Abstract

Information technology is the study or use of systems for storing, retrieving, and sending information. This study is intends to evaluate the impact of information technology in the banking industry. Much than most opposite industries, financial institutions rely on processing, analysing, and provide services in order to cater for the needs of their customers and this is why banks in this modem world of science and technology use information technology in most of their activities or dealings. It is apparently clear that banks in these days cannot do without information technology. The article will attempt to find out the significance of information technologies in the banking sector, as well as consider the advantages and disadvantages of information technologies in the banking sector, their impact and recommendations that can reduce any harmful threat arising from its use. and the importance of information technologies in the banking sector. The article discusses such concepts as daily banking, digital office, financial platform and media bank, as well as analyzes the main trends in the development of mobile banks in Kazakhstan.

Introduction

Every year, the retail business in the banking sector is increasingly focusing on the development and continuous improvement of the quality of customer service. The maturity level of Kazakhstani bank applications is growing following the increased interest of customers in this service channel, as more and more users positively evaluate the capabilities of mobile applications.

In Kazakhstan, the first banking applications for smartphones appeared in 2011. Since then, many banks have been implementing an active policy of transferring customers to service via digital channels, and they can already see its first results: the use of remote service channels by customers has increased significantly, which has helped banks to increase profitability and reduce costs.

IT in banking has its benefits and problems.

Benefits of IT in banking:

Globalisation: Information Technology has brought the world closer and allowed for information to be shared easily, quickly and effectively. Allowing for transactions to be performed regardless of where an individual or business are located. Information Technology has broken down geographical boundaries making the global village so small.

Communication: Information Technology has made communication easier, quicker, cheaper and more efficient. People are now able to communicate with each other from anywhere around the world. For example through video conferencing, email, texting, instant messaging, social networking, radio on the go, television on the go, voice calls and VoIP.

Cost effectiveness and operational excellence: Automation of processes for individuals and businesses means our daily lives have been transformed. Our daily lives have been made so much easier and economically effective. Cost effectiveness gives rise to profits realised and better pay for employees. Making daily lives easier and less strenuous working conditions. Transactions are achieved in the less amount of time compared to the days before automation. Fewer errors are made by the use of IT.

Bridging the Cultural Gap: People from different nationalities and cultures are able to communicate amongst themselves and this allows for exchange of views and opinions, which could better their lives, increase awareness and decrease prejudice.

Longer Working Hours: Business hours are extended from the normal Monday to Friday and 8-5 working days. The business is virtually open 24 hours and 7 days a week. This applies to all businesses around the globe. The extended hours allows for business transactions to be conducted from anywhere and anytime of day. People are now allowed to purchase anytime and anywhere.

- Creation of New and Exciting Jobs in the Field of IT: Creation of new and Interestingjobs within the Information Technology field. For example, would have computer programmers, system administrators, system analysts, technical specialists of hardware and software, web development, computer engineering and network administration.

- Business Intelligence: IT in banking gives competitive lead amongst other rivals. Crucial and essential information obtained will be used in making strategic business decisions. Information attained from competitors, individuals, business environment, internal operations and business partners.

Problems of IT in banking:

Mobile banking customers are at great risk of receiving fake SMS messages and scams from hackers and scammers. The loss of a person’s mobile device often means that the customer’s information can be accessed unlawfully. Gaining access to customer’s mobile banking PIN and sensitive information. In order to have better experience with mobile banking customers need to have access to more Modem mobile devices such as Smartphone, PDA’s and tablets. There are various problems customers face when using mobile banking. The problems being:

- Security and Risk: Mobile customers are susceptible to scammers. A customer receives a fraudulent email or SMS from a sender posing as a bank or financial institution. Requesting for the customer to send their bank account details. If and when a mobile device is stolen the customer is at great risk. Most customers automatically set their devices to save their personal information leaving the customers vulnerable to scammers. Many customers of mobile banking are uncertain with issues such as loss and theft by hacking thus discouraging the customers to adopt mobile banking.

- Compatibility: Banks offer the mobile banking services to all customers, some customers are limited to the number of services offered as they do not have compatible devices. Thus, the customer is limited to several services only with the constraint of the type of mobile they have. Mobile applications designed can also be exclusively available to certain mobile phone brands.

- Cost: The cost of mobile banking occur if the customer does not have a compatible device, though if the customer does have a compatible device they may still incur data and text messaging costs. Extra costs for mobile banking service, for software.

- Scalability and Reliability: The banks need to ensure that mobile banking systems are working for customers to access the service from anywhere and anytime. There can be loss of customer confidence if mobile banking services are not met continuously.

- Application Distribution: Customers would expect that the mobile application would be updated, upgraded and downloads being available. On the other hand, there are numerous issues to ensure that the upgrade, update and downloads are implemented successfully.

As of July 1, 2016, only 15 of the 35 second-tier banks in Kazakhstan had their own mobile banking applications. With the help of mobile banking, by using mobile applications, a client can remotely access their accounts and carry out banking operations without visiting bank branches.

At the same time, customers are using an increasing number of different applications and are beginning to make increased demands on their banks. In the future, the number of such users and the volume of operations carried out by them using mobile applications will only grow in the future [1].

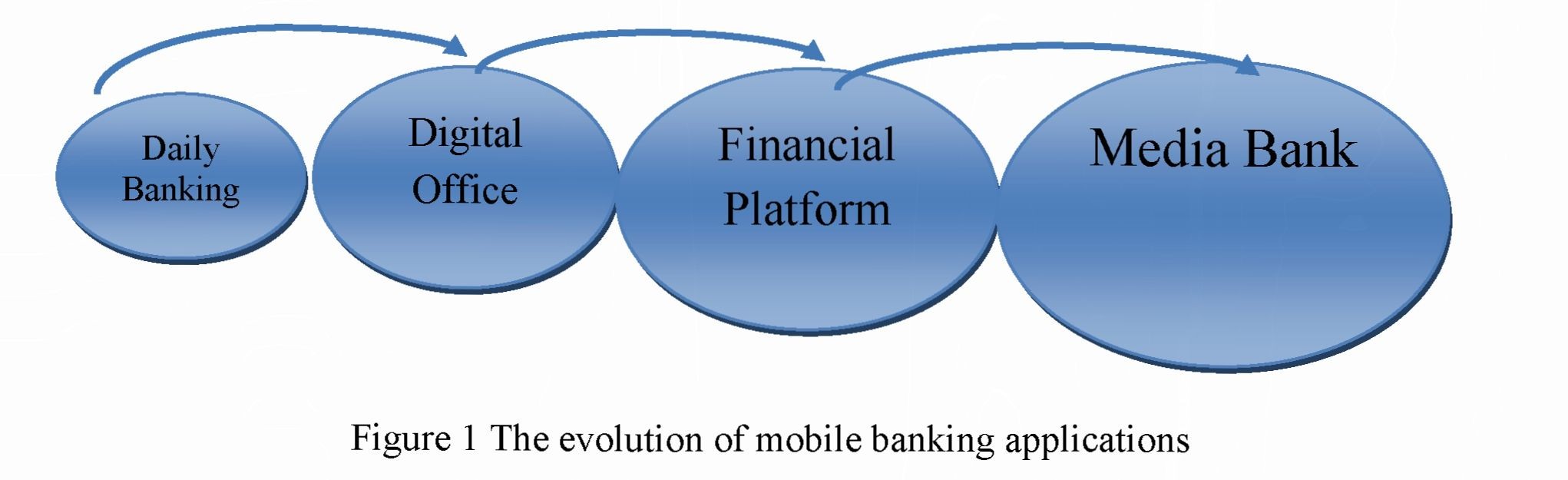

Daily Banking: Daily banking is all the tasks and needs of the client related to obtaining information about the product and performing payment and transfer operations using it. This is the concept of meeting the basic needs of the client, and it is relevant for any bank that is primarily engaged in the card business.

Daily banking is developing due to the emergence and improvement of various types of transfers and payments.

Sberbank, KaspiBank, Bank Center Credit and ATF Bank solve the customer's daily tasks in mobile banking better than others.

In the mobile applications of these banks, you can transfer money by various identifiers, find out about debts and create subscriptions, conveniently pay receipts and government payments.

Most applications have already implemented transfers by card number, phone number, between custom cards, adding funds to your card, and exotic transfer technologies are developing, such as QR - code transfers in KaspiBank. Debt requests and payment subscriptions have become widespread.

Digital Office: A digital office is a user-defined task that has historically been associated with visiting a bank's office. The concept of a digital office assumes that the customer eventually stops interacting with the bank offline: they can remotely open any product or refuse it, get advice and settle a claim, change settings and restore access, without calling the Bank or visiting its office once during the entire lifecycle.

The digital office is being developed through explosive sales of banking products.

Many applications have the opportunity to order a debit or credit card, apply for a cash loan or deposit. The CenterCredit Bank’s mobile application has the opportunity to open a current account in tenge or currency, open a deposit in KaspiBank, Bank CenterCredit and Home Credit Bank, open a debit card in Eurasian Bank, Sberbank and Center Credit Bank.

Many applications have the opportunity to order a debit or credit card, apply for a cash loan or deposit. The CenterCredit Bank’s mobile application has the opportunity to open a current account in tenge or currency, open a deposit in KaspiBank, Bank CenterCredit and Home Credit Bank, open a debit card in Eurasian Bank, Sberbank and Center Credit Bank.

The best digital office in a mobile bank was made by AltynBank, ForteBank and Sberbank.

In all three banks, you can remotely change the client’s personal data, open different banking products, reissue the card and order official documents. AltynBank is the only bank that fully identifies a customer remotely.

Financial platform: Turning the bank into a single window for gaining customer experience: it becomes an aggregator provider of not only financial but also non-financial services: KaspiBank and ForteBank - at the next stage in the development of digital banking. Over the past year and a half, four banks have the opportunity to change the PIN code (Eurasian Bank, HomeCredit Bank, AltynBank and KaspiBank) and configure the push notifications in three banks. Earlier these functions were not in any mobile bank of Kazakhstan. At the same time, everything related to changing personal data and uploading documents is still underdeveloped. In the KaspiBank and ForteBank mobile applications, commodity marketplaces are integrated where a client can remotely buy almost anything. KaspiBank actively uses macro play to promote its products: it allows payment only with a bank card and actively offers installment plans and consumer loans. ForteBank allows payment by any card and offers customers only one product - installment plan.

Media bank: The bank acts as an adviser, expert, consultant, which helps customers solve various consumer problems and tasks, offering him useful products and services. Moreover, not only in the process of solving the problem, but also long before its formulation.

When making a decision to switch from one business model to another, it is important for the bank to understand that each subsequent business model does not work without a debugged previous one. Before thinking about selling financial products and cross-channel customer experience, you need to make sure that Internet banking users can easily figure out statements and pay all their bills online. The transition from one business model to another is a serious business decision that involves large investments and the restructuring of processes and culture within the organization. Moreover, this business solution is not economically viable for all banks.

Let's consider the main trends in the development of mobile banks in the Republic of Kazakhstan at the end of 2019 [2].

Table 1 Main trends in the development of mobile banks in the Republic OfKazakhstan

|

For Android smartphones 1W1 |

For iPhone |

|||||

|

№ |

Mobile Bank |

Score |

Mobile Bank |

Score |

||

|

1 |

Sberbank Kazakhstan |

60 |

4.9/3.6 |

Sberbank Kazakhstan |

59.6 |

5.7/6.2 |

|

2 |

Kaspi Bank |

55.3 |

5.7/3.1 |

Kaspi Bank |

56.6 |

6.4/4.8 |

|

3 |

ATF Bank |

51 |

5.8/6.2 |

BankCenter Credit |

52.5 |

5.3/5.2 |

|

4 |

Bank CenterCredit |

47.3 |

4.1 /4 |

ATF Bank |

50.5 |

5.2/4.9 |

|

5 |

ForteBank |

45.9 |

6.1/4.9 |

ForteBank |

45.9 |

5.7/3.1 |

|

6 |

Altyn Bank |

43 |

5.3/4.9 |

Eurasian Bank |

39.5 |

3.9/4 |

||

|

7 |

Eurasian Bank |

40.5 |

5.5/3.8 |

HomeCredit Bank Kazakhstan |

36.1 |

3.8/3.4 |

||

|

8 |

Halyk Bank |

36.7 |

3.4/3.9 |

Halyk Bank |

35.9 |

4.1/3 |

||

|

9 |

Alfa Bank Kazakhstan |

36.6 |

4.3/2.9 |

Alfa Bank Kazakhstan |

35.6 |

3.3/3.8 |

||

|

10 |

HomeCredit Bank Kazakhstan |

36.5 |

3.8/3.5 |

Altyn Bank |

34.7 |

4.7/1.4 |

||

|

Final assessment of the effectiveness of the mobile bank (0-100 points) |

▲ |

Final assessment of the effectiveness of the mobile bank (0- 100 points) |

▲ |

|||||

|

Assessment of functionality and usability (1-10 points) |

Assessment of functionality and usability (1-10 points) |

|||||||

The market conditions (Daily Banking) are characterized by the following trends [3]:

- The digital office is developing mainly due to the opening of new products to the bank's customers: it is possible to obtain bank cards and cash loans completely remotely only in the AltynBank application. Other banks are limited to fewer products: debit and credit cards - ForteBank; only debit card - Sberbank, Eurasian Bank and ATF Bank. Only cash loan - KaspiBank, and in Alfa-Bank a credit manager leaves for the client.

- You can become a client completely remotely in four banks and only through a debit card order: only AltynBank uses a mobile bank as a full-fledged entry point, that is, identifies the client completely remotely), Eurasian Bank, ATF Bank. Sberbank carries out identification by meeting with a courier. Center-Credit Bank and Alfa-Bank do not use a mobile bank as an entry point at all.

- Chat in a mobile Bank does not solve the client's problems well. The chat is only available in Sberbank and HalykBank apps, and in both cases it is more focused on product sales and information requests (fare conditions, limits, and mobile app functions). The chat does not work with claims and problems: you will not be able to challenge the operation, cancel an erroneous transfer, change personal data or order documents.

However, Banks do not seek to implement features that do not have a direct benefit:

- Live chat support: even if the mobile bank has an informative guide, chat bot, or feedback form, they do not help the customer solve their problem so quickly and conveniently.

- Everything related to the history of operations: creating a single feed, information about specific operations, search, and expense Analytics.

- Product Management - card blocking and unblocking, limit management.

- Information functions - information about ATMs and terminals, tariffs and limits.

- Everything related to personal data is the ability to change and export it.

Thus, banks, when solving short-term and undoubtedly important tasks, such as the appearance and internal appearance of branches, equipment and their working condition, forget about creating long-term relationships with customers and bank values.

Based on the foregoing, it is advisable to identify the following areas for the development of mobile banking services:

- То increase the level of customer loyalty to the bank by establishing relations with the press, using print opportunities, oral propaganda, recommendations, charity, and informing the public about the bank's contribution to improving the country's economy.

- Build an effective system of employee motivation that correlates with the coefficient of customer satisfaction of the bank.

- Conduct regular monitoring of the quality of service, customer loyalty to the bank, customer awareness of banking products and services, as well as their involvement.

- Improve the material and technical support of the bank’s offices, introduce reliable and modernized equipment, as well as equipment, which will make it possible to use more efficient communication methods, build individual cross-selling systems and speed up the service process.

- To expand the coverage of customer bank cards in the market.

- Actively develop and implement innovative banking channels.

Conclusion

In general, the quality of service, customer loyalty, modem logistics and innovative banking channels as elements of business communications are being developed. There is a growing need for a comprehensive strategic approach to customers, which turns the quality of service into one of the necessary factors for the competitiveness of a retail Bank in the market and gives an impetus to financial growth. The quality of the Bank's relationship with the customer, and especially long-term relationships, becomes critical.

References:

- Mobile banking on smartphones overview of mobile applications of Kazakhstan banks in 2016 - https://deloitte.kz.

- Mobile banking rank Kazakhstan -2019 - https://markswebb.ru.

- The results of the study of the availability of banking applications in 2019 - https://usabilitylab.ru/blog/best-mobile-banking-kazakhstan.