Abstract

Object: To define the concept of internal audit in the commercial organisations in Kazakhstan, specify the problems, and find solutions to these problems.

Methods: System analysis (analytical and synthetic methods) and information structuring.

Results: The conceptual essence is systematized based on the scientific approaches of the internal audit understanding. Moreover, the cause-and-effect factors of the internal audit functioning are determined. In this study, the problems regarding the development of internal audit are studied and ways of solving these problems are proposed.

Conclusions: A clear systematization of scientific approaches to the concept of internal audit, identification of the causes of problems with the running internal audit in the commercial organisations in Kazakhstan will ensure the progressive development of internal audit.

In countries with developed market economies, almost all large companies have an internal audit that regularly checks certain areas of the production and economic activities of these companies. Internal audit tightly connects to internal control. The main task of the internal control system is to ensure the safety of the property of companies, the completeness, and reliability of the information on business transactions carried out, and use forms and methods of control that contribute to improving the efficiency of production and economic activities.

According to international standards, an internal audit should assist the organization in maintaining an efficient internal control system, assessing its effectiveness, contributing to its continuous improvement. The issues of increasing the effectiveness of the internal audit in companies in the last decade have become particularly relevant. The effectiveness of an internal audit depends on the efficiency of the company’s operations, as well as the company’s investment attractiveness in the market. Since the internal audit is a multipurpose profession it is hard to determine its actual role and functions.

The enlightenment of the essence of internal audit is possible only through determining its role within the goals, tasks and functions; understanding the internal audit in the business sector of the economy of the Republic of Kazakhstan and worldwide. The interpretation of the internal audit role changed throughout the development of corporate governance, as well as under the influence of economics. The lack of a unified approach to the definition of its role leads to different interpretations of its subject.

Nowadays, an internal audit is also an effective corporate governance tool. It protects the economic interests of companies and contributes to the achievement of their strategic goals. Properly organized internal audit contributes to the safety and efficient use of companies’ resources. It determines the degree of confidence of the financial statement users and helps to improve the profitability of the company. In addition, it can help to strengthen the position of the company in the market. All these factors determine the increased interest of the owners, top management, regulatory bodies, and other users of financial statements to the internal audit departments of commercial organizations.

*Corresponding author’s e-mail: karlygash.ramazanova@gmail.com

The research questions: If the Kazakhstani commercial organizations use the full set of internal audit functions, what is the current role of internal audit department and if internal audit has any problems in its organization and how this problem can be solved?

The audit was created based on accounting function, but later it was transformed into management- oriented competency. Currently, internal audit is an independent field of corporate governance that plays an important role in managing the policies of companies and countries. Compared to other professions, the profession of the internal auditor is a recent one. The first professional organization of internal auditors, The Institute of Internal Auditors (IIA), was set up in 1941. The unified international professional certification Certified Internal Auditor, which confirms the qualifications of an internal auditor, was established in 1974 (Kryshkin, 2017).

National institutions of internal auditors have been established and operate in almost 120 countries around the world. Kazakhstan is among these countries; in 2017, the IIA was established. Kazakhstani colleagues are also supported by the Russian IIA. The Russian IIA establishes its own professional magazine and actively participates in the formation of internal audit in the Russian Federation.

The IIA of Kazakhstan works passively, but it is the worldwide recognized public organization in Kazakhstan. It has access to the methodological materials of the International IIA, its members work in the internal audit services of organizations of various forms of ownership. The creation of the IIA in Kazakhstan is highly relevant during the period of development of the internal audit system in the Republic of Kazakhstan (RK) under the International Professional Standards for Internal Auditing.

The role of internal audit is increasing significantly and it started the transformation into a discrete part of discipline aims to cooperate and help management to stimulate realization of companies’ goals and objectives (Roussy, 2013). Internal auditors give guidance through recommendations (Chambers, 2014), and in that way maintaining support for the management of the company (Roussy, 2013).

The substance of internal audit cannot be disclosed only through its functions. Internal audit is a multifaceted tool in the hands of the company’s management and its shareholders. It can help to control via such functions as management, monitoring, advising, consulting and even prevising. Thus, we can note that internal auditor executes many functions and, at the same time, it is also a key component of risk management (Spira & Page, 2003; Arena et al., 2010; De Zwaan et al., 2011) that helps companies to fulfill its corporate goals (Spira & Page, 2003; Gramling et al., 2004).

Corresponding to its current standing, internal auditing has a separate way of its historical development in distinction to financial and management accounting or external audit. The historical path was the following, before the 1940s, the main idea of internal auditing was to check the correctness of the business transactions and documents. In the 1940s, the development of economy sped up the emergence of modern internal auditing with a focus on the evaluation of the companies’ systems (McNamee & McNamee, 1995) that insensibly replaced the emphasis on activities as a management approach.

Internal auditing can be suggested as a mechanism that helps management and the management board to decrease the risk not only by determining the areas that require management attention and its intervention but also by furnishing recommendations on proper management actions. Internal auditors can grant their services in a broad range; whereas external auditors focus mainly on the financial side of companies’ activities. For instance, the main cause of internal auditing with the economy, efficiency, and effectiveness (Al-Twaijry et al., 2003) – the 3Es – is tightly interlinked with the concept of risk management and how risks are managed through the technologies.

This notion demonstrates that internal auditing supports and helps management by detecting potential distractions that may prevent companies from reaching their goals. In line with the framework of companies’ policies that serve as control environment, internal auditing ensures the company in mitigating risks within its business operations. Internal audit reports also add trustworthiness to self-generated information.

The key research methods were the methods of system analysis and structuring information. Systems analysis methods include analytical and synthetic research methods. Based on the analysis of terminology and essence of internal audit, a synthetic method was applied, which made it possible to develop a refined author’s definition of internal audit. Based on the structuring information method, theoretical aspects were developed regarding the cause-and-effect factors of the problems of internal audit development.

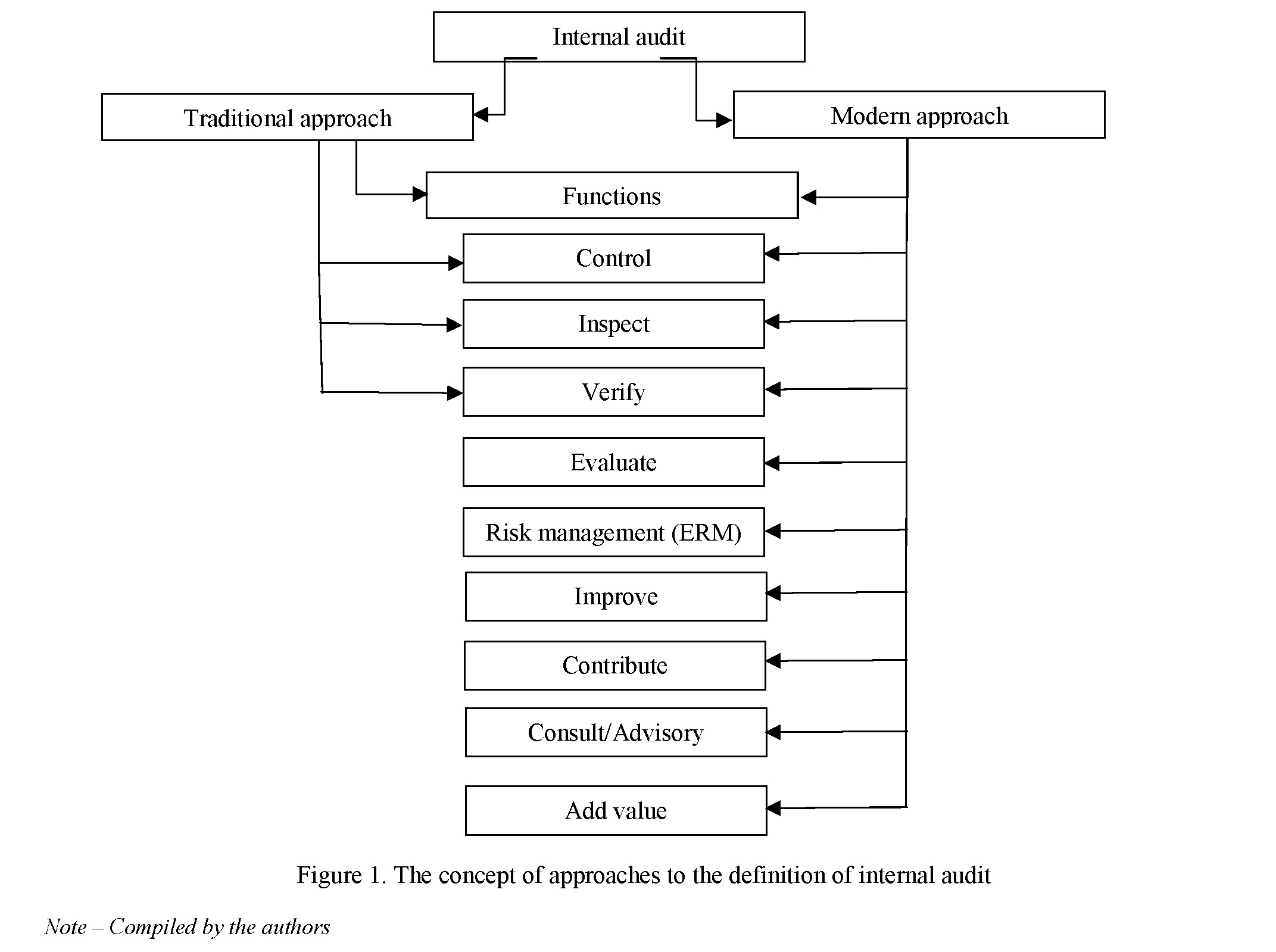

The term of internal audit shows two approaches: traditional (controlling) and modern (consulting). The first approach demonstrates only one side of the system – the controlling function. The second approach is more advanced and it adds management function and consulting character. There is a need for a unified approach to determining the essence of internal audit, which in turn directly influences the formation of conceptual and theoretical foundations of the terminology of internal control and its descriptive elements, like effectiveness, efficiency, and even the structure. Consideration of various ways to the interpretation of internal control can show a more complete picture.

Several authors look at the internal audit only from the managerial accounting side, for example, M.Kh. Abenova notes that internal control is connected with the work of cost accounting (Abenova, 2017). The main idea behind this approach is the designing managerial decision based on the results of accounting information.

A.B. Plisova also stands by this approach for determining role of internal audit. Such management decision is needed for the continuous stable development of any commercial organization (Plisova, 2017). Internal control is called managerial because the results of its inspections are indirectly used for organization management.

The second approach is a modern one. It is based on the definition of the internal audit answering the main questions, issues, purposes, and functions of the corporate environment. This type of approach is described in most international journals. The main point is that the internal audit function is not limited to the control functions. It also includes evaluation, appraisal, consulting, and adding value to the company.

The role of internal auditing can be examined in the context of enterprise risk management (ERM), which is a central concept in the corporate governance of today’s companies (Gordon et al., 2009) and defines the role of internal auditing as a risk-management tool. Committee of Sponsoring Organizations of the Treadway Commission (COSO) defines ERM as a process, influenced by companies’ management, personnel who can affect the direction in which the company will be developed, can manage the risk, accept the possible risk and decrease the risk that cannot be obtained.

Internal controls, with which internal auditing is tightly related, are considered a response to risk (Lenz & Hahn, 2015) and as part of the ERM. Thus, internal auditing can be treated as a technology embedded in the whole system of ERM. The greater size and complexness of companies have made ERM a key issue in governing organizations (Beasley et al., 2005), which in turn has revived the role of internal auditing. COSO describes internal auditing as a risk-management technology in business activities by giving assurance on companies’ systems, processes, transactions, and business activities. The ERM framework emphasizes the importance of risk management in corporate governance and the role of mechanisms, such as internal auditing in this process.

The role of internal auditors is changing from the traditional audit approach to a more productive and proactive value-added approach where internal auditors are setting up partnerships with management. Now, the evidence of more internal auditors changing their practices has begun to come up and examples are visible.

Analysis of approaches to the definition of internal audit allowed us to model the concept of this term (Figure 1).

The enactment of the Sarbanes–Oxley Act, after the financial reporting scandals, confirmed the significance of internal auditing (Carey et al., 2006). As an example, according to this Act, companies listed on the New York Stock Exchange are required to have internal audit departments that facilitate managing the risk management to audit committees by ascertaining that effective internal controls are in place. Therefore, internal auditing is contemplated as a cornerstone of corporate governance.

We assume that internal audit interconnects with internal control of the company and, at the same time, important part of the external audit (if there is any). Internal audit helps company to assess and improve the effectiveness of its internal control system, which includes risk management, accounting, financial, and corporate governance processes. According to the COSO, internal control is a process carried out by an organization’s highest body, its policymakers, its top-level management, and all other employees.

143

From the side of external audit, internal audit is assessed as part of internal control, created within the company, increases assurance in control environment, monitoring activities of auditing company. Figure 2 illustrates the place of internal audit in the organization’s internal control system.

Institutions and companies rely on internal audit as one of the main functions of the consulting activity that adds value to the institutions and companies (Hazaea et al., 2020). The internal audit functions play a fundamental and important role in promoting and improving good governance (Christopher, 2019).

Due to high involvement in the company’s operations, internal auditors can contribute to building a competitive and effective internal control structure that will improve the decision-making process. This value-added process shows the proactive approach to delivering services by internal auditors. The service provided by internal audit is far beyond financial control assessment and can be treated as achievement and fulfilment of business goals.

Everyday business needs to change and accommodate itself to new changes, e.g., introducing online commerce or running/saving a business during epidemic situations as COVID–19. Internal audit functions and roles are also changing due to these circumstances and provide assurance service, not just performing substantive procedures for companies.

In present days, the work of auditors has widened from the traditional job of detecting fraud to carrying out many tasks, such as

risk assessment;

investigating organizational culture;

performance evaluation;

ensuring the implementation of general regulations and procedures for securing financial data through the use of modern approaches (Deloitte, 2018).

Following these procedures and the updates that have occurred, IA’s use has become one of the most well-known mechanisms used in controlling financial statements. Despite this significant expansion in the audit functions, the internal audit faces significant criticism because of the failure to perform the function as defined by the IIA. IIA defines internal audit as “an independent, objective assurance and consulting activity designed to add value and improve a companies’ operations”. It further specifies that internal audit “helps a company to accomplish its objectives by bringing a systematic, disciplined approach to evaluate and improve the effectiveness of risk management, control, and governance processes” (The Institute of internal auditors, 2004) to promote the public interest. As a result of the failure that occurred to some companies, as Enron’s internal audit is facing risks represented in its incapability to perform required job and cannot achieve the IIA goal of internal audit functions to add value to companies.

Internal audit has its own cause-and-effect factors, which, in our opinion, should be divided into two areas:

Operational (daily) problems of internal audit based on the main activity of the organization;

Striving to meet the needs of organizations and different types of stakeholders (public).

Figure 3 represents the cause-and-effect factors of internal audit.

Figure 3 represents the cause-and-effect factors of internal audit.

Along with solving the operational problems of internal audit, it also involves solving the problems of meeting the basic economic needs of the public. This leads to the development of the economic system, economic growth, and increased improvement of the efficiency of production and economic activities through the development of small and medium-sized businesses and increasing their profitability.

Currently, an internal audit represents an independent service department in the company which is used for verification and evaluation of the results of the business activities in the interests of its stakeholders. Internal audit is widespread worldwide in medium and large-size organizations, most companies with a complex management structure. The presence of an internal audit service increases the confidence of external auditors and other stakeholders in the companies’ reporting.

Studying and analysing the main scientific approaches to understanding the essence of internal audit, we can conclude that internal audit is an integral element of multinational companies and medium-sized organizations that care about the achievements of their strategic goals and objectives in an efficient way. There is still a kind of reserve and potential for production opportunities, economic growth, innovation and competitiveness of the country’s economy if more organisations will introduce internal audit function with their organisational structure. Internal audit can be implemented through variable organisational forms and structures and is focused both on meeting public needs and on solving problems of particular organisations.

Today’s companies, especially Kazakhstan companies, pay attention more to risk management, governance, and control processes. Being no longer a part or continuation of the accounting profession or a branch of information technology, nowadays, internal auditing has become a thrilling and interdisciplinary profession. Internal auditors should perform various works such as risk management and consulting services. Reviewing the internal controls and business processes, they should have a deep understanding of business, not just monitor compliance with the legislation, governing the financial and economic activities, accounting, preparing for financial statements or just delivering the objective information to all interested parties.

Expert knowledge in accounting and information systems is unnecessary for the internal audit work; the main is the understanding of business processes and their risk. A value-added approach is possible when the internal auditors are flexible in their assignments and when the management is ready to accept these new roles.

Today, all internal auditors need to have logical and critical thinking, possess business-related skills, research ability and flexibility. Additionally, to be on the same level with the business development internal auditors need to have high technical skills and be smarter than employees of the company. Auditors should be one step ahead and see the full picture. Only then, they will be able to provide strong feedback and be independent. The internal audit department provides consultation on the financial report and other types of reports (management, business activities reports).

Auditing is now strictly regulated, especially in developed market countries. The Council of the European Communities has issued a number of directives that define both the composition and structure of companies’ reporting and the procedure for internal audits. Moreover, the directives also provide strict qualified requirements for auditors.

In Kazakhstan, the accounting and auditing legal basis is developed based on the requirements of the Constitution, Civil Code, Code of Administrative Offenses, Tax Code, Laws “On Bankruptcy”, “On JointStock Companies”, “On Foreign Investments”, and other Republic of Kazakhstan’s regulatory acts that govern the activities of companies, firms, and other commercial organizations.

During the V Audit Conference that took place in Almaty on March 16, 2000, International Audit Standards in Kazakhstan were adopted. International Auditing Practices Committee published the regulatory documents on International Standards on Auditing and Standards on the related services (Boolaky & Soobaroyen, 2017).

According to Articles 33 and 61 of the Law of the Republic of Kazakhstan “On Joint-Stock Companies”, the company can set up an internal audit department with a minimum of three members. However, for the joint-stock company it is mandatory to have an internal audit function. The internal audit is directly accountable to the board of directors of the company, and the board of directors can be convened at the request of the internal audit service of the company (Yurist, 2003).

Nevertheless, for small and medium enterprises there are no clear instructions for establishing internal audit departments. The management can decide what type of department, quantity of people, composition, level of competence, almost the full freedom in the decision (Russell, 2007).

Modern internal audit is capable to perform diverse and ambitious tasks. The result of the activities of the internal audit service should be an objective and independent assessment on issues related to the competence of internal audit, expressed in any kind form of reports, which can include information about:

- the effectiveness of the internal control environment, information and communications, monitoring;

- the efficiency of the company’s divisions in terms of completing the goals;

- the description of risks associated with the projects being implemented;

- the safety and liquidity of companies;

- the reliability of the reporting provided;

- the efficiency of the business and the state of the company reputation.

In Kazakhstan, internal audit is mostly associated with control and inspection work. There is no complete and systematic solution. The changing process in the internal audit is slow in Kazakhstan. It is necessary to improve the theory base of internal audit to solve problems at the present stage of its formation.

The development of internal audit in Kazakhstan is seriously slowed up by the lack of available information, the lack of interest of stakeholders in internal audit. Another problem is the lack of adapted certification for internal auditors. The internal auditor must have the obligatory presence of an “auditor” qualification certificate obtained under the Law of the Republic of Kazakhstan “On Auditing”, or a CIA (Certified Internal Auditor) certificate in the field of internal audit, or an ACCA (Association of Certified Chartered Accountants ), or a Diploma of DipIFR (Diploma in International Financial Reporting), or a certificate of an international professional accountant CIPA (Certified International Professional Accountant), or a certificate of a professional accountant obtained under the Law of the Republic of Kazakhstan “On accounting and financial reporting”. However, for the majority of Kazakhstani internal auditors, such qualification certificates are unavailable, because training is conducted mainly in English.

The performance gap in the internal audit functions arises due to a lack of clarity of vision in terms of its role in the companies (member of the board of directors versus management board), the function of internal audit (assurance versus consulting), the financial or accounting skills and experiences of the internal auditors and their membership in the IIA, and the extent to which the internal auditors perform in respect of the standards that regulate the profession of internal audit (Christopher, 2019).

The current internal audit system is characterized by a lack of integrity and consistency. The existing internal audit in local companies does not provide an increase in efficiency and effectiveness. It is not aimed at preventing violations and deficiencies.

International best practice indicates that internal audit needs to be focused on “getting ahead” of events and processes. Internal audit should be comprehensive, penetrating and permeating the business processes both vertically and horizontally. In the activities of internal audit, restrictions, and conflicts of interest can lead to violations of the principles of internal audit, negative audit results are strictly prohibited.

Additional key problem of internal audit is the insufficient level of theoretical and practical professional training of the personnel of the entire internal audit system, which is aggravated by the weak financial and resource support of internal audit. Also, as it was mentioned above, most professional certifications are provided in English. Kazakhstan has a problem with training and proficiency in English.

As a result, there are a lot of problems associated with the implementation of low-quality internal audit, which is carried out by low-skilled employees of the internal audit department. At the same time, it is advisable to approve the advanced training plan annually, considering innovations on a wide range of issues that are relevant, useful, and significant for a particular company, and are also necessary for the successful performance of internal audit employees of their duties, including improving the knowledge of the English languages.

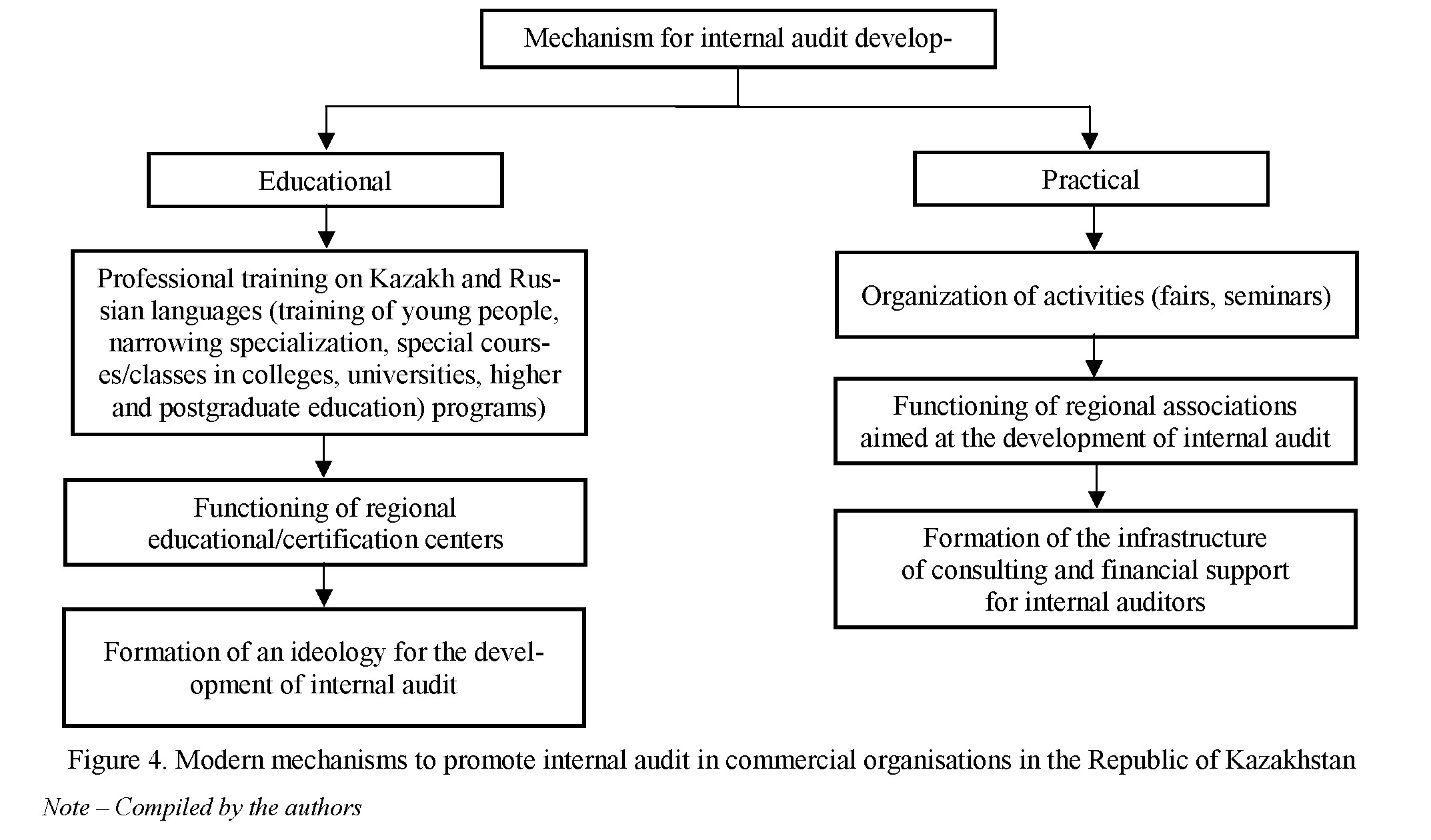

Mechanisms for promoting internal audit development in the Republic of Kazakhstan can be divided into two broad areas:

Educational mechanism for the formation of internal audit;

Practical mechanism focused on internal audit practice in the organisations.

For the development of internal audit from a theoretical point of view, a special role is assigned to “educational centers”. These education centers are specialized places in which mediation is carried out between professional internal auditors with high qualifications and employed/hired internal auditors in different types of organisations.

The leading element of the educational mechanisms for the development of internal audit in the Republic of Kazakhstan, according to Figure 4, is the training of professional personnel in Kazakh and Russian

147

languages (training of young people, narrowing specialization, special courses/classes in colleges, universities, higher and postgraduate education).

Along with the educational mechanisms for ensuring internal audit development, in the Republic of Kazakhstan, the formation of mechanisms focused on the practical point of view in business entrepreneurship is considered a strategic direction. These mechanisms provide for:

organization of activities in the form of fairs, seminars, webinars;

functioning of regional associations aimed at the development of internal audit in Kazakhstan cities and towns;

formation of the infrastructure of consulting internal auditors on topical issues and even financial support for internal auditors for education purposes (sponsorship).

The International Institute of Internal Audit describes the essence of internal audit as a process that helps prevent fraud, gives an assurance that organization works effectively and wants to reach its goals and objectives that will only improve the business activity in the future. Internal audit combines all. It is like a system, a tool that helps to increase efficiency of business processes, starting from the financial side and ending with the corporate governance. The role of internal audit is to review the company’s internal practices and procedures to ensure that its goals and objectives are being met. Internal audit is a part of the company itself, but, at the same time, the internal audit department must maintain its independence, subordination, and accountability directly to the head of the company.

Improving the current situation with internal audit in Kazakhstan will give only positive sides for the organisations and economy of the whole country. The development of internal audit will be facilitated by the process of integrating the interests of educational institutions, organizations, stakeholders (the public) and public authorities, which will achieve a synergistic effect.

From the above analysis, it can be seen that most Kazakhstani commercial organizations can learn from each other how to use the full set of internal audit functions and can borrow the experience of foreign companies and their practices from internal audit functions and usage. To make this possible, a lot of parties should be involved, including society institutions, public and state organizations with collaboration of not- for-profit organizations and internal auditors themselves. There are problems arising from incomplete use of internal audit functionality among Kazakhstani organizations. The measures provided in the article can contribute and help to develop internal audit in Kazakhstan and take it to the next level.

References

- Abenova, M.H. (2017). Vnutrennii audit kak samostoiatelnaia funktsiia upravleniia kompaniei [Internal audit as an independent function of company management]. Voprosy ekonomiki i upravleniia — Economics and management issues, 1.1 (8.1), 7–9 [in Russian].

- Al-Twaijry, A.A., Brierley, J.A., & Gwilliam, D. (2003). The development of internal audit in Saudi Arabia: an institutional theory perspective. Critical Perspectives on Accounting, 14(5), 507–531.

- Arena, M., Arnaboldi, M., & Azzone, G. (2010). The organizational dynamics of enterprise risk management. Accounting, Organizations and Society, 35(7), 659–675.

- Beasley, M.S., Clune, R., & Hermanson, D.R. (2005). Enterprise Risk Management: An Empirical Analysis of Factors Associated With the Extent of Implementation. Journal of Accounting and Public Policy, 24(6), 521–531.

- Boolaky, P., & Soobaroyen, T. (2017). Adoption of International Standards on Auditing (ISA): do institutional factors matter? International Journal of Auditing, 21 (1), 59–81.

- Carey, P., Subramaniam, N., & Ching, K.C. (2006). Internal Audit Outsourcing in Australia. Accounting & Finance, 46(1), 11–30.

- Chambers, R.F. (2014). Lessons Learned on the AUDIT TRAIL. The Institute of Internal Auditors Research Foundation.

- Christopher, J. (2019). The failure of internal audit: Monitoring gaps and a case for a new focus. Journal of Management Inquiry, 28(4), 472–483.

- De Zwaan, L., Stewart, J., & Subramaniam, N. (2011). Internal audit involvement in enterprise risk management. Managerial Auditing Journal, 586–604.

- Deloitte (2018). Forging Internal Audit’s path to greater impact and influence. Deloitte.

- Gordon, L.A., Loeb, M.P., & Tseng, C.Y. (2009). Enterprise risk management and firm performance: A contingency perspective. Journal of Accounting and Public Policy, 28(4), 301–327.

- Gramling, A.A., Maletta, M.J., Schneider, A., & Church, B.K. (2004). The role of the internal audit function in corporate governance: A synthesis of the extant internal auditing literature and directions for future research. Journal of Accounting literature, 23, 194.

- Hazaea, S.A., Tabash, M.I., Khatib, S.F., Zhu, J., & Al-Kuhali, A.A. (2020). The Impact of Internal Audit Quality on Financial Performance of Yemeni Commercial Banks: An Empirical Investigation. The Journal of Asian Finance, Economics and Business, 7(11), 867–875.

- Kryshkin, O. (2017). Nastolnaia kniga po vnutrennemu auditu: Riski i biznes-protsessy [The Handbook of Internal Auditing: Risks and Business Processes]. Moscow: Alpina Pablisher [in Russian].

- Lenz, R., & Hahn, U. (2015). A synthesis of the empirical internal audit effectiveness literature and new research opportunities. Managerial Auditing Journal.

- McNamee, D., & McNamee, T. (1995). The transformation of internal auditing. Managerial Auditing Journal.

- Parkinson, M. (1999). Presenter at the Institute of Internal Auditors Educators Symposium, 20 October. Sydney, Australia.

- Plisova, A.B. (2017). Vnutrennii kontrol i audit dostupnosti i potokov debitorskoi zadolzhennosti [Internal control and audit of availability and flows of accounts receivable]. Upravlenie ekonomicheskimi sistemami: nauchnyi elektronnyi zhurnal — Management of economic systems: scientific electronic journal, 1(95), 1–9 [in Russian].

- Roussy, M. (2013). Internal auditors’ roles: From watchdogs to helpers and protectors of the top manager. Critical Perspectives on Accounting, 24(7-8), 550–571.

- Russell, J.P. (2007). The Internal Auditing Pocket Guide: Preparing, performing, reporting and follow-up. Quality Press.

- Spira, L.F., & Page, M. (2003). Risk management: The reinvention of internal control and the changing role of internal audit. Accounting, Auditing & Accountability Journal, 16(4), 640–661.

- The Institute of Internal Auditors Kazakhstan (n.d.). The Institute of Internal Auditors Kazakhstan. institutes.theiia.org. Retrieved from https://institutes.theiia.org/sites/kazakhstan/about/Pages/default.aspx

- The Institute of internal auditors. (2004). Definition of Internal Auditing. Retrieved from The Institute of internal auditors. na.theiia.org. https://na.theiia.org/standards-guidance/mandatory-guidance/Pages/Definition-of-Internal- Auditing.aspx

- Yurist (2003). Zakon Respubliki Kazakhstan ot 13 maia 2003 goda № 415-II “Ob aktsionernykh obshchestvakh” (s izmeneniiami i dopolneniiami po sostoianiiu na 08.01.2022 g.) [Law of Republic of Kazakhstan of 13 May 2003 N 415-II “On Joint-Stock Companies” (as amended as of 08.01.2022)]. online.zakon.kz. https://online.zakon.kz/Document/?doc_id=1039594#pos=5;- 106&sdoc_params=text%3D%25D0%25B2%25D0%25BD%25D1%2583%25D1%2582%25D1%2580%25D0%25 B5%25D0%25BD%25D0%25BD%25D0%25B5%26mode%3Dindoc%26topic_id%3D1039594%26spos%3D1%2 6tSynonym%3D1%26tShort%3D1%26tSuffix% [in Russian].