Abstract. The purpose of the article is to study the role of Kazakhstan’s agro-industrial industry within the common agrarian market of the EEU, including the growth of the flow of exports in agricultural goods. The method of analysis includes the comparative analysis of statistical data on export flows and import volumes. As a result of the application of this method, factors are identified for the development of exports of individual Kazakh agricultural products in the EEU, the reasons for the Eurasian countries’ dependence on imports, and ways to increase the role of Kazakhstan’s agribusiness in the common market. Recommendations are given for the development of domestic exports of agricultural products in the context of regional integration processes.

The most important priority of the economic policy of Kazakhstan at the moment is the further deepening of trade with the EEU member states, including trade in agri-food products.

There is great potential for Kazakhstan to increase the export of agricultural goods to the EEU market.

At the same time, all the expectations and benefits for the republic from mutual trade in Eurasian space have not yet manifested themselves. The main obstacles have been the current practice of protectionism in the national markets of the Union and the use of barriers and restrictions in mutual trade. In addition, there is a low complementarity of trade between integrating states.

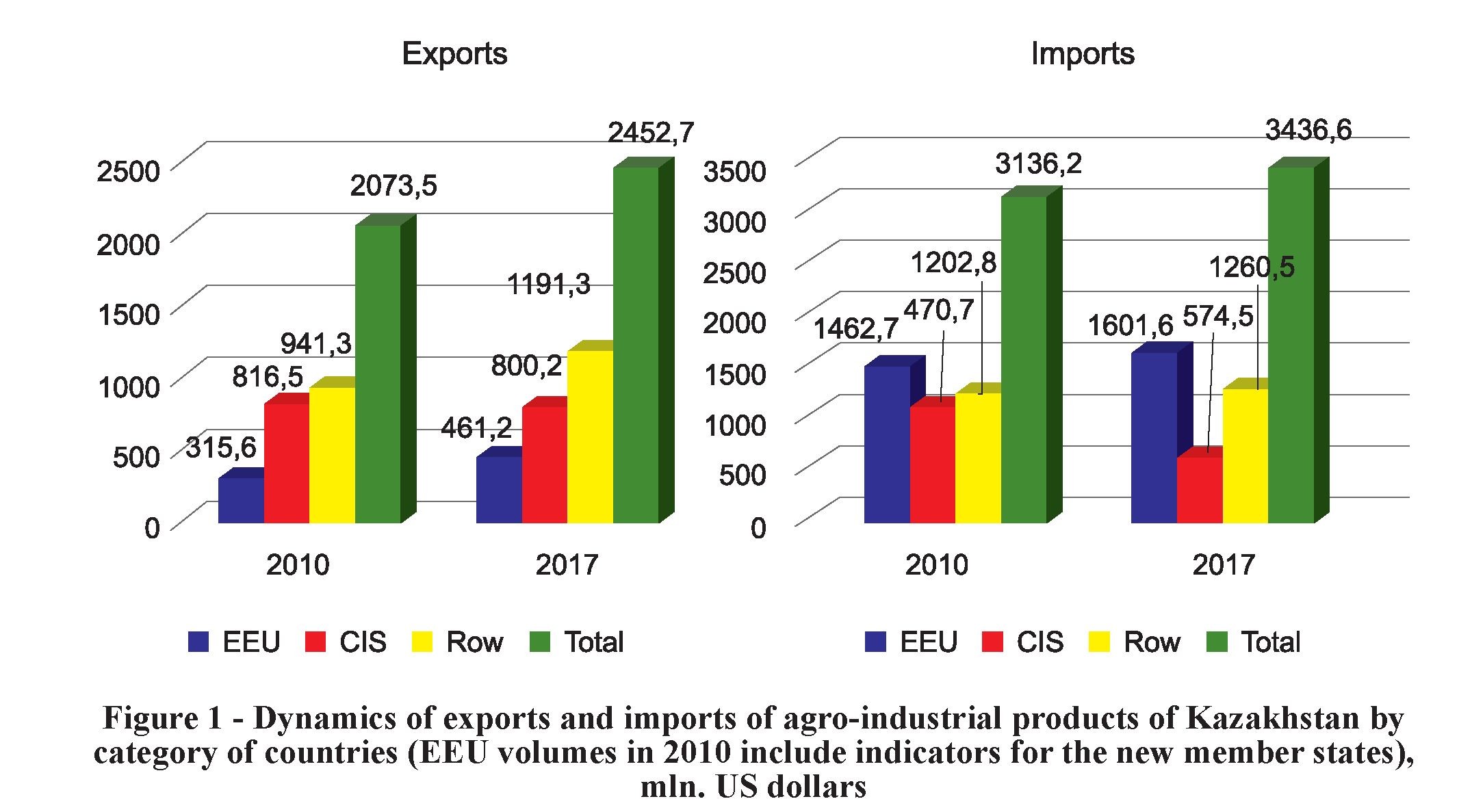

In 2017, the agricultural commodity turnover of Kazakhstan with EEU member states amounted to 2.1 billion US dollars, which is 16% more than in 2010 (Figure 1).

There is a tendency towards growth in the value of exports and imports. At the same time, the balance of mutual trade at all periods of integration development remained negative with all countries of the Union, except Kyrgyzstan.

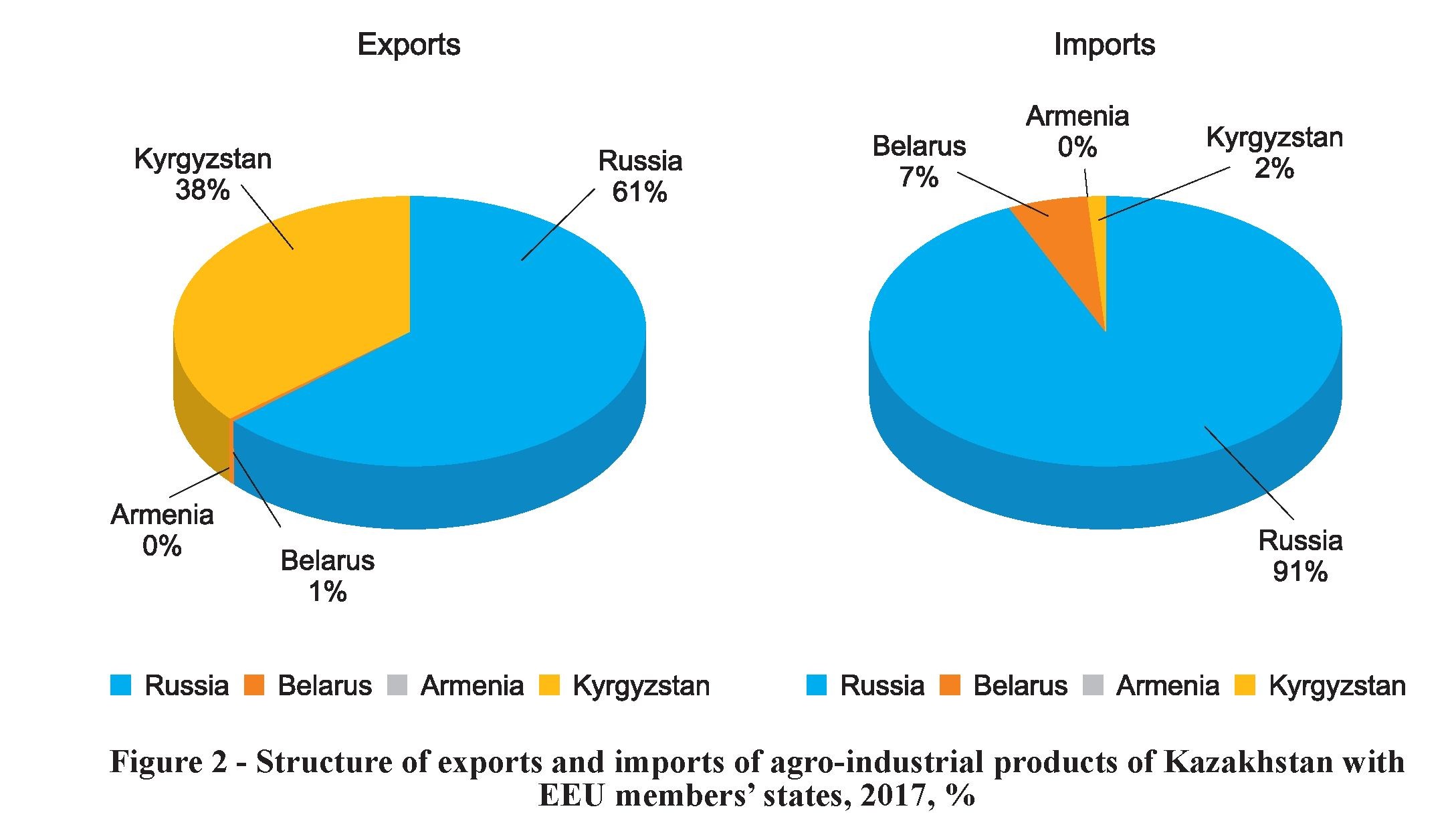

At present, the main trading partners are Russia and Kyrgyzstan. The main exported agricultural products of the republic fall on these states (Figure 2). The main reason is the existence of a common border, unlike Belarus and Armenia.

In the EEU market, Kazakhstani wheat flour, pork and vegetable oil have competitive advantages. Most Kazakhstani wheat is exported to Kyrgyzstan and Russia. Wheat flour and rice exported to these countries, as well as the export of melons and gourds to Kyrgyzstan, occupy a significant share of total exports. The main share in EEU member states’ imports is occupied by Kazakhstani rice and pasta (with especially high demand from Kyrgyzstan).

In general, the range of agricultural products exported to the countries of the Eurasian Economic Union is narrow, although these states need imports of vegetables, melons, gourds, and meat. It is these types of products in which the republic can specialize; and, under certain conditions of development and growth in the competitiveness of Kazakhstani products, there is the opportunity to expand their presence in the markets of the Union.

In addition, exports within the EEU are unstable (Table 1); and the markets of these states are not sufficiently developed for the agrarian sector of the republic (Table 2). This suggests that, despite the achieved level of mutual trade between Kazakhstan and the EEU member states, the potential for interaction in this area has not yet been fully implemented and, as an exporter, the republic remains the country with the least integration into intra-union economic ties.

The development of production and export of the above-mentioned goods is influenced by a number of negative factors that hinder the strengthening of the presence of Kazakhstani goods in the common market of the Union (Table 3).

Table 1 - Assessment of changes in export flows of agricultural products of Kazakhstan to the markets of the EEU member states, 2010-2016.

|

Product |

Change indices |

Share in agricultural export, % |

||

|

export volume |

export value |

2010 |

2016 |

|

|

Products with an ever-increasing export volume |

||||

|

Wheat |

1.557 |

1.444 |

26.6 |

22.9 |

|

Barley |

30.609 |

16.666 |

0.2 |

1.5 |

|

Cereals |

15.000 |

6.341 |

0.0 |

0.1 |

|

Pasta |

2.281 |

1.413 |

1.2 |

1.0 |

|

Poultry meat |

5.714 |

11.903 |

0.3 |

2.4 |

|

Canned meat |

2.333 |

2.190 |

0.3 |

0.4 |

|

Milk and cream not condensed |

107.000 |

42.7584 |

0.0 |

1.1 |

|

Cheese and curd |

2.167 |

2.298 |

0.6 |

0.8 |

|

Grapes |

376.667 |

95.255 |

0.0 |

0.6 |

|

Stone fruits |

162.222 |

11.576 |

0.0 |

0.1 |

|

Canned vegetables |

1.750 |

2.576 |

0.2 |

0.2 |

|

Products with an ever-decreasing export volume |

||||

|

Vegetables |

0.156 |

0.437 |

7.2 |

0.5 |

|

White sugar |

0.006 |

0.004 |

3.8 |

0.0 |

|

Vegetable oil |

0.274 |

0.217 |

6.3 |

0.8 |

|

Products with an unstable export volume |

||||

|

Corn |

0.010 |

0.000 |

0.0 |

0.0 |

|

Rice |

1.200 |

0.487 |

3.7 |

1.1 |

|

Gourds |

2.667 |

3.943 |

0.2 |

0.4 |

|

Product |

Change indices |

Share in agricultural export, % |

||

|

export volume |

export value |

2010 |

2016 |

|

|

Pome fruits |

3.333 |

1.456 |

0.0 |

0.0 |

|

Soy beans |

25.550 |

6.889 |

0.1 |

0.5 |

|

Sunflower seeds |

0.459 |

4.822 |

0.3 |

0.9 |

|

Lamb meat |

1.000 |

0.289 |

0.3 |

2.4 |

|

Wheat flour |

2.341 |

1.590 |

2.6 |

2.5 |

|

Margarine |

1.500 |

1.179 |

2.3 |

1.6 |

|

Butter and fat |

30.000 |

16.563 |

0.0 |

0.2 |

|

Canned fruits |

70.000 |

43.522 |

0.0 |

0.2 |

|

Wool |

0.867 |

0.600 |

0.4 |

0.1 |

|

Cotton fiber |

0.488 |

0.508 |

13.9 |

4.2 |

|

Note: statistics of the Committee on Statistics of the MNE RoK / http://stat.gov.kz/ |

||||

Currently, almost all the EEU member states (especially the agro-industrial exports of Belarus and Kyrgyzstan) are largely focused on the large Russian market. For Kazakhstan, export to the Russian market is constrained by the similar structures of agrarian production and the export of goods. In this regard, the republic remains the country with the least integration into intra-union economic relations as an exporter of products.

Table 2 - The volume of imports of agricultural products in the EEU member states, 2015

|

Products |

Import, thousand tons |

The share of Kazakhstan products in imports of the EEU members states, % |

||||||

|

Armenia |

Belarus |

Kyrgyzstan |

Russia |

Armenia |

Belarus |

Kyrgyzstan |

Russia |

|

|

Wheat |

332.3 |

26.7 |

461.1 |

331.4 |

- |

- |

100.0 |

98.9 |

|

Rice |

10.6 |

29.6 |

25.5 |

305.5 |

- |

- |

38.4 |

7.0 |

|

Wheat flour |

3.0 |

33.0 |

57.1 |

43.1 |

11.6 |

- |

30.6 |

37.3 |

|

Pasta |

5.3 |

38.0 |

2.3 |

15.5 |

0.3 |

0.05 |

100.0 |

32.9 |

|

Vegetables: |

11.6 |

213.5 |

11.0 |

1750.9 |

- |

- |

1.1 |

0.4 |

|

tomatoes |

0.2 |

103.2 |

- |

893.4 |

- |

- |

- |

0.01 |

|

onion turnip |

8.7 |

19.1 |

31.9 |

508.7 |

- |

- |

7.2 |

1.7 |

|

root plants |

0.2 |

13.9 |

45.6 |

118.4 |

- |

- |

- |

0.9 |

|

Gourds |

0.4 |

20.7 |

0.3 |

1468.9 |

- |

- |

20.0 |

3.4 |

|

Total meat |

44.2 |

100.4 |

62.4 |

1468.9 |

- |

- |

0.8 |

0.8 |

|

beef |

5.4 |

6.9 |

0.2 |

633.2 |

- |

- |

- |

0.3 |

|

pork |

7.1 |

33.0 |

3.5 |

372.7 |

- |

- |

- |

0.5 |

|

lamb |

- |

1.8 |

10.0 |

- |

- |

- |

0.1 |

|

|

poultry |

31.2 |

31.6 |

58.7 |

454.5 |

- |

- |

0.9 |

1.5 |

Note: statistics of the Eurasian Economic Commission / http://www.eurasiancommission.org

Table 3 - Problems of development of the export potential of agricultural products of Kazakhstan

|

Problems |

||||

|

wheat |

rice |

flour |

vegetables |

meat |

|

The mechanism for regulating relations between market participants has not been sufficiently developed. Low level of services, lack of targeted reproduction policy in the field of seed production. Periodic grain failure caused by the influence of weather conditions. Weak organization of transport logistics for the transportation of grain (lack of grain-carrying cars, etc.), high railway tariffs for the supply of grain. Strong regional (continental) competition from Russia. Critical deterioration of the infrastructure for the transportation of products to target markets and the associated increase in the cost of delivery. Low level of marketing of external demand and supply conditions |

High share of deteriorated irrigation systems, soil salinity. Kazakhstan’s high dependence on water sources with unresolved legal issues of settling transboundary water sources. Narrow varietal assortment and quality of Kazakhstani rice offered for export (78% exported as chaff). Imbalance between the acreage of rice and perennial grasses, which are its main predecessors. Changes in the level of world prices and increased competition from the countries of Southeast Asia. In addition, Russia is the main competitor in the common market of the Union, and has sufficient raw materials for rice production. |

High proportion of old equipment, which determines the high costs and prices. Competition in potential sales markets with local businesses using cheap imported grain as an improver. Tariff restrictions on imports of Kazakhstan flour (protective import duties, increasing excise taxes on flour from importing countries). Changes in consumer preferences in favor of the finished product (pasta); Increased competition from exporting countries offering lower prices and attractive terms of delivery and payment for products Increase in the number of intermediary structures in the market leads to higher prices |

Small-scale production of vegetables, which does not allow the volume of the commodity necessary for export. Weak development of domestic-seed production of vegetable crops. High seasonality of vegetable production and lack of storage facilities in production locations. Undeveloped logistic and transport infrastructure, high transport costs for the transportation of vegetables High competition in foreign markets and insufficient price competitiveness of domestic vegetable producers in comparison with the countries of Central Asia, China. Insufficient commercial processing of vegetables and non-compliance with technical regulations of the EEU |

Predominant placement of beef livestock in small farms of the population. Insufficient level of technical and technological equipment of the industry in the phase of reproduction of livestock and fattening young stock. Poor condition and use of fodder lands, weak forage base. Low productivity potential of livestock, low economic motivation of agricultural producers in fattening livestock. Unregulated economic relations in the chain of movement of products to the consumer. Low state support of beef farming in small business forms. |

The physical distance between individual EEU states (for example, Armenia and Kyrgyzstan) does not allow for full implementation of effective foreign-trade cooperation, which makes them focus on the development of technological cooperation that does not require physical interaction, for example, through the international outsourcing mechanism [1].

The current demand of the member states of the Eurasian Economic Union for imported agricultural products and foodstuffs for individual products is quite high.

For example, Armenia is insufficiently provided with pork, poultry, butter, vegetable oil, sausages, and sugar. It should be noted that these products are imported from third-party countries, with the only exception being vegetable oil, imported to a greater extent from the EEU member states.

In Belarus, high import demand is noted for grapes, pomegranates, melons and vegetable oil, which excluding melons and vegetable oil is mainly satisfied by imports from third-party countries.

Kyrgyzstan needs a significant external supply of poultry meat, vegetable oil and sugar, while, in addition to vegetable oil, the main share of imports is provided by third-party countries.

For Russia, the market of beef, butter, cheese, grapes and pomegranates is import-dependent, and is completely provided by from third-party countries, with the exception of dairy products, much of which goes to the Russian market from Belarus.

At the same time, many EEU member states import from Kazakhstan rice, both hulled and chopped rice, pasta, sunflower and other types of vegetable oils, margarine, tomatoes and canned meat and other goods.

Considering the demand for imported products of the EEU, the high volumes of supplies of products from third-party countries should be noted. These products include: beef, poultry, butter, cheese, grapes, pomegranates, etc. At the same time, the share of imports from third countries in Russia is about 89% of the total imports of agricultural products and foodstuffs, Armenia - about 76%, Belarus - 74%, Kyrgyzstan - 38%.

Kazakhstan’s dependence on imports of agricultural products and food from third-party countries is 57% [2].

In this regard, for the agrarian sector of Kazakhstan, the replacement of products imported from third countries and the expansion of mutual trade in agricultural goods within the Union are of current importance. The increased presence in the common EEU market is of primary importance, subject to increased competitiveness of the products supplied from specialized production areas, since Kazakhstan has favorable climatic conditions for increasing the production of grain, meat (beef, pork and lamb), vegetables and melons and vegetable oil.

Moreover, in the long term, the projected reduction in potato production in Armenia, Belarus and Russia, vegetables in Armenia, Belarus and Kyrgyzstan, and vegetable oil in the Russian Federation, with an increase in production in Kazakhstan, will in the future enhance the role of Kazakhstani agricultural products in the common agricultural market of the EEU.

World experience shows that the basis of the complex of measures for the formation of the export potential of the industry is a high degree of specialization and concentration of production, the establishment of sustainable production and economic ties with industry and trade. The main measures to enhance the export of agricultural and food products should be aimed at ensuring sustainable and innovative growth, based on taking into account the economic interests of the country and rational use of the productive potential of the agro-industrial complex, increasing its efficiency.

At the same time, from the trade complementarity point of view (that is, the export correspondence of one country to another in terms of the complementarity index ranging from 1 to 100, where 100 is full correspondence and1 is full non-correspondence) Kazakhstan and Russia have relatively high index when interacting with Belarus, i.e. its export basket is 50%, identical to what Russia and Kazakhstan would like to see in their imports.

In the case of Kazakhstan and Russia, the situation is different - complementarity is extremely low. This is due to the fact that the export set of countries does not correspond at all to what the partner country can offer as an export. This is quite a serious problem, because if we talk about successful regional integration blocks, complementarity within the EEU member states is 81, in NAFTA 73 and in ASEAN 87 [3].

The roots of this problem include reasons that prevent the effective implementation of legislative and other regulations and acts adopted within the framework of the EEU, as a result of which countries chose to ignore some decisions in some cases instead of coordinating.

In these conditions, the expansion of exports of products should be carried out by rationalizing the structure of exports in traditional markets (bringing new products to the market), as well as improving the competitiveness of domestic products. The main objectives of export promotion include:

- development of existing and formation of new commodity zones;

- reconstruction and modernization of production capacities of export-oriented agricultural organizations and processing enterprises;

- improving the quality of goods, improving the forms and methods of product quality management based on international standards;

- development and strengthening of mutually beneficial trade and economic relations with the EEU member states, consolidation of Kazakhstan exporters in the main segments of their markets;

- introduction of highly payable and resourcesaving technologies and business methods, allowing the development of competitive products.

- Kazakhstan has a number of opportunities to expand the presence of individual industries in the markets of other countries.

The basis for the further development of the export potential of Kazakhstan should be the formation of specialized export zones using intensive technologies that ensure the growth of product competitiveness.

Due to the fact that the main export product is wheat grain, effective measures are first of all needed to stimulate the export of these products. It should be borne in mind that the demand for wheat on the part of the EEU member states is not high enough and constant. Sustainable supply volumes, as the analysis shows, will reach a maximum of 0.8-1.0 million tons. Kyrgyzstan and Russia will remain the main consumers of Kazakhstani wheat. In the markets of Armenia, it is necessary to withstand competition with Russia, and in Belarus - with Ukrainian and Lithuanian grains. And given the need for transit through other countries, and, consequently, the rise in prices for the Kazakhstani product, it is possible to withstand competition only by supplying high-quality products.

Nevertheless, grain production will retain a leading position in the republic, and specialized areas of grain production have practically taken shape. So, a specialized area of wheat commodity production was created on the basis of three Northern regions, characterized by the cultivation of grain with high baking properties. About 80% of produced wheat belongs to the highest classes with a gluten content in excess of 23%. The existing lower costs for the production of wheat in the commodity area suggest that there is enough potential to maintain the price competitiveness of Kazakhstani grain in the Union and the world markets.

For the formation of consignments corresponding to the standard, it is necessary to create an effective system of quality assessment at all stages of the production cycle from harvesting, delivery to elevators and grain receiving points, storage, chipping-away - up to initial processing into finished products.

Under these conditions, an important direction for the expansion of wheat exports to the EEU member states is the production of high-protein, strong and solid grains.

At the same time, it is important to have alternative ways of supplying grain outside the EEU, that will expand the possibilities of exporting grain. An analysis of trends in major grain markets showed that global grain exports will grow, as do grain prices. The diversification of routes and the development of transport infrastructure will strengthen the negotiating position of Kazakhstan in concluding export contracts and setting tariffs for the transit of grain.

For the full sale of the export volumes of wheat, it is necessary to use the demand of other countries. The main areas of export of Kazakhstan wheat can be:

- Western European countries (Italy, Poland, Norway) importing high-quality durum wheat from Kazakhstan;

- Central Asian countries (Turkmenistan, Tajikistan, Uzbekistan), and possibly Afghanistan, where wheat and flour from Kazakhstan dominate in imports of wheat and flour;

- countries with access to the Mediterranean and Black Seas (Turkey, Egypt, Tunisia), where Kazakh wheat shares the market mainly with the Russian, Ukrainian, Canadian and other countries wheat;

- Azerbaijan, where Kazakh wheat shares the market with the Russian wheat;

- China and Iran, where Kazakh wheat competes with products from various producing countries.

In addition, it should be noted that in various areas, Kazakhstani wheat competes with the Russian one. This shows the need for the creation of a single export system, for example, “Grain of Eurasia”. At the same time, the organization of the Integrated Transport System of the EEU will increase traffic volumes and the quality of infrastructure, which will improve the conditions for trade and, first of all, increase trade.

It will also allow the creation of a land-transport bridge between Europe and Asia, giving a positive synergistic effect to the EEU member states.

Under certain conditions, vegetables can occupy a niche in the Kyrgyz market and expand into the Russian market, especially since natural and economic conditions favor the development of their production in the country.

It is advisable to create in the republic a specialized vegetable production zone in three Southern regions that have high competitive advantages. Here it is necessary to form large and medium-sized specialized farms (through cooperation), focused on the supply of export batches of homogeneous competitive products.

The commodity zone of vegetable growing is characterized by a wide range of vegetable crops and is distinguished by high price competitive advantages, which makes it possible to develop export potential (Table 9).

According to calculations, the republic as a whole has an excess of commodity resources of vegetables that can be sent for industrial processing in the domestic market, as well as for export.

Currently, commodity resources in the specialized zone amount to 1,135 thousand tons of vegetables (minus losses, production and domestic consumption in the farms of the zone). The capacity of the city market as a whole is 910 thousand tons. Consequently, agricultural units of the specialized zone can export about 200-225 thousand tons of products for export yet today. Taking into account the production in households, this volume can grow to 400 thousand tons.

The experience of countries with developed vegetable growing shows that it is advisable to create an Association of Producers and Exporters of Vegetables, performing the functions of purchasing seeds, fertilizers, plant protection products, organizing seminars together with representatives of scientific research institutes, as well as studying the sales markets, determining the price corridor, and providing assistance in sales of commodity products.

Having adjusted the process of obtaining phy- tosanitary certificates, Kazakhstan’s producers will be able to supply the Union with 300 thousand tons of vegetables (Kyrgyzstan and Russia) and export at least 100 thousand tons of vegetables to third countries. It should be noted that the demand is more focused on other vegetables (eggplants, peppers, etc.), that is, production restructuring is necessary.

For the development of export potential and access to the integrated market of the EEU, in addition to the formation of a specialized commodity zone in the Southern region, the following measures are necessary:

- to develop and adopt an export program for the production and processing of vegetables products;

- to develop and introduce the production technology of frozen vegetables, fruits and berries;

- to create an effective two-stage system for storing fruit and vegetable products in the places of production and consumption;

- to form a system of wholesale markets and sales cooperatives to promote products in the domestic and foreign markets;

- to modernize enterprises processing vegetables with export orientation.

Vegetable oil can be another export product, given the ongoing diversification and a significant expansion of oilseed production.

In the republic, it is possible to form two commodity zones for the production of vegetable oil - the northern and eastern ones, which specialize in its various forms. So, the northern zone will focus on the production of rapeseed and flaxseed oil, and the eastern on sunflower oil. Here the production is 75% oilseeds, which has a high efficiency (Table 10).

Beef farming in Kazakhstan has great potential for development. But it is focused only on providing meat for the consumer demand of the domestic market. The ability to export livestock products is still underused.

The republic is fully provided with all kinds of meat, except poultry, despite the fact that its production growth rates are among the highest (9% per year at an average rate of 3%). Therefore, the main problem of increasing exports is the lack of meat resources. As a result, with the planned indicator of meat exports of 60 thousand tons annually in 2016, Kazakhstan managed to export only 16 thousand tons of meat.

In addition to the lack of resources, barriers to the development of mutual trade in meat can be noted. In order to identify them, a survey of meat enterprises of Kazakhstan, which export products to the EEU member states, was conducted. The following factors were highlighted as the main ones:

- the spread of diseases, pollutants, toxins carried by animals, plants or products from them (the veterinary state of the industry);

- the lack of a common database containing information about the organization and subjects of mutual trade (information support);

- limited access to the results of market research of the EEU member states and other states (marketing);

- poor development of transport and logistics infrastructure (movement of goods);

- the lack of stable bilateral relations between suppliers and consumers (relationships).

In addition, Kazakhstani exporters pointed to differences in the amount of state support for agricultural production in the EEU member states and lending rates, which clearly affects the competitiveness of the exported goods and has a high degree of restrictive impact. A number of intermediary organizations exporting meat products to the EEU member states noted a difference in the transport tariff on the territory of Kazakhstan and Russia as a restrictive impact on the export of goods, which affects the costs of circulation.

At the same time, the difficulty of introducing the product into the retail networks of a number of large Russian markets is apparent. Excessively high conditions for entering the market are offered; and, as a result, the value of the export product increases several times (1.5-2).

Nevertheless, in modern conditions, considering the development of a specialized industry of beef farming and determining the main directions of its functioning for the future, one should proceed from the priority of placing beef farming in regions with the most favorable conditions.

Thus, for the purpose of intensive formation of export potential, Kazakhstan’s livestock industry needs to maximize the existing advantages of the industry’s development - favorable climatic and economic conditions of the regions, which allow to raise lower-cost livestock, which at optimal placement will contribute to sustainable growth of production of competitive products.

The main problem hindering the efficient use of the existing favorable climatic potential and competitive advantages of the regions is small-scale production in the absence of a solid fodder base.

At the same time, the development and creation of conditions that make it possible to optimize trade and economic cooperation with integrator countries is of current importance for Kazakhstan [7]:

- creation of a centralized mechanism for the organized multilateral trade in spot agricultural products, raw materials and food (spot market);

- development of balances of agricultural production and trade by the subjects of the wholesale food market;

- creation of a database of fixed-term (forward) contracts for the supply of agricultural raw materials and food between wholesale market participants;

- development of cooperation for the supply of products through the supple chain, use of complementary functions of partners, their specialization, that is, concentration and redistribution of resources to key positions in the general system of production development and product promotion.

As a result, Kazakhstan will be able to increase its presence in the market of the EEU member states for many products, creating conditions for import substitution of goods coming from third- party countries (Table 13).

According to calculations, it is possible to completely replace imports of wheat flour, melons and lamb from third-party countries only at the expense of Kazakhstani production.

However, for the implementation of these calculations it is necessary to formulate a common strategy for the development of mutual trade, containing the following areas [8]:

- creation of an integrated interstate commodity distribution system;

- creation of a joint stabilization fund;

- creation of interstate associations, joint ventures, industry (product) associations or unions of producers;

- coordination of export operations in order to expand the market and increase the economic interest of producers.

Thus, for the purpose of intensive formation of export potential, Kazakhstan’s livestock industry needs to maximize the existing advantages of the industry’s development - favorable climatic and economic conditions of the regions, which allow to raise lower-cost livestock, which at optimal placement will contribute to sustainable growth of production of competitive products.

In this regard, the following areas of development of Kazakhstan’s exports to the EEU member states are relevant. In order to further develop the export-oriented industries of the agrarian sector, it is advisable to identify the most effective areas of specialization with significant potential for further development.

In addition, export support tools that comply with international rules and practices should be more actively applied:

- subsidizing a business without being linked to “export performance” (that is, not taking into account the volume of export deliveries);

- subsidizing the transportation of goods through the territory of Kazakhstan;

- exchange rate regulation;

- informational support for exporters on promising sales markets, technical support in the form of financing research costs, consulting or assistance to regional development projects.

Increasing the benefits for Kazakhstan implies free choice of trading partners and building mutually beneficial trade and economic relations with them. It is extremely important, not focusing only on the trade within the EEU, to diversify exports, expanding supplies to China, Iran, as well as to other countries of Central Asia and the Caucasus. It is vital to develop economic integration in the framework of regional trade agreements, in particular, to expand mutual trade in the format of a free trade zone with the CIS countries.

Broad prospects for Kazakhstan are opened up with its participation in the Silk Road Economic Belt project, which is aimed at the development of international and regional trade. The new Silk Road connects China through Kazakhstan with Iran and Turkey, thereby opening up international transport routes to domestic exports not only to China, but also to Europe, as well as to the Middle East countries.

REFERENCES:

- A. Migranyan. Aggregated model for assessing the competitive potential of the EEU member states // Eurasian Economic Integration, 2015. - 4 (29). - P.45-64.

- Monitoring of food security of the EEU. - M.: ECE, 2015. – P.36.

- Prospects for the development of interstate integration: Eurasian Union. Electronic resource //kazorta.org/perspektivy-razvitiya-mezhgosudarstvennoj-integratsii