With Russian ruble crumbling, oil prices in freefall and Kazakhstan economy suffering the consequences the looming crisis it may seem the worst time for Kyrgyz state to enter the Eurasian Economic Union. Yet the ruling coalition, the Government and the President, are demonstrating readiness to enter the Union by May 9th with the agreements signed and roadmaps approved. The reason is, as stated in the local media “because it is lesser of evils” with implications being geopolitical pressure rather than economic interest the main motivator of entering the Eurasian Economic Union. This summarizes the general mood that is prevailing in Kyrgyz society at the moment.

The paper describes the studies made to forecast the impact the membership in the Customs Union on the economy of Kyrgyzstan as the factors and trends revealed then are still true for the Eurasian Union’ effects. It proceeds to discuss the estimations of the effects on the national economy made while taking into account the Eurasian Economic Union membership.

The following benefits of the EEU member ship are suggested as potential advantages of entering the Eurasian Economic Union:

- access to the common market with 170 million potential for Kyrgyz goods;

- free movement of capital, services, goods and labor, with special emphasis made on possible improvement of the labor conditions for the migrants from the country;

- easy access to fuels and commodities such as grain, wood, steel, oil, gasoline.

First. there were efforts taken to predict the impact of the membership in the Customs Union (Eurasian Union predecessor) for the national economy bearing that the effects might be both positive and negative. The meetings were held with the representatives of the ministries and departments, namely the Eurasian Service, Ministry of Economic Affairs, Ministry of Labor, Migration and Youth and Ministry of Foreign Affairs of the Kyrgyz Republic. As a result, the following types of possible shocks were identified in order to be applied in the simulation:

- trade (price) shocks: changes in the import tariffs;

- investment shocks: changes in the level of FDI and total factor productivity.

Given the above mentioned impact on the national economy, three basic scenarios were elaborated with the government measures taken accordingly, namely Baseline Scenario, Introduction of Import Tariffs Scenario and Export Facilitation Scenario.

Baseline Scenario actually captured the prevailing trends in the economy and in particular: the average moderate GDP growth, macroeconomic imbalances in the economy associated with high budget deficits. The role of Baseline Scenario was important because only in the comparison with the effect of comparative modeling one can identify any shock. That is, the use of shock should show whether there is an increase in the rate of economic growth or slowdown compared to the baseline scenario.

Introduction of Import Tariffs Scenario simulated the impact of the introduction of import tariffs only as a result of the adoption of the common tariff of the Customs Union. Exports Facilitation Scenario dealt with the reducing barriers on the exports to the Customs Union making the Kyrgyz entrepreneurs to decease the prices on the goods they are to sell. These two scenarios were the key, since these effects would be manifested when joining the Customs Union with a high degree of probability and the introduction of new import duties were imminent. A number of other calculations were FDI, total factor productivity and migration modeling. However, the emergence of such shocks could not be attributed to the shocks with a high proportion of the probability of their occurrence. Therefore, these calculations were not attributed to the basic scenario.

General Equilibrium Model

Tool for this evaluation is a general equilibrium model (MAMS Maquette for MDG Simulations) developed by a group of the World Bank researchers. This model has been developed in relation to the economic system of Kyrgyzstan in order to analyze its economic policy. The main source of the data for this model is a social accounting matrix (SAM) which is an extended version of the inter-industry balance.

The model consists of 66 equations that describe the entire economy, including:

- prices: export, import, domestic commodity, producer prices, consumer price index, etc.;

- production: aggregate supply and demand, GVA, production of goods, gross output, labor and so on;

- institutions: taxes, savings, net income transfers, consumption and so on;

- investment: foreign direct investment (FDI), public investment, the balance of payments and fixed assets, total factor productivity etc.

It should be noted that the modification of the model used has some limitations, particularly there are only two regions in the model: Kyrgyzstan and the rest of the world. Subsequently, the model requires that the main shocks were calculated in advance on the basis of the weighted average of the commodity turnover between the countries that are CU members and non-CU countries. Therefore, the model does not take into account the trade reorientation resulted of the changes in the import duties. This issue was resolved by applying the methods listed below.

Methods for Calculating Main Shocks

The change in import tariffs after joining the CU changed the prices on the imported goods. The equation of the import prices in the model is PM_ (c, t) = pwm (c, t)· (1 + tm(c, t)) · EXR_t+

∑c͵ϵC (PQc͵t ∙icm c͵, c, t) where PM_ (c, t) is the price of the imports in period t; pwm_ (c, t) is the average import price; (1 + tm_ (c, t)) is the effect of import tariffs; EXR_t is the exchange rate and ∑c͵ϵC (PQc͵t ∙icm c͵, c, t is the transaction costs (transport costs) [1].

In this model, the effect of the transaction costs on the formation of the import price is insignificant when new import tariffs are in troduced. The equation above shows that the import tariff is one of the key factors influencing the formation of the import price.

To determine the effect of the import tariff on the price the average tariffs were weighted for the each of the branches used in the model. In order to do that, the data provided by the Kyrgyz Eurasian Service in 2012 on the imports in all commodity groups (97 commodity groups, each with an average of 20 product categories) was used. As for the commodity sectors of industry, the aggregation model was produced in accordance with the agreement encodings the HS classifications and GKED. The next step was to calculate the average product for each sector on as well as the tariffs to be applied in Kyrgyzstan the basis of the currently existing import tariffs after joining the Customs Union (Table 1).

Table 1. Average Tariffs on Imports by Industry

|

Industry |

before joining CU,%, average |

after joining CU, % |

|

agriculture, forestry, fisheries |

0,905 |

1,375 |

|

fuel production |

0,062 |

0,015 |

|

metal mining and others. Minerals |

0,846 |

1,296 |

|

food industry |

2,763 |

9,164 |

|

light industry |

8,837 |

11,110 |

|

woodworking, paper, publishing |

0,109 |

6,276 |

|

chemical and petrochemical industry |

0,975 |

6,269 |

|

manufacture of other non-metallic mineral products |

5,764 |

10,757 |

|

metallurgical industry |

0,007 |

3,783 |

|

manufacture of metal products |

1,279 |

7,965 |

|

engineering |

4,799 |

3,760 |

|

other manufacturing industries |

2,049 |

11,939 |

Source: Eurasian Service of Kyrgyzstan, (calculated by author)

The table above shows that the weighted average tariffs on imports virtually for all industries were expected to grow, due to a significant increase in tariffs on imports from countries outside the Customs Union. On average, estimated increase was more than three-fold for the tariffs on imports of food and more than five times in the wood products, chemicals and metal products. Whereas. the import tariffs on engineering products should reduce slightly.

Nevertheless, it was clear that mere simultaneous assessment of the change rate was insufficient since the tariff rates changes might have

prolonged or delayed effects. At the same time, the studies indicated that this effect might be different depending on a particular category of goods. According to the available data Kyrgyzstan imported 49.8% goods from non CU countries 11.4% of goods were imported exclusively from the CU countries and 38.8% from both. This means that there are different scenarios of the changes in the structure of imports, which would entail change in the import tariffs. To assess the changes in the structure of imports two hypotheses were proposed.

According to the “Substitutable Products” Hypothesis due to the availability of the substitute goods more types of goods are more likely to be imported from the CU countries rather than from non-CU countries and the import tariffs for the countries outside the CU would grow.

According to “Inelastic Non substutitable Imported from non-CU Countries” Hypothesis the increase of the tariffs for certain types of the goods imported of non-CU countries would not change the structure of import as there were no alternative available to import then the CU countries.

The first hypothesis meant that since the new tariffs in the CU should be greatly reduced, the importers would switch on importing the certain goods from the Union instead of from elsewhere as it would be cheaper. But according to the second hypothesis, some categories of goods would be still imported from non-CU countries, despite the estimated increase in their prices.

Based on the hypotheses above new average tariffs were calculated with delayed effects on the import prices and, as a consequence, the structure of imports. For this purpose, the so- called “price flexibilities” were calculated on the basis of how historically the change of the structure of imports depended on the changes in prices for the period from 2008 to 2012 (Table 2).

Table 2. Flexibility of Import Structure of from Non-CU Countries, by Price

|

Industry |

Flexibility 12-08 |

Flexibility 12-09 |

Flexibility 12-10 |

|

agriculture, forestry, fisheries |

-4.10 |

-0.98 |

-8.78 |

|

fuel production |

-0.85 |

-2.75 |

-2.18 |

|

metal mining and others. minerals |

-0.85 |

-2.75 |

-2.18 |

|

food industry |

-0.52 |

-2.69 |

-2.85 |

|

light industry |

-0.29 |

-1.31 |

-6.03 |

|

woodworking, paper, publishing |

-2.11 |

-8.67 |

-9.80 |

|

chemical and petrochemical industry |

-0.85 |

-2.75 |

-2.18 |

|

manufacture of other non-metallic mineral products |

-0.17 |

-0.13 |

-0.91 |

|

metallurgical industry |

-0.99 |

-4.36 |

-2.07 |

|

manufacture of metal products |

-0.41 |

-1.72 |

-5.24 |

|

engineering |

-0.85 |

-2.75 |

-2.18 |

|

other manufacturing industries |

-0.17 |

-2.55 |

-2.69 |

Source: Akeleev, A., Hasanov, R., Attokurov et al . 2014. Analysis of consequences of entering Eurasian Union for Kyrgyz Republic

Table 2 shows how the structure of imports from the non-CU countries change when the price changes by 1%. For example, the average growth of 1% on the substitutable products in the food industry would reduce the proportion of these products in the import from the non-CU by 2.85% in the first two years; by 2.69% in the first three years, 0.52% in the next four years.

Based on the calculated flexibilities and the data on the average tariffs after joining the CU, a by-industry forecasts were made taking the average tariffs from CU and non-CU countries. Thus, the prolonged of the growth of import prices on the structure of the trade between the CU and non-CU countries was estimated based on the formula above and the price shock was modeled (Table 3). The calculations cover the period until 2019 meaning that the trends reveals are also relevant for the Kyrgyzstan’s membership in the Eurasian Economic Union.

Table 3 shows the changes of the average price of the imported goods in each sector of the industry given that the base price is taken as 1. Thus, having 2014 as the base price, all sectors are expected to face the increase in import prices during the period from 2015 to 2019. (excluding fuel production and engineering). A slight increase in the prices is expected in imports of agriculture, mining and other metals, minerals, iron and steel industry. The most significant increase is expected in the imports of

|

Industry |

2014 |

2015 |

2016 |

2017 |

2018 |

2019 |

|---|---|---|---|---|---|---|

|

agriculture, forestry, fisheries |

1 |

1,005 |

1,002 |

1,002 |

1,002 |

1 |

|

fuel production |

1 |

1,000 |

1,000 |

1,000 |

1,000 |

1 |

|

metal mining and others minerals |

1 |

1,004 |

1,002 |

1,002 |

1,002 |

1 |

|

food industry |

1 |

1,062 |

1,024 |

1,033 |

1,031 |

1 |

|

light industry |

1 |

1,021 |

1,004 |

1,011 |

1,010 |

1 |

|

woodworking, paper, publishing |

1 |

1,062 |

1,013 |

1,035 |

1,031 |

1 |

|

chemical and petrochemical industry |

1 |

1,052 |

1,023 |

1,027 |

1,026 |

1 |

|

manufacture of other non-metallic mineral products |

1 |

1,047 |

1,022 |

1,024 |

1,024 |

1 |

|

metallurgical industry |

1 |

1,000 |

1,018 |

1,019 |

1,019 |

1 |

|

manufacture of metal products |

1 |

1,066 |

1,020 |

1,034 |

1,033 |

1 |

|

engineering |

1 |

0,990 |

0,995 |

0,995 |

0,995 |

1 |

|

other manufacturing industries |

1 |

1,097 |

1,035 |

1,052 |

1,049 |

1 |

Table 3. Changes in Import Prices after Joining the CU/EEU by Industry (price shock)

Source: Akeleev, A., Hasanov, R., Attokurov et al . 2014. Analysis of consequences of entering Eurasian Union for Kyrgyz Republic food, metal products, wood processing industry, non-metallic mineral products, chemical and petrochemical industry and other manufacturing industries.

Change in Foreign Direct Investment

According to the analysis of the investment flows in the various regional groupings, the following assumptions can be made about the change in the flow of foreign direct investment after Kyrgyzstan’s entry into the EEU.

In the first year sharp increase in FDI is expected (threefold net growth in FDI) followed by a slowdown with some postponed increase in total factor productivity.

Consequences of Export Barriers Removed within the Eurasian Union

One reason for regional integration is that it enable to reduce the costs for the business while passing the state borders. According to the report published by the World Bank, the Eurasian Union might contribute into reducing the costs for the Eurasian borders. In general, the most plausible effects are the following:

- barriers of all kind removed throughout the entire Eurasian Union;

- number of documents required for foreign trade reduced and the procedures simplified;

- greater transparency and simplicity resulted in less corruption that, therefore will reduce significantly the transaction costs for importers and exporters

The report was made using the methodology to estimate the border costs via the comparison of the data from Kazakhstan with investigations of Ukraine. According to the report, the costs for the Eurasian borders of Kazakhstan make up 12% of the total trade within the Eurasian Union.

Given the geographical proximity of our countries one can apply this methodology to the case of Kyrgyzstan. Having done this, the author proposes the two possible scenarios.

The first pessimistic scenario suggests that joining the Eurasian Union will not bring expected positive changes in terms of simplification of the red tape and the transaction costs remain the same.

The second optimistic scenario suggests that the membership in the Eurasian Union may result in up to 25% reduce of the costs. In addition, such products as oil, gas, electricity, minerals will not be affected by the mechanisms aimed at the reduction of the transaction costs.

The Eurasian Union practices so far demonstrate that there is high risk that trade barriers and non-tariff policies would be arbitrarily implemented. Moreover, it is important to bear

in mind that the dispute resolution mechanisms within the Union are underdeveloped and lack legitimacy with some national governments and institutions. This has led to continued trade disputes and decreased competitiveness of smaller economies within the Union.

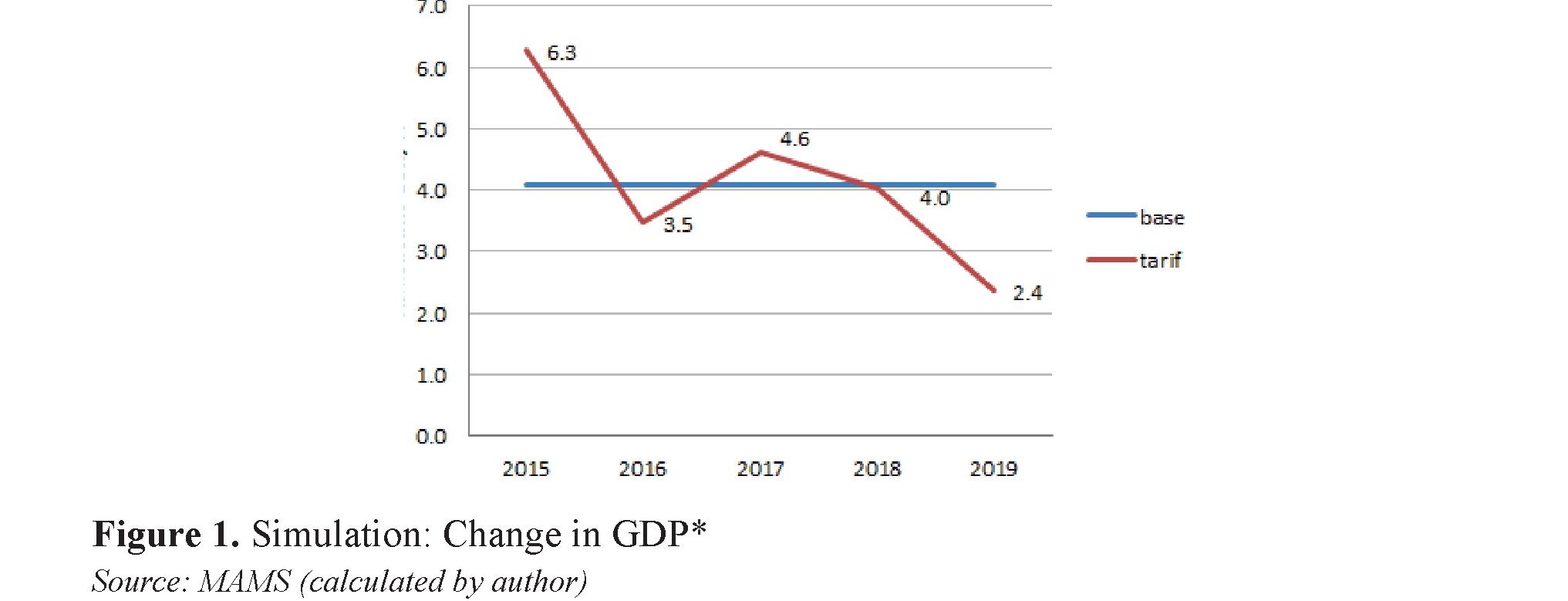

Increased Import Tariffs Simulation showed that the most significant effect the economy

Kyrgyzstan will be on trade meaning the price shocks, namely the increase of the import tariffs. Figure 1 shows possible developments provided the change of GDP, the data obtained via modeling the changes in the import prices.

Fig. 1 shows that in the first year after join ing the EU, a sharp increase in GDP (to 6.3%) is expected with the main reason for growth being the improvement in the net exports (see. Fig. 2 and 3) due to a significant increase of the import tariffs leading to a reduction of imports into Kyrgyzstan.

However, this will not be a long-term effect, further deterioration of trade shall lead to a slowdown in the growth figures as the major

players adapt to the new economic conditions, particularly to the increased import and slowing export growth.

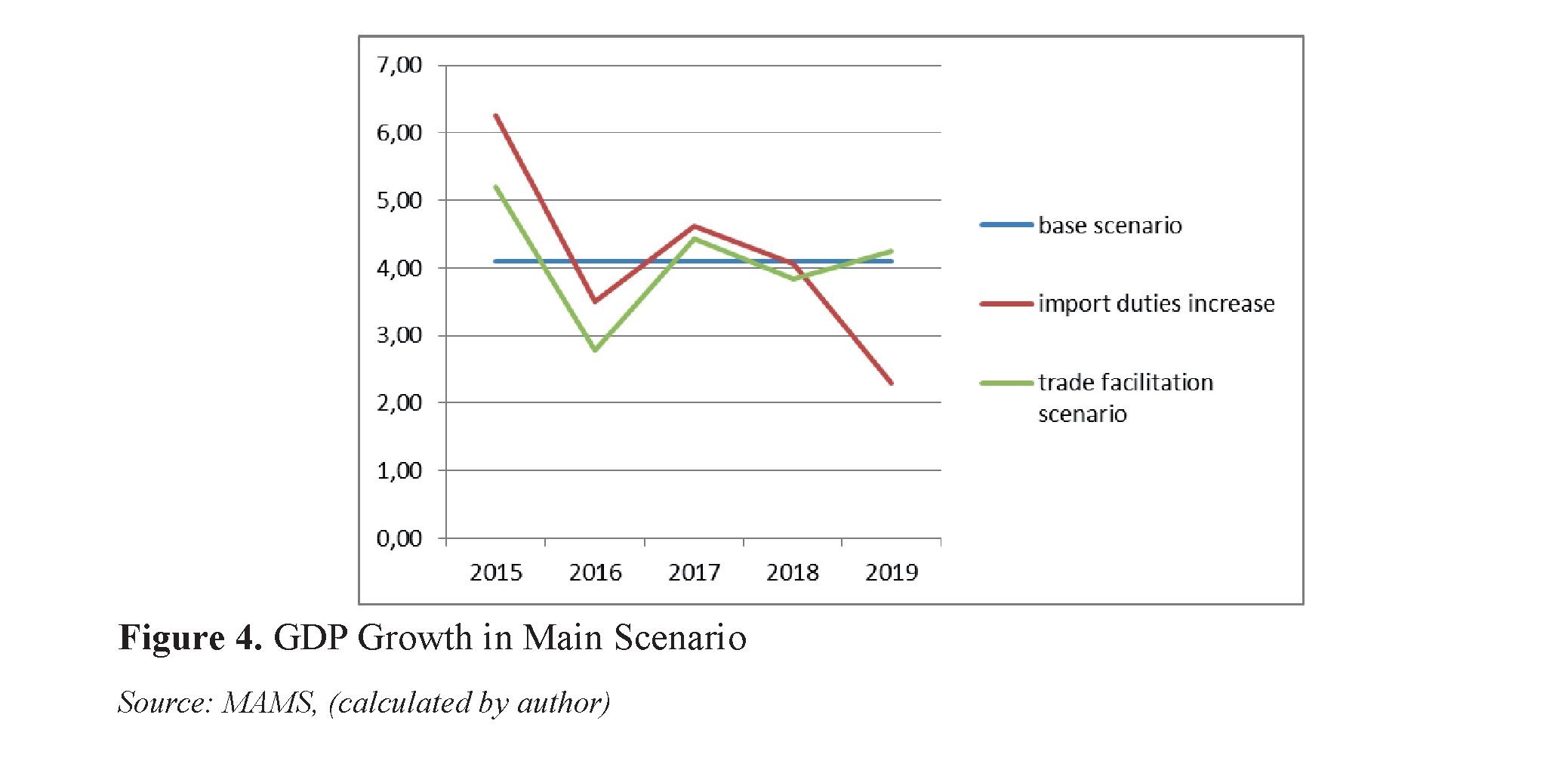

Trade Facilitation Simulation similarly to the scenario above is based on the assumption is that the trade barriers will be significantly reduced as well as the costs of the export to the countries of the Eurasian Union. As it is shown

in Figure 4, the GDP growth will be even higher in comparison with the Introduction of Import Tariffs Scenario above (Figure 3) by the end of the forecast period provided a real reduction in the trade costs.

Figure 4 shows that the average growth rate for the 2016-2019 is 4.10% for Baseline Scenario; 3.50% for Import Tariffs Scenario and 3.76% for Trade Facilitation Scenario.

However, negative development are forecast for 2016-2019 as the effects of the increase in the import tariffs will not be fully overcome. The explanation is that the imported shock of higher value will be received by all industries while the export positive shock will affect smaller number of industries. In this case, there is a negative balance that will also cause the slowdown.

This scenario shows that the GDP growth is possible in the long term after equilibrium is reached by 2019 provided that the export is supported and expanded.

The impact of the increased import tariffs will be positive for Kyrgyzstan during the initial period after joining the EEU and overall government revenues will increase due to the inflows of cash resulted from the increased tariffs. This will create additional domestic demand and thus increase overall GDP growth.

However, the simulations show that due to the increased price of raw materials and imported goods, there will be gradual slump in GDP growth by the second year of the EEU membership. The negative shock during the period of 2016-2019 will be hard to overcome as the competitiveness of the locally manufactured goods will suffer from the high-risk environment resulted from the removed tariffs.

It is important to note that this article and the modeling it analyses does not take into account very important recent developments.

The first is the current crisis in Russia and estimated GDP slowdown of -3-4%. This affects the all figures in the analysis (mainly migration and export) negatively. The second factor is potential demands for compensation and settlement conditions from the current WTO trading partners that may amount to $1.5 billion from China only according to some estimates.

SOURCES:

1. Akeleev, A., Hasanov, R., Attokurov, A. et al. 2014. Analysis of consequences of entering Eurasian Union for Kyrgyz Republic. Ministry of Economic Regulation of Kyrgyz Republic.