Abstract. This paper evaluates the prospects of increasing economic confrontation between Saudi Arabia and the United States, caused by the adoption of the "Justice Against Sponsors of Terrorism Act ", which allows U.S. citizens to file lawsuits demanding compensation for damage caused by the terrorist attacks of 11 September 2001. This Act permits, within the United States, the arrest and confiscation of the assets of states which are classified as “sponsors of terrorism”; and creates significant risks, primarily to the assets of Saudi Arabia. The adoption of this Act has caused increased tension between the two countries, as well as the outflow of Saudi investment in various U.S. assets. The biggest impact this process can have is on the stability of the treasuries market and the American system of public finance in general. This article discusses the possibility of Saudi Arabia having a hypothetical destabilizing effect on the US financial system in the specified context as well as the direction and potential of that effect.

At the end of September 2016, relations between the US and Saudi Arabia were affected negatively when the US Congress overcame President Obama's veto on the Justice Against Sponsors of Terrorism Act (JASTA). Justice Against Sponsors of Terrorism, among other things, allows for the filing of claims via US lawsuits against Saudi Arabia for compensation for damage caused by terrorist acts on September 11, 2001. Such claims can cause serious disagreements between the United States and Saudi Arabia, including economic and political confrontation, which under certain conditions may have a negative impact even on global financial stability. In this regard, it seems appropriate to consider the possible direction and consequences of a hypothetical confrontation in the economy between the two countries on the basis of this act, which has the potential to become a long-term factor of tension between the two countries.

The history of the Act is briefly as follows: In May 2016, the US Senate voted unanimously for the adoption of the Act, giving as an explanation the need to allow victims of terrorist attacks against US citizens to claim compensation from the countries sponsoring terrorism, as the current legislation does not give such an opportunity, recognizing sovereign immunity [3]. On 9 September, the Act was approved by the House of Representatives of the US Congress and was handed over to the President for signature. On September 23, 2016, US President Barack Obama imposed his veto on the act; but after the vote on September 28, the US Congress, for the first time in eight years of Obama's presidency, overruled his veto. 97 representatives voted in favour of the law and one against [4] [5].

JASTA suggests that, unlike existing legal norms, where the state sponsoring terrorism refuses to voluntarily cover damages as decided by the US courts, such coverage may be enforced. To ensure compensation is paid, the assets of countries recognized as sponsors of terrorism can be arrested, seized and subsequently used for the payment of claims. On October 1, the first lawsuit under this act was filed against Saudi Arabia by a US citizen, a woman who lost her husband during the September 11 attacks.

The adoption of this act, effectively canceling the immunity of a sovereign state within the territory of the United States, was perceived extremely negatively in Saudi Arabia. On September 29, the Foreign Ministry issued a statement, in which it was stated that “the erosion of sovereign immunity will have a negative impact on all states” 3. A statement of this kind by the Foreign Ministry can be interpreted as a threat of the use of response measures.

It may also be noted that, in connection with the adoption of JASTA, a quick and negative reaction to this act was demonstrated by some other states close to Saudi Arabia. On October 4 and 5, concerns were voiced by Sudan, Kuwait and Qatar over the attempt to remove sovereign immunity, which may be an indirect sign of the readiness of Saudia Arabia and its allies to raise the idea of confrontation with the United States.

The aforementioned reaction of the Saudi Foreign Ministry to this bill after the congressional overruling of the presidential veto was not the first - throughout its passage through the relevant institutions, various representatives of Saudi Arabia expressed their explicit negative attitude towards it, including in the form of threats by way of hindering economic cooperation. In particular, the New York Times reported in April that the Saudi Foreign Minister Adel Al Jubair delivered a personal message to Washington during a visit, stating that the country “will have to sell US Treasury bonds and other assets up to 750 billion dollars before they are exposed to the danger of being frozen by the American courts” [6].

This statement was commented on extensively, including by high-profile financial experts and publications, and the tone of these comments was unanimous. Saudi Arabia was threatening (or blackmailing) the US with the prospect of a collapse in the treasury bonds markets, the dollar and other areas of the financial market. The indicated amount of 750 billion dollars at that time represented about a quarter of foreign central banks’ investments in US government securities. This amount was considered to be particularly significant for the stability of the market for these instruments and related areas.

In this case, it is necessary to clarify that, at the time of this statement, the US Treasury’s statistics did not disclose the amount of funds invested by Saudi Arabia in the securities issued by this agency, and it could have given the impression that the Kingdom’s threat was extremely weighty. However, at that time, competent experts noted that the amount mentioned exceeds the entire amount of gold and foreign exchange reserves of the Arab monarchy [7].

Shortly after this statement by Saudi Arabia and the wave of commentaries that it sparked, the Treasury began to publish statistics regarding the volume of its obligations that the Kingdom owns (perhaps, precisely as a response to blackmail, and also to neutralize the potential tension in the market); and it turned out that these volumes are much less than the announced amount of $ 750 billion, slightly exceeding $ 100 billion. However, in the sensational statement by the Saudi Arabian Ministry of Foreign Affairs, not only was investing in treasury obligations mentioned, but other assets were also discussed, so the question of both the extent of the Saudi possessions in the US and the consequences of their rapid forced sale remains open. We will try to evaluate these complex parameters in detail.

First of all, it should be noted that the very formulation of the question of the economic confrontation between Saudi Arabia and the United States may seem fictitious, in view of the very large difference between the scales of their respective economies. The US GDP, at the end of 2015, was measured at $ 18,036 billion against $ 646 billion in Saudi Arabia 6 (exceeding it by more than 28 times); American exports ($ 1,505 billion in 2015) exceed Saudi exports ($ 202 billion) 7 times; and the other macroeconomic parameters of the United States and the Saudi Kingdom also differ in many aspects.

However, despite the United States’ repeated superiority over Saudi Arabia in macroeconomic indicators, in the field of bilateral cooperation, the situation is much more equal, and the Kingdom is an equal economic partner with the US in some areas. The main direction of international economic cooperation - mutual trade - is not significant for the United States. Saudi Arabia accounted for only 1.3% of US exports (19.7 out of 1,505 billion dollars) and 1% of imports (22.1 out of 2,241.1 billion dollars) 8. Saudi Arabia plays a much more significant role as a US investor.

As of 2014, the US employed 10,400 people in companies with Saudi capital. $1.7 billion was spent by such companies on R&D and they contributed $2.3 billion to US exports.9 The volume of Saudi Arabia’s accumulated foreign direct investment in the US exceeds the US investment in Saudi Arabia (Table 1) - that is, the Kingdom is a net lender of the United States for this type of investment and this situation has remained stable over a long period of time.

|

2010 |

2011 |

2012 |

2013 |

2014 |

2015 |

|

|---|---|---|---|---|---|---|

|

Accumulated FDI of Saudi Arabia in the US |

9,074 |

10,632 |

10,216 |

12,323 |

11,541 |

11,515 |

|

Annual inflow of Saudi Arabia’s FDI into the US |

-495 |

n/a |

n/a |

608 |

-1,185 |

477 |

|

Accumulated FDI of the US in Saudi Arabia |

7,436 |

8,132 |

9,500 |

10,084 |

9,502 |

10,509 |

|

Annual inflow of the US’ FDI into Saudi Arabia |

-66 |

807 |

1,690 |

635 |

245 |

1,053 |

Table 1. Indicators of bilateral investment cooperation between the United States and Saudi Arabia per million dollars.10

6 According to the World Bank: World Development Indicators// World Databank. The World Bank website. URL: http://databank. worldbank.org/data/reports.aspx?Code=NY.GDP.MKTP.CD&id=af3ce82b&report_name=Popular_indicators&populartype=series &ispopular=y# (last accessed date: 01.10.2016).

7 World Trade Statistical Review 2016. World Trade Organization website. URL: https://www.wto.org/english/res_e/statis_e/ wts2016_e/wts16_toc_e.htm

8 Foreign Trade. U.S. Census Bureau website. URL: https://www.census.gov/foreign-trade/statistics/highlights/top/top1512yr.html (last accessed date: 14.10.2016).

9 Foreign Direct Investment (FDI): SAUDI ARABIA// Select USA government program website. URL: https://www.selectusa.gov/ servlet/servlet.FileDownload?file=015t0000000LKNG (last accessed date: 13.10.2016).

10 FDI stocksOutward / Inward, Million US dollars, 2015// FDI stocks// OECD Data. OECD website. URL: https://data.oecd.org/fdi/ fdi-stocks.htm (last accessed date: 17.10.2016).

The data in Table 1 demonstrates, on the one hand, that Saudi Arabia is more important as an investor for the US despite a multiple backlog in quantitative measurement of the economic potential; and on the other hand, indicates a relatively small amount of accumulated direct investments by Saudis in the American economy. The sum of 11 billion dollars is incommensurate with the above estimates of 750 billion, as declared by the Kingdom’s representatives. It will also be noted, in the context of a potential economic confrontation between the countries, that Saudi Arabia's share in the total amount of accumulated US FDI is extremely low; and their possible withdrawal from the country in the light of a hypothetical deterioration of relations would not be capable of any significant impact on the American economy. According to the OECD, the total amount of accumulated FDI in the US at the end of 2015 amounted to $5,571 billion.11 The corresponding indicator of Saudi Arabia of $ 11.5 billion is, therefore, only 0.2% of this value.

It can be noted that, despite the significant economic potential of Saudi Arabia and the fact of high oil prices over the course of several years (expressed, for example, by the fact that it is in third position in the world in terms of international reserves), foreign direct investment from this country remains moderate (Figure 1). Their accumulated volume, of which the main part was created during the last decade, is $50 billion - less than 0.2% of the global level. This indicator is also significantly smaller than the share of Saudi Arabia in the world GDP (0.9%) and other key macroeconomic indicators, which in the context of economic confrontation, testifies to rather modest possibilities of influence on the curtailment of economic cooperation.

It can be noted that, despite the significant economic potential of Saudi Arabia and the fact of high oil prices over the course of several years (expressed, for example, by the fact that it is in third position in the world in terms of international reserves), foreign direct investment from this country remains moderate (Figure 1). Their accumulated volume, of which the main part was created during the last decade, is $50 billion - less than 0.2% of the global level. This indicator is also significantly smaller than the share of Saudi Arabia in the world GDP (0.9%) and other key macroeconomic indicators, which in the context of economic confrontation, testifies to rather modest possibilities of influence on the curtailment of economic cooperation.

11 Calculated on the basis of UNCTAD: Foreign direct investment: Inward and outward flows and stock, annual, 1980-2014// UNCTADStat. United Nations Conference on Trade and Development website. URL: http://unctadstat.unctad.org/wds/ ReportFolders/reportFolders.aspx (last accessed date: 12.10.2016).

On the other hand, foreign FDI to Saudi Arabia is also relatively small (their accumulated volume amounts to 224 billion dollars), with the inflow of foreign investments constantly declining since 2009, and by 2015 it had decreased about five times as compared to its peak level in 2008. At the same time, the amount of accumulated FDI from the US is very small, amounting to about $ 10.5 billion (see Table 1 above), and, under conditions of hypothetical economic confrontation, these funds cannot be an effective response tool for the possible arrest of Saudi assets in the United States.

Nevertheless, Saudi Arabia has a fairly effective lever of influence on the financial stability of the United States as it has reserves placed in US assets. The question of how painful the withdrawal of these funds by the kingdom would be remains to be seen because the statistics for most of these reserves are not sufficiently transparent; but one can try to assess the consequences of such a step, at least approximately.

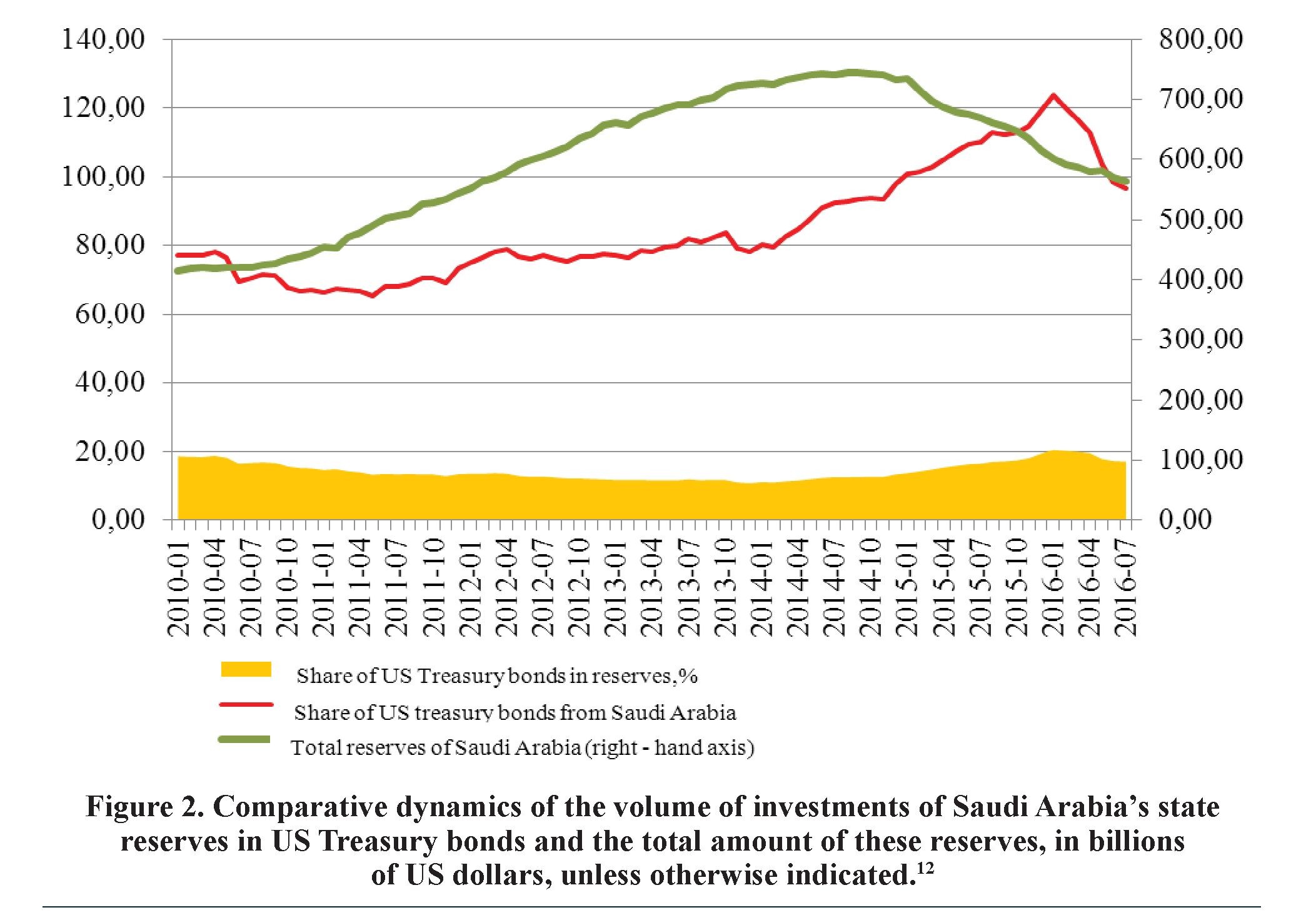

First of all, it should be noted that, after the fall in oil prices and the pressure exerted on the Saudi rial and the revenue side of the state budget, the size of Saudi Arabia's reserves has fallen significantly - from a maximum of about $750 billion in mid-2014 to 560 billion by mid-2016. In two years, therefore, almost $200 billion was spent. (Figure 2).

First of all, it should be noted that, after the fall in oil prices and the pressure exerted on the Saudi rial and the revenue side of the state budget, the size of Saudi Arabia's reserves has fallen significantly - from a maximum of about $750 billion in mid-2014 to 560 billion by mid-2016. In two years, therefore, almost $200 billion was spent. (Figure 2).

12 Calculated on the basis of the US Treasury and Saudi Arabia Monetary Agency: Major Foreign Holders of U.S. Treasury Securities// Securities (B): Portfolio Holdings of U.S. and Foreign Securities. U.S. Department of the Treasury website. URL: https://www.treasury.gov/resource-center/data-chart-center/tic/Pages/ticsec2.aspx (last accessed date: 12.10.2016); ); Monthly Statistical Bulletin. July 2016. Saudi Arabia Monetary Agency, August 2016. SAMA website. URL: http://www.sama.gov.sa/en-US/ Indices/Pages/Financial.aspx (last accessed date: 27.09.2016).

Nevertheless, even the reduced reserves are still quite large; and until recently the decrease in their total volume was not accompanied by a reduction in Saudi investments in US treasury bonds. Against the backdrop of the rapid depletion of reserves, the Kingdom even increased the amount of US national debt they purchased by contributing to the stability of the state’s financial markets. The US is its strategic ally, and Saudi increased the share of these liabilities in its reserves. The rapid growth of Saudi investments in US debt began in January 2014 (before that, their volume was stable) and lasted until early 2016, despite the deteriorating economic situation in Saudi Arabia and the rapid reduction in reserves. During 2014 and 2015, the Saudis increased the volume of investments in US national debt by 50% - from 80 to 120 billion dollars. Such a sharp increase in investments in US assets against the background of a fall in the total volume of its reserves does not correspond to the practice shown in previous years, when the share of Saudi reserves placed in treasury bonds was steadily declining, and the causes of this phenomenon can be more quickly sought in the foreign policy plane.

The new round of reduction of the volume of treasury bonds in Saudi Arabia coincides with the process of development and promotion of the JASTA law project. The first noticeable decline of this indicator occurred in February, March and in May (when the Senate voted for JASTA) and its monthly decline was almost $ 10 billion, about 10%, and from January to July. Saudi Arabia's investments in data instruments fell from $ 124 billion to $ 96 billion - by 28 billion, or by 22.5%. We can assume that the Kingdom’s reaction to the passing of JASTA through the House of Representatives and the overruling by Congress of the presidential veto will be equally unambiguous and will be expressed in a new strong fall of the indicator in the statistics for September and October.

There is a relationship between the passing of the JASTA through Congress and the withdrawal of Saudi Arabian funds from from US national debt. At the same time, the reason for this conclusion may not be so much an attempt of economic pressure by the Saudis on the US, but a more pragmatic aspiration to secure their investments from their possible arrest as security for claims. Regardless of the reasons, the conclusion is reached, and the question of consequences of this process arises for the stability of the US national finance system.

Saudi Arabia’s investments in treasury bonds, in any case, according to the statistics of the Treasury, are not very significant. Even at their peak in January 2016, when their volume was estimated at $ 123.6 billion, they accounted for only 3% of foreign government investment in these assets ($ 4,093 billion) which was 2% of total foreign investment (6,183 billion) and about 0.7% of the total volume of US national debt. Even with respect to the share of debt owned by foreign public investors, this amount is too insignificant to seriously affect the stability of the relevant market.

At the same time, it should be noted that equilibrium in any section of organized financial markets is currently fragile, and this also applies to the US Treasury bonds market. Market volatility is manifested in the fact that relatively small sales volumes, for example, within the framework of Saudi Arabia's withdrawal, can cause appreciable price and yield fluctuations. At the same time, the decrease in the volume of investments by the kingdom in treasury bonds has strongly affected the overall statistics of the withdrawal of funds from these instruments by foreign state holders.

At a time when Saudi Arabia was actively withdrawing its reserve funds from US debt from February 2016, there was also a general reduction in the presence of foreign government investment in these instruments. According to the US Treasury, the decline in such investments amounted to 83 billion dollars[8], according to the Federal Reserve, in terms of the funds held on its accounts - 70 billion.[9] Given that Saudi Arabia withdrew $ 28 billion from these assets over the same period, the country’s influence on the process of reducing foreign government investment structures in the US national debt was quite significant - the Kingdom accounted for up to 40% of the total funds withdrawn by foreign sovereign holders.

The process of a massive withdrawal of funds from financial assets, that is, their sale, is accompanied by a decrease in the prices of these assets. With respect to debt, this means an increase in their profitability, that is, an increase in interest that is paid to holders and the cost of servicing the debt as a whole, which is taken from the state budget. An intensive sale of US treasury bonds on the part of Saudi Arabia contributes to raising their profitability and increasing the federal budget’s spending on servicing national debt. It is this factor that is the main threat to the United States in the event of an economic confrontation with the Arab monarchies of the Persian Gulf, and an understanding of the significance of this factor has caused corresponding threats from the

Saudis in the process of adopting JASTA.

The degree of influence of the treasury bonds sale on their yield is difficult to assess, since the yield of these instruments is determined by a very large number of other factors. In general, during February and July 2016, the yield of these assets declined and it cannot be concluded that their sales by Saudi Arabia led to lower prices and higher yields. However, it should also be taken into account that the quota of these instruments during this period was influenced by stronger factors, against which the sales of Saudi Arabia (and other foreign state investors as a whole) did not manifest themselves. But the absence of a strong relationship does not mean the absence of influence of this factor - in case of maintaining the stable position of the kingdom in treasury bonds, their quota would be even higher.

It should also be noted that the month where there was the most active withdrawal by Saudi Arabia from these securities (May 2016, a decrease of almost $10 billion) still showed growth, reaching almost 0.2 percentage points (From 1.7 to 1.88% per annum for 10-year securities). In addition, it may be noted that the strong growth in the yield of treasury bonds occurred after Congress overcame the veto of Obama - since the end of September their profitability has grown quite significantly - from 1.54% on September 29 (the day of overruling the veto) to 1.8% to 17 October. It is likely that this growth in yield (reflecting the fall in market shares) was caused, among other things, by investors’ fears about a new round of selling US debt to Saudi Arabia and the implementation of this scenario.

The jumps in profitability in May, and its growth in October, after overruling the JASTA veto, are significant enough. The increase in yield by 0.2-0.4 percentage points, given the apparent insignificance of this figure, can complicate the budget process in the US, given the huge absolute size of national debt, which, in just its federal aspect, will reach $20 trillion by the end of this year. With this amount, each additional 1/10% of yield means an increase in the cost of services by $20 billion per year. Given that in recent years, the federal budget spent on servicing the national debt was about $400 billion, an increase in yield by 0.1% would mean an increase in expenditures by 5%, which is quite significant in the context of suppressed economic activity and a reduction in budget expenditures (the amount of the US federal budget is reduced from 2012).

Thus, despite the relatively small amount of Saudi Arabia's investment in US public debt, their rapid sale could have a destabilizing effect on the Treasury bond market and cause a noticeable increase in yield that could complicate public debt service and the budget process. It should also be taken into account that significant investments in these financial instruments have also been made by the allies of Saudi Arabia, the related monarchies of the Arabian Peninsula. Thus, the size of the state investments of the United Arab Emirates in July 2016 amounted to 66 billion dollars, Kuwait’s - 32 billion.[10] In the event that the escalation of tensions between

Saudi Arabia and the United States occurs, it is also possible that these countries will exit from US securities, which will also lend an impetus to further reduce their prices and increase the cost of servicing the US national debt.

The issue of the likelihood of such escalation is beyond the scope of this report and lies in the political plane, but its likelihood is not ruled out, including against the backdrop of increased disagreements among countries in the foreign policy area. So, in October, a representative of the US State Department announced the revision of US aid programs to Saudi Arabia against the backdrop of its military operations in Yemen. A much stronger incentive for activating the curtailment of economic cooperation and rapid withdrawal of funds from assets in the United States could be judicial decisions to recover the funds of the kingdom in favor of those suffered after the attacks of September 11.

Considering the escalation scenario of the hypothetical confrontation between Saudi Arabia and the United States, it should be borne in mind that the Kingdom’s investments in US assets are not limited to the amounts considered in the Treasury statistics discussed above. First, these statistics cannot take into account the whole amount of investments, since some of them can occur through other countries. Second, not all of the Saudi investments can be represented by the state reserves of the central bank (SAMA), and investments are made by other investment state institutions whose assets in July 2016 amounted to almost 170 billion dollars.[11] Third, the statistics of the US Treasury show a very small amount of investment in comparison with the amount of the reserves of Saudi Arabia. Meanwhile, in the above statement by the Foreign Ministry threatening to withdraw $ 750 billion from the US, it is drawn by the fact that it was precisely such a value that estimated the reserves of the kingdom by the end of 2014, and this suggests that all or nearly all of the country’s reserves were traditionally invested in American assets. Finally, considering the option of escalating economic confrontation with the involvement of Saudi allies from neighboring monarchies, it can be noted that the potential for their investment in the US economy is also very large given the sovereign funds and government investment companies (Table 2).

Table 2. Volumes of assets of leading state structures of the Arabian monarchies of the Persian Gulf, billion US dollars.17

|

Organization |

Country |

Total assets |

|

Abu Dhabi Investment Authority |

United Arab Emirates |

792 |

|

Kuwait Investment Authority |

Kuwait |

592 |

|

Qatar Investment Authority |

Qatar |

335 |

|

Investment Corporation of Dubai |

United Arab Emirates |

196 |

|

Public Investment Fund |

Saudi Arabia |

160 |

|

Abu Dhabi Investment Council |

United Arab Emirates |

110 |

The total amount of assets of just the six largest state institutions is almost 2.2 trillion. In spite of the fact that in these and other monarchies of the Persian Gulf, there are about a dozen less large state companies and funds. The aggregate financial capacity of these institutions far exceeds the amount of the international reserves of their central banks and, if necessary, can become a serious lever of economic pressure on the US, even taking into account the fact that most of the investments of these structures are not invested in US national debt.

However, the latter aspect does not reduce the destabilizing potential of this direction of a possible economic confrontation, like the sale of financial assets. The financial system of a country, especially countries like the US, with economies that depend so heavily on financial markets, can be effectively shattered, not only through government debt obligations, but also through other sectors of the market- the stock market, the market of corporate bonds, derivative financial instruments, etc. Undoubtedly, in all these sectors, the funds of the Arabian monarchies are represented by quite significant amounts, and their withdrawal can become a factor of strong destabilization, especially in the current pre-crisis conditions. The same applies to the potential withdrawal of funds from the US bank accounts - the same Saudi Arabia accounts for a third of foreign

17 Largest Sovereign Wealth Funds by Assets Under Management// Sovereign Wealth Fund Rankings. Sovereign Wealth Fund Institute website. URL: http://www.swfinstitute.org/sovereign-wealth-fund-rankings/ (last accessed date: 18.10.2016). exchange reserves on foreign deposits (as of July - $ 184 billion.18)

Thus, the potential for a negative impact on the stability of the US financial market from Saudi Arabia and its allies and partners on the Council of Cooperation of the Arab States of the Persian Gulf

is possible, and this potential is serious enough to cause the strong decline of quotes in many sectors of the US financial market. The question in this connection is whether Saudi Arabia will go to such confrontation, the economy of which is currently in an extremely tense situation.

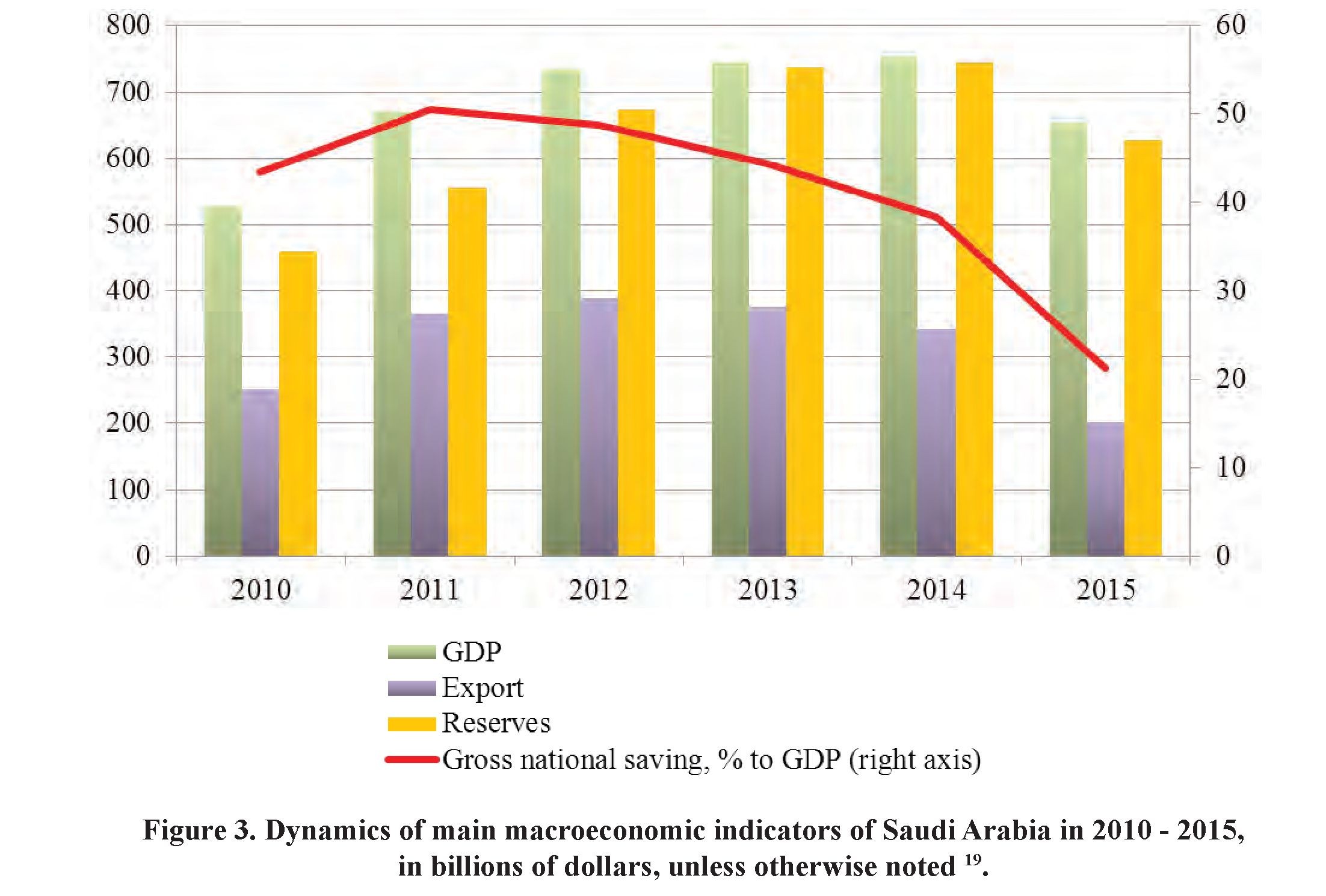

The fall in oil prices in the second half of 2014 and their further decline during 2015 greatly complicated the situation in key areas of the Saudi economy. Virtually all major macroeconomic indicators have been declining for two consecutive years (Figure 3), and by the end of 2016, this trend will continue. The factor most affected by the decline in oil prices was exports, which fell by almost half compared to the level of 2012, the rate of gross national savings, as well as the amount of international reserves, which is one of the main factors of the potential pressure of the kingdom on the United States.

18 Monthly Statistical Bulletin. July 2016. Saudi Arabia Monetary Agency, August 2016. SAMA website. URL: http://www. sama.gov.sa/en-US/Indices/Pages/Financial.aspx (last accessed date: 27.09.2016).

19 Calculated according to the data from the following sources: World Economic Outlook Database, April 2016. IMF website. URL: http://www.imf.org/external/ns/cs.aspx?id=28 (request date: 25.09.2016); Total reserves (includes gold, current US$). The World Bank website. URL: http://data.worldbank.org/indicator/FI.RES.TOTL.CD?locations=SA (request date: 26.09.2016); Goods and Services (BPM6): Exports and imports of goods and services, annual, 2005-2015// UNCTADStat. United Nations Conference on Trade and Development website. URL: http://unctadstat.unctad.org/wds/TableViewer/tableView.aspx (дата обращения: 30.09.2016).

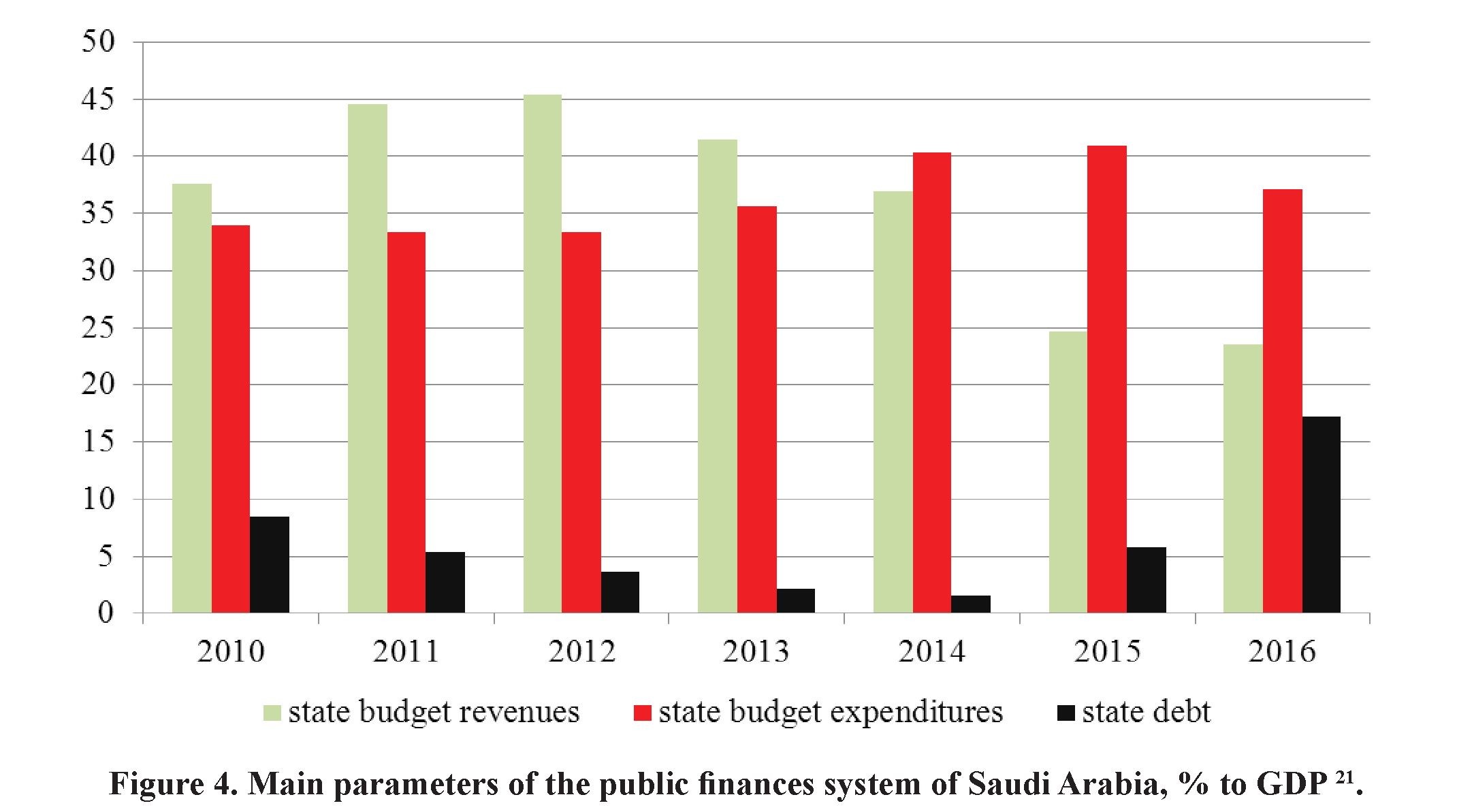

Economic slowdown and export earnings as a natural result have caused the reduction of government revenues with the assumption that the costs have continued to increase. As a result, the budget deficit has rapidly increased: if in 2012 the budget had a proficit of 12% of GDP, then the deficit formed in 2014 had reached 16.3 % of GDP 20 by 2015. Due to

this rapidly progressive budget deficit, Saudi Arabia’s public debt dramatically increased from 1.6% of GDP in 2014 to 17.2 % of the expected IMF according to the results in 2016. The dynamics of deterioration of the main parameters of the public finances system of the Kingdom over the last years is shown in figure 4.

The dramatically aggravated budget problems have forced the Kingdom to resort to external borrowing, for the first time in the past fifteen years. By April 2017, Saudi Arabia had applied for a five-year credit to the syndicate of foreign banks to the amount of 10 billion dollars. Earlier, in March 2015, state oil company Saudi Arabian Oil Co. (Aramco) signed an agreement on attraction of reserve revolving credit from a group of international banks for a total amount of 10 billion dollars.

The solution to the budget problems is not implemented by the attraction of debt financing alone, but other measures either on the expense item or revenue side of the budget. This year, Saudi Arabia was forced to start the reduction of expenses. In particular, in September, Salman bin Abdul-Aziz al-Saud, the King of Saudi Arabia, issued some decrees on the reduction of salaries and payments to state officials including Ministers and Deputies of the Consultative Council (Majlis ash-Shura) by 15-20 %. Other

20 Source: World Economic Outlook Database, April 2016. IMF website. URL: http://www.imf.org/external/ns/cs.aspx?id=28 (request date: 25.09.2016).

21 Calculated according to the data of IMF: World Economic Outlook Database, April 2016. IMF website. URL: http://www. imf.org/external/ns/cs.aspx?id=28 (request date: 25.09.2016).

expenses were also subject to reduction: provision of money for payment of housing and car servicing to public persons. In addition, the Kingdom is trying to find additional sources of income – from exotic incomes (increase in cost of entry visas and payment for departure from the country) - to the privatization income – entry of the largest oil company Saudi Aramco to IPO, plans for which were announced at the beginning of 2016.

In addition to the aggravation of a situation in public finance, problems in the financial sector are generally possible. In particular, a serious lack of liquidity is outlined by the banks, being that the state performs the bond flotation for financing of fiscal deficit that link the bank liquidity, as well as withdraws the funds from bank deposits. As a result of these actions, the inter-bank market rates were increased three-fold – which was the highest they have been since the failure of the Lehman Brothers’ American bank in the period of past crisis. Banks of the Kingdom have repeatedly appealed to the authorities for provision of liquidity. In June 2016, Saudi monetary regulator, Agency of monetary circulation of Saudi Arabia (SAMA) allocated 15 billion riyals (about 4 billion dollars), in September there was a second injection of liquidity into the banking system in the amount of $ 5.3 billion dollars, and other monetary easing measures were announced. The stock market of Saudi Arabia descended by two times in a period of reduction of oil prices - from almost 11,000 items on Tadawul index in September 2014 - to 5,500 items in October 2016.

Accordingly, Saudi Arabia’s current economy is in a very difficult situation, which seen over decades is unprecedented - the prospect of riyal devaluation is current for the first time; the reduction of budget expenditures is affected; and they are prepared for the denationalization of the oil sector. In these circumstances, a deliberate aggravation of relations with a key partner – the USA – seems a very irrational step, and its probability can be assessed as very small regardless of the emotional background specified by the JASTA adoption.

On the other hand, the threat to Saudi investments in the USA is real; and this threat, in our opinion, will force the state to take steps to minimise it by withdrawing their resources from American assets. The probability of arrest and confiscation of assets, belonging to the state, provides the necessity of withdrawal of all funds of state origin, including investments of monetary regulator SAMA, the state investment fund and other government organizations. Regardless of classification of such actions (defiantly confrontational or highly technical and not advertised), they will have a certain effect for those markets where the investments of the Kingdom were the highest.

There are three such main markets (informal markets – for example, fixed assets - in this case it is possible not to take it into account because of their less expressed reaction on this factor) – government liabilities, corporate bonds, and stock market. Concerning the potential impact of possible massive sales of the assets from the markets of Saudi Arabia to their stability we can judge by volumes and shares of the presence of Saudi capital on it. These indicators are extremely low – not only relative to the total volumes of these markets, but even in comparison with foreign investments into the respective assets (Table 3).

As can be seen from the data set out here, the share of Saudi Arabia among the total volume of foreign investments both as a whole on the securities market and on their key segments, is small. Investments from the Kingdom into non-state papers (shares and corporate bonds) are very small; their presence is more significant in the treasury bonds markets and the obligations of various government agencies. However, in the case of treasury obligations, the share of Saudi funds is insignificant and cannot become a significant factor in the destabilization of their market; and the bond market of government agencies is relatively small and due to limited sizes cannot have a significant impact on the financial stability of the USA. Here, it may be noted also that Table 3 shows the data on all types of Saudi investments, not only originating from the state; while the threat of assets being frozen applies only to state funds and this threat provokes the withdrawal of only these investments. Private and corporate investments will not necessarily be derived from American assets, i.e., the funds appearing in Table 3, can be transferred not completely, but partially, and this fact also reduces the potential negative effect from the withdrawal of Saudi funds from the USA.

|

All types of capital issues |

Treasury obligations |

Obligations of USA Agency |

Corporate and other obligations |

Shares |

|

|---|---|---|---|---|---|

|

Saudi Arabia |

147,220 |

94,222 |

7,244 |

10,525 |

35,229 |

|

Total foreign investments |

16,535,316 |

5,568,404 |

965,706 |

3,594,363 |

6,406,843 |

|

Including state investments |

5,200,894 |

3,733,964 |

449,920 |

165,624 |

851,386 |

|

Share of Saudi Arabia in total volume of foreign investments, % |

0.9 |

1.7 |

7.4 |

0.3 |

0.05 |

Table 3. Investments by Saudi Arabia into main types of USA financial assets in comparison with the general volume of foreign investments by million dollars 22.

As for the withdrawal of Saudi Arabia from the American banks, it has already begun, but much like the situation with the assets of the securities market, it has limited potential. The scope of liabilities of the American banks to the investors from Saudi Arabia is decreased by more than two times – from 33.6 to 14.7 billion dollars23 since the beginning of 2016.

- Prepared according to the data of USA treasury: TABLE 1D: U.S. Long-Term Securities Held by Foreign Residents in July 2016// Securities (B): Portfolio Holdings of U.S. and Foreign Securities// Treasury International Capital (TIC) System - Home Page. U.S. Department of the Treasury website. URL: https://www.treasury.gov/resource-center/data-chart-center/tic/Pages/ ticsec2.aspx (request date: 19.10.2016).

- Total Liabilities to Foreigners by Type and Country Saudi Arabia (45608)// Treasury International Capital System (TIC)// U.S. Banking Liabilities to Foreigners by Country. U.S. Department of the Treasury website. URL: https://www.treasury.gov/resource- center/data-chart-center/tic/Pages/country-liabilities.aspx (request date: 19.10.2016).

- Total Liabilities to Foreigners by Type and Holder 1/ as of: August 2016// U.S. Financial Firms' Liabilities to Foreign Residents// Treasury International Capital (TIC) System - Home Page. U.S. Department of the Treasury website. URL: https://www.treasury. gov/resource-center/data-chart-center/tic/Pages/ticliab.aspx (request date: 19.10.2016).

Consequently, the total volume of liabilities of American banks to foreign investors was measured as 4,971 billion dollars24, i.e. the share of deposits from Saudi Arabia is only 0.3 % that does not allow considering the outflow of Saudi contributions as any significant factor of the potential destabilization of American banking system.

A review of Saudi capital presence in the USA’s financial market shows that their share is extremely small in all the main sectors; and the commenced withdrawal cannot have a significant impact on the quotation of securities or destabilize the banks.

At the same time, the negative impact of the withdrawal of Saudi Arabia may appear on the market of treasury obligations if it coincides with the actions of other factors that are also emerging and can mutually complement each other in the process of loosening the market and reducing the quotations of these financial instruments, creating a kind of “resonant” effect. Withdrawal of state funds of Saudi Arabia from American debt securities occurs against the background of accrued pressure on this market associated with two main factors – similar measures (withdrawal of standby funds), People's Republic of China and some other Central banks, as well as the peculiarities of monetary policy of RFC.

Over the past few months, the decrease of treasury obligation volumes is recorded not only for Saudi Arabia, but generally for sovereign holders of USA state debt as well as acceleration of sales of these security papers. So for the last 12 months, these holders have sold the treasury obligations in the amount of 346,4 billion of dollars “unprecedented amount of volume” 25. Currently the biggest seller is China, facing pressure on the rate of yuan, and forced to support it by intervention from the reserves, for which purpose the sale of part of the reserve assets is required, including treasury obligations of the USA. China sold those securities for 34 billion dollars in August, which was the highest figure since December 2015 and reduced the volume of Chinese investments in it up to at least 1,185 billion dollars since November 2012.

The situation with sales of US state debt by foreign government holders has been observed for a long time since the end of 2014, which makes the reduction of foreign investments in the securities of treasury as a whole (Fig.5).

Consequently, the two-year trend of sales of treasury obligations by sovereign holders is supported by growth in the area of non-state investors in recent months, with the result that the total volume of net purchases by all foreign investors has gone into the red. This negative trend is a factor in reducing the attractiveness and price of USA bond of obligations and the growth of their profitability that was observed in the same months and was very intensive - from 1.5% in June to 1.8% in October.

The uncertainty of the monetary policy of the FRS brings pressure on the bond market too, which did not dare to raise rates throughout 2016, thereby supporting the riskappetite of investors in the stock and other markets, and reducing the flow of funds into government stock. The disadvantage of these funds (continually increasing due to the growth of state debt with their offer) also contributes to the gradual growth of treasury obligations

profitability and as a consequence – increase of expenses for debt service.

Against the background of a difficult situation in the market of USA treasury obligations, there appeared in progressive reduction of demand, the reduction of prices and growth of profitability, rapid withdrawal of these securities and the reserve funds of Saudi Arabia (and maybe its allies in the face of other monarchies of Arabian Peninsula) can be one of the factors of escalation of the crisis in the market of American state debt, or at least – a significant increase in the cost of its maintenance. According to our assessment, in

the event of Saudi Arabia entirely getting rid of its American obligations, the withdrawal of remaining funds (even if they are evaluated at a minimum only in accordance with statistics of treasury in the amount of about 95 billion dollars) over several months may lead to a growth in profitability up to the level of about 2-2.3 % per annum with a current 1.75-1.8%27.

Such a scenario could have long-term negative consequences for the system of state finances in the USA and even for global financial stability as a whole. In that case, if the profitability of American obligations rises to a level of above 2% and stays there, there

- The world's Central Bank arrange a record-breaking sale of treasuries. Economy News, 19.10.2016 08:34. URL: http://www. vestifinance.ru/articles/76457 (request date: 20.10.2016).

- Calculated according to the data of USA treasury: Net Purchases Of U.S. Treasury Bonds & Notes By Major Foreign Sector: Foreign Official Institutions, Other Foreigners, And International & Regional Organizations// Securities (A): U.S. Transactions with Foreign-Residents in Long-Term Securities// Treasury International Capital System (TIC)// U.S. Banking Liabilities to Foreigners by Country. U.S. Department of the Treasury website. URL: http://ticdata.treasury.gov/Publish/tressect.txt (request date: 19.10.2016).

- According to ten year obligations

is a threat of its further growth due to technical reasons caused by market conditions. A further increase in the cost of state debt servicing with the prospect of increasing profitability up to 3-4% could have disastrous results for the Federal budget process. In future years, it would mean around a doubling of budget expenditures on interest payments, a reduction of costs for other items, and an acceleration of the process of state debt accumulation and its output to completely unprecedented levels.

Prevention of this scenario will force the FRS to follow a rigid monetary policy aimed at increasing investments into treasury obligations and reducing their profitability. In turn, such a policy would be a major factor in the disruption of most markets, including stock and commodity, which may lead to a new cycle of the global financial crisis. This scenario may be quite possible in the case that the courts of the USA satisfy the claims against Saudi Arabia by the law of JASTA, and there will be the first arrests and confiscation of sovereign assets of the Kingdom in the frame of execution of court decisions that provoke panic and a very quick withdrawal of the remaining funds.

There is another scenario, without a strong negative impact on the markets of introduction into effect of JASTA. Prevention of shock is possible if the withdrawal of Saudi capital from USA is not accompanied by a strengthening of their influence at the expense of the factors discussed above – the withdrawal of funds by other foreign sovereign holders and the tough monetary policy of FRS. This is possible in the case of significant improvement of the global economic situation, which will interrupt a decrease of the reserves of developing countries, which makes them sell American obligations as well as maintaining a soft line in FRS policy. However, in our view, this development now appears to be somewhat unlikely.

REFERENCES:

- V. Katasonov JASTA – A mine for America and global financial system. Fund of strategic culture, 3.10.2016. URL: http://www.fondsk. ru/news/2016/10/03/jasta-mina-pod-ameriku-i-mirovuju-finansovu- sistemu-42713.html

- Official at Ministry of Foreign Affairs: JASTA great concern to community of nations objecting to erosion of prin-ciple of sovereign immunity. Saudi Press Agency, Thursday 1437/12/27 - 2016/09/29. URL: http://www.spa.gov.sa/viewstory.php?lang=en&newsid=1543953.

- M. Mazzetti. Saudi Arabia Warns of Economic Fallout if Congress Passes 9/11 Bill. The New York Times, April 15, 2016. URL: http://www. nytimes.com/2016/04/16/world/middleeast/saudi-arabia-warns-ofeconomic- fallout-if-congress-passes-9-11-bill.html?_r=0. А. Wong, L. McCormick. Saudi Arabia's Secret Holdings of U.S. Debt Are Suddenly a Big Deal. Bloomberg, January 22, 2016. URL: http://www. bloomberg.com/news/articles/2016-01-22/u-s-is-hiding-treasury-bond-data- that-s-suddenly-become-crucial.

- World Development Indicators// World Databank. The World Bank website. URL: http://databank.worldbank.org/data/reports.aspx?Code=NY. GDP.MKTP.CD&id=af3ce82b&report_name=Popular_indicators&populart ype=series&ispopular=y#.

- World Trade Statistical Review 2016. World Trade Organization website. URL: https://www.wto.org/english/res_e/statis_e/wts2016_e/ wts16_toc_e.htm

- Foreign Trade. U.S. Census Bureau website. URL: https://www.census. gov/foreign-trade/statistics/highlights/top/top1512yr.html.

- Foreign Direct Investment (FDI): SAUDI ARABIA// Select USA government program website. URL: https://www.selectusa.gov/servlet/ servlet.FileDownload?file=015t0000000LKNG.

- FDI stocksOutward / Inward, Million US dollars, 2015// FDI stocks// OECD Data. OECD website. URL: https://data.oecd.org/fdi/fdi-stocks.htm.

- Foreign direct investment: Inward and outward flows and stock, annual, 1980-2014// UNCTADStat. United Nations Conference on Trade and Development website. URL: http://unctadstat.unctad.org/wds/ReportFolders/ reportFolders.aspx.

- Major Foreign Holders of U.S. Treasury Securities// Securities (B): Portfolio Holdings of U.S. and Foreign Securities. U.S. Department of the Treasury website. URL: https://www.treasury.gov/resource-center/data- chart-center/tic/Pages/ticsec2.aspx.

- Monthly Statistical Bulletin. July 2016. Saudi Arabia Monetary Agency, August 2016. SAMA website. URL: http://www.sama.gov.sa/en- US/Indices/Pages/Financial.aspx.

- Major Foreign Holders of U.S. Treasury Securities// Securities (B): Portfolio Holdings of U.S. and Foreign Securities. U.S. Department of the Treasury website. URL: https://www.treasury.gov/resource-center/data- chart-center/tic/Pages/ticsec2.aspx

- Memorandum Item: Securities Held in Custody for Foreign Official and International Accounts: Marketable U.S. Treasury Securities// FRED Economic Data. Federal Reserve Bank of St. Louis website. URL: https:// fred.stlouisfed.org/series/WMTSECL1#0.

- Largest Sovereign Wealth Funds by Assets Under Management// Sovereign Wealth Fund Rankings. Sovereign Wealth Fund Institute website. URL: http://www.swfinstitute.org/sovereign-wealth-fund-rankings/.

- World Economic Outlook Database, April 2016. IMF web-site. URL: http://www.imf.org/external/ns/cs.aspx?id=28.

- Total reserves (includes gold, current US$). The World Bank website. URL: http://data.worldbank.org/indicator/FI.RES.TOTL.CD?locations=SA.

- Goods and Services (BPM6): Exports and imports of goods and services, annual, 2005-2015// UNCTADStat. United Nations Conference on Trade and Development website. URL: http://unctadstat.unctad.org/wds/ TableViewer/tableView.aspx.

- TABLE 1D: U.S. Long-Term Securities Held by Foreign Residents in July 2016// Securities (B): Portfolio Holdings of U.S. and Foreign Securities// Treasury International Capital (TIC) System - Home Page. U.S. Department of the Treasury website. URL: https://www.treasury.gov/resource-center/ data-chart-center/tic/Pages/ticsec2.aspx.

- Total Liabilities to Foreigners by Type and Country Saudi Arabia (45608)// Treasury International Capital Sys-tem (TIC)// U.S. Banking Liabilities to Foreigners by Country. U.S. Department of the Treasury website. URL: https://www.treasury.gov/resource-center/data-chart-center/ tic/Pages/country-liabilities.aspx.

- Total Liabilities to Foreigners by Type and Holder 1/ as of: August 2016// U.S. Financial Firms' Liabilities to Foreign Residents// Treasury International Capital (TIC) System - Home Page. U.S. Department of the Treasury website. URL: https://www.treasury.gov/resource-center/data- chart-center/tic/Pages/ticliab.aspx.

- The world's Central Bank arrange a record-breaking sale of treasuries. Economy News, 19.10.2016 08:34. URL: http://www.vestifinance.ru/ articles/76457.

- Net Purchases Of U.S. Treasury Bonds & Notes By Major Foreign Sector: Foreign Official Institutions, Other Foreigners, And International & Regional Organizations// Securities (A): U.S. Transactions with Foreign- Residents in Long-Term Securities// Treasury International Capital System (TIC)// U.S. Banking Liabilities to Foreigners by Country. U.S. Department of the Treasury website. URL: http://ticdata.treasury.gov/Publish/tressect.txt.