Abstract

Object: The analysis of financial position indicators and the selection of more optimal ones for effective management decision making is a significant task for the formation of a financial stability strategy influenced by financial planning indicators. This article sets the purpose of analyzing the impact of financial planning on financial stability on the example of oil and gas industry.

Methods: We wrote this article using the following methods: economic and statistical, abstract and logical, monographic, economic comparison, methods of system analysis.

Findings: Findings and conclusions given in the article can be used for the financial planning development and implementation. The analysis on XXX JSC material considering a logarithmic function has helped us to identify forecast for the development of financial planning and conditions of both internal and external environment. Also based on regression analysis we have given corresponding proposals and conclusions.

Conclusions: Using statistical data based on XXX JSC's financial indicators, we have analyzed the influence of some factors - such as the current liquidity ratio, income from sales of products and services—on the final profit by constructing a regression model.

Introduction

The relevance of the research is that in the context of globalization and digitalization of the economy and situation on the market changing rapidly—also on an international level—companies need to use innovative methods in their management and technological process. The emphasis is on business processes, which should not just improve methods and form of management, but also constantly transform and react flexibly to changes in the company's development strategy. All actions encourage and motivate companies to improve their business processes. Company managers should seek out and apply different and effective methods of business process management. In this regard, the research topic appears highly relevant and significant at the present stage.

The company should detect various factors of instability in time, plan both short and long-term tasks to improve financial stability. This calls for rethinking some of the company's financial management methods and adoption of methods able to improve planning and financial sustainability.

In modern conditions, the problem of managing the company's financial stability appears to be one of the most urgent ones. Very low financial stability may cause the company to fail to discharge its obligations and debts, and the lack of funds for production development (logistical support expansion, investment). Excess sources of own working capital can hinder development by burdening the company's expenses with excess reserves and stocks.

Financial planning and forecasting allow the company to resolve main tasks of ensuring its financial stability:

- coordinate the company's need for investment with the availability of financial sources;

- compare and evaluate various scenarios of the company's financial development and select the most optimal ones accordingly;

- consider the development of various trends in the company's activities;

- create a timely anti-crisis action plan in case negative events take place;

- harmonize various objectives, often contradictory ones;

- allocate resources more effectively and thus strengthen control in the company.

The process of financial planning and its stages are closely interrelated and mutually dependent. To clarify financial tasks, we do not just recalculate natural data into cost data; we determine the effectiveness of certain costs and choose rational forms of income concentration and distribution based on reasonability and accurate results (Allen, Wood, 2006).

Literature Review

The company's activity cannot proceed effectively without the use of current financial management methods. One of the key ways to increase financial management effectiveness is to improve financial planning, forecasting and control. In this regard, “financial planning” appears to be an important concept.

Financial planning stands as planning of all income and expenditure of funds to ensure the company's development (Lambekova, Nurgalieva, 2017). The main objectives of this process are a specific correspondence between the need and availability of effective financial resources and selection of effective sources of creating financial resources and mutually beneficial options for their use (Shakar, 2008).

F. Delmar and S. Shane interpret financial planning as a preliminary activity that plays a central role in planning the start of the process (Delmar, Shane 2003). R.H. Garrison believes that planning involves setting objectives and specifying how to achieve them (Garrison, Noreen, Brewer,2011).

In financial management literature, J. Brinckmann shows that financial planning and control help, first, to ensure a rational and targeted financial resources distribution and, second, to evaluate its effective and efficient use (Brinckmann, Salomo, Gemuenden, 2011).

Baker, H. Kent and Ricciardi, Victor describes the security of financial interests at all levels of financial relations, the level of stability, independence and endurance of the state's financial system under the influence of various external and internal factors, and the ability of the state's financial system to ensure the effective functioning of the national economic system (Baker, Ricciardi, 2015).

In her publications, Ma, C. proves that financial stability lies in national interests represented by a set of plans implemented by the state through tax, budget, monetary and investment policies (Ma,2019).

Taskinsoy, John, explains financial stability in the industry due to food security (Taskinsoy, 2020).

Festa, G., Rossi, M., Kolte, A. and Marinelli, L. in terms of existing definitions of financial stability, emphasizes its role and fundamental importance for creating the structure and level of assessment of the company's potential for development. Here he considers such concepts of elements as financial activities, operations and risks associated with financial activities (Festa, Rossi, Kolte, Marinelli 2020).

Keister, T. associate financial stability with the overall financial structure of the company and the degree of its relationship between creditors and investors (Keister, 2016). For the accuracy of the assessment, we need to analyze the structure of funding sources.

Methods

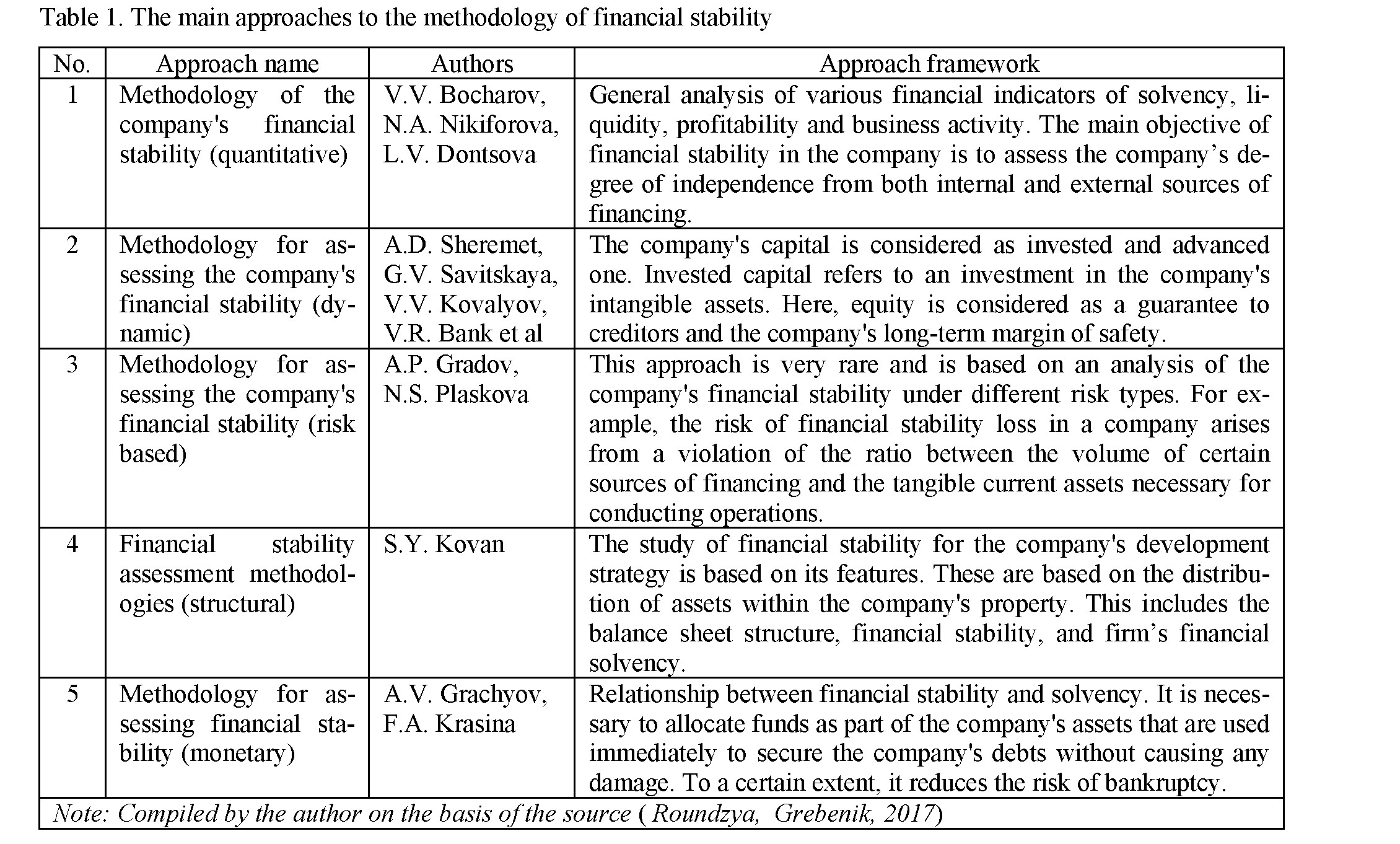

Financial stability is a system that includes a set of different elements, based on differentiation and indicators allocated to assess its state, and providing conditions for sustainable development of the company.

By now, many researchers have proposed various approaches to the methodology of financial stability to justify the company's development strategy (Roundzya, Grebenik, 2017).

Results

We shall build an econometric model based on the data we've collected using the Gretl software.

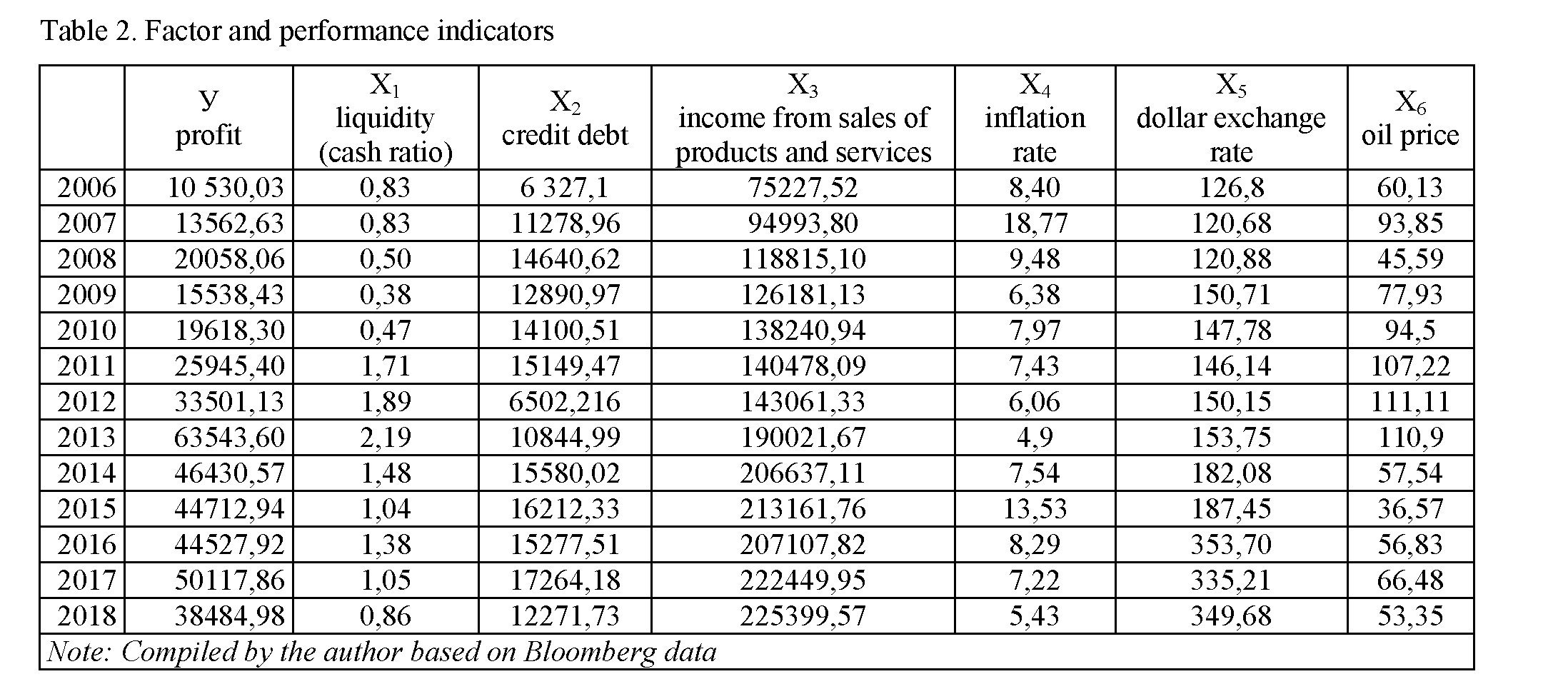

As an example of our research, we shall consider the model of profit's dependence in billion tenge on the following predictors: liquidity, credit debt, income from sales of products and services, inflation level, dollar exchange rate, oil price for 13 years. Due to the fact that the company's data is restricted for public disclosure we have renamed the company's name to XXX JSC.

To give the model more sense, let us check our predictors for multicollinearity. We have checked multicollinearity using the correlation matrix in Microsoft Excel software and using multicollinearity in the Gretl software package itself.

The minimum possible value of the inflationary factor method is 1.0. Values >10.0 indicate multicollinearity. x1liquidity = 2,733; x2creditdebt = 2,243; x3incomefromsalesofproducts = 6,216; x4inflationrate = 1,360; x5dollarrate = 3,011; x6oilprice = 2,098.

We see no multicollinearity between regressors. It is not bad, but despite this, only the following independent variables will take part in the model construction: X1, X3, X4, X5. Oddly enough, when constructing the correlation matrix, the “oil price” indicator did not show a connection with the effective feature; it was equal to (-0.05). Moreover, connection also proved to be reverse.

The greatest correlation has been observed for indicators X1 and X3. We can state these indicators as main ones that require almost constant monitoring since current liquidity is the indicator by which the company's solvency is judged.

The coefficient shows the ability to meet current obligations at the expense of the company's current assets only. The higher this indicator, the better the solvency (Liquidity. Calculation of liquidity ratios). Revenue from sales is the main source of cash and displays the company's performance. External indicators are also included in the model. These are the dollar exchange rate and the consumer price index (inflation rate). In the global business market, these indicators are treated as important and significant as well. So far, we have been reasoning based on the tightness of the relationship shown by the correlation matrix, but whether these indicators are significant in the equation itself, we shall observe by building an equation model (a regression).

We have built the model using econometric modeling software package Gretl.

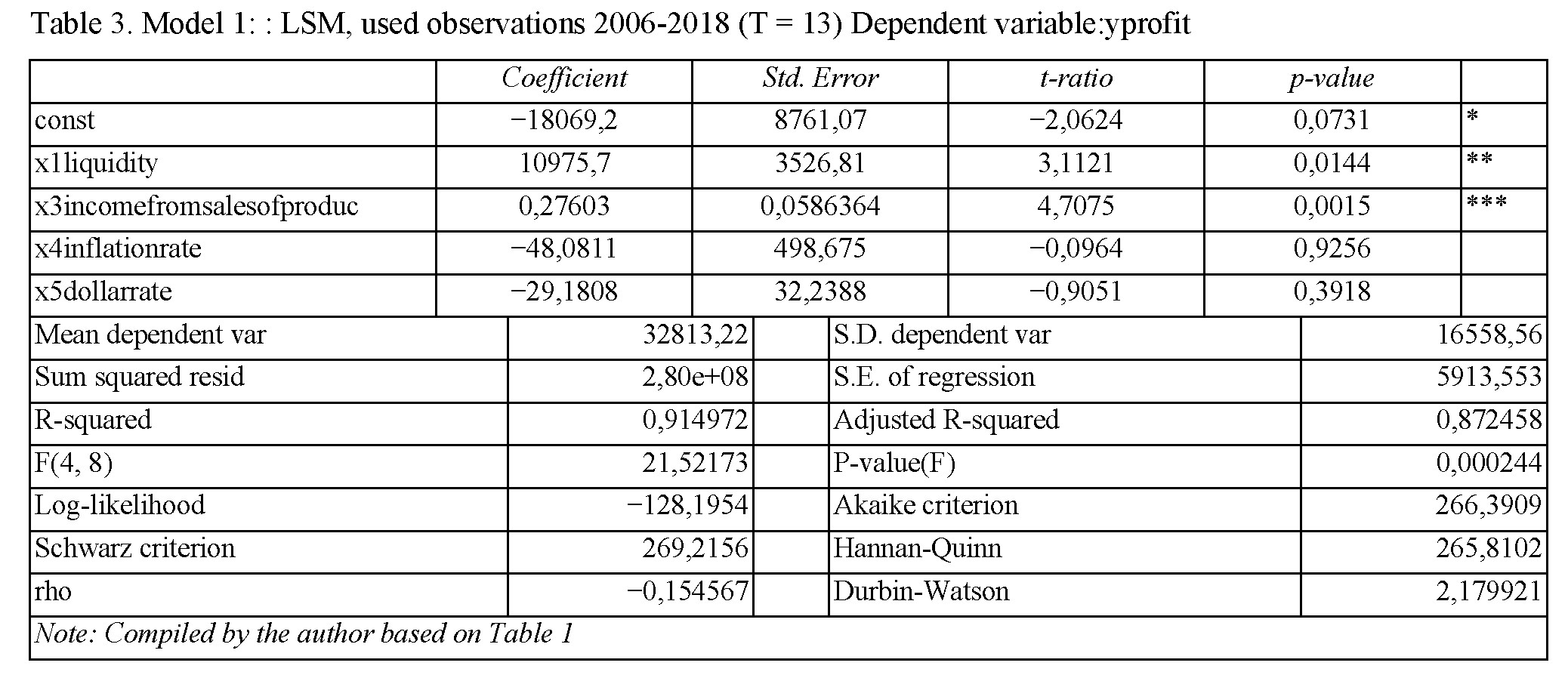

As we mentioned earlier, internal indicators X1 and X3 will be significant for the model.

We observe this based on the p-value, i.e. we accept the alternative hypothesis and reject the null hypothesis for the first and third predictors. In other words, the p-value for the alternative hypothesis is <0.05. Indicators of external factors have accepted the null hypothesis. Based on the calculated data we leave the financial indicators as they are and build another model but without X4 (inflation rate) and X5 (dollar exchange rate).

|

Coefficient |

Std. Error |

t-ratio |

p-value |

|||

|

const |

-18661,4 |

5498,41 |

-3,3940 |

0,0068 |

*** |

|

|

x1 liquidity |

12131 |

2995,83 |

4,0493 |

0,0023 |

*** |

|

|

x3 incomefromsalesofproduc |

0,234057 |

0,0331862 |

7,0528 ~ |

<0,0001 |

*** |

|

|

Mean dependent var |

32813,22 |

S.D. dependent var |

16558,56 |

|||

|

Sum squared resid |

3,08e+08 |

S.E. of regression |

5553,974 |

|||

|

R-squared |

0,906248 |

Adjusted R-squared |

0,887497 |

|||

Table 4. Model 2: LSM, used observations 2006-2018 (T = 13) Dependent variable: yprofit

ECONOMY Series. № 3(99)/2020

137

Let us outline the resulting equation model:

|

F(4, 8) |

48,33207 |

P-value(F) |

7,24e-06 |

|

|

Log-likelihood |

-128,8303 |

Akaike criterion |

263,6607 |

|

|

Schwarz criterion |

265,3555 |

Hannan-Quinn |

263,3123 |

|

|

rho |

-0,220343 |

Durbin-Watson |

2,262707 |

|

|

Note: Compiled by the author based on Table 1 |

||||

У = -18661,4+12131,0 X1 +0,2341 X2

The resulting model itself—without checking for various tests, that is—does not tell us anything yet. Based on this, let us test our resulting model for adequacy and significance.

Model's significance hypothesis as a whole

- H0: All model parameters except the constant are equal to each other and are equal to zero. The model as a whole insignificant.

- H1: All model parameters except the constant are not equal to each other and are not equal to zero. The model as a whole is significant.

- P-value (F) = 0.007 <0.05. Therefore, the null hypothesis is rejected in favor of the alternative with a 95% probability, meaning the model as a whole is significant.

Evaluating the model quality based on graphs

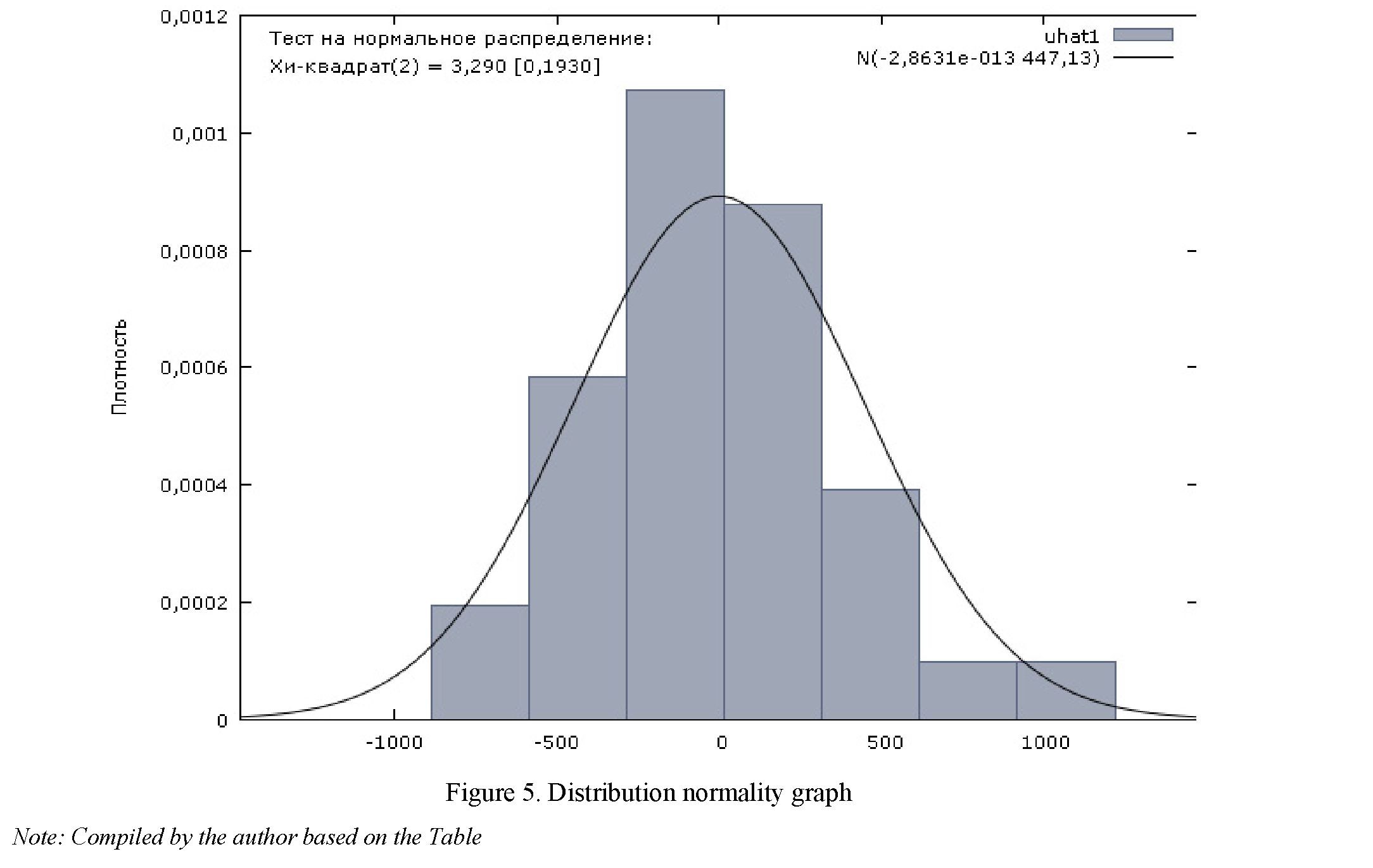

Let us also perform the normality of residuals test, i.e. normal (Gaussian) distribution of a feature in the sample

The normality of the distribution test has shown that the probability of the sample we studied satisfies the normal distribution law.

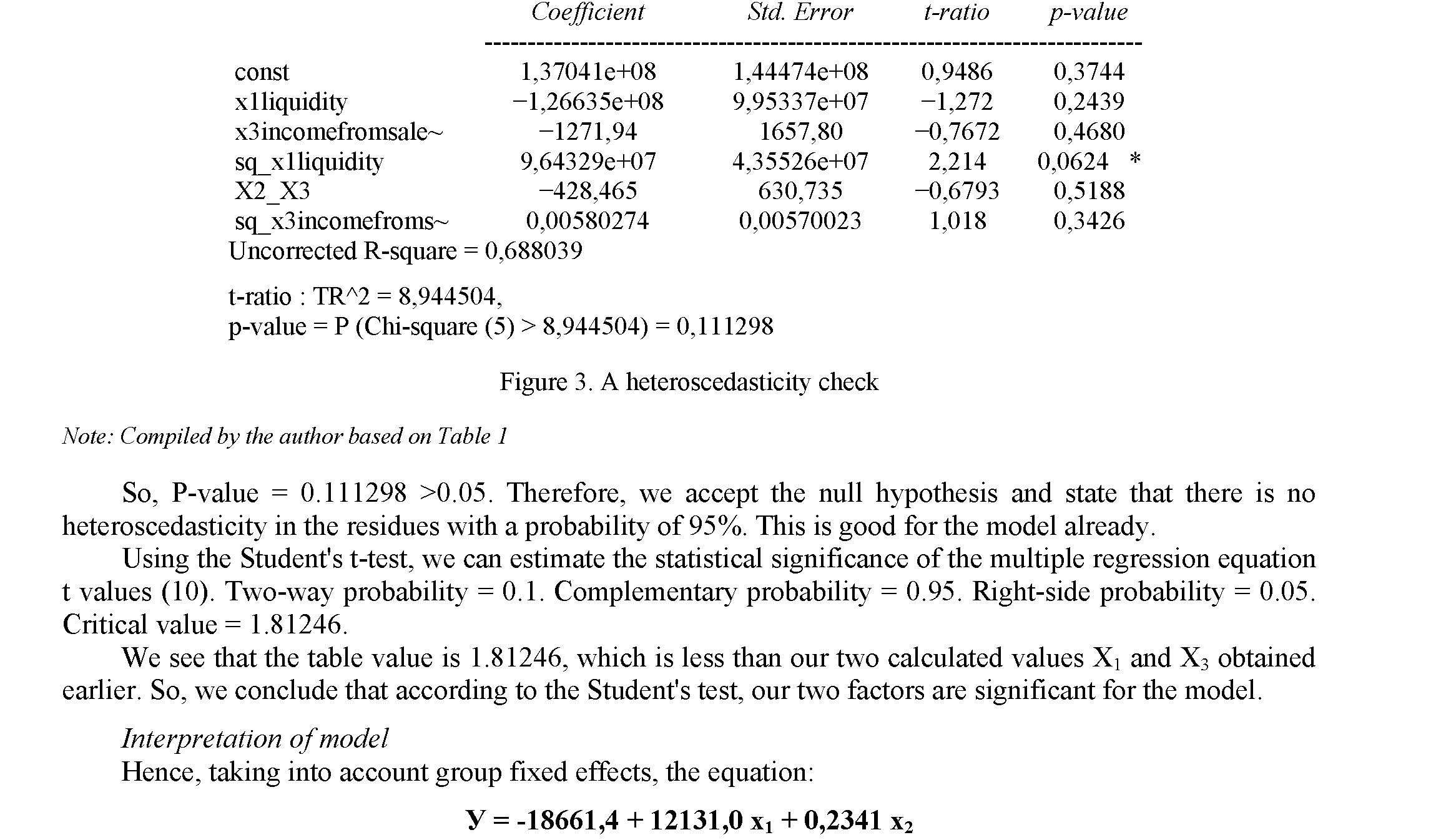

Tests for heteroscedasticity

The heteroscedasticity of regression models indicates that estimates will be ineffective. In other words, the phenomenon of heteroscedasticity shows the inadequacy of the statistical results of the research (White's

139

Test). For the White test for heteroscedasticity and MLS, we used observations for the period of 2006— 2018. (T = 13). Dependent variable: uhat^2.

is valid.

With an increase in the solvency index by 1 million tenge, the profit shall increase by 12 million tenge, and with an increase in revenue by 1 million tenge, the profit shall increase by 234 thousand tenge.

We conclude that “XXX” JSC effectively manages working capital. They can also optimize current liquidity by increasing the share of profit, and to increase current liquidity, they need to ensure the profitability of the company's activities and its growth. Having analyzed our research, we can say that financial indicators such as liquidity and revenue have a direct and close relationship with the company's profit. This is also indicated by the coefficient of determination equal to 0.91, that is, our financial indicators describe the resulting model by 91%.

Conclusion

A clear and accurate assessment of the financial situation stability will help determine the level of financial resources' effective use, determine the direction of future development or financial recovery, clearly assess financial opportunities, and maximize the internal financial potential. Such an accurate and optimal analysis will help the company identify problems arising as a result of the rapid change of any factors and possible sources of new investment projects.

Financial stability is the final indicator that determines the company's financial condition. Successfully management of financial stability requires an ability to make effective management decisions and soberly assess financial stability. Effective financial management means the ability to correctly, effectively and profitably use modern ideas.

Assessing the stability of the financial position allows the manager to determine the activity direction. Although there is no common definition of financial stability, this is the final indicator that determines the financial condition of an economic entity as a whole.

Successfully management of financial stability requires an ability to effectively choose methods for managing and evaluating financial stability. Thus, in our opinion, financial stability is the ability of a compa-

ECONOMY Series. № 3(99)/2020

ny to successfully operate in a constantly changing market environment while maintaining a stable solvency and investment attractiveness by establishing a stable balance sheet (Krysovaty, Fedosov, Ryazanov, 2013).

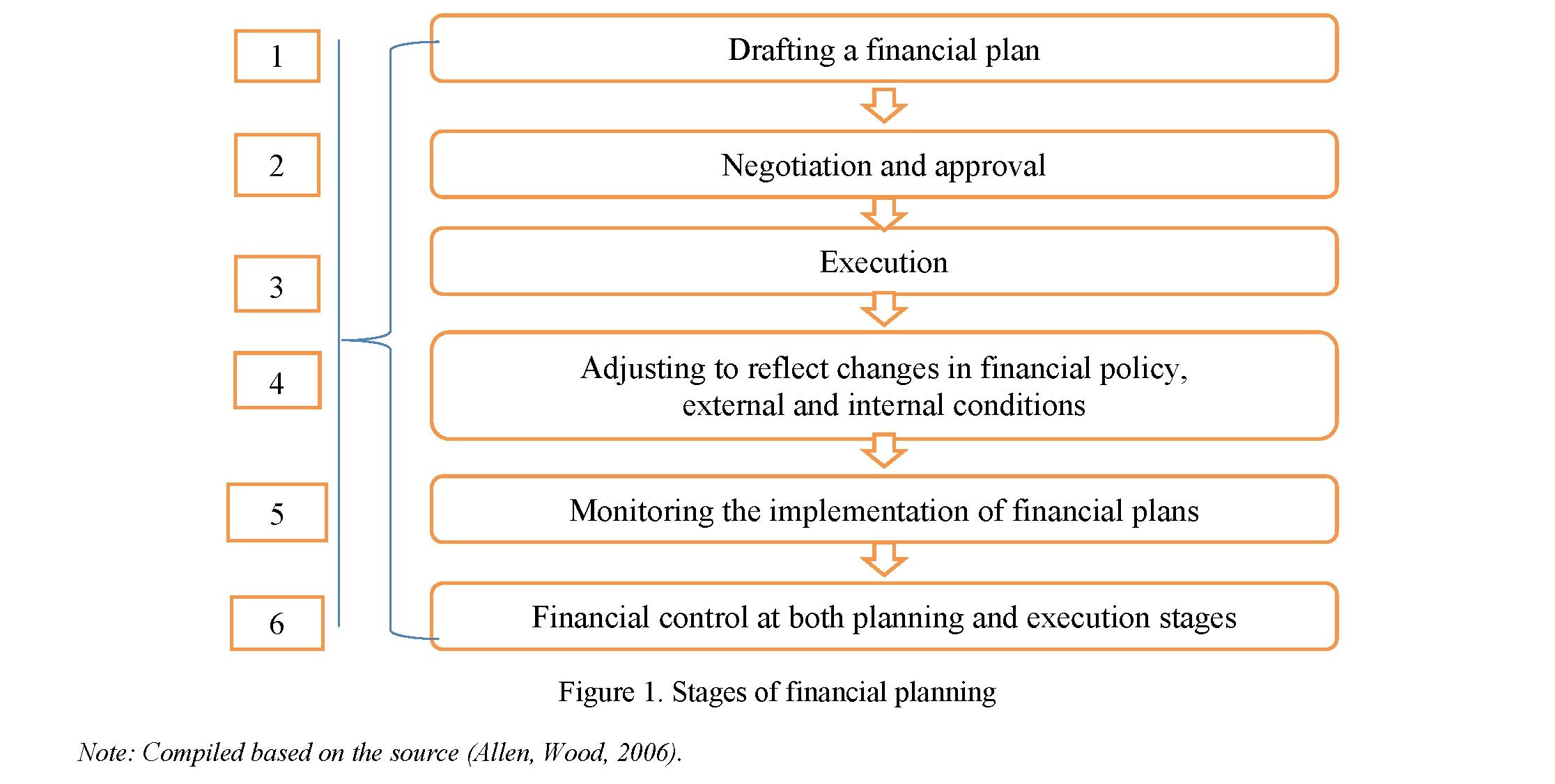

Planning shows a general analysis of social and economic development plan of a particular object in the economy. Financial planning is considered in assessing the impact of factors of company's both external and internal capabilities.

The first step is to review the company's capabilities, competitors' market position, and the terms of service.

At the second stage, company defines its main tasks as a whole. After that, for further work for each of its divisions, company sets the exact time period for the implementation of these capabilities.

At the third stage, the company takes a set of actions necessary to complete specific tasks. This set is formed taking into account various internal and external conditions of the company.

In the fourth stage, the company needs to develop a clear plan based on forecasts and research. Comprehensive economic analysis is closely related to planning and forecasting activities. It is a means of justifying plans and monitoring their implementation. The manager must select specific special alternatives.

At the final stage, the approved plan is to be implemented. If necessary, the manager can make changes or add to the financial plan. Financial planning plays a big role in promotion. Competent financial planning positively affects the company's financial stability.

References

- Allen, W. A., & Wood, G. (2006). Defining and achieving financial stability. Journal of Financial Stability, 2(2), 152– 172. doi:10.1016/j.jfs.2005.10.001

- Brinckmann, J., Salomo, S. & Gemuenden, H.G. (2011). «Financial management competence of founding teams and growth of new technology-based firms», Entrepreneurship: Theory & Practice, 35, 2, 217–243.

- Baker, H. Kent and Ricciardi, Victor, (2015). Understanding Behavioral Aspects of Financial Planning and Investing. Journal of Financial Planning, 28, 3, 22–26,

- Festa, G., Rossi, M., Kolte, A. & Marinelli, L. (2020), «The contribution of intellectual capital to financial stability in Indian pharmaceutical companies», Journal of Intellectual Capital, Vol. ahead-of-print No. ahead-of-print. https://doi.org/10.1108/ЛC-03-2020-0091

- Garrison, R.H., Noreen, E.W. & Brewer, P.C. (2011). Managerial Accounting, McGraw-Hill/ Irwin, New York.

- Keister, T. (2016)/ Bailouts and financial fragility. Review of Economic Studies 83(2), 704–736.

- Krysovaty, A., Fedosov, V., & Ryazanov, N. (2013). Corporate finance in context of modern innovation calls of the economy [Corporate Finance in the context of modern innovative economy challenges]. Finance of Ukraine, 9, 7– 27.

- Lambekova, A.N., & Nurgalieva, A.M. (2017). «Halyq Bank» Aktsionerlik qogamynyn qarzhylyq turaqtylygyn taldau ishki audit zhuiesinin tiimdiligin arttyru quraly retinde [Analysis of financial stability of Halyk Bank joint-stock company as a tool for improving the effectiveness of the internal audit system]. Vestnik Karahandinskoho universiteta. Seriia Yekonomika — Bulletin of the Karaganda University. Economy Series, 2(86), 236–242.

- Liquidity. Calculation of liquidity ratios. audit-it.ru. Retrieved from https://www.audit- it.ru/finanaliz/terms/liquidity/calculation_of_liquidity.html

- Ma, C. (2019). Financial stability, growth and macroprudential policy. Journal of International Economics, 103259. doi:10.1016/j.jinteco.2019.103259

- Roundzya, N.A. & Grebenik, V.V. (2017). Theoretical aspects and problems of justifying the strategy of a financially unstable company. Naukovedenie, Vol. 9, No. 6, 9–10.

- Shakar, E. (2008). Financial Planning and Cashflow Management. Elan & Co With Advice and Case Studies. elantax.com. Retrieved from http://elantax.com/wp-content/uploads/2016/12/FinancialPlanningeBook.pdf

- Shane S and Delmar, F (2003). Does business planning facilitate the development of new ventures?», Strategic Management Journal, 24, 12, 1165–1185.

- Taskinsoy, John, (2020). Old and New Methods of Risk Measurements for Financial Stability Amid the Great Outbreak. ssrn.com. Retrieved from https://ssrn.com/abstract=3587150 or http://dx.doi.org/10.2139/ssrn.3587150

- White's Test. spravochnick.ru. Retrieved from https://spravochnick.ru/ekonometrika/test_uayta/