates with the possibilities of high-quality sustainable socio-economic growth of the economy. Today, the essence of the definition of “Institute” has not

104

Вестник Карагандинского университета

only the established rules and regulations, but also the appropriate mechanisms that support their strict implementation. In other words, modern interpretations of the concept of “Institute” emphasize the relationship between the effectiveness of institutions and their stability both in the behavior of subjects and in the time period. In this regard, the effectiveness of the process of interaction between the subjects of the financial and credit and innovation sectors of the economy, in our opinion, can be ensured by cultivating stable informal (ethics of behavior of subjects) institutions on the basis of improving and thoughtful use of formal (reflexive — established by law norms and rules of behavior of subjects) regulatory institutions. The practice of such countries as England, the USA, Sweden, Denmark, the Netherlands, which tried to solve this problem at different periods of time, has shown that they succeeded only in combination, enhancing the role and quality of work of state and public institutions, focused on the diversity of opinions of economic agents and slow, progressive formation of a complex of informal institutes that has a huge potential to support the process of inter-sectoral cooperation, which is able to generate positive macroeconomic effects in an unstable economic environment (Gusmanova et al., 2019).

In the field of improving the use of existing formal institutions, it should be noted about the observed asymmetry in the current practice of regulating subjects, or rather about the disproportionality of the regulator's requirements. There are a large number of institutional frameworks for financial and credit sector entities: laws, regulations, limits, reserve requirements, licensing, availability of infrastructure organizations (rating agencies, credit bureaus, etc.), and there are no such regulatory requirements for entities in the real and innovative sectors of the economy. This only increases the asymmetric nature of the interaction between the parties and significantly expands the risk and uncertainty zone of the behavioral strategies of the interacting subjects. With one-sided use of only formal regulatory institutions, their role in the interaction of the financial and credit and innovation sectors is quite contradictory and sometimes fruitless. This fact is confirmed by the implementation of numerous state programs for financing priority sectors of the economy through the involvement of commercial banks and the use of a wide range of incentive tools (insurance, subsidies, tax breaks, etc.) and the simultaneous impact of regulatory requirements of the financial regulator aimed at minimizing risks — they do not allow the subjects of the financial and credit sector to adequately finance the needs of the subjects of the real (including innovative) sector, distorting the initial behavioral strategies (Rakhmetova et al., 2017).

In this regard, we believe that maintaining stable intersectoral interaction can be achieved by replacing strict measures with indirect and incentive measures that would give freedom of action to financial and credit sector entities, but with stricter responsibility for the results of decisions taken. At the same time, the parties involved in the implementation of an innovative project (financial organizations and innovative enterprises) must share not only the profit in case of a successful outcome, but also the losses in case of failure (adaptation and implementation of the principles of Islamic Finance). In this case, the rationality of using the principles of Islamic Finance, in our opinion, is justified, since formal institutions must necessarily be supported by properly nurtured informal ones, which contain and operate a more robust mechanism of self-support, including certain behavior based on high responsibility, morality, honor and conscience. Additional arguments for adapting certain principles of Islamic banking can be: 1) stability of interaction is ensured due to the fact that monetary resources are provided with real assets; 2) the principle of partnership prevails, eliminating the dominance of one of the parties (reducing asymmetry); 3) a mechanism for mandatory mutual fulfillment of obligations by the parties is built in.

It is important to note that within the framework of improving institutional reforms, models of state regulation that have long been developed in the world can be used. Judging by the emerging trends of expanding the state's presence in promoting intersectoral development, Kazakhstan uses the Anglo-Saxon model of regulation, which is based on the state's influence on the economy through the financial and credit sector, in particular the banking sector (this model is widely used in Canada and England). The essence of this model is that the primary assistance and support of the state is provided primarily to financial and credit organizations in order to direct financial resources to the development of the real economy, including innovation. However, the choice of this model, in our opinion, exacerbates the asymmetry in the development of sectors and limits their convergence, since the funds allocated by the state are deposited in the financial and credit sector due to high risks. The question arises “How to break this vicious circle? “The answer to this question is given by the second model of state regulation of intersectoral interaction — continental (used in European countries), in which the state directs its assistance and provides support directly to the real and innovative sectors, or the state pointwise participates in supporting enterprises of priority industrial sectors in times of crisis, which raises the level of development of the real (including innovative) sector to an investment attractive in the “eyes” of financial and credit organizations. We believe that the use of the continental model solves several unsolved problems: 1) a decrease in dependency sentiment in the financial and credit sector; 2) increased competition in both sectors; 3) increased presence in priority industries, which is supported by the state, which reduces industry risks; 4) opens access to resources for industrial enterprises, which improves their condition, increasing their solvency and creditworthiness.

In addition, the high level of state intervention in the economy in a market economy indicates the asymmetry of institutional reforms. The weakness of the institutions of an independent assessment, the lack of specific limits of state participation in economic processes, lack of transparency institutional changes, reforms “for the sake of reforms” and not in the name of the specific results — all this, in our view, triggers the growth of bureaucracy and corruption, limiting the effectiveness of cross-sectoral collaboration, which should ensure stable and progressive development of the entire Kazakh economy.

Thus, the current system of institutions regulating the subjects of interaction between the financial and credit and innovation sectors of the economy, against the background of an imperfect institutional environment, still does not contribute to the activation of a qualitative process of interaction that ensures high and stable economic growth. The initial, high rate of change of existing and introduction of new formal institutions is in conflict with established informal institutions, dooming the implemented institutional reforms to failure, creating an institutional vacuum that exacerbates the asymmetric nature of interaction between the subjects of the financial and credit and innovation sectors of the Kazakh economy.

The next element of the institutional matrix is the institutional infrastructure, the elements of which together are designed to maintain the interaction process in an up-to-date state, in a correctly set trajectory and regardless of cyclical fluctuations, not allowing the subjects of the sectors to move away from each other.

The practice of economically developed countries of the world shows that the solvency of the infrastructure and all its main elements is ensured: by the state, partly by the state, partly by private business. Despite the fact that individual elements of the infrastructure have already been developed in Kazakhstan through analysis and adaptation of international best practices (operation rating, statistical and collection agencies, credit bureaus, the institutions of guarantees and insurance), however, the problems of interaction of subjects of financial-credit and innovative sectors a not reduced, because of the weakness of the institutions of an independent assessment of the risks of real assets; institutions insurance investment risks in the innovation sector; lack of private development institutions, underdevelopment of the segment of auxiliary information-analytical and consulting agencies with increased responsibility for the results of their activities, etc.

In terms of ensuring positive effects by means of interaction between the financial and credit sectors, it is necessary to diversify the levels of the banking sector as a leading segment of the financial and credit system as a part of the infrastructure. In particular, it is necessary to take into account the significant territorial dispersion of the economically and industrially developed zones of Kazakhstan and their distance from the center of the country through the expansion of financial and credit organizations of a specialized level, the main feature of which will be represented by regional and sectoral binding. For example, successful implementation of such example is available in Germany (land banks), Switzerland (office banks), Denmark (infrastructure “green” banks), the Netherlands (agricultural innovation banks), India (craft banks), and Bangladesh (rural banks). We believe that the best solution, taking into account the peculiarities of the development of the domestic economy, will be the revival of branch banks in key sectors of the economy with the function of crediting innovative projects for each specific industry that has its own specifics. The form of ownership of such banks can be either private or shared with the state. Deepening regional and industry diversification will ensure, in our view, that local regional characteristics and industry specifics are taken into account, that individual approach to risk assessment is taken, that appropriate methods are developed and gradually improved, and that staff competencies are increased. The use of the public-private partnership model in the formation of such financial structures is a priority for work in the innovation sector, as it will simplify access to an adequate amount of resources necessary for the implementation of all stages of the innovation process and will make it possible to use state institutions of insurance, guarantees and subsidies. A supportive set of measures can be the practice of applying a differentiated approach to the implementation of prudential and tax policies in relation to such elements of the institutional infrastructure in accordance with the results of their activity and effectiveness in the innovation sector.

One of the relevant issues of forming the appropriate information infrastructure in Kazakhstan is the establishment of the Institute of national rating assessments. However, views on the activities of international agencies (Fitch, Moody's, Standard&Poor's) has changed significantly after the global financial crisis, increasing the degree of distrust towards them, making possible the creation of a network of national rating agencies

107

of national and regional importance on the basis of licensing or regional rating agency on the basis of the National Bank of the Republic of Kazakhstan while pinning responsibility for the results of such activities.

Thus, the modernization and improving the existing infrastructure can significantly reduce the pressure of key barriers on the process of interaction between the subjects of the financial and credit and innovation sectors of the economy. The solvency, diversity and availability of fully developed infrastructure elements can give impetus to the convergence of financial and credit organizations and innovative enterprises. This element of the institutional matrix is designed to eliminate existing market failures and contribute to the formation of stable informal institutions that ensure the stability of not only the process of intersectoral interaction, but also the development of the economy as a whole.

Innovations as an element of the institutional matrix, representing various types of novelty and novation (Yagudina, 2004), reflect not only significant changes in the structure of the economy, contributing to progressive economic development, but also can form the basis for the development of new forms of interaction between financial and credit organizations and enterprises of the innovative sector. The presence of signs of dynamic development in the essence of innovation is noted in his works by J. Schumpeter (Schumpeter, 1982).

Asymmetric processes in the development of the innovation sector and existing regulatory institutions is confirmed by the fact that in the conditions of realization of the program of industrial — innovative development in the Republic of Kazakhstan, the level of innovative activity of enterprises the last few years does not exceed 7–8 %, while, in developed countries this ratio is much higher: Germany — 70 %, Canada — 65 %, Belgium — 60 %, in Denmark — 55 %, Europe 20 — 40 %.

Discussions

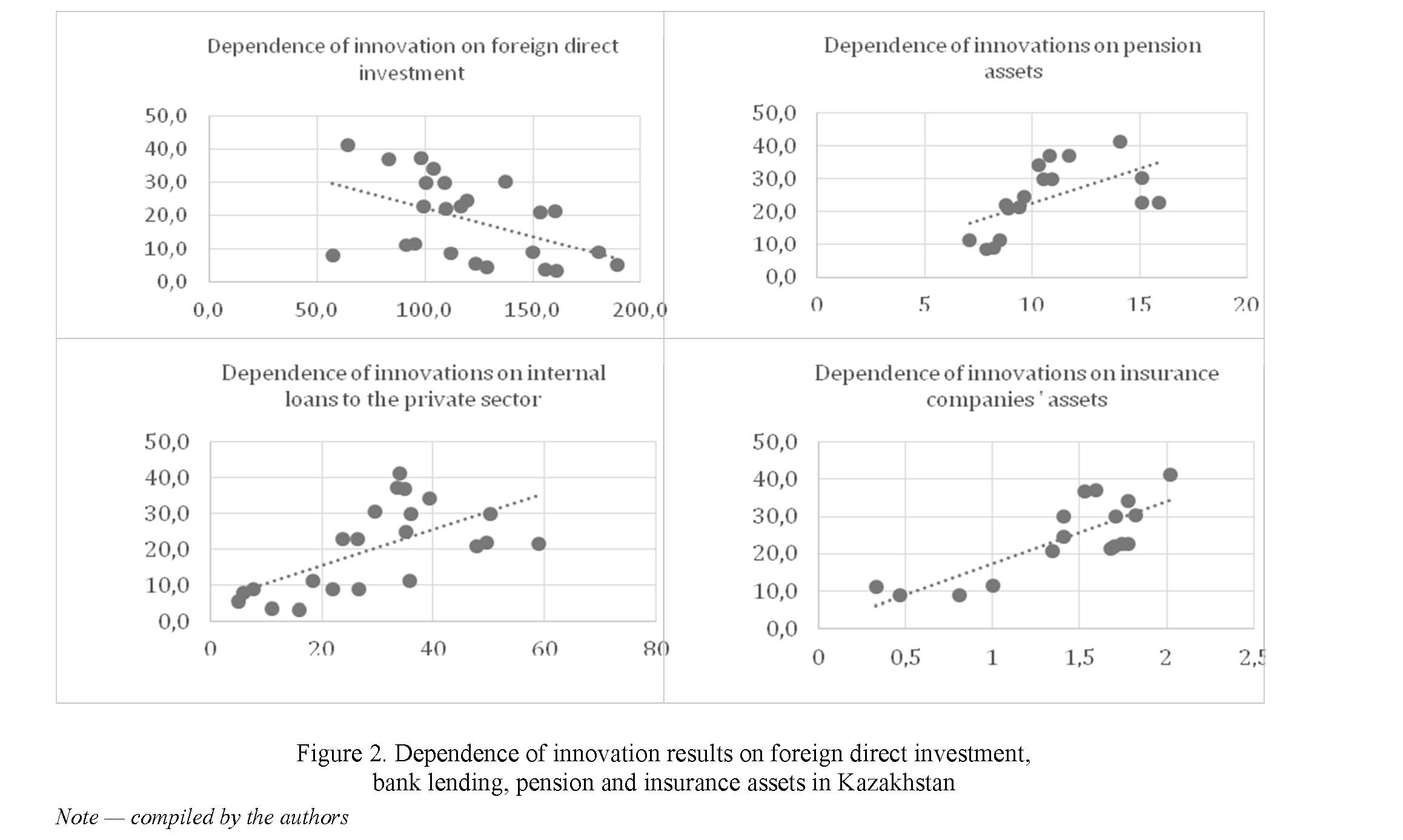

The results of the analysis of a group of factors showed that there is an inverse relationship between the export of high-tech goods in Kazakhstan and foreign direct investment (rlnnj3 = –0.48) (Figure 2).

The result confirms the thesis that the quantitative growth of foreign direct investment does not provide a guaranteed impact on improving the results of the innovation sector in the Republic of Kazakhstan. This result is not accidental. It confirms the choice of the so-called “catch-up development” model by Kazakh enterprises in the industrial sector, according to which the owners of enterprises (both domestic and foreign investors) do not invest resources in innovative developments, but buy ready-made high-tech equipment. The assessment of the impact of bank loans showed the strongest correlation between the indicator of exports of high-tech products with indicator of domestic lending to the private sector, since the correlation coefficient has the value. All regression coefficients are statistically significant. At the same time, with an increase in the share of domestic loans to the private sector in GDP by 1 %, the share of high-tech exports in industrial exports will grow by 0.49 %. Similarly, an increase in the share of long-term bank loans to legal entities in GDP by 1 % will contribute to an increase in the share of exports by 1.8 % respectively.

As part of the assessment of the impact of pension and insurance sector assets on the indicator of innovation performance (exports of high-tech products in the total volume of industrial exports) in the Republic of Kazakhstan, it was found that the resulting indicator is influenced mostly by the assets of insurance companies (rinnA3 = 0.79) and to a lesser extent by pension assets (rInnA2 = 0.56).

If the share of banking assets in GDP increases by 1 %, we can expect an increase in the share of high- tech exports in industrial exports by 0.33 %. In turn, if the share of pension assets increases by 1 %, the share of exports of high-tech goods will increase by 1.89 %. The increase in the share of insurance companies' assets will contribute to the growth of exports of high-tech products by 29.4 % of industrial exports.

Thus, despite the still insufficient role of the banking, pension and insurance segments in financing innovative companies, due to the concentration of long-term resources, they have a great potential to interact with the subjects of the innovative sector of Kazakhstan.

Conclusions

Thus, the analysis of institutional inconsistencies that exacerbate the asymmetric nature of interaction between the financial and credit and innovation sectors of the economy allows us to conclude that the main reasons for the periodic cooling of relations between the subjects of two important sectors for the economy and their periodic distance from each other are: 1) the dominance and pressure of formal institutions without a focus on the cultivation of stable informal institutions; 2) the weakness of the institutional infrastructure; 3) the absence of an integrated approach to the implementation of economic policy, when each of its directions has a purely individual goal setting and an appropriate vector; 4) in the context of dynamic economic development there is a mismatch between time and the stage of initiation and implementation of innovation by actors, interactions and the regulatory bodies (in terms of the key stages of the economic cycle — in times of crisis innovation sector needs funding for innovation, in order to overcome the crisis and financial-credit institutions do not want to risk, and, conversely, in a period of economic growth — financial and credit organizations are willing to risk and finance innovations in order to diversify their investments, but the subjects of the innovation sector are not ready for this kind of borrowing.

References

- Brown, J.R., Martinsson, G. & Petersen, B.C. (2017). Stock markets, credit markets, and technology-led growth. Journal of Financial Intermediation, 32, 45–59.

- Xiao, S. & Zhao, S. (2012). Financial development, government ownership of banks and firm innovation. Journal of International Money and Finance, 31, 880–906.

- Botric, V. & Bozic, L. (2017). Access to Finance — Innovation Relationship in Post-Transition. KnE Social Sciences, 1, 28–41.

- Hudson, J. & Orviska, M. (2014). Financial Institutions, Universities, Innovation and Growth: The Whole Story. 8th International Conference on Currency, Banking and International Finance. The Role of Financial Sector in Supporting the Economic Recovery of CEE Countries, Bratislava, 121–132.

- Viskovic, J. & Udovicic, M. (2017). Awareness of SMEs on the EU Funds Financing Possibilities: The Case of Split- Dalmatia County. KnE Social Sciences, 1, 319–332.

- Kryskova, L. & Strzelczyk, W. (2013). Public Aid in Financing innovations in Poland: The Operational Programme “Innovative Economy”. Business and Non-Profit Organizations Facing Increased Competition and Growing Customers Demands, 12, 169–186.

- Nicolov, M. (2013). Modelling European Public Finance and Support for RDI Sector. Procedia Economics and Finance, 6, 754–759.

- Fogarassy, C., Horvath, B. & Magda, R. (2017). Business Model Innovation as a Tool to Establish Corporate Sustainability. Visegrad Journal on Bioeconomy and Sustainable Development, 6, 50–58.

- Yuzvovich, L.I. (2012). Finansovo-kreditnyi mekhanizm dlya privlecheniya real'nykh investitsii [Financial and credit mechanism for attracting real investment]. Finansy i kredit — Finance and credit, 32(512), 53–59.

- Rakhmetova, A., Kalkabayeva, G., & Essengeldin, B. (2019). Finansovaya podderzhka innovatsionnykh proektov po linii institutov razvitiya [Financial support for innovative projects through development institutions]. Vestnik Karagan- dinskogo universiteta. Seriya Ekonomika — Bulletin of the Karaganda University. Economy series, 2(94), 113–120.

- North, D. (1997). Instituty, institutsional'nye izmeneniya i funktsionirovanie ekonomiki [Institutes, institutional changes and the functioning of the economy]. Moscow: Publishing Foundation of the economic book “Beginnings”.

- Gusmanova, Zh., & Kurmanalina, А. (2019). Osnovnye tendentsii v oblasti optimizatsii sistemy regulirovaniya: mirovoi opyt [The main trends in the field of optimization of the regulation system: world experience]. Vestnik Karagan- dinskogo universiteta. Seriya Ekonomika — Bulletin of the Karaganda University. Economy series, 2(94), 232–239.

- Rakhmetova, A., Kurmanalina, А., Gusmanova, Zh., & Erzhanova, S. (2017). Napravleniya stimulirovaniya bankov v finansirovanii innovatsionnogo sektora [Directions encouraging banks in financing innovation sector]. Vestnik Kara- gandinskogo universiteta. Seriya Ekonomika — Bulletin of the Karaganda University. Economy series, 4(88), 231– 239.

- The World Bank (2019). International statistical classification. Retrieved from https://databank.worldbank.org/ home.aspx.

- The National Bank of Kazakhstan (2019). Statisticheskii byulleten' [Statistical Bulletin]. www.nationalbank.kz Retrieved from http://www.nationalbank.kz/cont/Binder12.pdf.

- The Global Innovation Index. (2019). INSEAD international business school, Cornell University, World Intellectual Property Organization. National Agency for technological development. www.globalinnovationindex.org Retrieved from https://www.globalinnovationindex.org

- Bagudina, E. G. (2004). Ekonomicheskii slovar' [Dictionary of Economics]. Moscow: Publishing Prospect.

- Schumpeter, J. (1982). Teoriya ekonomicheskogo razvitiya [The theory of economic development]. Moscow: Publishing Progress.

- Litvinova, A. (2015). Innovatsionnaya aktivnost' v Rossii stabil'na, no ne vyderzhivaet mezhdunarodnoi konkurentsii [Innovative activity in Russia is stable, but does not withstand international competition]. Ezhednevnaya delovaya gazeta RBK daily — Daily business newspaper RBC daily. Retrieved from http://www.rbcdaily.ru