Abstract

Object: The purpose of this study is to determine the degree of influence of various economic indicators on the competitiveness of Kazakhstan's economy. To identify the challenges of competitiveness' establishment. At the moment, there is a need to find ways to increase the competitiveness of domestic economy in the light of Kazakhstan's integration into the world. The purpose of the study is to identify the features of the competition development in the modern economy of Kazakhstan. The object of the study are the aspects of competition in the economy of Kazakhstan. The subject of the study are the peculiarities of competition in Kazakhstan as an integral feature of a market system that can positively affect the country's economic growth.

Methods: statistical and comparative analysis.

Findings: This article explores aspects that affect competitiveness. Performed was the analysis of indicators on the global competitiveness rating, foreign direct investment (FDI) for the period of 2009–2019 for such countries as Kazakhstan, Russia, Azerbaijan, and Kyrgyzstan. FDI is an indicator of the “confidence” of investment by large companies. Studied were the indicators of the innovation index and the costs of research and development for the period of 2011– 2019.

Conclusions: Globalization and the post-industrial era require Kazakhstan to increase competitiveness. At this stage of development, innovative methods of increasing the economy are becoming more and more sought after. The results of the study allow us to conclude which of the listed aspects affect the competitiveness of the domestic economy. These results are very important for decision making within the economy.

Introduction

The basis for developing competitive relations in Kazakhstan and increasing the competitiveness of its economy should not be formed according to foreign standards, but rather on our own experience of evolutionary development using incentive mechanisms of the state in expanding competition among domestic producers and modernizing the national economy.

Literature review

In the process of research, we have analyzed the scientific works of Russian and foreign scientists on the issues of economic competitiveness: M. Porter, R. Huggins, K. Giovanni, G. Edimon and Kiyoshi Taniguchi, K.S. Momaya, etc.

At the same time, the study of competitiveness and the development of proposals to regulate this phenomenon in Kazakhstan are characterized by the peculiarities common to most countries at their nascent stage. Domestic authors studying the country's competitiveness and conducting research are as follows: G.K. Ki- shibekova, G.A. Abdulina, S.M. Zhanbyrbayeva, G. Aubakirova, I.P. Stetsenko, E. Orynbasarova, etc., and statistical data published in domestic and foreign periodicals.

Results

In Kazakhstan, the competitive environment has not formed in an evolutionary way as it has in most developed countries, but by creating institutional conditions for the competitive behavior of economic entities.

During its development, domestic economy was accompanied by crises of economic and political instability, thereby negatively affecting the conditions and forms of competitive relations.

The modern economic reality, characterized by the transformation of economic relations, the globalization of business, the integration of Kazakhstan into the world places an even greater responsibility on the development of competitive relations for improving economic, innovative indicators, the quality of life and the well-being of society.

The concern of modern analysts is caused, above all, by the fact that the majority of domestic entities with their uncompetitive goods cannot withstand competition with import (Huggins, R. 2015).

Therefore, addressing the issues related to the selection of ways of economic development based on innovation is becoming particularly relevant. The creation of optimal motivational conditions for both business and employees for the effective development of competitive relations can contribute to this (Jha, S. K., 2018).

A number of works and studies of various economic schools and directions in foreign economic literature are devoted to competition issues.

The first most comprehensive theoretical provisions on competition issues were formulated in the XVIII century by the classics of political economy (A. Smith, D. Ricardo, J.S. Mill). They have developed a model of perfect competition and characterized the features of a competitive market. Deviation from perfect competition, as a reference model of the market, was regarded negatively. Neoclassicists A. Marshall, A. Cournot argued that monopoly, as the antipode of free competition, reduces the efficiency of the economy. (Porter M., 2016).

The development of competition concepts leads to the realization that competition and monopoly are so interwoven that it makes it necessary to talk monopolistic competition, such a market structure which combines features of both competition and monopoly at the same time. (Pragya Bhawsar, 2015).

Later, J. Schumpeter has expressed the essence of competition in the struggle between the new and the old. Thanks to competition, the economy “cleanses” itself of inefficient firms. The economist called this process a “creative destruction” and paid great attention to the relationship between innovation and competition.

Competition is not static. It develops under the influence of various factors; the forms and methods of competitive relations are being transformed, the criteria for competitive advantages, competitiveness, etc. are changing. This circumstance determines the importance of further studying the specifics of competitive relations in the modern economy of Kazakhstan and addressing the issues related to the motivation of competitive behavior of its economic agents.

The term “competition” comes from the Latin word “concurrentia,” which means, collision. At the same time, it is legitimate to note that this concept is cognate to the Latin term “concurus,” competition. The fundamental similarity of concepts implies a single competitive character of competition. (Aiginger, K. 2015)

With the development of society's economic system, forms and methods of competitive relations evolve as well, reflects in theoretical provisions on the competition content. (Aiginger, K. 2015)

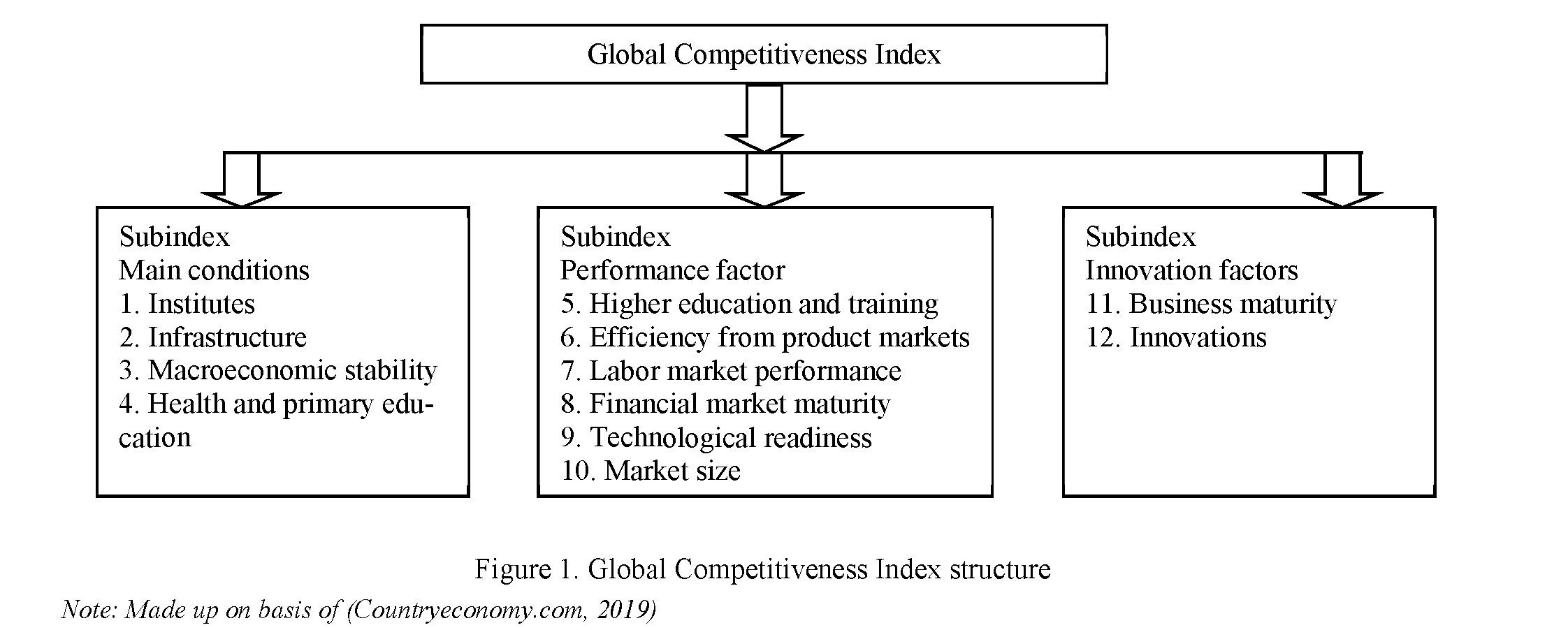

Figure 1 shows the mutual relations between the components: The Global Competitiveness Index (GCI). Also indicated are the sub-indices included in the final index. We emphasize once again that the ratio of estimates of 12 terms is constant, but the proportion of sub-indices in the final indicator varies depending on the stage of country's development.

In the Global Competitiveness Rating as of 2019, Kazakhstan ranks 55th with an index of 62.9 (out of 141 countries). This indicator has decreased by 1.13 index points compared to the maximum for 2016, which

amounted to 64.07. Observing the competitiveness index in the period of 2013–2019, one can note the stagnation of index fluctuations (Trading economics. 2019).

One of the reasons for the low competitiveness is that domestic companies cannot compete with companies from Western and Southeast Asian countries on equal ţегтśю therefore, if foreign trade is liberalized, all domestic production will be supplanted by import (Stetsenko, I. 2017).

In Table 1, we reflect the Global Competitiveness Index in a comparative analysis for the period of 2009– 2019, for such countries as Kazakhstan, Kyrgyzstan, Russia, and Azerbaijan.

|

Date |

Kazakhstan (Competitiveness) |

Kyrgyzstan |

Russia |

Azerbaijan |

||||

|

Ranking |

Index |

Ranking |

Index |

Ranking |

Index |

Ranking |

Index |

|

|

2019 |

55 |

62.94 |

96 |

54.00 |

43 |

66.74 |

58 |

62.72 |

|

2018 |

59 |

61.80 |

97 |

53.02 |

43 |

65.62 |

69 |

60.04 |

|

2017 |

57 |

62.14 |

102 |

55.71 |

38 |

66.29 |

35 |

67.00 |

|

2016 |

42 |

64.07 |

102 |

54.78 |

45 |

63.42 |

40 |

64.35 |

|

2015 |

50 |

63.09 |

108 |

53.22 |

53 |

62.43 |

38 |

64.72 |

|

2014 |

50 |

62.95 |

121 |

51.01 |

64 |

60.66 |

39 |

64.48 |

|

2013 |

51 |

62.52 |

127 |

49.09 |

67 |

59.96 |

46 |

63.01 |

|

2012 |

72 |

59.78 |

126 |

49.25 |

66 |

60.21 |

55 |

61.63 |

|

2011 |

72 |

58.85 |

121 |

49.79 |

63 |

60.54 |

57 |

61.26 |

|

2010 |

67 |

58.22 |

123 |

48.00 |

63 |

59.33 |

51 |

61.43 |

|

2009 |

65 |

58.66 |

122 |

48.60 |

51 |

61.63 |

69 |

58.60 |

|

Note: Countryeconomy.com, 2019: https://countryeconomy.com/government/global-competitiveness-index/kazakhstan |

||||||||

Table 1. Kazakhstan — Global Competitiveness Index

Table 1 clearly shows that Kazakhstan has scored 62.94 points out of 100 in the 2019 Global Competitiveness Report. Competitiveness rating: Russia (43rd), then Kazakhstan (55th), Azerbaijan (58th), and Kyrgyzstan (96th). (Countryeconomy.com).

The latest issue of the 2019 Global Competitiveness Report estimates 141 countries. GCI (Global Competitiveness Index) ranges from 1 to 100, a higher average score means a higher degree of competitiveness.

Report consists of 98 variables based on a combination of data from international organizations and on a survey of the World Economic Forum leaders. These variables are organized into twelve columns with the most important ones, including the following: institutions, infrastructure, ICT implementation, macroeconomic stability, health, skills, product market, labor market, financial system, market size, business dynamism, and innovative potential.

In its 2018 edition, the World Economic Forum has introduced a new methodology with a goal to integrate the concept of the 4th industrial revolution into the definition of competitiveness. It emphasizes the role of human capital, innovation, sustainability and flexibility as not only the driving forces, but also the defining characteristics of economic success in the 4th industrial revolution. (Trading economics, 2019).

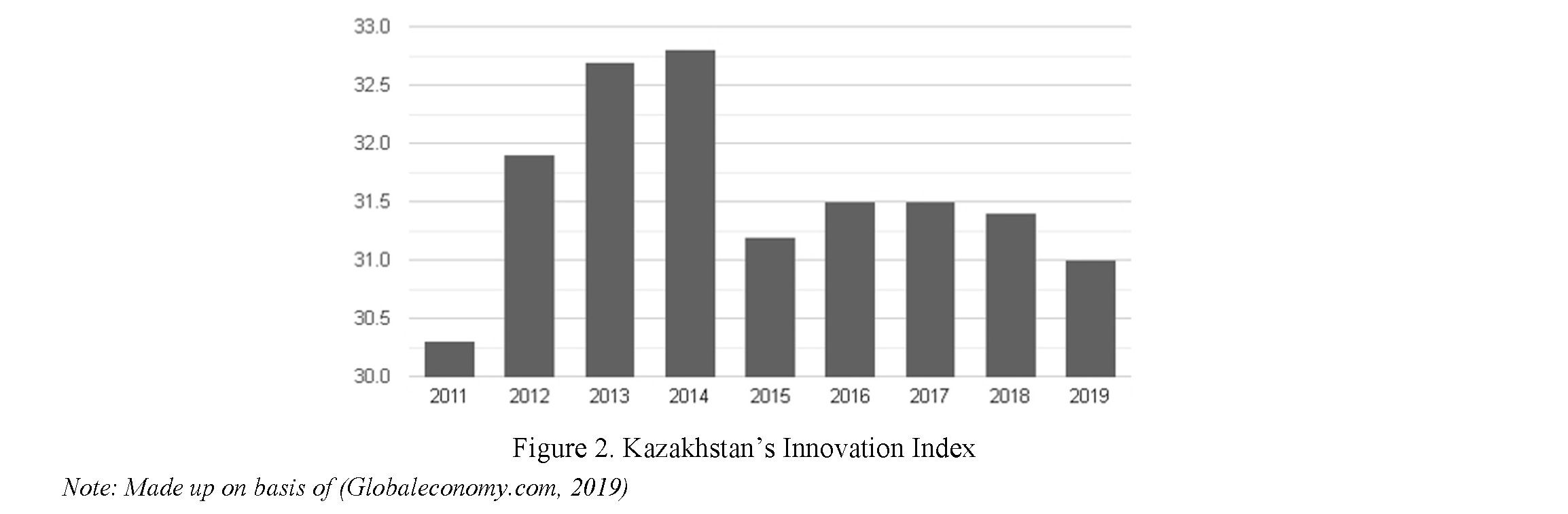

Next, we consider the indicator of the Innovation Index, which varies from 0–100. For this indicator, Cornell University, INSEAD, and the WIPO provide data on Kazakhstan for the period of 2011—2019. The average for Kazakhstan during this period was 31.59 points with a minimum of 30.3 points in 2011 and a maximum of 32.8 points in 2014. (The WorldBank, 2019).

Серия «Экономика». № 1(97)/2020

123

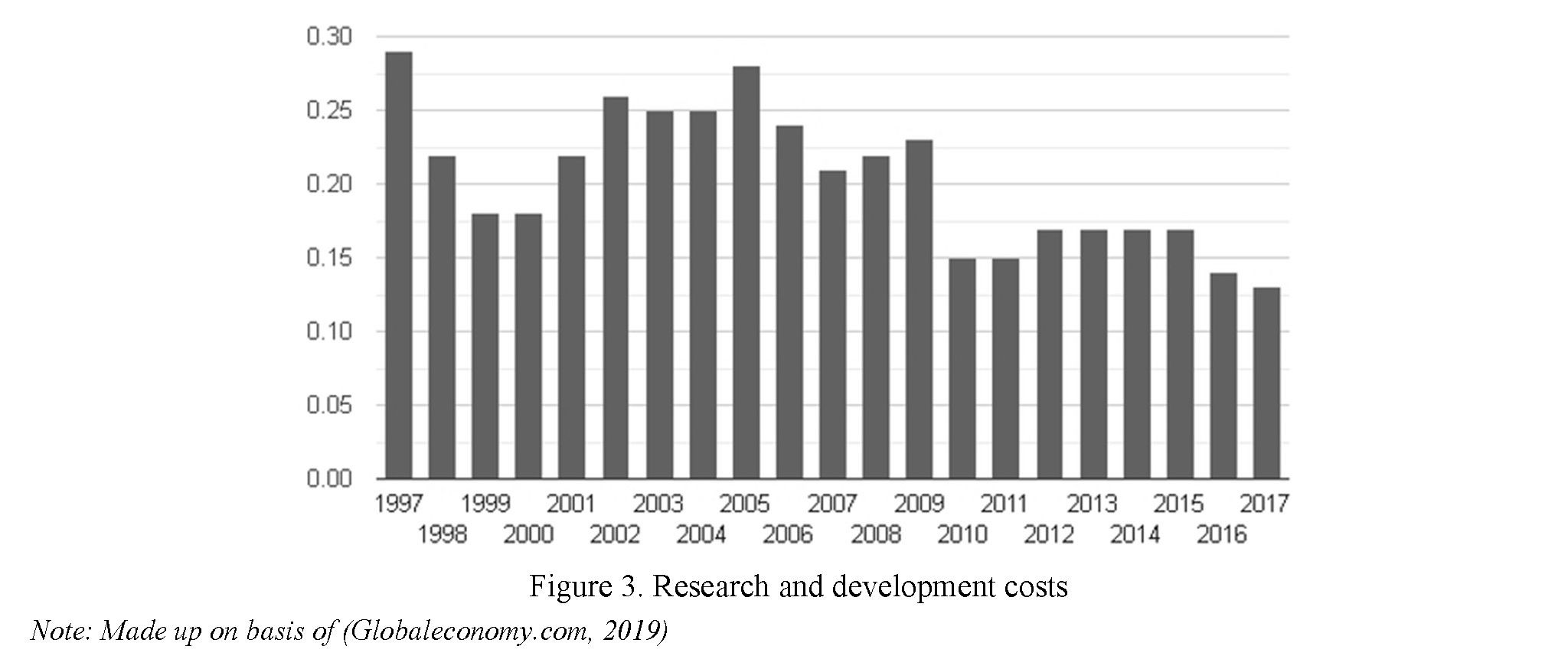

The next important indicator that affects competitiveness is research and development costs, percentage of GDP: For this indicator, The United Nations provides data on Kazakhstan for the period of 1997–2017. The average for Kazakhstan during this period was 0.2 % with a minimum of 0.13 % in 2017 and a maximum of 0.29 % in 1997 (The World Bank, 2019).

The final result demonstrates Kazakhstan's low competitiveness, underdeveloped institutions and low performance of product and financial markets, low competitiveness of companies with a relatively higher development of education, scientific and technological infrastructure. This result was obtained thanks to the aggregation of 114 primary indicators, among which on 24 indicators our positions are higher than our final 53rd place, and on 87 they are lower. Among 114 indicators, about 80 were obtained as a result of a survey of business representatives, 17 are data from statistics of international organizations and 16 are data from other indices, in particular, “Doing Business” (Caurkubule et al., 2019)

To protect and increase competitiveness, countries need to develop leading industries through tariffs or quotas until they become competitive in the global economy, and only then can they open the market.

This argument has the right to exist where it meets two conditions:

– first, in case of protection, the industry should develop at a faster pace than that of foreign competitors';

– second, the initial drag in competitiveness should be small. Protection of each industry leads to welfare losses; therefore, protectionism should be extremely selective and limited in time. If you protect all industries, the real exchange rate of the national currency increases, the benefit of each industry is small, and the welfare losses are huge.

The same thing happened in most developing countries where industrial policy is based on the restriction of imports. Each industry would declare itself almost competitive. Naturally, defenses would be sought by politically strong industries, and not those actually growing.

At the same time, due to the lack of competition, entities would not have incentives to increase efficiency; therefore, the “almost competitive” industries could not manage to get rid of this “almost” and they would demand an extension of the protection period. (Esengeldinova et al., 2017)

The next important aspect of competitiveness is foreign direct investment (FDI). It is a form of participation of foreign capital in the implementation of investment projects in the host state, which is a long-term investment of a foreign investor in manufacturing, trading and other commercial entities for profit.

The methodology of the International Monetary Fund (IMF), which annually calculates the volume of foreign direct investment at the international level, states that foreign investment can be considered direct if it implies the acquisition by a foreign investor of at least 10 % of the commercial organization's share capital in the territory of the host state, and allow the investor (or his representative) to exert a strategic influence on the invested entities, including partial or complete control over them. In practice, however, in some countries, a 10 % stake in the share capital of an invested entity is considered insufficient to establish effective control over the management or to demonstrate long-term investor interest. (Tlesova et al., 2019)

Thus, foreign direct investment as a whole should be large enough and long-term to allow a foreign investor to establish effective control over the management of the invested entity and ensure its long-term interest in the successful operating and development of said entity. At the same time, the long-term investment as part

124

Вестник Карагандинского университета

of FDI limits the investors' possibilities to quickly exit the market and thereby increases the interest of FDI importing countries in them. In many countries, the implementation of investment projects involving foreign capital is regulated by law, and the structure of the executive branch, as a rule, includes a state body responsible for the development and implementation of state investment policy.

The main stimulus for the intensive development of the international investment process is the need for large businesses to increase their competitiveness at the international level by means of expanding their activities in new markets, production rationalization, reducing costs, diversifying risks and gaining access to resources and strategic assets in the economies of different countries. Currently, the main subject of FDI are international companies and financial groups.

The basis of FDI data in the economies of different countries is the periodicals of the statistical reports of the International Monetary Fund's (IMF) Balance of Payments Statistics series, the World Bank's World Development Indicators, and the United Nations Conference on Trade and Development's (UNCTAD) World Investment Report, as well as annual economic reports of national statistical institutes, the data from which are accumulated by the indicated international organizations (Koksharov et al., 2019).

Presented is the table of FDI over the past 10 years for four countries: Kyrgyzstan, Azerbaijan, Russia, and Kazakhstan.

Table 2. FDI for the period of 2009–2019 (million USD)

|

FDI amount |

Kazakhstan |

Azerbaijan |

Russia |

Kyrgyzstan |

|

2019 |

208,064,585 |

1,402,998,000 |

8,784,850,000 |

46,599,800 |

|

Rating |

134 |

75 |

31 |

161 |

|

2018 |

471,263,147 |

2867487000 |

28557440000 |

-107212800 |

|

2017 |

172,209,625 |

4499666000 |

32538900000 |

619220700 |

|

2016 |

657,782,404 |

4047630000 |

6852970000 |

1144054000 |

|

2015 |

730,811,264, |

4430466000 |

22031340000 |

343010700 |

|

2014 |

1,001,129,328 |

2619437000 |

69218890000 |

612016900 |

|

2013 |

1,364,813,437 |

5293250000 |

50587560000 |

260927500 |

|

2012 |

13760291528,5034 |

4485120000 |

55083630000 |

685760800 |

|

2011 |

7456117901,08145 |

3352997000 |

43167780000 |

472768300 |

|

2010 |

14275888207,0145 |

2900030000 |

36583100000 |

189377400 |

|

2009 |

16818890680 |

3986807000 |

74782910000 |

376992152,1 |

Note: (The World Bank, 2019): https://datarworldbank.org/indicator/BX.KLT.DINV.CD.WD? most recent year desc=false

In 2018, Kyrgyzstan observed negative FDI, which was due primarily to the fact that foreign investors would withdraw more of their funds than they would invest.

However, an increase in capital investment in the first half of this year would seem like a positive signal. In the whole country, this grew up to 5.25 trillion tenge (13.82 billion USD) or almost 12 % compared to the corresponding period of 2018.

A significant increase was enjoyed by investments in such areas as agriculture (by 62.7 % to 191 billion tenge), construction (by 54.7 % to 52.86 billion tenge), mining (by 31.7 % to 2.67 trillion tenge). However, we also noted a significant drop in investment indicators in the manufacturing industry for the reporting period due to the completion of a number of large investment projects, and a number of other reasons: by 37.9 % to 344 billion tenge. This is despite the sharp increase in the indicator for Nur-Sultan, Karaganda and East Kazakhstan regions.

We should note that the fixed rate of growth in capital investment is still lagging behind the annual increase by average of 20 % indicated by the government in order to bring their share to 30 % of GDP by the middle of the next decade. Last year, this indicator was 17.2 % on an annualized basis (11.13 trillion tenge). Given the improvement of the general conditions for doing business and the state's promotion of additional measures to support foreign investors, Kazakhstan enjoyed an increase in the volume of attracting foreign direct investment. (Reforms in Kazakhstan: successes, challenges and prospects. OECD. 2018).

In particular, according to the National Bank, the gross inflow of foreign direct investment last year amounted to 24.28 billion USD. This is the highest ever since 2012. According to the results of the first quarter of last year, 5.54 billion USD were attracted. At the same time, the net inflow of foreign direct investment (inflow of FDI to Kazakhstan minus FDI abroad) in the first quarter of 2019 amounted to 2.43 billion USD. For reference, in the period of January-March of last year, indicator in question amounted to 2.94 billion USD.

In the first quarter of 2019, more than half of the gross inflow or about 3.3 billion USD accounted for investments in oil and natural gas production, 15.5 % or 0.9 billion USD in the metallurgical industry, 9.8 % or 0.6 billion USD in wholesale and retail trade. As a result, additional measures are required for the diversification of foreign investment by industry. This includes expanding the investment attractiveness of the manufacturing sectors. In general, the accumulated direct investments in Kazakhstan have reached 151.3 billion USD, while the accumulated direct investments from the republic abroad cap at 18.2 billion USD.

The government focuses on increasing annual foreign direct investment to 34 billion USD, among other ways through further improvement of the business climate and the development of public-private partnerships in the country. In this context, noteworthy is the fact that in the World Bank's Doing Business 2019 ranking, Kazakhstan took 28th place among 190 countries, ahead of such large economies as Spain, France, Switzerland and Japan. Over the past 11 years, Kazakhstan has moved up the ranking under review by 36 points, including 6 points compared to Doing Business 2018 (Orynbasarova et al., 2017).

Table 3. FDI in the first quarter of 2019 (million USD)

|

Gross FDI inflow |

Net FDI inflow |

|

|

Total |

5 964 |

2 428 |

|

including |

||

|

The Netherlands |

1 798.9 |

154.5 |

|

USA |

1 450.7 |

1200.3 |

|

Switzerland |

647.2 |

493.0 |

|

China |

362 |

158.4 |

|

France |

255.7 |

23.0 |

|

Russia |

229.7 |

31.0 |

|

Belgium |

218.2 |

78.1 |

|

Note: Data, from NBK |

||

The dependence of Kazakhstan on oil resources holds an important value. Given that the price of oil shall only increase by 1.6 % per year from the current relatively low level (as per the latest World Bank price forecast) and labor productivity shall increase at the same rate as in the past, a strategy based on the oil and gas sector will not bring as much economic growth for Kazakhstan as in the recent past, and will not bring the country closer to achieving its growth potential.

In this case, GDP growth is expected to average only 2.3 % annually from the current moment until the year 2030. In contrast, reforms in key sectors to improve the business climate, increase competitiveness, and increase private sector participation, along with other reforms, as outlined in the new medium-term Strategic Plan (Government of Kazakhstan, 2017), shall improve the country's growth rate by about 1.2 percentage points per year (Comprehensive country review of Kazakhstan. 2017).

There is a decrease in price dynamics in the oil market. The cost of the Brent mix fell by more than 10 % compared to local maximums in the middle of last April amounting to more than 74 USD per barrel. At the same time, in April-May, the average monthly wholesale price would exceed 71 USD per barrel, while in June- July it was about 64 USD. The International Energy Agency expects this spread to be reduced to 4 USD in the last quarter of 2019.

Table 4. Dynamics of the wholesale price of Brent oil in Kazakhstan

|

Month |

Year |

USD |

|

July |

2019 |

63.91 |

|

June |

2019 |

64.22 |

|

May |

2019 |

71.32 |

|

April |

2019 |

71.23 |

|

March |

2019 |

66.14 |

|

February |

2019 |

63.96 |

|

January |

2019 |

59.41 |

|

December |

2018 |

57.36 |

|

November |

2018 |

64.75 |

|

October |

2018 |

81.03 |

|

September |

2018 |

78.89 |

|

August |

2018 |

72.53 |

|

Note: Data from the Statistics Committee of the Ministry of National Economy. 2019 |

||

The reason for the trend decline is that the long-term forecast for the global economy remains not entirely favorable, including from the point of view of the formation of global demand for crude oil and petroleum products.

Many financial experts predict a high probability of a global recession in the foreseeable future, around 2020–2021. Real demand for raw materials is now weaker than financial markets believe. Market players are closely monitoring the situation around the trade conflict between China and the USA, to which their growing political contradictions are added.

In its 2018 review of the global economy, the OECD has lowered its growth forecast compared to the previous estimate to 3.2 %. Global trade growth has slowed to the lowest levels since the financial crisis.

The consequences for oil demand are obvious: in 2019, its growth won't exceed 1.2 million barrels per day. According to International Energy Agency's estimates, in the first quarter of 2019, growth was only 300 thousand barrels per day compared to the same period last year. This was the lowest value since the last quarter of 2011. The main reason is the weakness in the OECD economies, where demand fell by a significant value of 600 thousand barrels per day due to various factors (a warm winter in Japan, a slowdown in the petrochemical industry in European countries, etc.). For comparison, countries outside the OECD have enjoyed an increase in demand of 900 thousand barrels per day, despite the decline in China. (Data from the Statistics Committee of the Ministry of National Economy, 2019).

Considering the expected oil production volumes and the projected world price of Brent oil of 55.0 USD per barrel, direct taxes from the oil sector entities into the National Fund are projected to be 1947.9 billion tenge in 2019, 1952.3 billion tenge in 2020, and 1971.9 billion tenge in 2021.

According to the pessimistic case scenario of a summary forecast for the socio-economic development of the Republic of Kazakhstan for 2019–2023 (approved at a meeting of RBC on May 15, 2018, minutes No. 9), the oil price shall drop to the level of 45 USD per barrel in 2019—2023. The average annual GDP growth amount to 3.9 %. Deteriorating external conditions and declining business activity shall restrain growth in all sectors of the economy. The average growth shall slow down to 3.7 % in tradable sectors, and to 4.1 % in nontradable ones.

In the pessimistic case scenario of the forecasts, revenues will amount to 6,614.1 billion tenge in 2019, 7395.8 billion tenge in 2020 and 7,729.5 billion tenge in 2021. For 2019–2021, the deficit is projected at 1.1 % of GDP. The non-oil deficit (excluding ETP) is projected at 6.1 % of GDP in 2019, 5.3 % of GDP in 2020, and 5.0 % of GDP in 2021. (State program of industrial and innovative development of the Republic of Kazakhstan for 2015–2019).

The main objectives for the budget policy for 2019–2021 shall be reducing the dependence of the budget on oil revenues;

To reduce the budget's dependence on oil revenues, fiscal policy will be formed on the basis of a gradual decrease in the non-oil deficit in relation to GDP and an increase in non-oil revenues.

In the medium term, the main focus shall be on reducing the level of non-oil deficit to 7.0 % of GDP in 2020.

At the same time, it is planned to maintain the budget deficit at 1.0 % of GDP from 2019, which shall allow keeping the Government debt at no more than 25.0 % of GDP. The reduction of the non-oil deficit shall be ensured by reducing the use of funds of the National Fund, stimulating the growth of revenues from the non-oil sector, and rationalizing budget expenditures.

To increase the efficiency of budget expenditures, funds shall be redistributed from ineffective programs to budget programs that ensure the implementation of the priorities of socio-economic development. (State program of industrial and innovative development of the Republic of Kazakhstan for 2015–2019).

Most crises are associated with insufficient diversification of the economy, budget dependence on revenues of the energy sector. In the presence of oil resources, countries with economies in transition have specific features of the “Dutch disease”: revenues would grow faster than productivity, and domestic goods, which were already inferior in competitiveness, became even less demanded on the domestic market. (Momaya, K.S., 2019).

At the moment, exports should be increased in other sectors of the economy, primarily manufacturing and agriculture. Given the wider range of diversified sources of growth, the country's current vulnerability to external shocks shall be reduced (Issabekov O. 2018).

The average growth of 3.5 % projected until 2030 under this scenario is lower than the potential growth of Kazakhstan at 4 % recently projected by the IMF. This is due to the fact that in the modeling of policies in chapter 6, more conservative shock effects are used compared to government ones and include only a few government initiatives to reform economic policies. With less conservative assumptions about the scope and number of reforms, a potential growth rate of 4 % proposed by the IMF may be quite achievable, which may help move towards a more diversified economy over time. (Reforms in Kazakhstan: successes, challenges and prospects. OECD. 2018).

Discussions

The revealed features of domestic competition and the proposed ways to improve the competitive environment and increase the competitiveness of the domestic economy can be taken into account in the formation of state programs for the development of competition.

Conclusions

1. Kazakhstan's oil revenues create symptoms of the “Dutch disease” for the economy. The oil industry attracts foreign investment, financial and human resources, while other sectors producing goods and services, such as agriculture and production, experience a decrease in competitiveness. Kazakhstan helps accelerate the development of the Astana financial center, which shall become the region's financial center. However, both oil and financial sectors only create limited employment, mainly with high salaries, creating pressure around inclusive growth. To counter this, the economy needs to be diversified. To create a diversified economy, the agri-food sector needs to be developed as a key to further economic development. According to projections, the decline in prices for agricultural products in international markets in the foreseeable future, along with the growth of demand in a number of developing countries slowing down and the effect of stimulating biofuel programs smoothing out, shall be less conspicuous than the drop in oil and gas prices. Initially, our country owns a large agricultural potential of Kazakhstan. The gradual introduction of digital technology shall increase productivity and reduce costs.

2.The reduction in research and development costs shall negatively affect the projected case scenario for the development of competitiveness. For effective competition, efforts should be made to interact innovation and research with business. From a broader macroeconomic point of view, government policy should stimulate the launch and growth of innovative entities. Since competition plays a key role in innovation, government needs to encourage market competition and minimize interference that distorts product and factor markets. Investments in research and development, both from the government and the private sector, are urgently needed to stimulate innovation while gradually reducing the participation of state-owned entities to expand and develop a more dynamic and innovative private sector.

References

- Aiginger, K. & Vogel, J. (2015). Competitiveness: from a misleading concept to a strategy supporting Beyond GDP goals. Competitiveness Review, 5, 497–523.

- Issabekov, O. (2018). The analysis of export competitiveness of Kazakhstan. International Conference on Mathematics, Modeling, Simulation and Statistics Application, 166–168.

- Pragya, B. & Utpal, C. (2015). Competitiveness: Review, Reflections and Directions. Global Business Review, 16, 665– 679.

- Huggins, R. & Izushi, H. (2015). The competitive advantage of Nations: Origins and journey. Competitiveness Review, 25, 458–470.

- Jha, S., Dhanaraj, C. & Krishnan, R. (2018). From arbitrage to global innovation: Evolution of multinational R&D in emerging markets. Management International Review, 58, 633–661.

- Porter, M. (2016). International Competition: Competitive Advantages of Countries. Moscow: Alpina Publisher. Giovanni, C. Edimona, G. & Kiyoshi, T. (2019). Accelerating Economic Diversification. Kazakhstan. 115–143. Momaya, K.S. (2019). The Past and the Future of Competitiveness Research: A Review in an Emerging Context of Innovation and EMNEs. International Journal of Global Business and Competitiveness, 14, 1–10.

- Kishibekova, G., Abdulina, G. & Zhanbyrbaeva, S. (2016). Factors of increasing the competitiveness of the national economy in the context of globalization. Reports of the National Academy of Sciences of the Republic of Kazakhstan, 4, 188–197. ...

- Assessment of the impact of integration on the competitiveness of member states of the Eurasian Economic Union. (2019). www.eurasiancommission.org Retrieved from http://www.eurasiancommission.org/ru/act/integr_i_makroec/dep_ makroec_pol/SiteAssets/%D0 %94 %D0 %BE%D0 %BA%D0 %BB%D0 %B0 %D0 %B4_12.12.pdf

- Reforms in Kazakhstan: successes, challenges and prospects. OECD. (2018). www.oecd.org Retrieved from https://www.oecd.org/eurasia/countries/Eurasia-Reforming-Kazakhstan-Progress-Challenges-Opport.pdf

- Comprehensive country review of Kazakhstan. In-depth Analysis and Recommendations. OECD Part II (2017). www.oecd.org Retrieved from https://www.oecd.org/dev/MDCR_Kazakhstan_Vol_2_web.pdf

- Global economy.com. (2019). ru.theglobaleconomy.com Retrieved from https://ru.theglobaleconomy.com/Kazakhstan/ Research_and_development/

- Stetsenko, I., Tasmaganbetov, A. & Aldashova, G. (2019). Otsenka konkýrentosposobnostı otrasleι promyshlennostι v Kazahstane ı Rossii [Assessment of the competitiveness of industries in Kazakhstan and Russia]. Vestnik Karagan- dinskogo universiteta. Seriya Ekonomika — Bulletin of the Karaganda University. Economy series, 2(94), 62–72.

- Countryeconomy.com. (2019). Retrieved from https://countryeconomy.com/government/global-competitiveness-in- dex/kazakhstan

- Trading economics. (2019). Kazakhstan Competitiveness Index. tradingeconomics.com Retrieved from https://tradingec- onomics.com/kazakhstan/competitiveness-index? poll=2019-03-31

- The World Bank (2019). data.worldbank.org Retrieved from https://data.worldbank.org/indicator/BX.KLT.DINV. CD.WD? most_recent_year_desc=false

- Caurkubule, Z., Kenzhin, Zh. & Sultanova, Z. (2019). Naγchnye podhody k otsenke konkýrentosposobnostı regionov [Scientific approaches to the evaluation of the competitiveness of regions]. Vestnik Karagandinskogo universiteta. Seriya Ekonomika — Bulletin of the Karaganda University. Economy series, 4(92), 153–161.

- Yesengeldinova, R. (2017). Strategies for the competitiveness of the national economy of Kazakhstan. Accelerating diversification and increasing the competitiveness of the national economy of Kazakhstan based on potential opportunities. Journal. Astana.

- Tlesova, E. Zhanabaeva, Zh. (2019) The competitiveness of the economy as the most important factor in the economic security of Kazakhstan. Journal Economics and statistics, 2, 34–35.

- Data from the Statistics Committee of the Ministry of National Economy (2019).

- State program of industrial and innovative development of the Republic of Kazakhstan for 2015–2019. (2014). qazindus- try.gov.kz Retrieved from https://qazindustry.gov.kz/docs/otchety/1650686.pdf

- Aubakirova G. (2019). New approaches to building a model of economic growth in Kazakhstan. Journal of Economic Relations. 1, 123–134.

- Koksharov, V. Jamaibaly, B. Komissarov, O. (2019). The current state of economic development of the Republic of Kazakhstan and its prospects. Bulletin of Volgograd business institute Journal. Ser. Business. Education. Law, 4, 34– 35. '

- Orynbassarova Y., Legostayeva A., Omarova A., Ospanov, G. & Grelo, M. (2017). Razvitie finansovoi podderjki inno- vatsionnoi deiatelnosti v Respγblike Kazahstan [Development of financial support of innovative activity in the Republic of Kazakhstan]. Vestnik Karagandinskogo universiteta. Seriya Ekonomika — Bulletin of the Karaganda University. Economy series, 4(88), 224–231.