Abstract

Object: To identify possible ways to improve the deposit insurance system in the Republic of Kazakhstan on the basis of studying the world practice of deposit insurance and identifying the functioning of various models of deposit insurance systems.

Methods: Used such basic methods of cognition as the method of description and comparison, periodization, generalization and logical analysis.

Results: A retrospective review of the establishment of deposit insurance systems in different countries of the world and integration associations was carried out, differences in the organization of deposit insurance according to the American and continental models were identified, suggestions were made for further improvement of the practice of deposit insurance in the Republic of Kazakhstan.

Conclusions: The author defines further directions for the development of the global practice of deposit insurance by unifying deposit guarantee systems and the emergence of superstructure deposit protection systems within integration associations and the functioning of cross-border insurance systems. Based on international experience, the author formulated a conclusion about the need to change the legislative conditions for guaranteeing deposits in the Republic of Kazakhstan in terms of recognition by entities of the deposit insurance system of non-bank organizations, the extension of insurance liability to deposits of legal entities, and increasing the maximum security for guaranteed deposits. The author proposes a change in the practice of forming a deposit guarantee fund in order to improve the conditions for participation in the deposit guarantee system for second-tier banks.

Introduction

In the face of intensified crisis manifestations in the global financial markets and their negative impact on the solvency of banks, it becomes relevant to study the mechanisms for ensuring the financial stability of banking markets. In world practice, the creation of deposit insurance systems has become a tool to solve the problem of maintaining the financial stability of banking markets, maintaining the confidence of depositors in banks and other credit organizations, and preventing the massive withdrawal of bank deposits in the context of economic crises.

This study will allow us to summarize the global experience of deposit insurance, to identify features of the organization of deposit insurance within the framework of various models of these systems in order to identify possible ways to improve the deposit guarantee system in the Republic of Kazakhstan. In the literature, a number of authors discuss changes to the conditions of deposit insurance in order to provide the most reliable insurance protection for depositors of banks in their countries. It is a merit of the author that he allocated the best conditions for deposit insurance in various national practices and made proposals for amending domestic legislation. It is especially important to discuss the issue of changing the method of financing the deposit guarantee fund in the Republic of Kazakhstan in order to improve the conditions for participation in this system for second-tier banks.

As a scientific hypothesis, it can be assumed that, precisely, world experience in building deposit insurance systems will allow organizing the most optimal deposit guarantee system in the Republic of Kazakhstan.

Literature Review

The theoretical basis of the study was the scientific works of leading Kazakhstani, Russian and foreign economists on the study and comparison of deposit insurance systems in different countries of the world. Foreign scholars dedicated their work to the study of various aspects of theory, world practice and the analysis of deposit insurance systems: Demirgyuch-Kunt A., Kane E., Laeven L., Boyle G., Stover R., Tivana A., Zhilievsky O. (2015) , Zimovtsev V.I., Snytko A.E., Khodanchik G.E., Arzamastsev A., Kotina O. et al. (2019, 2020). The authors consider the historical aspect of creating deposit insurance systems in various countries, spend periodization phases of development of the deposit insurance system, classified deposit insurance systems that take place in the practice of foreign countries. Among foreign authors, the most famous is the work of Garcia Gillian G.H., devoted to a review of best practices for deposit insurance and their use in crisis management (2000).

Detailed study of US deposit insurance practices was conducted by Robb T. (2001). The banking crisis during the Great Depression led to the creation of a unified deposit insurance system in the United States represented by the Federal Deposit Insurance Corporation, which went through a series of development stages and successfully continues to this day. Russian scientists devoted their work to the study of American experience Turbanov A.V. and Evstratenko N.N. (2008), Zemtsov A.A. and Tsibulnikova V.Yu. (2017).

The study of the German model of deposit insurance is dedicated to the work of Beck T. (2001), which traces the history of deposit insurance against the existence of regional schemes until the creation of an insurance system for private commercial banks in 1974, and subsequently insurance systems for savings institutions and cooperative banks were created. A review of the current state and development prospects of deposit insurance systems in European countries was carried out by Kohlert W. (2015), Snell J. (2017), Scheible V., Zahari D., Bumsma P.J. et al. (2019).

The work of many scientists, including Kovalenko SB, Shernina PG, is devoted to the study of the organization of modern deposit insurance systems in the countries of the former Soviet Union. (2016), Urazova S.A., Isaeva P.G., Makhacheva D.M., Nurgazy A.R. (2017), Kononenko O.V., Zemtsova A.A., Tsibulnikova V.Yu. (2018). The works of these authors carry out a comparative analysis of the American and European models of deposit insurance systems, examine the practice of deposit insurance in the CIS countries and countries of the Eurasian Union, formulate suggestions for improving modern deposit guarantee practices in the Russian Federation and the Republic of Kazakhstan. Scientists' proposals are related to the justification of such basic conditions of deposit insurance as objects and subjects of deposit insurance, deposit currency, differentiation of tariff rates, the size of the maximum insurance coverage, etc.

Methods

The object of the study was the historical processes of organizing deposit insurance systems in world banking practice.

The subject of the study was economic relations regarding the functioning of deposit insurance on the example of different countries and integration associations.

When writing the article, we used both general scientific methods of cognition, such as historical and logical methods, analysis and synthesis, induction and deduction, the method of scientific abstractions, the use of analogies, and empirical methods of cognition such as methods of generalization, periodization, description and comparison.

Results

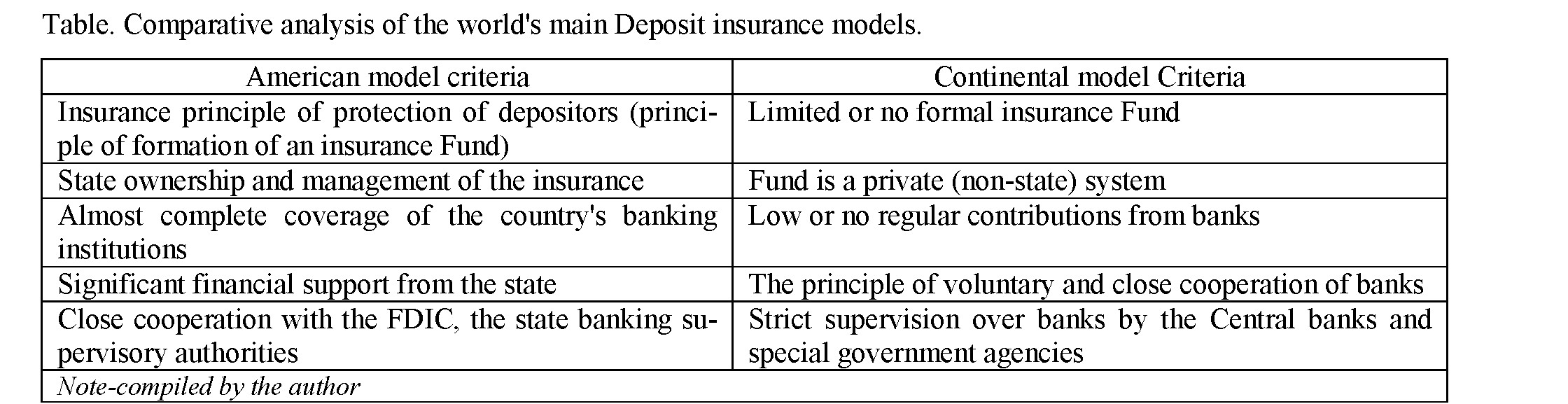

In world practice, two main models of the functioning of deposit insurance systems have formed: American and German. The American system involves the creation of a state corporation that provides insurance for deposits attracted by banks from private and corporate clients. The German system is focused on the creation of a number of deposit insurance funds associated with associations of banks of certain types. In this case, insurance is carried out on a voluntary basis and the initiative to create insurance funds belongs to banks and their associations, associations.

The first experience in creating a system of guaranteeing deposits in the form of insurance took place in the USA in the 19th century. Initially, legislation was drafted to regulate banking at the state level and various insurance systems appeared that attracted funds from banks. Subsequently, during the period of the Great Depression, in the midst of the most acute banking crisis and the massive bankruptcies of banks and other savings institutions, a unified deposit insurance system was created in the United States. For deposit insurance in commercial and savings banks, the Federal Deposit Insurance Corporation (FDIC) was founded, for deposit insurance of individuals in specialized savings institutions, the Federal Deposit Insurance Corporation in loan and savings associations (which was merged with the FDIC in 1989), for credit unions deposit insurance other funds and insurance companies operate.

Currently, the FDIC is an independent federal agency reporting to Congress, and banks and other credit organizations are not eligible to participate in the management of the system. The Federal Deposit Insurance

Corporation insures all deposit products, including current and savings accounts, deposit accounts, and certificates of deposit. The sum insured up to 250 thousand US dollars is calculated separately for each category of accounts owned by the client. The funds of individuals and corporate clients are subject to insurance. (Urazova, 2017) Until 1995, the USA was the only country that used contribution rates differentiated by degree of risk. Since then, the number of countries applying differentiated contribution rates has increased significantly (Republic of Kazakhstan, Argentina, Canada, Finland, Hungary, Italy, Sweden, Taiwan, Turkey, etc.)

Currently, the US deposit protection system is universal by the mid-90s. The FDIC insurance system covered up to 98% of all deposits, representing over 99% of the country's assets. A historical retrospective has shown that this particular model of deposit insurance turned out to be the most effective organization for protecting deposits of the population, and therefore was used in banking practice in many countries of the world.

The second model of the deposit insurance system operates in Germany and a number of its characteristics are also used in other countries of continental Europe (Austria, Switzerland, the Netherlands, and in part France). Deposit insurance is organized here by the banks themselves through their industry associations without the direct participation of the state, although with its indirect assistance. In Germany, the corresponding insurance funds are formed from formally voluntary contributions from banks and other savings institutions, but their sizes are small, and banks' contributions amount to about 0.03% of deposit balances per year. However, banks and savings institutions commit themselves to making additional contributions if necessary.

There are currently three insurance systems in Germany created by private banks, savings institutions and cooperative banks. All of these systems are voluntary and funded by participating banks. Deposit insurance is carried out by nine specialized organizations. Each of the three main banking groups in Germany has its own deposit insurance system. The funds of individuals and corporate clients are subject to insurance. Insurance indemnity is provided in the amount of up to 100 thousand euros, but in some cases the indemnity increases to 500 thousand euros.

It is believed that the advantages of continental deposit insurance systems are their independence from state policy, voluntary participation of banks, a minimum of formalism and red tape. (Table) In the period after the Second World War, the savings systems of Western Europe functioned satisfactorily and without losses for investors, which to some extent is associated with the competent organization of the deposit insurance system.

The intensification of the spread of the practice of developing deposit insurance systems in various countries led to the creation of the International Association of Deposit Insurers (IASD) in May 2002. The “Guidelines for Effective Deposit Insurance Systems” developed by the Association are applied in various countries and are used by the International Monetary Fund and the World Bank as part of the Financial Sector Assessment Program to determine the effectiveness of deposit insurance systems.

The Islamic deposit insurance system, created in Bahrain in 1993, can be considered a special model. This system provides for fundraising to reimburse affected bank depositors only after recognition of the fact of bankruptcy. Later, a system of insurance of Islamic deposits was created, involving the preliminary formation of a fund of funds necessary for deposit insurance (Sudan, Turkey, Malaysia). The difference from traditional deposit insurance is that insurance premiums received from Islamic banks are accounted for separately from the traditional cash desk and are invested only in accordance with Sharia principles, in the event of a bankruptcy of a financial institution for Islamic deposits, payment priorities exist for various accounts.

(Kalieva, 2010) In 2007, the Islamic Deposit Insurance Group (IDIG) was established under the auspices of the Research Committee of the International Association of Deposit Insurers.

During the global financial crisis of 2008, deposit insurance has become even more common in world practice. According to the International Association of Insurers, in 2016, deposit insurance was carried out in 125 countries and another 34 countries were in the process of creating similar systems. For comparison: in 1974, deposit insurance was valid in 12 countries. The overwhelming majority of organizations that manage deposit insurance systems are created by governments and are under their control, the second largest number are organizations introduced by the government legislatively, but managed by private companies. At the same time, the number of organizations managed by central banks is growing.

A special stage in the development of deposit insurance systems was the creation of integration associations in the world, within the framework of which many national practices began to be coordinated. First, European national deposit insurance systems began to operate - in Norway since 1921, in Finland and Czechoslovakia since 1924, and subsequently this process began to become widespread. Since the 70s, when a common economic space began to take shape in Europe, one of the aspects of integration was the extension of the practice of guaranteeing deposits of individual European countries - EU members and to other countries of the Community.

By 1990, national deposit insurance systems (DIS) had been established in all countries of the European Union (EU). A study of deposit insurance systems in the EU countries shows that in some of them the American model with strong state regulation and the presence of a state deposit insurance fund is taken as a basis. In other countries, such as Germany, Italy, Austria, Belgium, France, and others, several deposit insurance systems operate simultaneously, both private and private, with state support.

In 1994, the European Parliament adopted the “EU Directives on Deposit Guarantee Systems”, which prescribed the obligation for the presence of DIS in each country of the Union and the participation of all banks in it. The EU directives determined the types of guaranteed deposits, the terms for the payment of reimbursements, a phased increase in deposit guarantee limits (in 1994 no more than 20 thousand euros, from 2009 no less than 50 thousand euros). Currently, in most EU countries the guaranteed contribution is 100 thousand euros. It was envisaged to extend the protection to deposits in branches of foreign banks if the parent bank is registered in another EU country. At the same time, there were no strict restrictions on the choice of a financing system and the use of funds from guarantee funds for depositors.

Currently, the EU countries, in order to bring their DIS closer together, which have significant differences in governing bodies, the procedure for forming guarantee funds, the borders and conditions of compensation, etc. At this stage of integration, reinsurance and co-insurance mechanisms between the EU member states are used to ensure the stability of national deposit guarantee systems and make the transition to a single European DIS. As a result of the creation of a unified deposit insurance system, centralization of the funds of deposit guarantee funds will be centralized at the European level and a unified insurance cover will be provided for depositors throughout the EU.

In the countries of the former Soviet Union, such a long history of the existence of deposit insurance systems did not exist, and similar mechanisms to protect the stability of the banking market began to appear relatively recently. Currently, nationwide deposit insurance systems have been created in the countries of the Eurasian Economic Union (EAEU): in the Republic of Belarus in 1995, in the Republic of Kazakhstan in 2000, in the Russian Federation and the Republic of Armenia in 2003, in the Republic of Kyrgyzstan in 2008 year.

The EAEU member countries have created almost identical mandatory state deposit insurance systems (the so-called American model), there are unified institutions that ensure the formation and use of bank deposit guarantee funds. At the same time, there are certain differences in the conditions of deposit insurance in the member countries of this integration association. The identity of national deposit insurance systems in the EAEU countries will greatly facilitate the integration of these systems in order to create a single banking space and protect the interests of depositors of banks in these countries.

The deposit guarantee system created in the Republic of Kazakhstan ensures the protection of deposits and their guaranteed return (including deposit remuneration) in the event of bank bankruptcy. The deposit guarantee system in Kazakhstan is mandatory; it includes all second-tier banks licensed to accept deposits, open and maintain bank accounts of individuals, including individual entrepreneurs. The central element of the deposit guarantee system in the country is the Kazakhstan Deposit Guarantee Fund, the founder and sole shareholder of which is the National Bank of the Republic of Kazakhstan. The formation of the funds of the deposit guarantee fund is carried out at the expense of deductions of commercial banks, differentiated depending on the risk of their operations. If there is a lack of funds for the full payment of deposits, the state often provides temporary financial support on the terms of the mandatory repayment of funds issued.

Discussion

The study of world experience in deposit insurance has revealed the features of its functioning in the practice of various countries. Foreign best practices in organizing deposit insurance systems require critical reflection and subsequent application in practice of the Republic of Kazakhstan.

The system of guaranteeing deposits operating in Kazakhstan complies with all the principles proclaimed by the International Association of Deposit Insurers. Nevertheless, we consider it appropriate to make a number of changes to the conditions for organizing and conducting deposit insurance:

- To recognize subjects of the deposit insurance system along with second-tier banks and non-bank financial institutions, the list of operations of which includes attracting deposits of individuals. In world practice, two different approaches are used with respect to insurance of non-bank organizations: either they are included in the national deposit insurance system, or separate funds or insurance organizations are created for them. In order to ensure the stability of the deposit market in the Republic of Kazakhstan, it makes sense to include non-banking organizations in a single deposit guarantee system.

- Extend insurance liability to deposits of not only individuals and individual entrepreneurs, but, according to the experience of other countries, guarantee deposits to legal entities, including institutional investors, whose funds are also modified deposits of the population (for example, in pension deposits and insurance payments for accumulative types of insurance). The experience of the Russian Federation, where the phased introduction of deposit insurance of legal entities is carried out, is indicative. At the first stage, insurance liability was extended to small enterprises (with the exception of individual entrepreneurs whose deposits were already insured), and at subsequent stages, medium and large enterprises will be provided with insurance cover. The introduction of legal entities deposit insurance will help increase the confidence of this category of customers in Kazakhstan banks and will lead to an increase in the deposit base.

- To carry out a gradual increase in the size of the maximum security for guaranteed deposits. Currently, in the post-Soviet space, Kazakhstan provides its citizens with one of the highest levels of insurance coverage for deposits (about 40 thousand US dollars). As world experience shows, in most developed countries insurance limits are set at a higher level, and there are also examples of countries where deposits are guaranteed in full (UAE, Austria, Greece, Belarus). Raising the limits of insurance coverage in Kazakhstan will provide protection to large private capital, and subsequently to the capital of institutional investors.

- Change the method of financing the deposit guarantee system. So, in accordance with the documents of the International Association of Deposit Insurers (IASB), there are three possible methods of financing the deposit insurance system: advance, ex-post and hybrid (combined). In the practice of the Republic of Kazakhstan, a combined method for the formation of a deposit guarantee fund is defined by law, which combines elements of advance financing and ex-post financing. This method provides for credit organizations to pay advance insurance contributions (advance financing) and, in addition, it is expected to receive funds from participants in deposit insurance after the fact - as special charges (additional and emergency) in the event of an unfavorable situation in the banking market. As a result of this, all extraordinary risks are completely transferred from the insurer to other participants of the deposit insurance system (banks).

We consider it expedient to introduce into practice the advance method of forming a deposit guarantee fund in Kazakhstan, which does not provide for the payment of additional and extraordinary contributions by banks in case of insufficient funds for the target reserve to fulfill obligations to investors. This will reduce the financial burden on participants in the deposit insurance system during periods unfavorable for them and will not contribute to the onset of a systemic crisis. In the event that the funds of the formed trust reserves are insufficient to fulfill the obligations on guaranteed deposits, we consider it possible to use the reinsurance mechanism as is assumed in traditional insurance, as well as to attract state sources of financing.

Conclusion

As a result of a retrospective study of world experience in building deposit insurance systems, it can be assumed that the following directions of development of the world deposit guarantee practice will be: ubiquitous creation of deposit insurance systems in various countries of the world as the most important factor in maintaining the financial stability of the state banking market; the functioning of cross-border insurance systems that ensure the free movement of capital across the territory of the member countries of the integration association; the emergence of superstructure deposit protection systems within the framework of integration associations in order to coordinate national deposit insurance systems and unify the insurance coverage of depositors in the territory of the participating countries.

The study of world experience in the organization of deposit insurance systems and the identified prospects for its development made it possible to formulate certain conclusions and proposals in order to improve the practice of deposit insurance in the Republic of Kazakhstan. So, according to the experience of foreign countries, it is necessary to gradually extend the practice of deposit insurance to both bank and nonbank credit organizations; extending insurance liability to operations to attract deposits of legal entities; gradual increase in maximum security for guaranteed deposits; application of the advance method of forming a deposit guarantee fund.

As a hypothesis of this study, the assumption was made that, world experience in building deposit insurance systems will allow to organize the most optimal deposit guarantee system in the Republic of Kazakhstan. The formulated conclusions and suggestions confirm this hypothesis, since the most advanced ideas in organizing protection systems for deposits of citizens are introduced into the practice of the domestic banking market. Moreover, examples of other national practices make it possible to use their experience to optimize further the deposit guarantee system in the Republic of Kazakhstan.

The practical significance of the results of the study lies in the fact that the proposals developed can be used by the state supervisory authority for regulation and development of the financial market of the Republic of Kazakhstan to amend domestic legislation governing the organization of the deposit insurance system in order to further improve it.

References

- Beck, T. (2001). Deposit Insurance as Private Club: Is Germany a Model? Retrieved from https://openknowledge.worldbank.org/bitstream/handle/10986/19705/

- Boyle, G., Stover, R., Tiwana, A. et al. (2015). The Impact of Deposit Insurance on Depositor Behavior During a Crisis: A Conjoint Analysis Approach. Retrieved from https://doi.org/10.1016/jjfi.2015.02.001

- Demirgug-Kunt, A., Kane E., Laeven, L. (2015). Deposit Insurance around the World: A Comprehensive Analysis and Database. Retrieved from https://doi.org/10.1016/jjfs.2015.08.005

- Directive 94/19/ЕС of the European Parliament and of the Council of 16 May: federal law. Approved May 16, 1994.

- Retrieved from http://eur-lex.europa.eu/LexUriServ /LexUriServ. do?uri=CELEX:31994L0019:EN:HTML Directive 97/9 / EC of the European Parliament and of the Council of 03.03.1997 on compensation schemes for investors. Retrieved from http://base.garant.ru/70256774/?_utl_t=vk

- Directive 2009/14 / EC of March 11, 2009. Retrieved from http://base.garant.ru/2568238/

- Directive 2014/49 / EU of the European Parliament and of the Council of 04.16.2014 “On deposit guarantee systems” Retrieved from https://www.asv.org.ru/documents_analytik/analytics/international / 32943512.

- Colaert, V. (2015). Deposit Guarantee Schemes in Europe: Is the Banking Union in need of a third pillar? European Company and Financial Law Review, 12(3), 372-424.

- Colaert, V. (2015). European banking, securities, and insurance law: Cutting through sectoral lines? Common Market Law Review, 52 (6), 1579-1616.

- Commission Recommendation of December 1986 concerning the introduction of deposit-guarantee schemes in the Community. Official Journal, no L033, 04 February, 1987. - Р.16-17. Retrieved from

- https://publications.europa.eu/en/publication detail/-/publication/7945b0b1-2e99-4f46-bc98-e2c4fd9032c1/ lan- guage-en

- Chudinovskih, M.V. (2017). Sistema zaschityi prav vkladchikov v stranah Evraziyskogo ekonomicheskogo soyuza: sravnitelno-pravovoy analiz [The system of protecting the rights of depositors in the countries of the Eurasian Economic Union: comparative legal analysis]. Finansovoe pravo i upravlenie [Financial Law and Management], 4, 48 - 55.

- Garcia, Gillian G.H. (1999). Deposit Insurance: A Survey of Actual and Best Practices. Retrieved from https://www. imf.org/external/pubs/ft/wp/1999/wp9954.pdf

- Garcia, Gillian G.H. (2000). Deposit Insurance and Crisis Management. IMF Working Paper WP/00/57. March 2000. Retrieved from https://www.imf. org/external/pubs/ft/wp/2000/wp0057.pdf

- History of the FDIC. Historical Timeline (2017). Retrieved from https://www.fdic.gov/about/ histo- ry/timeline/index.html

- Kalieva, Zh. (2010). Kogda dengi zhivut po zakonam shariata [When money lives according to Sharia law]. Delovaya gazeta "Vzglyad" [Business newspaper "Vzglyad"], 42 (178), 5-6.

- Research & Analysis of Federal Deposit Insurance Corporation (2017). Retrieved from https:// www.fdic.gov/bank/statistical/stats /

- Snell, J. (2017). Risk sharing in the Eurozone: not just high politics. European Law Abstract, 6, 791-792.

- Sembekov, A.K., Budeshov, E.G., Tingisheva, A.M. (2017). Opit formirovaniya Evropeiskogo strahovogo rinka [Experience in the formation of the European insurance market.] Vestnik Karagandinskogo universiteta Seriya «Ekonomika». [Bulletin of the Karaganda University Series "Economics"], 3 (87), 224-230.

- Urazova, S.A. (2017). Sistemyi strahovaniya depozitov: zarubezhnyiy opyit i perspektivyi razvitiya v Rossii [Deposit insurance systems: foreign experience and development prospects in Russia]. Finansyi i kredit [Finance and Credit], 23(41), 2438 - 2455.

- Zemtsov, A.A., Tsibulnikova, V.Yu. (2017). Analiz etapov razvitiya Federalnoy korporatsii po strahovaniyu vkladov SShA [Analysis of the stages of development of the US Federal Deposit Insurance Corporation]. Fundamentalnyie issledovaniya. [Fundamental research], 4-2, 344-350.