Abstract

Object: Annually financial technologies have an increasing impact on the banking sector. The article provides definitions of the term "financial technologies" by international organizations, foreign, Russian and Kazakh experts. In the context of the fourth industrial revolution, the relevance of the topic is justified by a sharp increase in the development of financial technologies and spread of digitalization in the banking sector. The purpose of the research is to survey the impact of digital technologies on the financial sector.

Methods: The main categories of financial technologies in the world and in Kazakhstan, in particular, are considered. The strengths and weaknesses, opportunities and threats of financial technologies in the banking sector are analyzed.

Findings: Digital transformation paves the way for a wide range of mobile data deployments that require ongoing security. In addition, the active development of information technology should stimulate the financial sector to be flexible and apply innovative approaches in all areas. The material also provides the prerequisites and reasons for digitalization in the area of banking services.

Conclusions: The transition of traditional types of banking services to a new level of technological development shows a direct relationship between the development of financial technologies and data security. In this regard, it seems relevant to effectively allocate priorities, taking into account the characteristics and specifics of each subject of banking activities. In an increasingly competitive environment, the most rational and digitally oriented strategy of the bank is becoming important.

The development of information technology has a multiplier effect on the development of society and the state. The client, business and the state have in turn, a direct impact on increasing level of digitalization in society. It should be noted that the priority task of the State Program of the Republic of Kazakhstan "Digital Kazakhstan" is "the development of financial technologies and non-cash payments". In this context, the concept of financial technology in business is largely associated with the wide possibilities of information technologies and Big Data.

According to experts, technological innovations and modern challenges require the banking sector to move away from the traditional practice of providing services to digital. Digital financial services include a wide range of high-tech products, software, new forms of interaction with customers. For this reason, financial technology research in banking is highly relevant.

This article provides the current state analysis, dynamics and growth of services provision in Kazakhstan banks using the “transfer and payment” method. According to the National Bank of the Republic of Kazakhstan, the volume of payments and their number is growing rapidly, which gives rise to risks and opportunities. The SWOT analysis provides a realistic assessment of the strengths and weaknesses, opportunities and threats of the banking sector in Kazakhstan.

The article notes that the focus of banks on the development of financial technologies will further determine their competitiveness. At the same time, security is a basic requirement for customers and partners.

In addition, based on a comprehensive analysis the financial technology, the article provides a detailed overview of the concept of "financial technology".

The development of digitalization and technology has had a huge impact on the emergence of new processes and products in the field of financial services. In 2017, participants of the World Economic Forum described financial technologies as a “digital weapon” that strikes at traditional financial institutions and breaks down barriers (World Economic Forum,2017).

As defined by the Financial Stability Board (FSB), fintech – based on financial innovations that can lead to new business models, applications, processes or products that have a significant impact on financial markets and organizations and financial services (IMF, 2017).

The analysis of the definition of financial technologies is based on the definitions of Kazakh and foreign authors (see Table 1).

Table 1. The concept of financial technologies by Kazakh and foreign authors

|

Year |

Source |

Author |

Definition |

|

2014 |

Deutsche Bank Research |

Dapp T. |

Modern technologies for the provision of financial services in the field of e-commerce, mobile payments or financing of startups at an early stage (crowdfunding, crowdinvesting). |

|

2015 |

Research Paper No. 2015/047 |

Arner D.W. Barberis J.N. Buckley R.P. |

New marriage of financial services industry and information technology. |

|

2016 |

Financial Innovation, |

Zavolokina L. Dolata M. Schwabe G. |

The result of three main factors: organizations, people and geographic location (markets). |

|

2016 |

Problemy ucheta i finansov |

Osipova T.Yu., Klimenko E.N. |

Business processes using new technologies in the field of mobile payments, money transfer, lending, etc. |

|

2017 |

Finance: Theory and Practice |

Maslennikov V.V., Fedotova M.A., Sorokin A.N. |

A complex system that brings together the sectors of new technologies, financial services, start-ups and related infrastructure. |

|

2017 |

European Economy – Banks, Regulation, and the Real Sector |

Navaretti G B Calzolari G Mansilla-Fernández J Pozzolo A F |

Through the development of digital technologies, in the financial services industry new processes and products are becoming available. |

|

2018 |

Jekonomika. Nalogi. Pravo |

Bakulina A.A., Popova V.V |

Market segment in which companies operate at the intersection of traditional financial services and functioning of innovative companies. |

|

2019 |

Bulletin USPTU. Science, education, economy. |

Kurmanova D.A. |

Companies use the new technology and innovation that aims to compete with traditional financial methods in the delivery of financial services. |

|

2020 |

Web of Conferences |

Doszhan R. Nurmaganbetova A. Pukala R. Yessenova G. Omar S. Sabidullina A. |

Providing financial and banking services using modern technological innovations based on computer programs and algorithms. |

|

2020 |

Centr delovoj informacii kapital.kz |

Dzoekaeva A. |

Payment aggregators, p2p lending platforms, instant digital transfer systems, crowdsourcing projects. |

|

Note – compiled by the author |

|||

The literature review revealed common features in the definition "financial technology". In particular, the authors agree that the main components of the term "financial technology" are innovation, digitalization and financial services. It should be noted that the term focuses on technological innovation and technological development. Most fintech companies are rooted in IT companies that create new solutions to the problems and challenges in the financial industry (Gomber, Siering, 2017).

Financial technology is the main driver of traditional financial services evolution. According to the report of the investment company H2 Ventures and KPMG Fintech, the list of the top financial technology innovators from around the world in 2019 was as follows:

- 27 payment and transaction companies,

- 19 companies engaged in private equity and brokerage services,

- 17 insurance companies,

- 15 credit companies,

- 9 Neobanks,

- 13 companies operating in various sectors of financial technology.

According to the Astana International Financial Center, the following companies engaged in the development of financial technologies:

- banks (Kaspi bank, Forte bank, Halyk bank, etc.);

- regulatory authorities (AFSA, National Bank of the Republic of Kazakhstan, Agency of the Republic of Kazakhstan on regulation and supervision of the financial market and financial organizations);

- enterprises (Kazakhtelecom, Beeline, Transtelecom, etc.);

- international payment systems (Kazpost, KASE, VISA, mastercard, etc.);

- venture funds (Qaztech ventures, Samruk Kazyna, Baiterek venture fund);

- accelerators (Astana hub, AIFC FINTECH hub, KAZ FINTECH and others);

- educational platforms (Nazarbayev University, Kazakh British Technical university, AIFC professionals and others);

- payment solutions (Senim, Paysend, Smart pay and others);

- credit platforms (Altenge, CreditOn, Otbasy 365);

- blockchain solutions (BlockchainKZ, FinTech Group and others).

The perception of fintech in the banking sector is controversial. Financial technologies are, however, threatened by great opportunities and high risks. Thus, the development of financial technologies and its impact on the banking future are extremely relevant. In her article "The influence of financial technologies on the development of the banking sector" Alpatova E.S., identifies the following six prerequisites:

First, the global financial crisis has had a strong impact on the banking sector, which has resulted in customer distrust and increased regulation of banking activities. High costs and strict controls are significantly narrowed the range of services. Startups have more opportunities in the financial sector.

Secondly, with the development of information technology, consumer behavior has changed. As a result, the provision of banking services has become less efficient. Technological innovations and product improvements were required. The development of social networks has also stimulated the new types of services.

Thirdly, the expanded capabilities of mobile communications with Internet access, mobile applications, social networks are set the task for commercial banks to pay attention to the provision of certain types of services in online format, through mobile applications.

Fourthly, the author of the article draws attention to the involvement of the modern generation in digital technologies, as well as their heightened to “easy use of services, quality and speed of obtaining information,” which is engine the development of financial services.

Fifth, the correct response of the banking legislation to innovations is generating an increase in digital technologies in traditional financial institutions.

Sixth, offering of accessible and affordable financial products and services increases the demand among the bank's clients (Alpatova, 2019).

To identify the factors that influence financial technologies in the banking sector, a SWOT analysis was defined as a research method, it also allows account to be taken the internal and external factors of organizations (Timofeeva, Mavrodieva, 2010). The analysis allows to identify the greatest threats to the banking sector, taking into consideration the development of digital technologies and the priority areas of the industry.International and Kazakhstani reports on the classification of categories of financial technologies also became the methodological basis of the study. The statistical research is the use of Internet banking on the territory of the Republic of Kazakhstan. Theoretical and empirical data measure the potential of financial technologies in the banking sector.

Conducting a SWOT analysis will help understand the development of financial technologies in the banking sector in modern conditions and its further trends. (see Table 2) (Pyzhlakov, 2008).

Table 2. Strengths of fintech development in the banking sector.

|

Title |

Description |

|

Provision of services through multiple channels |

ATMs, terminals, Internet banking, mobile banking, to some extent reduce the burden on employees. Banks are placing their surplus workforce in new areas such as product marketing, field surveys, loan repayments. This improves the productivity of banks |

|

A competitive advantage in the market |

Promotes broadened coverage of business and clients |

|

Promotes support common standards in operating procedure, products and services |

Increase the level of credibility of employees and customers, the overall efficiency of the bank |

|

Offering financial services through web platforms, without any geographic restrictions, financial technology allows banks to provide faster and more efficient transactions |

Clients do not have face to face meeting with bank employees, thus, banks can reach a wider customer segment. |

|

Banks can consolidate the complexity of their business |

With the development of advanced technologies, banks can consolidate the complexity of their businesses, increase efficiency, accelerate operations, cost savings and economies of scale. |

|

Note – compiled by the author |

|

The strengths of the development of financial technologies in the banking sector determine the most demanded types of services and directions for further development. In this context, a strong and paramount task is the introduction of advanced technologies in banks, remote and accessible banking services 24/7, will be their competitive advantage (Table 3).

Table 3. Weaknesses of fintech development in the banking sector

|

Title |

Description |

|

Increased demand for qualified personnel to perform complex banking operations |

Due to technology upgrades, banks constantly need renew their personnel through staff rotation |

|

Internet banking is vulnerable to cyber attacks |

This creates the need to implement highly reliable security controls such as biometrics, public key infrastructure and digital signature controls |

|

The accessibility of the Internet, the increased number of owners of a personal computer. The target customer segment is very specific |

Online banking users are people with a high level of education and have a good understanding of IT technologies. For this reason, clients who do not have the skills requesting a bank |

|

One of the main concerns is personal data security and integrity |

There is a need to invest in software security. Account information theft and virus attacks occur with high frequency |

|

Note – compiled by the author |

|

The most expensive for banks can be the threat of cyber attacks and the leakage of information about the customers personal data. Trust is the basis of the relationship between the bank and the client. Online banking should be clear and convenient to reach a larger number of users. At the same time, simplicity and convenience should be combined with a multilevel security system (Table 4).

Table 4. Opportunities for the development of fintech in the banking sector

|

Title |

Description |

|

Digitally maintain customer database |

If you have databases, for certain categories of users there is no need to design others |

|

Standardization of banking products and services |

It has a positive value in increasing the efficiency and availability of similar services for customers and staff. Promotes equal opportunities for all |

|

In addition to a cost-effective marketing channel, online banking provides 24/7 customer service |

Customers can get the latest information on banking products and services. The ability to integrate links to various related services (online trading, stock markets, income tax payments). This will provide a single point for customers and eliminate the effort to switch to other Internet resources. |

|

Internet banking, allows enter new areas (online shopping, marketing and selling products or services) |

Internet banking opens up new opportunities for banks to conclude agreements with various agencies (utilities, education, insurance and others). This creates favorable conditions for business development at minimal cost. |

|

Cooperation between banks and other platforms (online stores, providers) |

Opportunities for opening or buying assets (bonds, options, mutual funds and mortgages), a differentiation of bank services and obtaining competitive advantages |

|

Cooperation between banks and other platforms (online stores, providers) |

Collaboration between banks and other stakeholders lays the foundation for the implementation of new business strategies that bring benefits to both customers and banks |

|

Note – compiled by the author |

|

Interbank cooperation contributes to the creation of a unified database, digitization and automation of customer data. With a wide range of financial products, banks are differentiate services and create new opportunities.

Table 5. Threats to the development of fintech in the banking sector

|

Title |

Description |

|

High tech products have a very short ‘life span’ |

Before introducing any new banking products and services is required a rigorous planning |

|

Due to dependence on third parties, outsourcing of banking processes or activities contains certain operational risks |

The development of financial technologies requires substantial investments. This reduces bank’s mobility and prevents from introducing various programs. In this context, it is necessary to define outsourcing more precisely. Outsourcing reveals the inside secrets of the banks. When switching to outsourcing, it is necessary to take into account the compatibility and standards of banking products and services. In addition to current trends in the banking market, the decision can be made by analyzing the existing infrastructure, the level of personnel qualifications. |

|

The safety of electronic banking has a location risk: natural phenomena (floods, fires, earthquakes) and criminal activities can harm the bank's operations |

Control measurements are needed to mitigate risks, which includes the smooth implementation of security measures and backup systems to avoid loss of financial data and operational disruptions |

|

The growing dependence of financial institutions on information technology has significantly increased the role of information security |

Information security protects, maintains the confidentiality and integrity of customer information. It is necessary to maintain the interest of customers, their level of trust, trust in the products and online services of the bank. Risks can be mitigated by properly deploying security policies, regularly updating antivirus software, implementing biometric measures, public key infrastructure and digital signatures. |

|

Electronic banking is also subject to legal and reputational risks |

Foreign banks may have access to the domestic market and turn it into an aggressive competitive environment by offering more attractive products and better services, which poses a greater threat to banks |

|

Lack effective legal regulations and supervision on the Internet |

The development of information technologies requires an adequate legal framework that meets modern requirements. In case of financial losses of customers or other situations, there are no appropriate compensation measures. |

|

Note – compiled by the author |

|

Through the SWOT analysis, the following parameters were identified as the most important to qualitatively increase the level of digitalization of services in banks. The development of digital technologies must occur in all areas of banking services simultaneously. This will lead to tremendous changes in the financial sector. High competition in the domestic and foreign markets should stimulate banks to use a customer-oriented approach. At the same time, the security system of banks should be ahead and anticipate the risks associated with the development of digitalization.

The development of financial technologies in the banking sector of Kazakhstan is increasing every year. Modern technologies are being introduced: blockchain, artificial intelligence, Bigdata, biometrics technologies for personal identification (Bizhikeeva, 2020). Compare the global dynamics of the use of financial technologies, most of the transactions are in the banking sector.

According to the EY’s Global Fintech Adoption Index 2019, money transfers and payments are at the top of the ranking, use of financial technology in this category more than quadrupling over four years, from 18% in 2015 to 75% in 2019. I would like to note that banking services for money transfers and online payments are growing rapidly all over the world.

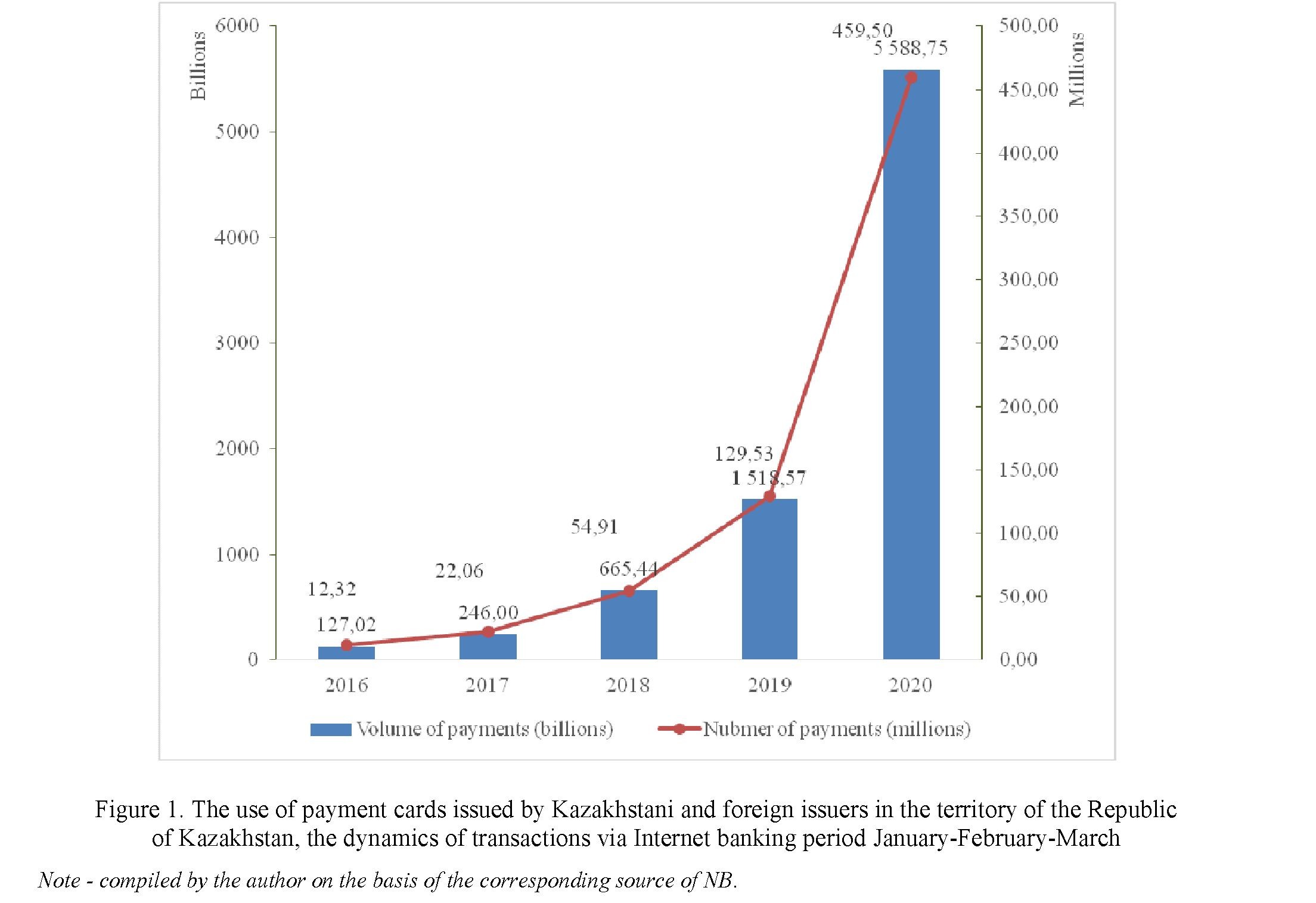

The use of money transactions and payments via Internet banking for the period 2016-2020 in the territory of the Republic of Kazakhstan also increased. Every year, there is an increase in transactions in three to four times. And probably, due to the current situation in the world, the coronavirus pandemic, the use of Internet banking for money transactions and payments will grow steadily. According to the press service of Jýsan Bank, during the state of emergency and the quarantine, there was a change in consumer behavior. The need for a contactless service increased the number of registered users of the bank's mobile application in three times. Jýsan Bank realized the opportunity of online lending, delivery of payment cards, remote account opening, biometric identification and registration (Bizhikeeva, 2020).

According to the analytical center the Association of Financiers of Kazakhstan in 2019, online payments increased by 21% compared to 2018. The use of POS terminals as a payment option dropped sharply from 43% to 26%; ATM payments in the total volume of card transactions decreased from 4% to 1% (Table 6).

Table 6. Use of payment cards issued by Kazakhstani and foreign issuers on the territory of the Republic of Kazakhstan, dynamics of transactions via Internet banking, first quarter of the year.

|

Years |

2016 |

2017 |

2018 |

2019 |

2020 |

|

Thousand transactions |

12322,2 |

22060,3 |

54911,4 |

129532,7 |

459500,1 |

|

Million tenge |

127021,9 |

245999,4 |

665444 |

1518566,3 |

5588753,5 |

Note - compiled by the author on the basis of the corresponding source of NB.

Сompared to 2018, the number of transactions via Internet mobile banking in 2019 increased by 21% in comparison with other transactions. It was decided to analyze the use of Internet banking for the 1st quarter in different years, starting from 2016. The popularity of online banking transactions has grown steadily every year. In 2018, the number of payments increased by 2.7 times compared to the same period in 2017. High growth rates of 2.2 times in 2019 indicate a steady increase in the popularity of online banking. Since March 16, 2020, due to the regime for a state of emergency imposed by the coronavirus pandemic, the volume of payments in 2020 has increased by about 3.6 times, the number of transactions has also increased by 3.5 times compared to last year.

The use of payment cards issued by Kazakhstani and foreign issuers on the territory of the Republic of Kazakhstan, the dynamics of transactions via Internet banking, the period January-February-March (Figure 1).

Consequently, payment for goods and services, all banking operations via the Internet, will require even greater implementation of financial technologies in the banking sector. Trends in the use of Internet banking will only increase, the pandemic has changed the views of users on online shopping. With the rise of digital technologies, customers choose the time. The Internet banking provides such an opportunity.

The analysis showed that the progress in the banking sector is directly related to the development of financial technologies and security. It is very important for banks to increase funding for new technologies, thereby becoming innovative and flexible market participants. Key new technologies must be deployed on all fronts: apply timely analytical methods and working approaches, redefine service distribution channels, strengthen further standardization of back office functions and services. Banks should pay special attention to providing security in the same areas. With the advancement of technology, cyberattacks have been conducted more frequently. The integrity of personal data, the reliability of the bank in all respects will give a competitive advantage.

At present Kazakh banks are being tested by advanced technologies. Since the beginning of 2020, the banking sector has experienced amazing growth of transactions via Internet banking. Therefore, the issue of financial technology in the banking sector is very relevant. The bank's primary task is to redistribute priorities. A correct analysis of the financial and economic activities of the bank will allow to find strengths and weaknesses, to determine the level of digitalization of banking services. The provision of banking services through information technology and the confidence in the security of transactions will be the main advantage.

The speed and efficiency used security technologies usually lag behind of new Internet technologies. This is reflected in the growth of cybercrime, an increase in cases misuse of data. In particular, rapidly growing mobile application market are discovering an increasing number of security vulnerabilities, misuse of data, espionage, malware and spyware hacking. The importance of information security is becoming more prominent in both private and business areas.

Thus, the SWOT analysis of the development of financial technologies in the banking sector showed that there are a number of problems that can affect the further development of digitalization in the banks of the Republic of Kazakhstan. It is therefore essential that traditional banks provide modern additional services to customers through digital channels. Such services must be efficient, reduce search costs and provide easy access to information. To solve the problems identified during the SWOT analysis, the following recommendations are offered:

Banks' primary task is to protect customers from cyber threats and ensure the highest security measures for personal data. The use of Internet banking from any device will lead to the accumulation of a huge data set, which is known as Big Data. The financial sector needs to rethink the implementation of such security control mechanisms as biometric authentication, public key infrastructure, digital signature control, use of one-time password. Also pay special attention to blockchain technologies that handle big data, and has a stable and convenient form of encryption (Khan, Yaacob, 2019).

Secondly, in a new reality, banks need to move to a digital transformation strategy. This involves banks to go beyond conventional websites, chatbots, for remote interaction provide customers with an interactive hub through digital channels. Banks need to develop a virtual banking system that will organically provide services to users, while simultaneously expanding their presence on the Internet.

Thirdly, financial institutions need to update technology, also redirect their thinking. Customers should be a center of all digital strategies. Banks has spent large sums of money on digital interactions with customers, which reduced the number of visits to branches, opened the possibility of interaction with the bank at the touch of a button using mobile phones or laptops. This progress has generated positive customer feedback, but more work needs to be done. Customer data is the new banking opportunity and the main success of digital transformation.

Fourthly, qualified and efficient staff will analyze the collected customer data, thus provide them an objective advice. An individual approach to clients will be visible, which will improve the brand and reputation of the financial institution.

Fifth, to succeed banks must take customer focus marketing approach to attract and retain customers. Especially in the early days of digital banking, it is important that bank employees talk and promote the benefits of online banking in order to gain customer’s trust and loyalty (Drenik, 2020).

References:

Alpatova, E.S. (2019). Vliyanie finansovykh tekhnologii na razvitie bankovskogo sektora [Influence of financial technologies on the development of the banking sector]. Economics: Yesterday, Today and Tomorrow, Vol. 9, 1, 783790. Retrieved from:http://publishing-vak.ru/file/archive-economy-2019-1/80-alpatova.pdf [in Russian].

Arner, D.W., Barberis J.N., & Buckley R.P. (2015). The evolution of Fintech: A new post-crisis paradigm? University of Hong Kong Faculty of Law Research Paper, 047, 1-44. Retrieved from:

Assotsiatsiya finansistov Kazakhstana [Association of Financiers of Kazakhstan]. (2019). afk.kz. Retrieved from :http://afk.kz/ru/analytics/monitor-ryinka/kolvo-platzhnx-kart-v-kz-vyirsl-bol-chem-na-chetvrt.html [in Russian].

Bakulina, A.A., Popova, V.V. (2018). Vliyanie fintekha na bezopasnost' bankovskogo sektora [Fintech's impact on the security of the banking sector]. Ekonomika. Nalogi. Pravo – Economy. Taxes. Law, 2, 84-89. Retrieved from: http://elib.fa.ru/art2018/bv471.pdf [in Russian].

Beyond FinTech: A pragmatic assessment of disruptive potential in financial service. (2017). weforum.org. Retrieved from: https://www.weforum.org/reports/beyond-fintech-a-pragmatic-assessment-of-disruptive-potential-in-financial- services

Calzolari, G., Mansilla-Fernández J.M., & Pozzolo, A.F. (2017). FinTech and Banking. Friends or Foes? European Economy – Banks, Regulation, and the Real Sector, 2, 9-31. Retrieved from: http://european-economy.eu/wp- content/uploads/2018/01/EE_2.2017-2.pdf

Dapp, T. (2014). Fintech – The digital (r)evolution in the financial sector. Deutsche Bank Research. Retrieved from: https://www.deutschebank.nl/nl/docs/Fintech-The_digital_revolution_in_the_financial_sector.pdf

Doszhan, R., Nurmaganbetova, A., Pukala, R., Yessenova, G., Omar, S., & Sabidullina, A. (2020). New challenges in the financial management under the influence of financial technology. E3S Web of Conferences 159. Retrieved from: https://www.researchgate.net/publication/340122135_New_challenges_in_the_financial_management_under_the_in fluence_of_financial_technology

Fintech100. h2.vc Retrieved from: https://h2.vc/wp-content/uploads/2020/02/2019Fintech100.pdf

Forbes (n.d.). forbes.com. Retrieved from: https://www.forbes.com/sites/garydrenik/2020/09/22/mobile-banking-is-on- the-rise-due-to-covid-19but-somethings-lacking-from-most-bank-apps/?sh=773cce31a957

Global FinTech Adoption Index 2019. ey.com. Retrieved from: https://fintechauscensus.ey.com/2019/Documents/ey- global-fintech-adoption-index-2019.pdf

Gomber, P., Koch, J-A., & Siering, M. (2017). Digital Finance and FinTech: current research and future research directions. Journal of Business Economics. Retrieved from: https://ssrn.com/abstract=2928833

Khan, B., Olanrewaju, R., Anwar, F., Mir, R., & Yaacob, M. (2019). Scrutinising internet banking security solutions. International Journal of Information and Computer Security 12, 1-34. Retrieved from: https://www.researchgate.net/publication/330521655_Scrutinising_internet_banking_security_solutions

Kurmanova, D. A. (2019). Finansovye tekhnologii na roznichnom rynke bankovskikh uslug [Financial technologies in the retail banking market]. Vestnik UGNTU. Nauka, obrazovanie, ekonomika – Bulletin USPTU. Science, education, economy, 1, 60-67. Retrieved from: https://cyberleninka.ru/article/n/finansovye-tehnologii-na-roznichnom-rynke- bankovskih-uslug [in Russian].

Maslennikov, V.V., Fedotova, M.A., & Sorokin, A.N. (2017). Novye finansovye tekhnologii menyayut nash mir [New financial technologies are changing our world]. Finansy: teoriya i praktika - Finance: Theory and Practice, Vol. 21, 2, 6-11. Retrieved from: https://doi.org/10.26794/2587-5671-2017-21-2-6-11 [in Russian].

Ofitsial'nyi internet-resurs Gosudarstvennoi programmy «Tsifrovoi Kazakhstan» [Official Internet resource of the State Program «Digital Kazakhstan»]. (n.d.) digitalkz.kz. Retrieved from: https://digitalkz.kz/o-programme/ [in Russian].

Osipova, T.Yu. & Klimenko, E.N. (2016). Finansovye tekhnologii kak obolochka instrumentov finansov domashnikh khozyaistv [Financial technologies as a shell of household finance instruments]. Problemy ucheta i finansov – Accounting and finance problems, 4, 27-36. Retrieved from: http://vital.lib.tsu.ru/vital/access/manager/Repository/vtls:000582046 [in Russian].

Perspektivy razvitiya regional'noi ekonomiki [Prospects for the development of the regional economy]. (2017). img.org. Retrieved from: http://www.imf.org/~/media/Files/Publications/REO/MCD-CCA/2017/October/CCAnovember1 /Russian/chapter-5-final-rus-oct-20.ashx?la=ru [in Russian].

Pyzhlakov, D.S. (2008). Kontseptsiya dinamicheskogo SWOT-analiza [Dynamic SWOT Analysis Concept]. Rossiiskoe predprinimatel'stvo - Russian entrepreneurship, 6, 133-138 [in Russian].

Russia, CIS and the Caucasus report. (2019). aifc.kz. Retrieved from: https://aifc.kz/uploads/finreport.pdf [in Russian].

Timofeeva, S.A., Mavrodieva, K.S. (2010). Primenenie SWOT-analiza v protsesse strategicheskogo planirovaniya pri razrabotke investitsionnoi politiki na primere kreditnoi organizatsii [Application of SWOT analysis in the process of strategic planning in the development of investment policy on the example of a credit institution]. Nauchnye zapiski OrelGIET - Scientific Journal of OrelSIET, 1, 132-137. Retrieved from : https://old.orelgiet.ru/monah/32.tm.pdf [in Russian].

Tsentr delovoi informatsii. [Business Information Center]. kapital.kz. Retrieved from: https://kapital.kz

/finance/84207/fintekh-pomogayet-sokratit-razmer-tenevoy-ekonomiki.html [in Russian].

Tsentr delovoi informatsii. [Business Information Center]. kapital.kz. Retrieved from: https://kapital.kz

/finance/88934/bank-fintekh-potrebitel-kak-spros-menyayet-format-sotrudnichestva.html [in Russian].

Zavolokina, L., Dolata, M., & Schwabe, G. (2016). FinTech – What's in a Name? Thirty Seventh International Conference on Information Systems. Retrieved from: https://www.zora.uzh.ch/id/eprint/126806/1/FinTech_Research_ Pa- per_revised.pdf