Abstract

Object: The purpose of this study is to identify the main problems of budgeting in second-tier banks in Kazakhstan based on the analysis of the development of the level of budgeting and modern methods of budgeting in Kazakh banks.

Methods: The collected data for the assessment and development of budgeting were analyzed using the matrix method for evaluating internal (IFE) and external factors (EFE), and QSPM (Quantitative Strategic Planning Method).

Findings: As a result of the QSPM analysis, the Bank can become aware of its position in the market and step up its activities to improve management accounting, including budgeting in the bank.

Conclusions: QSPM analysis in JSC Bank CenterCredit revealed the main strengths and weaknesses of budgeting development, as well as existing opportunities and threats. As a result, it was revealed that the bank is aware of its position in the market and is stepping up its activities to improve management accounting, including budgeting in the bank.

Most modern Kazakhstani banks apply management accounting partially. Mostly it is an abbreviated form of financial statements, which reflects the plan, fact, deviation and forecasts. In this setting, forecasts are still being carried out on past period budgets, which are carried forward to the next period with insignificant adjustment to the projected inflation rate and profit, division expenses, etc. that are supposed in a similar way.

QSPM analysis allows to identify main strengths and weaknesses of budgeting development, opportunities and threats, as a result of which the bank can realize its market position and intensify its activities to improve management accounting, including budgeting in the bank.

Management accounting in banks aims at obtaining reliable information on the actual state of affairs with resources and their allocation, risks, ensuring control over profitability of all operations and providing it to management for decision making.

According to I. Kasasbeh, management accounting in banks acts as a basis for financial accounting (bookkeeping) and reporting. The main factor in its creation is its economic efficiency, a significant excess of income over expenses associated with the creation and introduction of banking products and services (Kasasbeh, 2018).

We feel worth noting that budgeting serves as a basic tool of management accounting. Since budgeting has always remained the primary concern of any accounting, it has always been the focus of attention. At the same time, the development of budgeting would be accompanied by certain problems that banks face constantly in their activities.

The modern approach to budgeting in banks is based not only on the preparation of cost and income estimates with their subsequent analysis, but also includes certain actions aimed at achieving the strategic or operational goals of the bank, which use budgeting methods to control and manage the bank’s financial resources.

Strategic planning refers to the preparatory stages for budgeting, which is an essential element of management (Bindra et al., 2019). Strategic planning is a part of the management process aimed at maintaining balance and alignment between the goals and resources of the bank in a constantly changing environment (Papke-Shields, K. E., & Boyer-Wright, K. M., 2017). At the same time, those indicators that the management considers necessary to determine as standards for each FAC can be designated as targets. For instance, profitability of capital, profitability of assets, rate of return, cost limitation, cost rationing, etc. Forecasting is of great significance, which, moreover, should be actively used not only at the preparatory stage.

The collected data for the assessment and development of budgeting were analyzed using the matrix method for evaluating internal (IFE) and external factors (EFE), and QSPM (Quantitative Strategic Planning Method — a method of quantitative strategic planning

Forecasting macroeconomic indicators allows to determine the main regulatory guidelines for the activities of both the bank as a whole and financial accounting centers (Forgione, A.F., & Migliardo, C., 2018). Establishment of strategic guidelines is the prerogative of the bank's board of directors, which sometimes delegates these powers to the chairman of the board or the bank's budget committee. Designing a precise budgeting schedule will allow to determine not only time frames, but also an indication of the budgeting stages themselves, which will contribute to effective planning. Our proposed timetable can be used as an example (Table 1).

Table 1 — Timetable for budgeting

|

№ |

Budgeting stage |

Term, days |

Period, date |

Responsible |

|

1 |

2 |

3 |

4 |

5 |

|

1. |

Account of transfer rates and internal norms |

1 |

20.09.2019 |

Budgeting department |

|

2. |

Informing FAC about changes in transfer rates and norms |

|||

|

3. |

Development of planned budget forms of the FAC and submission to the Budgeting Department |

1 |

21.09.2019 |

FAC |

|

4. |

Cost-benefit analysis |

1 |

22.09.2019 |

Budgeting department |

|

5. |

Establishment of a management budget balance |

|||

|

6. |

Establishment of own budget capital |

1 |

23.09.2019 |

Budgeting department |

|

7. |

Profit and loss budgeting |

|||

|

8. |

Profit and loss budgeting based on transfer pricing |

2 |

24.09.2019 25.09.2019 |

Budgeting department |

|

9. |

Approval of budgets |

1 |

26.09.2019 |

Budget committee |

|

Note: compiled by the authors |

||||

Thus, according to Table 1, budgeting will take no more than 7 days. The last stage of budgeting is monitoring and control over the execution of budgets. Here it can be said that budgeting ends and at the same time starts again, which testifies to the renewability of this process and its endlessness.

In the process of budgeting, it is important that the FAC budgets are made not for themselves, as is often the case (employees manipulate indicators), but directly for making management decisions. This kind of manipulation is called a “mine” of delayed action (Nurgaliyevа et al., 2020).

In order to build an effective budgeting system in a bank, it is necessary to carry out comprehensive and purposeful activities of bank managers in the following areas: structuring information flows between various structural divisions of the bank; distribution of budgeting functions across the FAC; motivating FAC to execute budgets (Alabdullah, Tariq Tawfeeq Yousif, 2019).

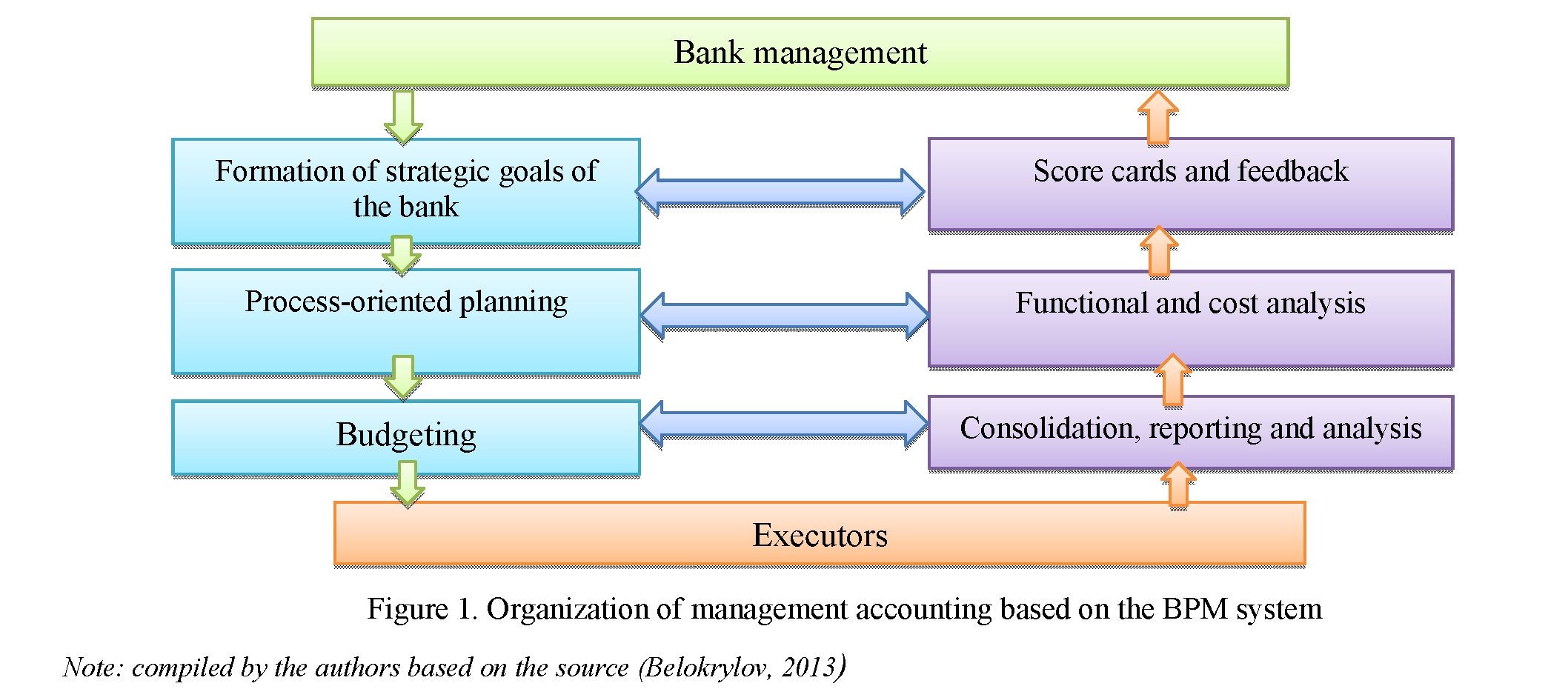

It should be noted that PBB is based on the BPM model (Business Performance Management (Brimson, 2007), the use of which in the bank will allow the formation of management accounting with feedback (Figure 1).

In Figure 1, management accounting includes both top-down and bottom-up processes. The first cycle begins with the formation of the bank's goals, key performance indicators, and the structure of communications between the financial accounting centers.

The results of an empirical study conducted in Kazakhstan banks have shown that budgeting in banks is for the most part uses traditional methods, which have a number of drawbacks. Current period budgets get carried over to projected values only with insignificant adjustment to projected values of inflation and exchange rate. As a result, the shortcomings and mistakes of past periods smoothly transition into future ones while real expenses are not taken into account. There is also the problem of estimating costs; the self cost of banking products, to be precise. Traditional methods misrepresent and unfortunately, are incompatible with modern management accounting.

The dynamics of the modern banking market is increasing every day. Second-tier banks are increasingly under pressure from non-bank organizations, which constitute a serious competition for them. As a result, banks are trying to become more flexible and are revising conservative approaches, including those to budgeting, since in a dynamic market spending several months on budgeting is doomed to failure.

Moreover, traditional budgeting is a constant conflict of shareholders and bank management. Managers strive to demand the maximum amount of resources, increase the budget. Shareholders want to perform large tasks with a minimum of resources. As a result, bank remains ineffective financially.

Many economists identify several reasons why traditional budgeting is outdated today. In general, negative aspects of traditional budgeting in banks are as follows:

- it does not promote value creation;

- budget for the future period is prepared on the basis of the previous one with arbitrary correction;

- it does not take into account the features of banking products and customers;

- it gives the opportunity to manipulate the budget;

- it does not take into account the workload by type of activity;

- it does not take into account business processes;

- it does not track service levels;

- it does not take into account functional capabilities of the bank units.

As per the results of an empirical study on the development of management accounting in Kazakhstan banks, currently most banks use traditional budgeting (67.2 % of experts) and only 32.3 % have indicated the use of a more advanced method of Activity Base Budgeting. 59.1 % of experts have indicated a standard cost estimate in banks.

This state of affairs creates the need for analysis of the budgeting development in banks. For these purposes we used QSPM (Quantitative Strategic Planning Method), a high-level strategic management approach to evaluate possible strategies. QSPM provides an analytical method for comparing possible alternative actions and is based on IFE and EFE matrices (Zulkarnain et al., 2018).

The Internal Factor Evaluation (IFE) is a strategic tool for managing an audit or evaluating the main strengths and weaknesses in budgeting in a bank. The IFE matrix provides the basis for identifying and evaluating the relationships between budgeting elements.

The matrix method of evaluating external factors (EFE) is used to assess current business conditions (Mina Salehi et al., 2018). The EFE matrix is a great tool for visualizing and prioritizing the opportunities and threats the bank faces.

In general, the EFE and IFE matrices are very similar. The main difference between the two is the type of factors included in the model: the IFE matrix evaluates internal factors, while the EFE matrix evaluates external factors exclusively.

The external factors evaluated in the EFE matrix are those that obey the will of social, economic, political, legal and other external forces.

In turn, the QSPM technique consists of several stages:

- Listing the key factors reflecting strengths and weaknesses of budgeting in the bank.

- Determination of scores (score — S) of each factor. With that, in the IFE matrix, a predetermined group of experts evaluates the factors on a scale of 1 to 4 as follows: 1 — the factor is the bank’s main weakness, 2 — the factor is the bank’s insignificant weakness; 3 — the factor is the bank’s minimum strength; 4 — the factor is the bank’s main strength. Thus, weaknesses are scored 1 and 2, and strengths are scored 3 and 4. In the EFE matrix, a predetermined group of experts evaluates the factors on a scale of 1 to 4 as follows: 1 — a weak response to the environmental factor, 2 — response to the environmental factor is weaker than average, 3 — response to the environmental factor is higher than average, 4 — a very strong response to the environmental factor.

- Determination of the attractiveness (attractiveness score — AS) of each factor in such a way that the total of attractiveness of both strengths and weaknesses is 1.

- Determination of the weighted total score (total attractiveness score — TAS) for each factor by multiplying the score by attractiveness.

- Definition of the result as a sum of the final points (final total attractiveness score — FTAS) for each factor.

- Building a diagram where the value of the IFE matrix is displayed on the X axis, and the EFE matrix on the Y axis.

To evaluate these factors we have created a group of experts consisting of senior and middle managers, and bank unit employees with a total of 116 people.

AS and S indicators in tables 2 and 3 have been calculated as the weighted average of the results obtained from the expert group.

So, let us assess the strengths and weaknesses of budgeting development in the Bank CenterCredit JSC (Table 2).

Table 2. IFE matrix of strengths and weaknesses of the budgeting development in Bank CenterCredit JSC

|

Factors |

Weight (AS) |

Rating (S) |

Weighted score (TAS) |

|

1 |

2 |

3 |

4 |

|

Strengths |

|||

|

Interconnected management system formation |

0.07 |

2.8 |

0.196 |

|

Ability to introduce modifications at a particular level of the business system |

0.04 |

3.1 |

0.124 |

|

Ability to introduce modifications when deviations occur, not in response to |

0.06 |

3.87 |

0.2322 |

|

Orientation of employees to achieve measurable goals |

0.04 |

3.92 |

0.1568 |

|

Has a positive effect on employee motivation |

0.07 |

3.73 |

0.2611 |

|

Allows to improve the resource allocation process |

0.08 |

3.3 |

0.264 |

|

Ability to track any stage of budgeting |

0.03 |

2.66 |

0.0798 |

|

Release of a large amount of time and labor |

0.06 |

4 |

0.24 |

|

Creation of accounting by financial management centers |

0.09 |

3.21 |

0.2889 |

|

Ability to take into account overhead dynamics |

0.05 |

4 |

0.2 |

|

Weaknesses |

|||

|

Different perceptions of FMC budgets |

0.04 |

1.98 |

0.0792 |

|

Conflict of interests of employees and management |

0.08 |

0.95 |

0.076 |

|

1 |

2 |

3 |

4 |

|

The discrepancy between forecasts and facts |

0.08 |

1.13 |

0.0904 |

|

Inadequate staff skills to apply advanced budgeting methods |

0.03 |

1.84 |

0.0552 |

|

Lack of budget flexibility |

0.05 |

1.66 |

0.083 |

|

Exaggeration of own results by some unit employees |

0.05 |

0.97 |

0.0485 |

|

Errors in the distribution of overhead costs for banking services |

0.04 |

1.72 |

0.0688 |

|

Lack of feedback required for immediate management |

0.04 |

1.33 |

0.0532 |

|

FTAS |

100 |

2.5971 |

|

|

Note: made up on the basis or research and calculations |

|||

According to the data obtained, the most powerful aspects of budgeting development in Bank CenterCredit JSC are accounting by financial management centers — 0.2889, improvement of the resource allocation process — 0.264 and presence of a positive effect in the form of employee motivation — 0.2611.

The weakest points of the budgeting development strengths in the bank are the ability to track any stage of budgeting — 0.0798, the ability to introduce modifications to the budget at a particular level of the business system — 0.124, and orienting employees to achieve measurable goals — 0.1568.

In addition, the following areas are the main weaknesses in budgeting development in Bank CenterCredit JSC: many employees exaggerate their performance as a result of KPI introduction — 0.0485; the bank has not established feedback information necessary for effective immediate management — 0.0532; the score and qualifications of employees of the budgeting unit are not enough to apply new budgeting methods — 0.0552.

Thus, this analysis allows the bank to identify problem points and work directly in strictly defined areas without spreading on other factors with much higher scores.

Let us analyze the possibilities and threats of budgeting development in Bank CenterCredit JSC (table 3).

Table 3. EFE Matrix of Opportunities and Threats of Budgeting Development in Bank CenterCredit JSC

|

Factors |

Weight (AS) |

Rating (S) |

Weighted score (TAS) |

|

Opportunities |

|||

|

The use of more advanced budgeting methods |

0.09 |

3.46 |

0.3114 |

|

Estimation of the cost of individual banking products |

0.12 |

3.11 |

0.3732 |

|

Providing feedback information for managers |

0.07 |

2.11 |

0.1477 |

|

Increased budget flexibility |

0.11 |

2.85 |

0.3135 |

|

Elimination of the budget manipulation |

0.09 |

2.18 |

0.1962 |

|

Further training for employees and management |

0.05 |

3.76 |

0.188 |

|

Conducting regular surveys of bank employees to improve the budget process quality |

0.04 |

2.34 |

0.0936 |

|

Threats |

|||

|

Global competition |

0.07 |

2.96 |

0.2072 |

|

High cost of software for budgeting |

0.08 |

3.88 |

0.3104 |

|

The use of more advanced costing methods by competitor banks |

0.09 |

2.98 |

0.2682 |

|

Distortion of financial results as a result of the introduction of modern budgeting methods |

0.08 |

2.77 |

0.2216 |

|

Failure to adopt a new budgeting method by employees |

0.06 |

2.13 |

0.1278 |

|

Transformation of budgeting from a method of increasing efficiency into a system of supervision over employees |

0.05 |

2.35 |

0.1175 |

|

FTAS |

1 |

2.8763 |

|

|

Note: made up on the basis or research and calculations |

|||

The results of the analysis show that currently, to the fullest extent Bank CenterCredit JSC has the ability to estimate the cost of individual banking products — 0.3732 with the use of more advanced budgeting techniques — 0.3114, which shall increase budget flexibility — 0.3135.

At the same time, the high cost of budgeting software products — 0.3104, the use of more advanced budgeting methods by competing banks — 0.2682, and the distortion of financial results due to the incorrect

introduction of modern budgeting methods may prevent the bank from achieving its goals using the available capabilities — 0.2216.

Thus, the results shown in the EFE matrix also allow us to focus on the identified opportunities and threats to the greatest extent.

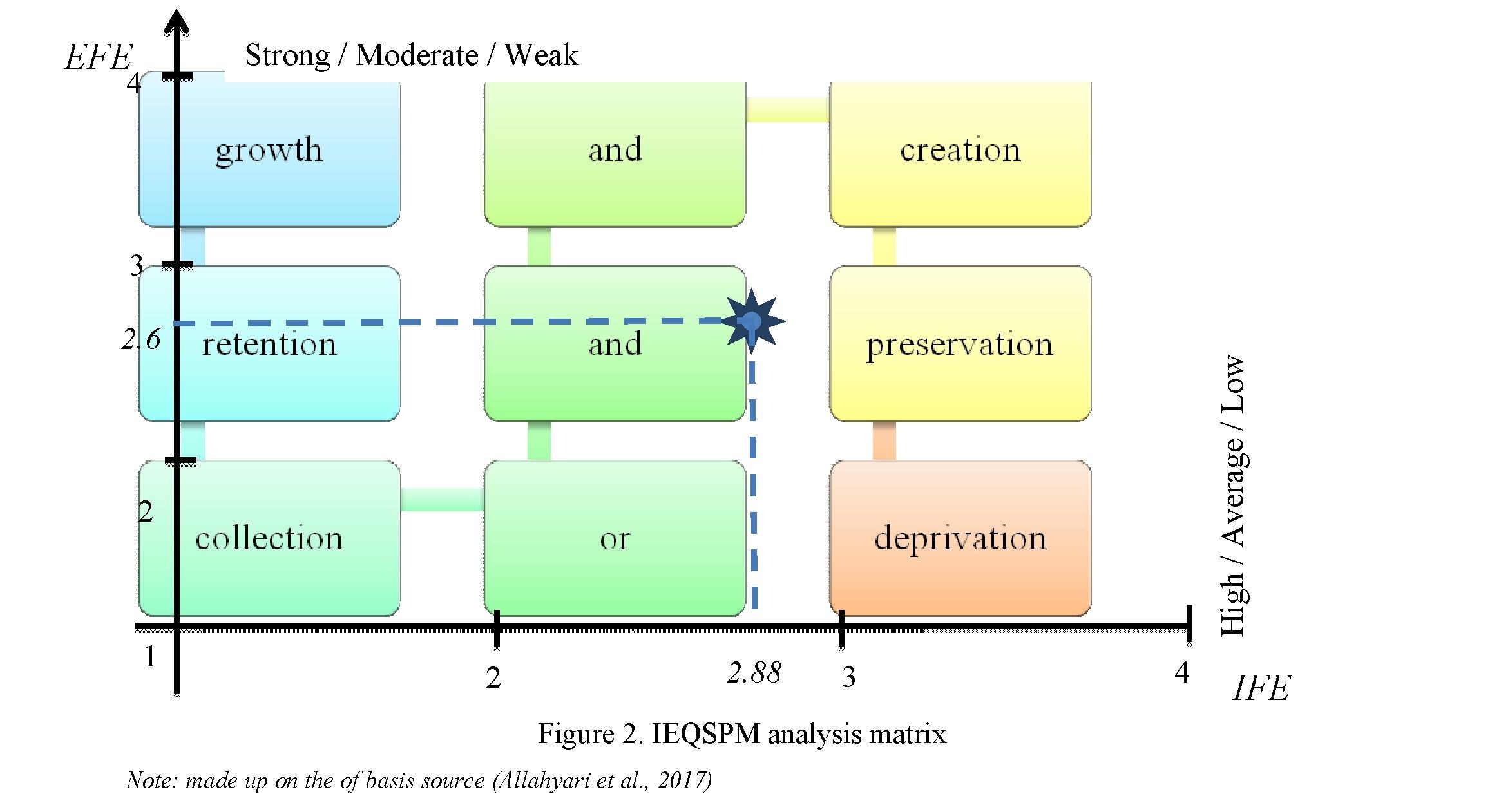

The obtained FTAS results for both matrices are reflected in the X and Y coordinate system. In this case, the IFE matrix value is on the X axis, and EFE matricx value is on the Y axis. As a result, both points shall indicate a specific segment of the IE matrix shown in Figure 2.

The strategy of “growth and creation” means intense and aggressive tactical behavior. The bank should be focusing on creating new budgeting system, developing a methodological and organizational base and designing a new strategy different from all those available on the banking market.

The “retention and preservation” strategy assumes that the bank needs to continue the existing initiatives regarding the restructuring of the budgeting system in the bank in the same direction and hold on to those positions that the bank has been able to take and present them in the form of its strengths.

The “collection or deprivation” strategy suggests that the bank needs to choose between investing in this area and its further development, or explore other ways to improve budgeting.

Thus, according to the data obtained, the IFE value is close to 3, a value that approaches the retention strategy, and the EFE value is in the middle of the retention strategy. Such a result indicates that the bank in question has certain strategically important positions in the development of the budgeting system. These need to be maintained and directed towards improving the results, having established the existing positions as the strengths of the bank's budgeting system.

Employees of Bank CenterCredit JSC have pointed out the most significant aspects of the development of the budgeting system in the bank. In particular, such strengths of improving the budgeting process as the ability to introduce modifications when deviations occur, and not in response to, orienting employees to achieve measurable goals, and having a positive effect on employee motivation have received the highest significance: 3.87; 3.92 and 3.73 out of 4 maximum points, respectively. This data indicates that the ongoing processes of improving budgeting in the bank primarily had an effect on human capital (the active use of KPI also played a role here as the main method for assessing the performance of the central financial institution).

The most significant weak aspects of budgeting development are different perceptions of the FMC budgets, insufficient qualifications of employees for applying advanced budgeting methods, and errors in the distribution of overhead costs for banking services that received 1.98; 1.84 and 1.72 out of 2 maximum possible points, respectively. Thus, once again the main issue of improving the budgeting process in the bank is human capital. However, as can be noted, these aspects are quite fixable and require introduction of minor but decisive measures to develop these areas. Especially if we consider that the basic capabilities of the bank were the advanced training of employees and management, the use of more advanced budgeting methods and the ability to assess the cost of individual banking products, which received 3.76, 3.46 and 3.11 out of 4 maximum points, respectively.

Thus, the bank solves the issues identified as weaknesses in improving budgeting on its own. The only thing that the bank is particularly concerned about as external challenge factors is the presence and growth of global competition seen from not only local but also foreign banks; the relatively high cost of budgeting software and the ability of competing banks to use more advanced costing methods. We feel worth noting that the acquisition of expensive software products may possibly be unjustified due to the fact that budgeting techniques are constantly being improved due to the internationalization and globalization of banking markets. However, regular further training of employees may be much less costly, yet more progressive because it allows the development and not just introduction of modern budgeting methods in the bank.

References

- Alabdullah, Tariq Tawfeeq Yousif (2019). Management Accounting and Service Companies' Performance: Research in

- Emerging Economies, Australasian Accounting, Business and Finance Journal, 13(4), 100–118. doi:10.14453/aabfj.v13i4.8

- Allahyari, H., Nasehi S., Salehi E. and Zebardast L. (2017). Evaluation of visual pollution in urban squares, using SWOT, AHP, and QSPM techniques // Pollution, 3 (4), 655–667.

- Belokrylov, I.S. (2013). Aktualnost' transformacii byudzhetirovaniya v kreditnyh organizaciyah v processno- orientirovannoe byudzhetirovanie [The relevance of the transformation of budgeting in credit organizations into a process-oriented budgeting] // Vysshaya shkola — biznesu – Higher school — to business. 19(3), 156–162 [in Russian].

- Bindra, S., Parameswar, N., & Dhir, S. (2019). Strategic management: The evolution of the field. Strategic Change, 28(6), 469–478. doi:10.1002/jsc.2299

- Brimson James (2007). Process-oriented budgeting. Implementation of a new company value management tool. from English V.D. Goryunova; under the general. ed. V.V. Bad luck. — M.: Peak.

- Forgione, A. F., & Migliardo, C. (2018). Forecasting distress in cooperative banks: The role of asset quality. International Journal of Forecasting, 34(4), 678–695. doi:10.1016/j.ijforecast.2018.04.008

- Kasasbeh, I. (2018). Problems of Management Accounting Implementation: The Case of Balanced Scorecard Implementation within Jordanian Commercial Banks. International Journal of Academic Research in Accounting, Finance and Management Sciences, 8, 200–207

- Mina Salehi, Jalal Ebrahimi Askari, (2014). Shaghayeghe Behrouzi Strategy Formulating by SWOT and QSPM Matrix // International SAMANM Journal of Marketing and Management. 2 (2), 226–240.

- Nurgaliyevа A.M., Mynbaeva D.E., Zhapbarkhanova M.S. (2020). Budgeting as a STEM-tool for management accounting in second-tier banks // Economics and Management Systems Management, 1 (35), 50–56

- Papke-Shields, K. E., & Boyer-Wright, K. M. (2017). Strategic planning characteristics applied to project management. International Journal of Project Management, 35(2), 169–179. doi:10.1016/j.ijproman.2016.10.015

- Zulkarnain A., Wahyuningtias D., Putranto T.S. (2018) Analysis of IFE, EFE and QSPM matrix on business development strategy // IOP Conference Series Earth and Environmental Science. 126, P. 012062 Retrieved from https://iopscience.iop.org/article/10.1088/1755–1315/126/1/012062/pdf.